Bio-based Polymers Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

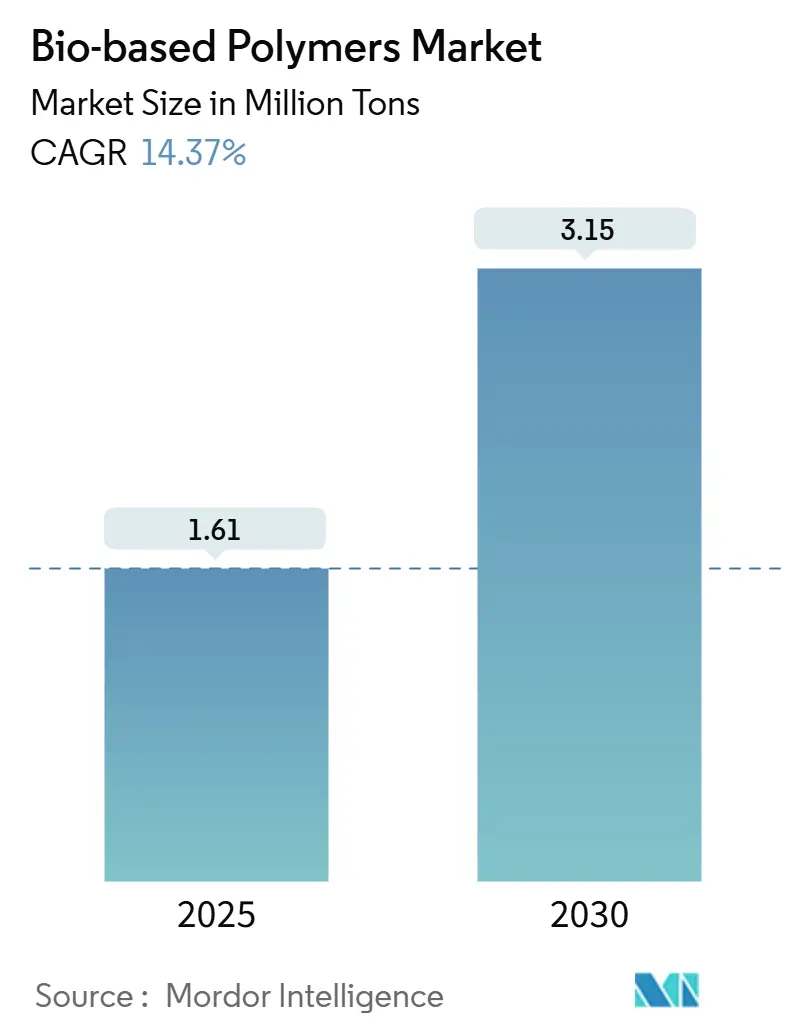

| Market Volume (2025) | 1.61 Million tons |

| Market Volume (2030) | 3.15 Million tons |

| Growth Rate (2025 - 2030) | 14.37% CAGR |

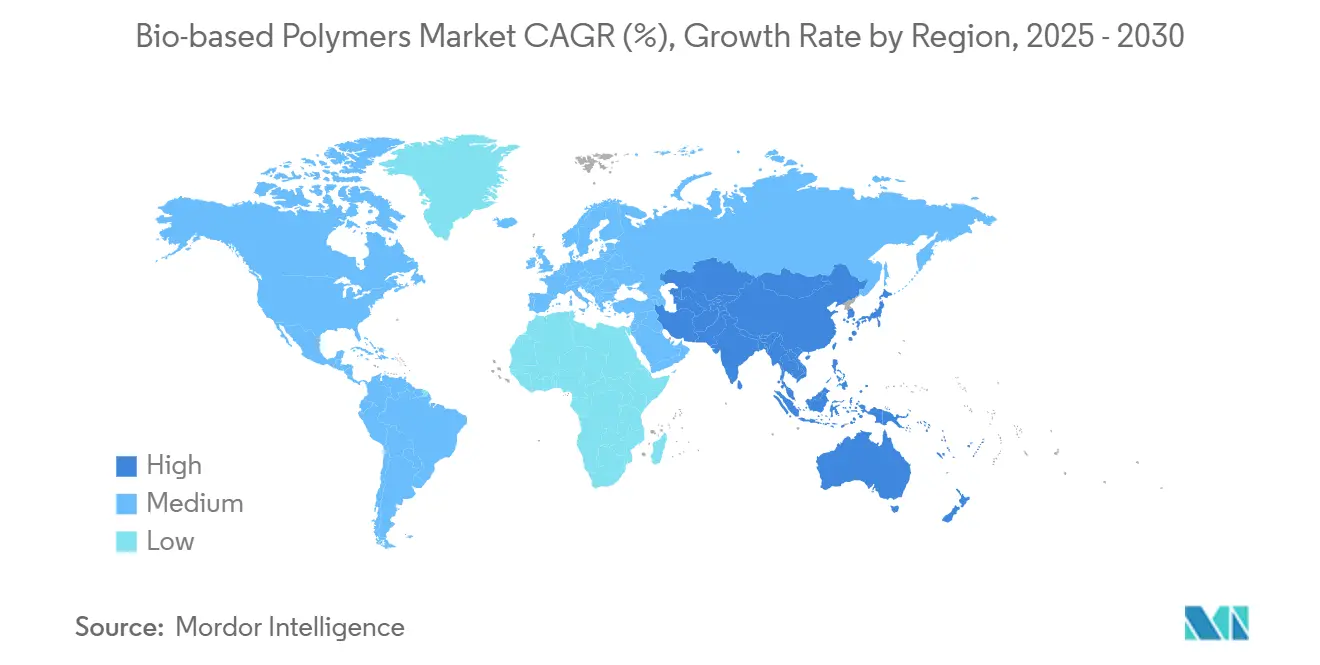

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Bio-based Polymers Market Analysis by Mordor Intelligence

The Bio-based Polymers Market size is estimated at 1.61 million tons in 2025, and is expected to reach 3.15 million tons by 2030, at a CAGR of 14.37% during the forecast period (2025-2030). The sharp expansion comes from mandatory single-use plastic bans, fast-maturing bio-refinery technologies, and mass-balance certification that allows drop-in resins to flow through existing assets. Producers lock in long-term offtake agreements with global brands pursuing net-zero timelines, giving financiers visibility to support new capacity. Regionally, Asia-Pacific captures much of the incremental tonnage because agricultural residues supply low-cost feedstock and local policies encourage renewable materials. Premium segments open in medical, automotive, and electronics as improved heat resistance and biocompatibility formulations move bio-based polymers beyond commodity packaging.

Key Report Takeaways

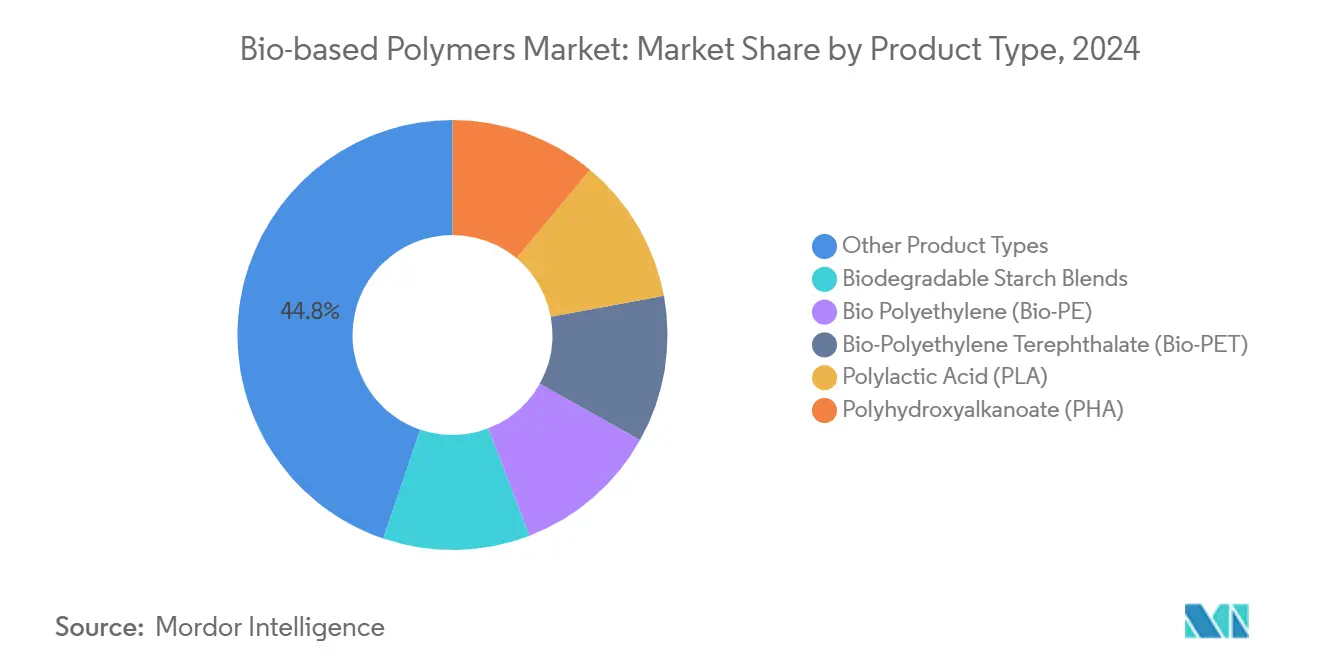

- By product type, polybutylene succinate and polybutylene adipate terephthalate held 44.78% of bio-based polymers market share in 2024. Polylactic acid is projected to expand at an 18.50% CAGR through 2030.

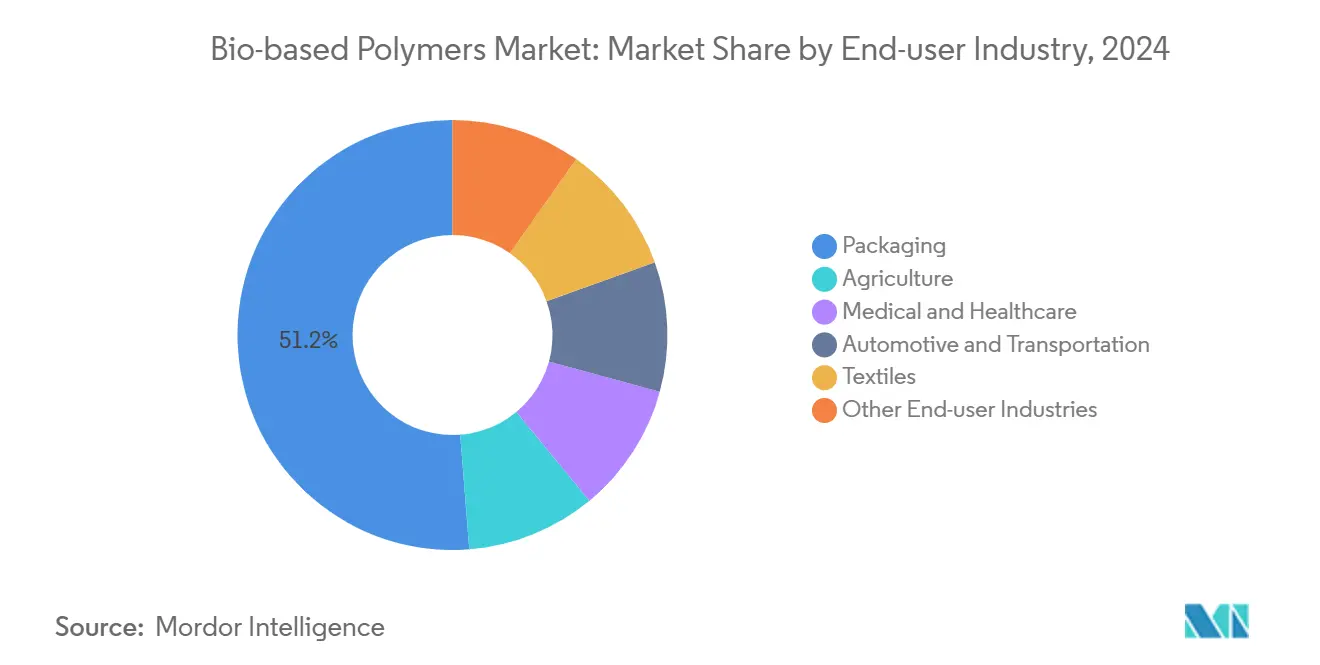

- By end-user, packaging led with a 51.22% revenue share in 2024 and is advancing at a 17.72% CAGR to 2030.

- By geography, Asia-Pacific accounted for 44.45% of the bio-based polymers market size in 2024 while recording the highest regional CAGR at 16.88% through 2030.

Global Bio-based Polymers Market Trends and Insights

Driver Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulation-led bans on single-use plastics | +3.2% | Global, with early implementation in EU, Canada, Australia | Short term (≤ 2 years) |

| Rising consumer demand for sustainable materials | + 2.8% | North America and EU core, expanding to APAC urban centers | Medium term (2-4 years) |

| Corporate net-zero and renewable-carbon sourcing pledges | +1.9% | Global, concentrated in multinational corporations | Medium term (2-4 years) |

| Mass-balance certified drop-in resins adoption | +0.8% | North America and EU, with APAC following | Short term (≤ 2 years) |

| Scale-up of CO₂- and agri-waste-based biorefineries | +1.2% | APAC core, with expansion to Americas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulation-led Bans on Single-use Plastics

Australia widened its plastics prohibition in 2024 to ban heavyweight shopping bags and polystyrene food containers, pushing retailers toward certified compostable options[1]Australian Department of Climate Change, “Single-use Plastics,” dcceew.gov.au. The European Union now enforces extended producer responsibility that prices end-of-life costs into each package, narrowing the cost gap with the bio-based polymers market[2]European Commission, “Circular Economy Action Plan,” ec.europa.eu. Canada implemented a federal plastics prohibition in late 2024, creating a contiguous North American market for renewable packaging. China tightened domestic restrictions after banning waste plastic imports, forcing local converters to source compliant materials. Early adopters show that once bans enter force, demand shifts quickly because compliance risk outweighs price premiums.

Rising Consumer Demand for Sustainable Materials

Global surveys show that 73% of shoppers weigh sustainability claims in purchase decisions and will pay 15-20% more for verified renewable content. Brand owners translate this signal into procurement rules that favor mass-balance certified feedstocks, protecting margins in the bio-based polymers market. Food service chains swap conventional coatings for compostable films to meet customer expectations on waste reduction. B2B buyers embed carbon intensity scores in supplier scorecards, raising entry barriers for fossil plastics. The demand pull spreads to electronics and apparel as lifestyle brands position renewable materials as a marker of quality.

Corporate Net-zero and Renewable-carbon Sourcing Pledges

Major consumer-goods groups publicly link packaging portfolios to science-based targets, allocating fixed tonnages to renewable carbon. Multi-year offtake contracts lower counter-party risk and unlock project finance for greenfield plants. Carbon accounting frameworks such as the Science Based Targets initiative accept certified bio-based content as valid Scope 3 abatement, converting polymers from a cost line to a decarbonization lever. Producers design dashboards that feed chain-of-custody data directly into customer ESG reports, reducing audit friction. The result is predictable baseline demand that tempers cyclical swings, strengthening the long-run outlook for the bio-based polymers market.

Scale-up of CO₂- and Agri-waste-based Biorefineries

Braskem’s bagasse-based ethylene line targets 200,000 tons annual capacity by 2025 and validates residue-to-polymer economics. Similar concepts arise in Thailand, India, and Brazil where integrated sugar and starch complexes supply low-cost feedstock. Pilot plants convert captured flue-gas CO₂ into polyols, situating capacity near renewable power sources to cut emission factors. Waste-based routes avoid food-versus-fuel debates while earning carbon credits, which widen the margin over petrochemical incumbents. Location flexibility allows regional clusters to balance feedstock, energy, and logistics, reinforcing Asia-Pacific dominance in the bio-based polymers market.

Restraint Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher cost vs. petro-plastics | -1.5% | Global, most pronounced in price-sensitive applications | Medium term (2-4 years) |

| Limited composting and recycling infrastructure | -1.1% | Global, with infrastructure gaps in developing regions | Long term (≥ 4 years) |

| Feedstock price volatility from biofuel mandates | -0.8% | Americas and EU, regions with biofuel mandate policies | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Higher Cost vs. Petro-plastics

Bio-based grades sell at 20-50% premiums compared with fossil alternatives because smaller plants lack scale efficiencies. Production costs ease when plants share utilities with existing chemical hubs, yet capital intensity delays parity. Price spikes in crude oil narrow the gap temporarily but do not erase structural differences. Specialty uses such as medical devices absorb premiums because biodegradability trims regulatory burdens. Broader parity depends on doubling current capacity so fixed costs spread across more tons.

Limited Composting and Recycling Infrastructure

The United States runs fewer than 5,000 industrial composting sites, far short of volumes implied by nationwide adoption of compostable packaging. Europe fares better but still faces uneven municipal collection rules that confuse consumers. When biodegradable items enter mechanical recycling streams they downgrade resin quality, prompting reclaimers to oppose mixed-waste systems. Municipalities hesitate to fund new plants until throughput is assured, while converters need infrastructure to justify switching. This chicken-and-egg dynamic slows growth even when consumer demand exists.

Segment Analysis

By Product Type: Specialty Polymers Drive Innovation

Other product types, dominated by polybutylene succinate and polybutylene adipate terephthalate, accounted for 44.78% of bio-based polymers market share in 2024. Producers win adoption in mulch films and flexible pouches because these resins combine compostability with heat-seal strength. Their large base lifts the overall bio-based polymers market size for specialty grades and supports incremental debottlenecking projects. Supply security improves as Asian firms integrate succinic acid and adipic acid back to local feedstock, trimming freight and currency risk.

Polylactic acid leads growth at an 18.50% CAGR to 2030. The segment benefits from recent heat-stable grades that unlock electronics housings and automotive trim. Medical innovators exploit PLA’s bioresorption to design screws and plates that dissolve after healing, avoiding secondary surgeries. Capacity expansions in the UAE and Thailand add scale and lower cost floors, which enlarges the bio-based polymers market size for PLA applications. Competitive intensity rises as new entrants license technology that had been confined to one or two players.

Note: Segment shares of all individual segments available upon report purchase

By End-user Industry: Packaging Dominance Accelerates

Packaging retained a 51.22% stake of bio-based polymers market share in 2024 and is forecast to grow 17.72% a year to 2030. Food service operators rush to replace expanded polystyrene clamshells and thin plastic carry-outs because fines hit margins under new bans. Flexible snack films now blend PBAT with PLA to reach home-compostable thresholds, extending shelf life while meeting labeling laws. E-commerce brands pilot cushioning foams that biodegrade in ambient soil, cutting return-pack waste volumes.

Medical and healthcare segments are growing as implantable devices shift to resorbable polymers that eliminate removal surgeries. Controlled-release capsules exploit bio-polyester matrices to achieve precise dissolution without microplastic residue. The automotive cabin adopts renewable fabrics and trim inserts to lift life-cycle assessment scores, especially in electric vehicles where every gram of embedded carbon counts. Agriculture uses mulch films that plow into the soil, sparing farmers the retrieval costs and enriching organic content. Collectively, these shifts broaden revenue pools and reduce reliance on any single end-use within the bio-based polymers market.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Asia-Pacific captured 44.45% of the bio-based polymers market size in 2024 and is expanding at a 16.88% CAGR to 2030. China anchors regional leadership through tax rebates, green loans, and integrated corn-to-polymer complexes run by COFCO and peers. Thailand grants eight-year tax holidays on bio-chemical investments, luring joint ventures that colocate sugar mills with polymer units. India leverages surplus bagasse to backfill domestic polymer demand while exporting credits to multinationals.

Europe supports demand with a mature policy mix that combines the Single-Use Plastics Directive and mandatory extended producer responsibility. Germany and France internalize collection fees that make fossil plastics relatively more expensive, steering converters toward certified compostables. Industrial composting coverage surpasses 3,500 sites, enabling true circularity claims. Regional offtake agreements let suppliers lock multi-year prices, stabilizing the bio-based polymers market against feedstock swings.

North America accelerates through state-level laws such as California’s SB 54 that requires a 65% cut in single-use plastic packaging by 2032. Canada’s federal ban synchronizes product specifications across provinces, creating a continental platform for investment. Corporate buyers formalize renewable-carbon quotas in supplier contracts, delivering predictable tonnage. Elsewhere, emerging Latin American sugar economies and selected African nations replicate policy templates that fast-track adoption where agricultural residues are plentiful.

Competitive Landscape

The bio-based polymers market remains moderately fragmented because production technologies vary by feedstock and application. Integrated petrochemical majors such as BASF secure ISCC PLUS certification across large resin families, using existing logistics to flood global channels. Collaborations proliferate between polymer producers and brand owners to co-create grades that slot into end-use tooling without capital upgrades. Patent filings rise in catalyst engineering and fermentation yield, signaling an innovation race. Mergers remain selective; firms prefer supply alliances to outright takeovers due to divergent technology stacks. Competitive differentiation tilts toward verifiable carbon accounting, prompting laggards to scramble for certification.

Bio-based Polymers Industry Leaders

-

BASF

-

Braskem

-

Corbion

-

NatureWorks LLC

-

Novamont S.p.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Ukhi India Pvt. Ltd. launched EcoGran at Vigyan Bhawan during World Environment Day, a home-compostable biopolymer made from hemp, flax, and stubble waste.

- December 2024: Emirates Biotech selected Sulzer technology to build the world’s largest PLA plant in the UAE, with operations slated for early 2028.

Global Bio-based Polymers Market Report Scope

Bio-based materials are derived from plants and are biodegradable. Similarly, bio-based polymers are also derived from plants such as corn, sugarcane, vegetable oil, soybeans, cellulose, and others. These polymers are also known as next-generation polymers, which are used to reduce the use of fossil fuels. Cellulose and starch were the first bio-based polymers invented and used in textiles, packaging construction, and other applications. The bio-based polymers market is segmented by type, application, and geography (Asia-Pacific, North America, Europe, and the rest of the world). By type, the market is segmented into starch-based plastics, polylactic acid, polyhydroxy alkanoates, polyesters, and cellulose derivatives. By application, the market is segmented into agriculture, textiles, electronics, packaging, healthcare, and other applications. The report also covers the market size and forecasts for the bio-based polymers market in 13 countries across major regions. The report offers market sizes and forecasts for each segment based on volume (tons).

| Biodegradable Starch Blends |

| Bio Polyethylene (Bio-PE) |

| Bio-Polyethylene Terephthalate (Bio-PET) |

| Polylactic Acid (PLA) |

| Polyhydroxyalkanoate (PHA) |

| Other Product Types (Polybutylene Succinate (PBS), Polybutylene Adipate Terephthalate (PBAT), etc.) |

| Agriculture |

| Medical and Healthcare |

| Packaging |

| Automotive and Transportation |

| Textiles |

| Other End-user Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Rest of the World | South America |

| Middle East and Africa |

| By Product Type | Biodegradable Starch Blends | |

| Bio Polyethylene (Bio-PE) | ||

| Bio-Polyethylene Terephthalate (Bio-PET) | ||

| Polylactic Acid (PLA) | ||

| Polyhydroxyalkanoate (PHA) | ||

| Other Product Types (Polybutylene Succinate (PBS), Polybutylene Adipate Terephthalate (PBAT), etc.) | ||

| By End-user Industry | Agriculture | |

| Medical and Healthcare | ||

| Packaging | ||

| Automotive and Transportation | ||

| Textiles | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Rest of the World | South America | |

| Middle East and Africa | ||

Key Questions Answered in the Report

How large is the bio-based polymers market in 2025?

The bio-based polymers market size is 1.61 million tons in 2025.

What CAGR is expected for bio-based polymers through 2030?

Volume is forecast to grow at 14.37% a year between 2025 and 2030.

Which region leads in demand for bio-based polymers?

Asia-Pacific holds 44.45% of global volume and posts the fastest 16.88% CAGR.

Which product category is expanding fastest?

Polylactic acid records the highest 18.50% CAGR to 2030.

Why is packaging the largest application?

Regulatory bans and consumer preference push packaging to 51.22% share and 17.72% CAGR.

What limits wider use of bio-based plastics?

Price premiums and insufficient composting infrastructure remain the main barriers.

Page last updated on: