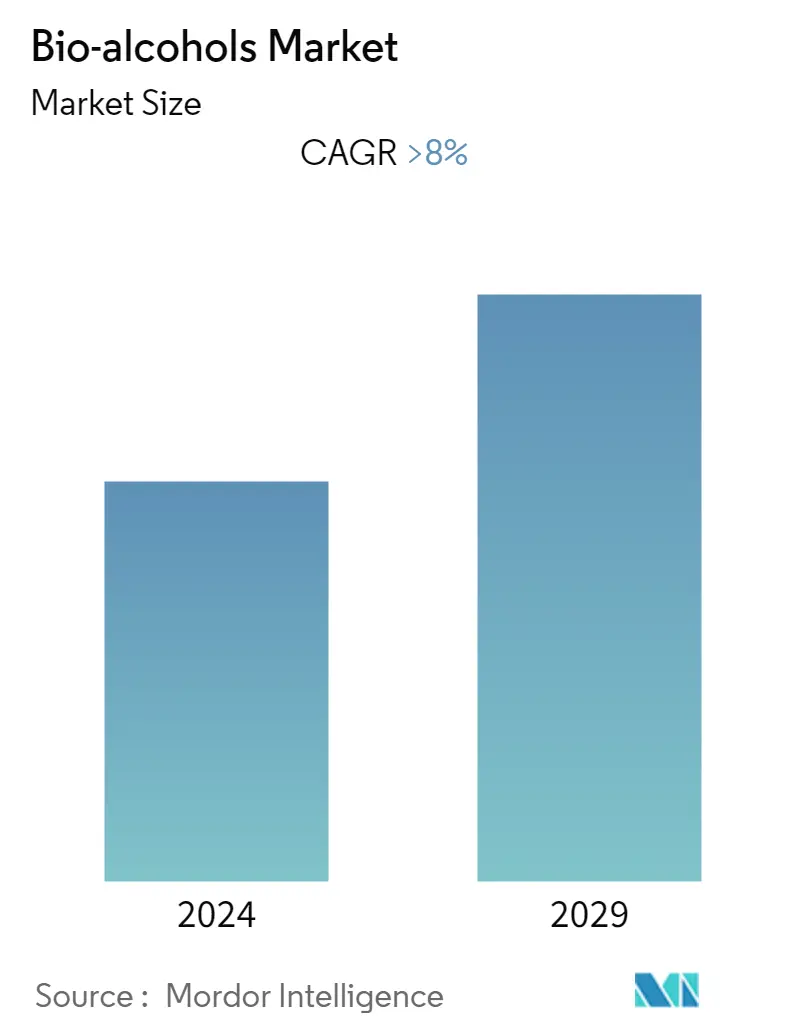

Bio-Alcohol Market Size

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

| Forecast Data Period | 2024 - 2029 |

| CAGR | > 8.00 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

Bio-Alcohol Market Analysis

The global bio-alcohols market is expected to grow with a CAGR greater than 8% during the forecast period. One of the major factors driving the market is the growing growing demand for bio-based products. However, the declining automotive production is hindering the growth of the market studied.

- Asia-Pacific is expected to account for the highest growth rate during the forecast period.

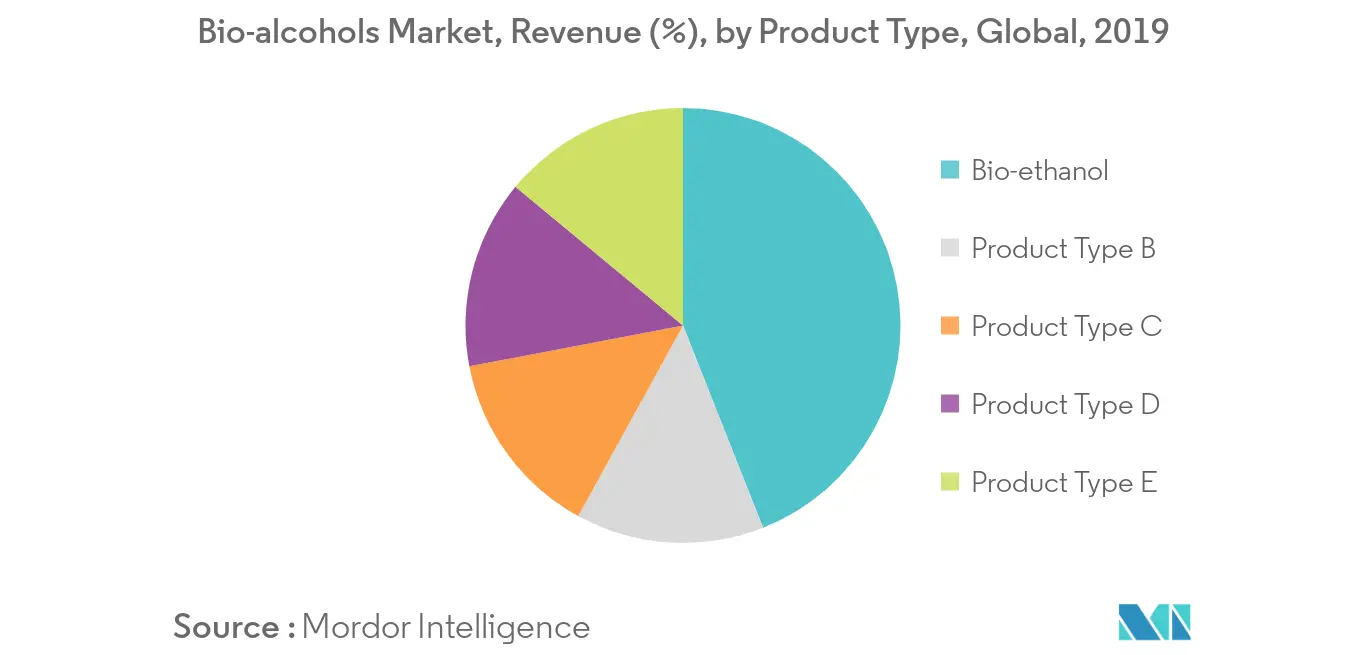

- Among the product types, bio-ethanol is likely to account for the highest market share during the forecast period.

Bio-Alcohol Market Trends

This section covers the major market trends shaping the Bio-Alcohols Market according to our research experts:

Bio-ethanol to Dominate the Market

- Bio-ethanol offers higher-octane fuel alternative and is also used for energy oriented applications, such as power generation.

- Its applications in trucks, buses, airplanes, medical industry, and fuel cells are to lift the growth in the market.

- The blending of bio-ethanol with petrol can increase the life span of diminishing oil supplies and ensure greater fuel security globally.

- The demand for bio-ethanol is also boosted by its biodegradability and low toxicity than fossil fuels.

- Hence, owing to the above-mentioned factors, bio-ethanol is likely to dominate the market studied during the forecast period.

Asia-Pacific to Witness the Highest Growth Rate

- Asia Pacific region is expected to be the fastest-growing market for bio-alcohols owing to the ongoing growth in the end-user industries like construction, and electronics.

- The region has the presence of a large population and is witnessing a continuously growing demand for high-performance products with an increase in the income of the middle class.

- The countries in the region including China, India, and Indonesia are investing highly in the construction and infrastructure projects.

- However, the declining automotive industry may hinder the demand for bio-alcohols in the region in the coming years.

- Hence, owing to the above-mentioned factors, Asia-Pacific is likely to witness the highest growth rate during the forecast period.

Bio-Alcohol Industry Overview

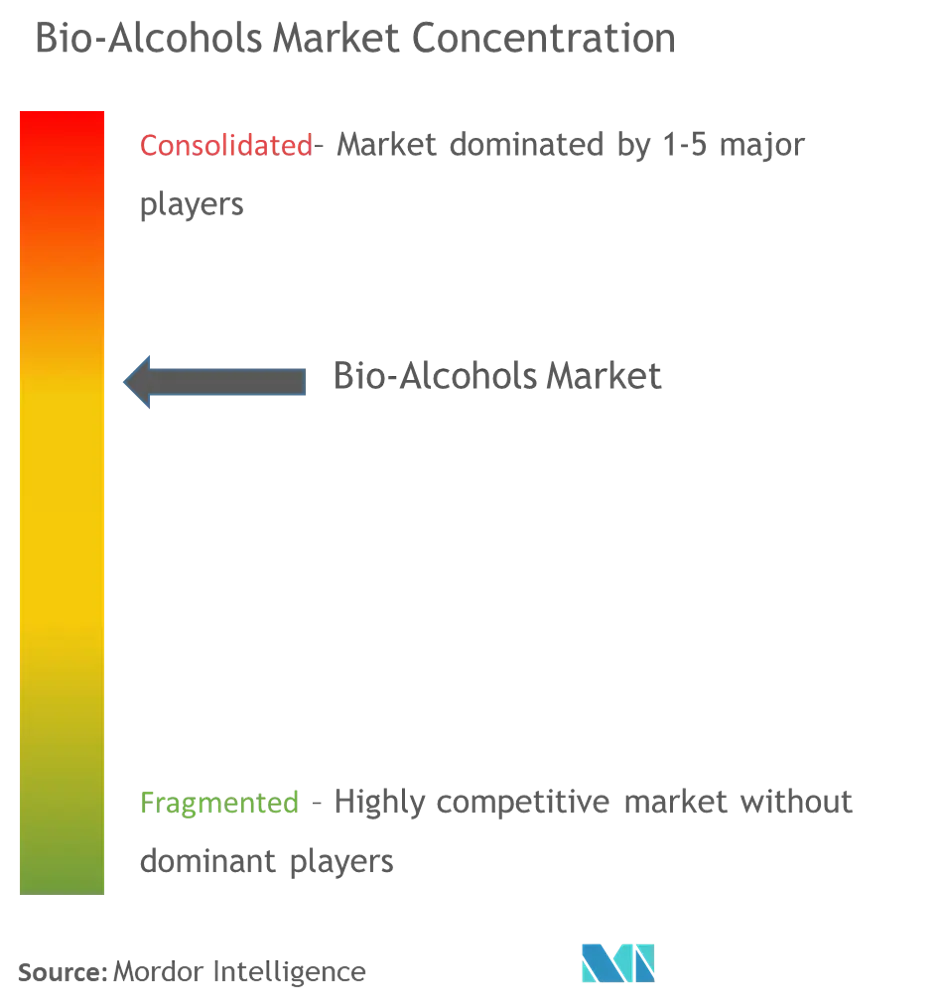

The global bio-alcohols market is moderately consolidated as the market of the market share is divided among few players. Some of the key players in the market include BASF SE, Asahi Kasei Corporation, INVISTA, Evonik Industries AG, and Toray Industries, Inc., among others.

Bio-Alcohol Market Leaders

BASF SE

Asahi Kasei Corporation

INVISTA

Evonik Industries AG

Toray Industries, Inc.

*Disclaimer: Major Players sorted in no particular order

Bio-Alcohol Market Report - Table of Contents

-

1. INTRODUCTION

-

1.1 Study Assumptions

-

1.2 Scope of the Study

-

-

2. RESEARCH METHODOLOGY

-

3. EXECUTIVE SUMMARY

-

4. MARKET DYNAMICS

-

4.1 Drivers

-

4.1.1 Growing Demand for Bio-based Products

-

4.1.2 Other Drivers

-

-

4.2 Restraints

-

4.2.1 Declining Automotive Production

-

4.2.2 Impact of COVID-19 Pandemic

-

-

4.3 Industry Value-chain Analysis

-

4.4 Porter's Five Forces Analysis

-

4.4.1 Bargaining Power of Suppliers

-

4.4.2 Bargaining Power of Consumers

-

4.4.3 Threat of New Entrants

-

4.4.4 Threat of Substitute Products and Services

-

4.4.5 Degree of Competition

-

-

-

5. MARKET SEGMENTATION

-

5.1 Product Type

-

5.1.1 Bio-methanol

-

5.1.2 Bio-ethanol

-

5.1.3 Bio-butanol

-

5.1.4 Bio-BDO

-

5.1.5 Other Product Types

-

-

5.2 Application

-

5.2.1 Transportation

-

5.2.2 Construction

-

5.2.3 Electronics

-

5.2.4 Pharmaceutical

-

5.2.5 Other Applications

-

-

5.3 Geography

-

5.3.1 Asia-Pacific

-

5.3.1.1 China

-

5.3.1.2 India

-

5.3.1.3 Japan

-

5.3.1.4 South Korea

-

5.3.1.5 ASEAN Countries

-

5.3.1.6 Rest of Asia-Pacific

-

-

5.3.2 North America

-

5.3.2.1 United States

-

5.3.2.2 Canada

-

5.3.2.3 Mexico

-

-

5.3.3 Europe

-

5.3.3.1 Germany

-

5.3.3.2 United Kingdom

-

5.3.3.3 Italy

-

5.3.3.4 France

-

5.3.3.5 Rest of Europe

-

-

5.3.4 South America

-

5.3.4.1 Brazil

-

5.3.4.2 Argentina

-

5.3.4.3 Rest of South America

-

-

5.3.5 Middle-East and Africa

-

5.3.5.1 Saudi Arabia

-

5.3.5.2 South Africa

-

5.3.5.3 Rest of Middle-East and Africa

-

-

-

-

6. COMPETITIVE LANDSCAPE

-

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

-

6.2 Market Share/Ranking Analysis**

-

6.3 Strategies Adopted by Leading Players

-

6.4 Company Profiles

-

6.4.1 BASF SE

-

6.4.2 Braskem

-

6.4.3 Cargill, Incorporated.

-

6.4.4 DSM

-

6.4.5 Fulcrum BioEnergy

-

6.4.6 Harvest Power

-

6.4.7 Mascoma LLC

-

6.4.8 Mitsubishi Chemical Corporation

-

6.4.9 Valero Marketing and Supply Company.

-

6.4.10 Venture Center

-

- *List Not Exhaustive

-

-

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

Bio-Alcohol Industry Segmentation

The bio-alcohols market report includes:

| Product Type | |

| Bio-methanol | |

| Bio-ethanol | |

| Bio-butanol | |

| Bio-BDO | |

| Other Product Types |

| Application | |

| Transportation | |

| Construction | |

| Electronics | |

| Pharmaceutical | |

| Other Applications |

| Geography | ||||||||

| ||||||||

| ||||||||

| ||||||||

| ||||||||

|

Bio-Alcohol Market Research FAQs

What is the current Bio-alcohols Market size?

The Bio-alcohols Market is projected to register a CAGR of greater than 8% during the forecast period (2024-2029)

Who are the key players in Bio-alcohols Market?

BASF SE, Asahi Kasei Corporation, INVISTA, Evonik Industries AG and Toray Industries, Inc. are the major companies operating in the Bio-alcohols Market.

Which is the fastest growing region in Bio-alcohols Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2024-2029).

Which region has the biggest share in Bio-alcohols Market?

In 2024, the North America accounts for the largest market share in Bio-alcohols Market.

What years does this Bio-alcohols Market cover?

The report covers the Bio-alcohols Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the Bio-alcohols Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

Bio-Alcohol Industry Report

Statistics for the 2024 Bio-Alcohol market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. Bio-Alcohol analysis includes a market forecast outlook 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.

Bio-Alcohol Market Report Snapshots