Market Size of Beverage Caps And Closures Industry

| Study Period | 2019 - 2029 |

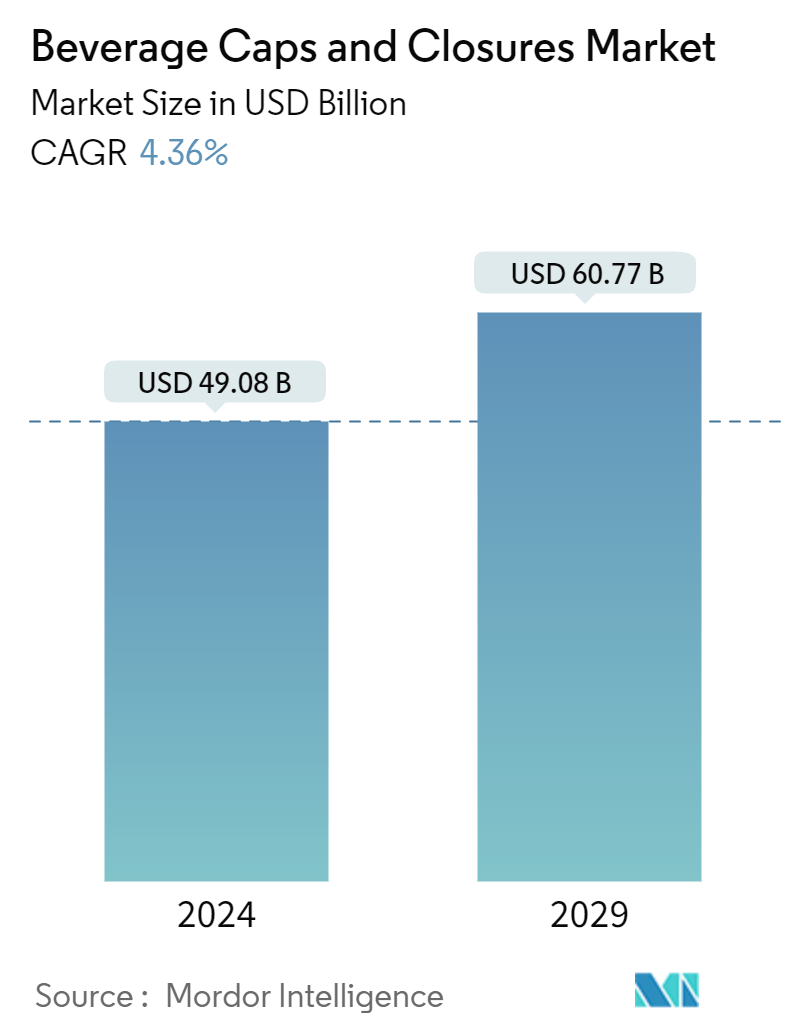

| Market Size (2024) | USD 49.08 Billion |

| Market Size (2029) | USD 60.77 Billion |

| CAGR (2024 - 2029) | 4.36 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players.webp)

*Disclaimer: Major Players sorted in no particular order |

Beverage Caps And Closures Market Analysis

The Beverage Caps And Closures Market size is estimated at USD 49.08 billion in 2024, and is expected to reach USD 60.77 billion by 2029, growing at a CAGR of 4.36% during the forecast period (2024-2029).

- Caps and closures are crucial in preventing beverage spillage and maintaining product freshness, regardless of the beverage type or packaging material. These components extend shelf life and protect against microbial contamination through tight seals. In the United States, the demand for plastic caps and closures is primarily driven by consumer preferences for convenience and ease of use. Plastic caps effectively shield products from contaminants and microorganisms. Additionally, plastic caps and closures offer a cost advantage over their metal counterparts.

- The global demand for caps and closures is increasing due to their ease of use and sustainable packaging qualities. PET and PP are the primary raw materials used in their manufacture. These components are extensively utilized in the beverage industry for both alcoholic and non-alcoholic products. Caps and closures serve multiple functions: they extend product shelf life, protect against contaminants and moisture, and regulate oxygen levels in packaged goods. As demand continues to rise, the market is expected to experience further growth during the forecast period.

- Bottled water is one of the fastest-growing beverage categories in terms of volume. This increasing consumer demand for bottled water is expected to drive the need for tamper-proof caps and closures during the forecast period. The growing awareness of health and wellness among consumers has shifted from sugary drinks to healthier alternatives, with bottled water being a primary beneficiary of this trend. Additionally, concerns about water quality in some regions have further boosted the demand for bottled water, necessitating robust packaging solutions.

- The modern consumer's "on-the-go" lifestyle has driven demand for lightweight, user-friendly packaging solutions. Custom caps and closures manufacturers are responding with lighter and more efficient designs. The global market growth is further propelled by increasing demand for various beverage types. These trends have led to packaging innovations, including recyclable materials and designs catering to e-commerce needs. The custom caps and closures market continues evolving, meeting consumer preferences and product requirements across diverse industries.

- Moreover, changes in lifestyle patterns and increased per capita consumption fuel the expansion of the bottled water market. Urbanization, busy lifestyles, and the convenience of bottled water have contributed to its popularity. As consumers increasingly opt for on-the-go hydration, manufacturers are responding by offering a variety of bottle sizes and innovative closure designs that ensure product safety and ease of use. This trend will likely continue, driving further growth in the tamper-proof caps and closures market for bottled water packaging.

- Technological advancements in plastic packaging have led to significant innovations in product development within the industry. Many companies invest heavily in research and development activities to create unique and cost-effective products, resulting in increased market innovations. However, the growing concern over climate change has led to stringent government regulations on plastic usage for packaging. These regulations are expected to be the primary constraint on the growth of the beverage caps and closures market during the forecast period.

Beverage Caps And Closures Industry Segmentation

Beverage caps and closures are vital in sealing a range of containers, from bottles and cans to cartons. These products preserve contents and prevent contamination, ensure product safety, and allow for easy opening and resealing. The market presents various caps and closures, differing in materials, designs, and sizes, tailored to various beverage types, packaging formats, and consumer preferences. While traditional options like screw caps and crown corks remain prevalent, the market also embraces innovations such as tamper-evident and child-resistant closures. The rising demand for these products can be attributed to their user-friendliness and sustainable packaging attributes. Widely utilized in both the alcoholic and non-alcoholic beverage sectors, caps and closures are instrumental in extending shelf life, safeguarding against dirt and moisture, and preserving optimal oxygen levels in packaged products.

The beverage caps and closures market is segmented by material (metal, plastic, other materials [rubber and cork]), by application (beer, wine, bottled water, carbonated soft drinks, dairy products, condiments, sauces, and other applications), and by geography (North America [United States, Canada], Europe [United Kingdom, Germany, France, Italy, and Rest of Europe], Asia-Pacific [China, Japan, India, and Rest of Asia-Pacific], Latin America [Brazil, Mexico, Colombia, and Rest of Latin America], Middle East And Africa [United Arab Emirates, Saudi Arabia, and Rest of Middle East and Africa]). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| By Material | |

| Metal | |

| Plastic | |

| Other Materials (Rubber, Cork) |

| By Application | |

| Beer | |

| Wine | |

| Bottled water | |

| Carbonated soft drinks | |

| Dairy products | |

| Condiments and sauces | |

| Other Applications |

| By Geography*** | |||||

| |||||

| |||||

| |||||

| Australia and New Zealand | |||||

| |||||

|

Beverage Caps And Closures Market Size Summary

The Beverage Caps and Closures Market is poised for growth, driven by the increasing demand for packaged beverages and advancements in packaging technology. Established beverage categories like milk and fruit juice are expected to experience slow growth, while newer categories such as sports drinks, ready-to-drink tea and coffee, and healthy alternatives are anticipated to boost demand for closures. However, stringent regulations on plastic bottle usage pose challenges to market expansion. Technological innovations in plastic packaging have led to significant product development, with companies investing in research and development to create unique and cost-effective solutions. This has resulted in new product offerings, such as FIJI Water's Sports Cap bottle and Dow Industries' PET resins portfolio, which are contributing to the market's growth.

The Asia Pacific region has demonstrated robust growth in the beverage industry, driven by rising disposable incomes and changing consumer preferences towards energy and nutritional drinks. The evolving middle class and workplace culture have increased alcohol consumption, further driving the demand for caps and closures in the region, particularly in countries like India and Taiwan. The market is highly competitive and fragmented, with major players like Amcor and Ball Corporation leading the market share. These companies are pursuing strategic collaborations, such as mergers and acquisitions, to expand their product offerings and geographical reach. The market landscape is characterized by the presence of both regional and international players, contributing to its dynamic nature.

Beverage Caps And Closures Market Size - Table of Contents

-

1. MARKET DYNAMICS

-

1.1 Market Drivers

-

1.1.1 Increasing Beverage Consumption in Developing Economies

-

1.1.2 Technological Advancements and Innovative Packaging Solutions

-

-

1.2 Market Restraints

-

1.2.1 Stringent Regulations on the Usage of Plastic caps and closures

-

-

-

2. MARKET SEGMENTATION

-

2.1 By Material

-

2.1.1 Metal

-

2.1.2 Plastic

-

2.1.3 Other Materials (Rubber, Cork)

-

-

2.2 By Application

-

2.2.1 Beer

-

2.2.2 Wine

-

2.2.3 Bottled water

-

2.2.4 Carbonated soft drinks

-

2.2.5 Dairy products

-

2.2.6 Condiments and sauces

-

2.2.7 Other Applications

-

-

2.3 By Geography***

-

2.3.1 North America

-

2.3.1.1 United States

-

2.3.1.2 Canada

-

-

2.3.2 Europe

-

2.3.2.1 Germany

-

2.3.2.2 United Kingdom

-

2.3.2.3 France

-

-

2.3.3 Asia-Pacific

-

2.3.3.1 China

-

2.3.3.2 Japan

-

2.3.3.3 India

-

-

2.3.4 Australia and New Zealand

-

2.3.5 Latin America

-

2.3.5.1 Brazil

-

2.3.5.2 Mexico

-

2.3.5.3 Colombia

-

-

2.3.6 Middle East and Africa

-

2.3.6.1 United Arab Emirates

-

2.3.6.2 Saudi Arabia

-

2.3.6.3 South Africa

-

-

-

Beverage Caps And Closures Market Size FAQs

How big is the Beverage Caps And Closures Market?

The Beverage Caps And Closures Market size is expected to reach USD 49.08 billion in 2024 and grow at a CAGR of 4.36% to reach USD 60.77 billion by 2029.

What is the current Beverage Caps And Closures Market size?

In 2024, the Beverage Caps And Closures Market size is expected to reach USD 49.08 billion.