Market Trends of Base Metals Industry

Growing Demand from the Construction Industry

- Base metals, prized for their durability and strength, play diverse roles in the construction industry, with aluminum and copper being the most prevalent.

- Aluminum's corrosion resistance, high conductivity, and ductility make it a staple in construction. Its weather resilience is utilized in windows, doors, wires, outdoor signage, and street lights. Processed into sheets, tubes, and castings, aluminum finds its way into HVAC ducts, roofs, walling, and handles, underscoring its frequent presence in the industry.

- Copper's unique properties, including ductility, malleability, and corrosion resistance, make it a top choice for building pipes. Its recyclability and ease of soldering, forming durable bonds, further enhance its appeal. Rigid copper tubing serves hot and cold water pipes, while soft copper is preferred for refrigerant lines in HVAC systems and heat pumps.

- Oxford Economics forecasts a robust growth trajectory for global construction output, projecting an increase from over USD 4.2 trillion today to a staggering USD 13.9 trillion by 2037, predominantly fueled by the construction powerhouses of China, the United States, and India.

- Both Asia-Pacific and North America are experiencing a surge in residential construction. In Asia-Pacific, countries like India, China, the Philippines, Vietnam, and Indonesia are at the forefront. Meanwhile, North America's residential construction is buoyed by a growing population, rising immigration, and the trend toward nuclear families.

- With housing markets on the rise, the Asia-Pacific region, spearheaded by China and India, is set to lead the global surge in housing construction.

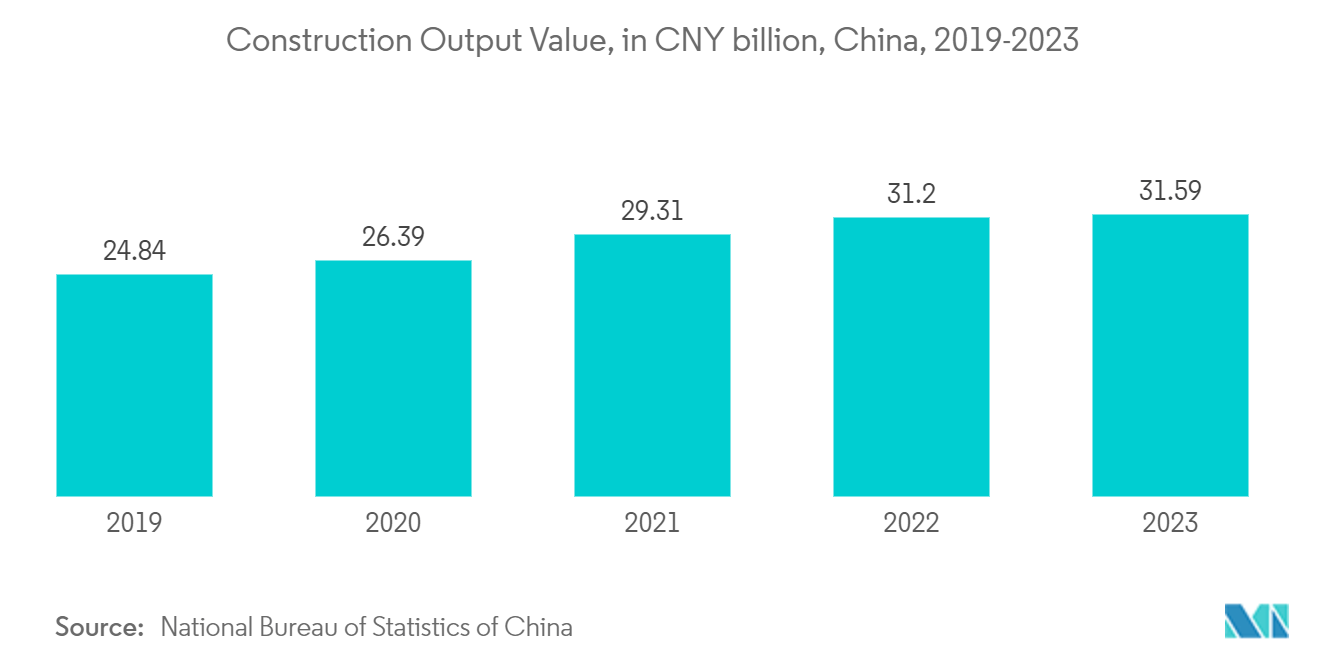

- As per the data from the National Bureau of Statistics of China, the construction industry in China produced an output exceeding CNY 31.59 trillion (~USD 0.002 trillion) in 2023, marking a 1.3% rise from the prior year. Moreover, China, commanding 20% of the world's construction investments, is projected to channel nearly USD 13 trillion into buildings by 2030, underscoring a bullish outlook for the base metals market.

- Highlighting India's momentum, the National Real Estate Development Corporation (NAREDCO) reports that the top 7 cities collectively completed 4.35 lakh units in 2023, with 2024 poised for a substantial uptick. Further underscoring this trend, County Group, a prominent Noida-based real estate developer, is set to unveil over 4 million sq. ft across three ambitious housing projects this year.

- The United States dominates the construction industry in North America, with Canada and Mexico also making substantial investments. According to the US Census Bureau, the US saw a 4.46% increase in new housing units in 2023, reaching 1,452 thousand units, up from 1,390.5 thousand in 2022. Additionally, in May 2024, approximately 116,900 home constructions started in the United States.

- Germany's robust economy is fueling a demand for commercial spaces, especially high-quality, ESG-compliant office buildings, which is evident from rising prime rents. In Q3 2023, 246,000 square meters of office space were completed, with projections reaching 1.8 million square meters in 2024. Retail space development, particularly in shopping centers, grew consistently in 2023.

- Brazil's residential sector is drawing substantial private investments fueled by swift urbanization. In response to this burgeoning demand, the government reintroduced the "Minha Casa, Minha Vida" (My Home, My Life) program in February 2023, setting an ambitious goal of 2 million new projects by 2026.

- The Jeddah Central megaproject epitomizes Saudi Arabia's construction boom. Led by the Jeddah Central Development Company (JCDC), a Public Investment Fund (PIF) subsidiary, this ambitious USD 20 billion endeavor features a museum, opera house, sports stadium, 17,000 residential units, and over 3,000 hotels. With the first phase slated for completion in 2027, developments will continue through 2030 and beyond.

- Given these dynamics, the demand for base metals is poised to increase during the forecast period.

Understand The Key Trends Shaping This Market

Download PDF

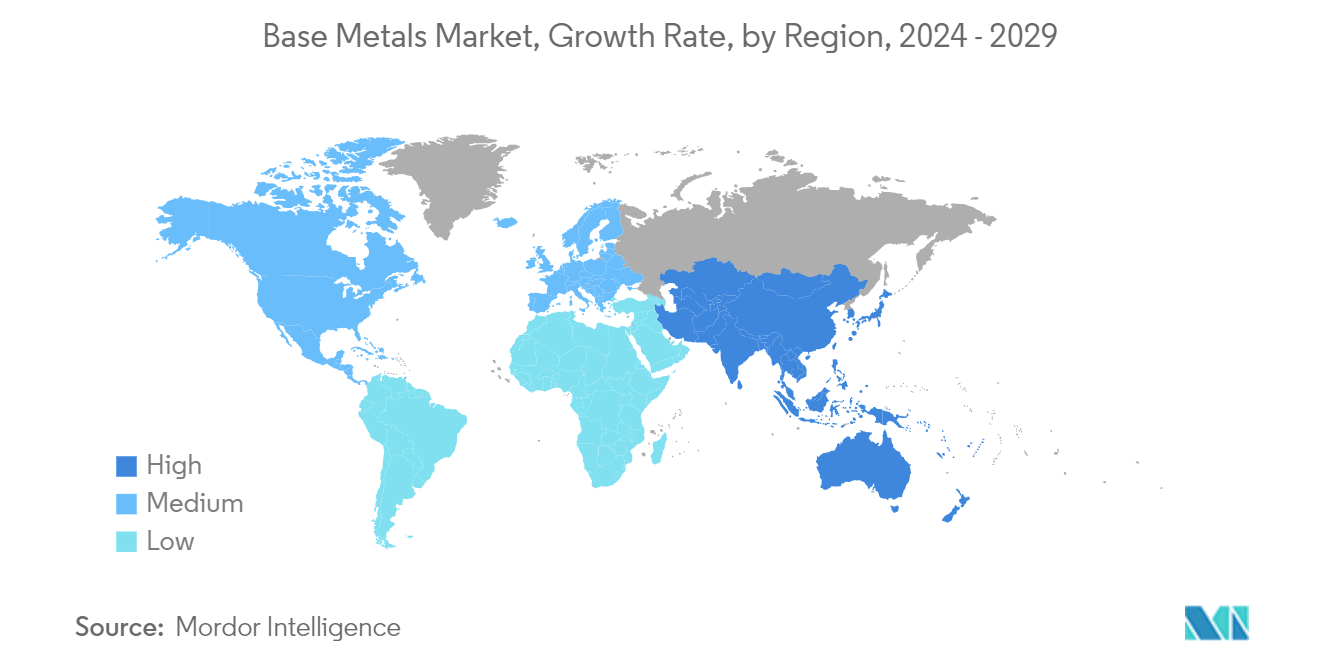

Asia-Pacific to Dominate the Market

- The Asia-Pacific region is set to dominate the base metals market in the coming years. Key drivers include heightened investments in construction, a booming electrical and electronics sector, and a growing demand for heavy equipment bolstered by multinational companies' industrial investments.

- China leads the Asia-Pacific in base metals market share. With ongoing investments and construction activities, China's demand for base metals is on the rise. China's significant infrastructure investments globally are evident. For instance, this year, Chinese governors are boosting budgets for major building projects by nearly 20%. This move underscores the nation's reliance on infrastructure to rejuvenate its post-pandemic economy. Furthermore, over two-thirds of China's regions have earmarked more than CNY 12.2 trillion (USD 1.8 trillion) for key projects, including transportation and industrial zones, in 2024.

- In 2024, India is set to witness a 70% surge in the availability of affordable housing. According to Invest India, the construction sector is projected to attain a valuation of USD 1.4 trillion by 2025. With forecasts suggesting that over 30% of the population will be urban dwellers by 2030, there's a pressing need for 25 million more mid-end and affordable housing units. Recent reforms, such as the Real Estate Act, GST, and REITs, aim to expedite approvals and strengthen the construction industry, driving market growth.

- In India, data from the Society of Indian Automobile Manufacturers (SIAM) indicates that from January to March 2024, the production of passenger vehicles, commercial vehicles, three-wheelers, two-wheelers, and quadricycle reached 7.39 million units. Specifically, sales for passenger and commercial vehicles were 1.14 million and 268 thousand units, respectively. As base metals are used in the automotive, such trends in production are likely to increase the demand for the market studied.

- South Korea boasts a mature automotive industry with notable brands like Hyundai, Renault, Samsung, and Kia. Projections from the Automobile Manufacturers Association and The Korea Automobile Research Institute anticipate a 1.0% rise in domestic automobile production for 2024, reaching 4.36 million units. This growth is expected to drive demand in the studied market.

- Common metals like copper, tin, nickel, and aluminum play pivotal roles in electronics. Dominating the global stage, Asia, led by countries like China and Japan, stands as the foremost producer of electrical and electronics.

- According to Xinhua News Agency, China's electronics sector witnessed a strong start in 2024, driven by rising production and a resurgence in demand. From January to April 2024, major companies in the sector reported a remarkable 75.8% year-on-year profit surge, totaling CNY 144.2 billion (~USD 20.3 billion). This upswing in consumer electronics shipments bodes well for the base metals market. Therefore, increasing the shipments of consumer electronics from the country is expected to have an upside for the base metals market.

- In 2023, China's National Medical Products Administration (NMPA) processed 466 applications for innovative medical devices, granting special approval to 69. Over the past decade, NMPA has approved 250 devices from 185 companies, with a notable quarter of approvals happening in 2023. This trend highlights the growing allure for domestic and international firms to prioritize the Chinese market, a sentiment echoed in the base metals sector.

- Given these positive trends and investments, the Asia-Pacific region is poised for a robust demand for base metals in the coming years.

Get Analysis on Important Geographic Markets

Download PDF