Bakery Processing Equipment Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

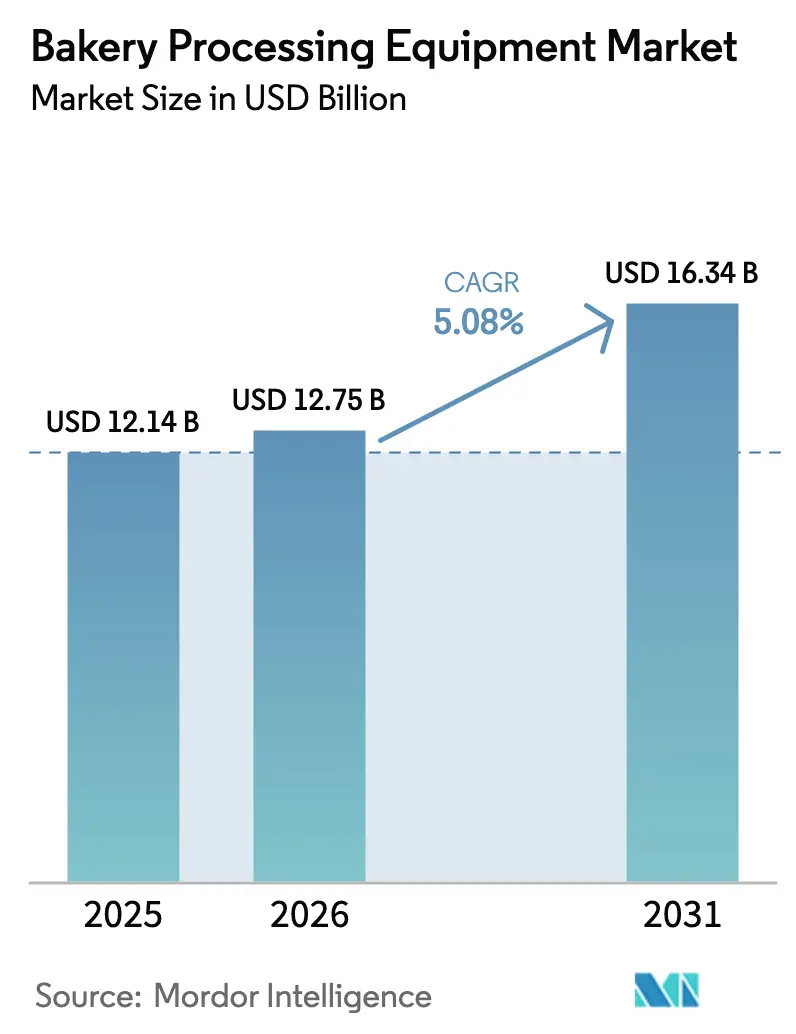

| Market Size (2026) | USD 12.75 Billion |

| Market Size (2031) | USD 16.34 Billion |

| Growth Rate (2026 - 2031) | 5.08% CAGR |

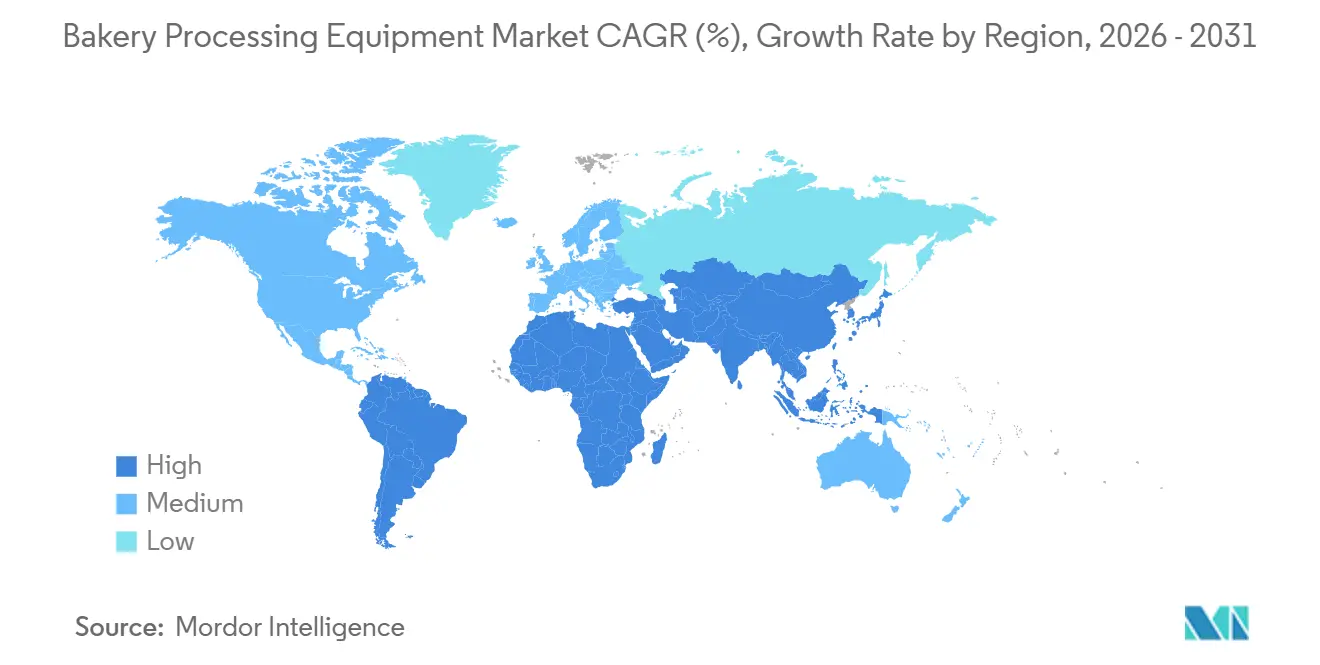

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

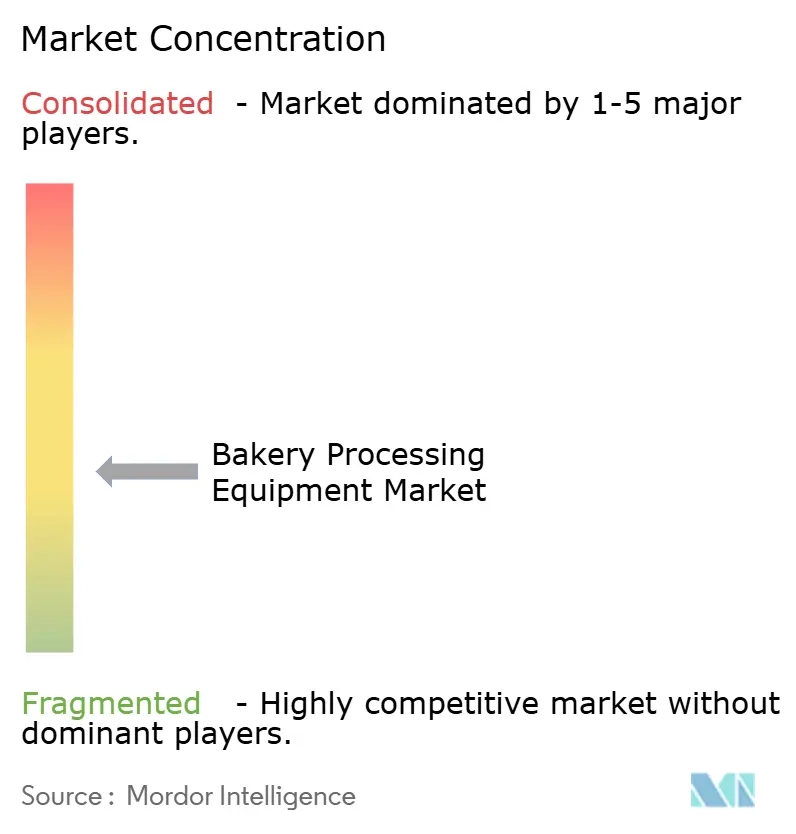

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Bakery Processing Equipment Market Analysis by Mordor Intelligence

The bakery processing equipment market size is expected to increase from USD 12.14 billion in 2025 to USD 12.75 billion in 2026 and reach USD 16.34 billion by 2031, growing at a 5.08% CAGR over 2026-2031. Heightened automation demands in food manufacturing and a surge in the need for scalable, labor-efficient baking solutions are driving this growth. Companies are responding with significant investments: In 2023, Bridor allocated USD 410 million for new production facilities, and in 2024, Campbell Soup announced a USD 160 million expansion for its Goldfish brand, bolstering its baked goods operations. These moves underscore the industry's pivot towards automation in response to evolving consumer preferences. Leading this market expansion, the Asia-Pacific region is buoyed by China's rapid modernization of industrial bakeries and India's expanding retail bakery scene. Highlighting this momentum, The Baker’s Dozen secured USD 5 million in 2024, with plans to strengthen its foothold in tier-II cities. As the production of artisanal bread and pizza crusts gains popularity, there's a marked shift towards specialized equipment like sheeters and molders. The competitive landscape is further intensified by strategic acquisitions, including Middleby Corporation's buyout of GBT GmbH and Bühler Group's integration of Esau & Hueber, both underscoring a focus on technological differentiation and automation.

Key Report Takeaways

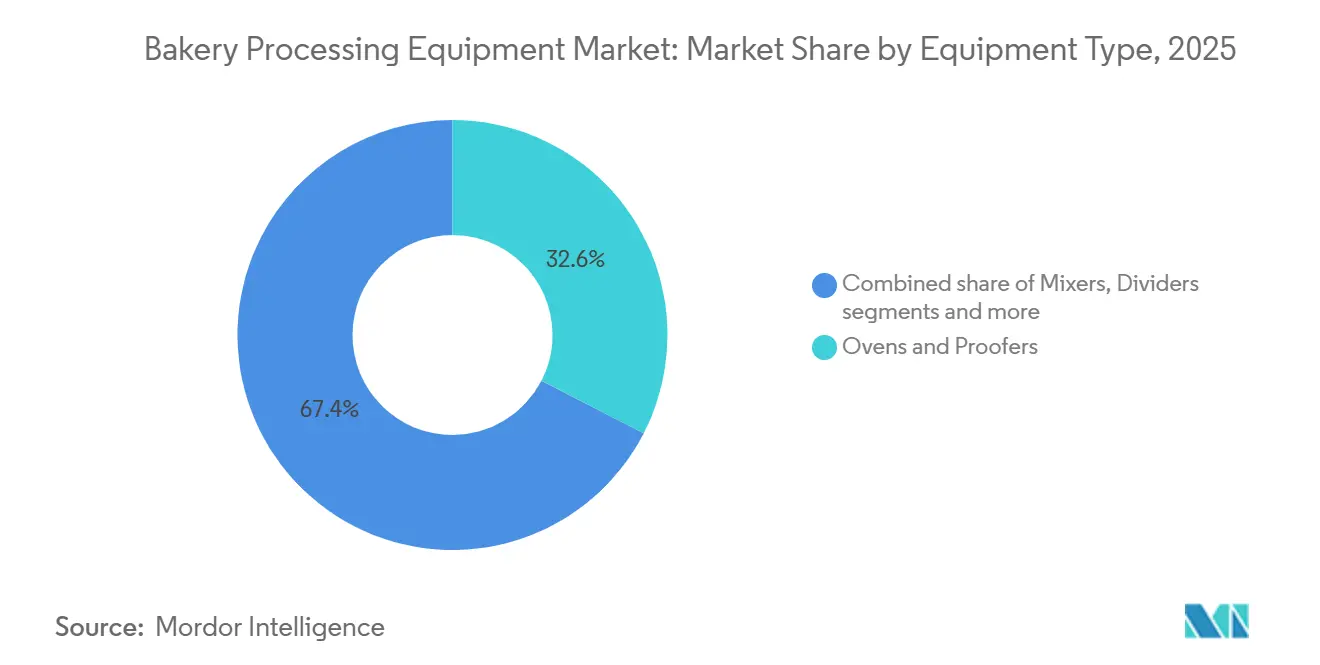

- By equipment type, Ovens and Proofers held the largest 32.56% share of 2025 revenue and are forecast to advance at a 5.08% CAGR through 2031.

- By equipment type, Molders and Sheeters are the fastest-growing block, expanding at an 8.61% CAGR over 2026-2031.

- By application, Bread captured a 36.05% share in 2025 and will expand in lock-step with staple-food demand in emerging economies, while Cakes and Pastries equipment leads growth at an 8.14% CAGR.

- By geography, Asia-Pacific commanded 39.53% of 2025 revenue, yet the Middle East and Africa will record the fastest 7.02% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Bakery Processing Equipment Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) %Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global demand for artisanal and specialty bakery products | +1.2% | Global, concentrated in North America, Western Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Increased automation and hygienic-design standards | +1.5% | Global, led by North America and EU regulatory mandates | Short term (≤ 2 years) |

| Energy-efficient equipment adoption amid sustainability mandates | +0.9% | Europe and North America, spillover to Asia-Pacific | Medium term (2-4 years) |

| Expansion of industrial-scale bakeries in emerging Asia-Pacific markets | +1.8% | China, India, Southeast Asia, spillover to Middle East | Long term (≥ 4 years) |

| IoT-enabled predictive maintenance reducing unplanned downtime | +0.7% | Global, early adoption in North America and Western Europe | Short term (≤ 2 years) |

| Specialized equipment for gluten-free and alt-grain formulations | +0.5% | North America, Western Europe, Australia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising global demand for artisanal and specialty bakery products

Independent zone-control deck ovens and gentle-handling molders are now at the forefront of design briefs, allowing for high-hydration, long-fermentation doughs that maintain their gas-cell structure, which is critical for achieving desired texture and flavor profiles in artisanal baking. Moreover, as 6% of consumers shift their preferences towards bakery purchases, whether at home or in-store, the demand for adaptable and efficient processing equipment becomes increasingly evident[2]Source: Food Industry Association, “Power of In‑Store Bakery 2023,” fmi.org. Suppliers in the ovens and proofers market are witnessing a surge in demand for flexible lines, capable of transitioning from ciabatta to focaccia without the need for tooling swaps, thereby enhancing operational efficiency and reducing downtime. An IBIE survey from 2025 highlighted that 64% of North American bakers are allocating budgets for specialty lines within the next 24 months, with a particular focus on spelt and einkorn capabilities, driven by consumer interest in ancient grains and their perceived health benefits. While this trend is muted in the cost-sensitive Asia-Pacific region, boutique chains in Shanghai and Mumbai are already aligning with Western demand patterns, albeit with a five-year delay, as they gradually cater to a growing niche of health-conscious and premium-seeking consumers.

Increased automation and hygienic-design standards

Protocols like FSMA, NSF/ANSI 169, and EHEDG mandate sanitary enclosures, tool-free disassembly, and CIP circuits to ensure compliance with stringent hygiene and safety standards in food processing and manufacturing. Vendors, including Middleby and VMI, tout mixers and ovens that slash cleaning time by 40% and digitally log sanitation cycles, lightening the audit load and improving operational efficiency. With embedded sensors and smart HMIs, operators enjoy a 60% reduction in labor costs and a return on investment within 12 to 18 months. This is especially appealing as wage inflation surpasses financing expenses, making automation a cost-effective solution. Meanwhile, smaller operators are turning to leasing structures with seasonal repayments to navigate the capital gap, enabling them to adopt advanced equipment without significant upfront investment.

Energy-efficient equipment adoption amid sustainability mandates

Prototypes harnessing hydrogen combustion and electric infrared tunnels achieve energy savings of 20-30%. These technologies not only reduce energy consumption but also contribute to operational efficiency and sustainability goals. This positions their early adopters to benefit from utility rebates and pursue ISO 50001 certification, which is a globally recognized standard for energy management systems. Starting in 2027, European carbon-border taxes, ranging from EUR 50-150 per metric ton of embedded CO₂, are nudging purchase choices towards low-carbon steel and energy-recovery solutions[3]Source: Organisation for Economic Co-operation and Development, "Carbon Border Adjustments: The potential effects of the EU CBAM along the supply chain", oecd.org. These taxes aim to encourage industries to adopt greener practices and reduce their carbon footprint. In states like California and New York, rebates can cover as much as 25% of the acquisition cost for ENERGY STAR-qualified ovens, significantly lowering the financial burden on businesses. This incentive shortens the simple payback period to under three years, making energy-efficient investments more attractive and economically viable.

Expansion of industrial-scale bakeries in emerging asia-pacific markets

In response to rising demands from supermarkets and quick-service restaurants (QSRs), new plants across China, India, and ASEAN have set up advanced production lines capable of producing 96,000 buns per hour. At the 2024 Convention of the American Bakers Association, nearly 70% of member companies announced plans to adopt automation and AI within the next year, aiming to boost capacity and streamline labor and workflow[1]Source: American Bakers Association, “Navigating the Future: Convention Spotlights Automation, Community Impact and Sustainability,” americanbakers.org.These facilities are equipped with multi-story proofing towers, which enhance production efficiency and meet the high-volume requirements of the market. Chinese OEMs, offering turnkey systems at prices 40-50% lower than their European counterparts, have successfully secured contracts despite facing challenges related to software support and after-sales service. Following a similar approach, the Gulf Cooperation Council, supported by sovereign funds, is heavily investing in the establishment of factories. These initiatives aim to address regional bread shortages while also leveraging the growing foodservice sector, which is being fueled by an increase in tourism and related hospitality demands.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital expenditure for advanced equipment lines | −0.8% | Global, acute in emerging markets and mid-tier bakeries | Short term (≤ 2 years) |

| Skilled-labor shortage and steep learning curve | −0.6% | North America, Western Europe, emerging impact in Asia-Pacific | Medium term (2-4 years) |

| Electronic-component supply-chain fragility | −0.4% | Global, dependent on Asian semiconductor supply | Short term (≤ 2 years) |

| Prospective carbon-border taxes inflating lifecycle costs | −0.3% | Europe, secondary impact on exporters to EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High capital expenditure for advanced equipment lines

Turnkey bakeries now demand an investment of USD 2-5 million. This challenge is intensified by lead times stretching 9-12 months and financing costs that are 200-300 basis points higher than averages seen before 2024. These higher costs and extended timelines have created significant barriers for new players in the market. With tighter budgets, new entrants are leaning towards refurbished European machinery, snagging them at discounts of up to 70%. This approach allows them to reduce initial capital expenditure but often comes at the expense of operational efficiency. Additionally, the reliance on refurbished equipment limits the scalability of operations, making it harder for these players to compete with established market leaders. This choice has led to a postponement in fully adopting automation, a trend particularly evident in Latin America and Southeast Asia. The delayed automation adoption further impacts productivity and the ability to meet growing consumer demand in these regions.

Skilled-labor shortage and steep learning curve

U.S. trade associations highlighted a significant 78% gap in engineering maintenance, with projections indicating a potential shortfall of 53,000 workers by 2030. As automation transitions roles from line operators to mechatronics technicians, the demand for higher skills intensifies. This shift is driven by the increasing adoption of advanced manufacturing technologies, which require specialized training and expertise. The shortage is further compounded by a lack of sufficient training programs to upskill the existing workforce. Moreover, the growing complexity of automated systems necessitates continuous learning to keep pace with technological advancements. The gap also poses risks to operational efficiency, as unfilled positions could lead to delays in maintenance and production. While cloud diagnostics and user-friendly HMIs help bridge this gap, they can't fully replace the need for on-site expertise. Additionally, companies are increasingly investing in apprenticeship programs and partnerships with educational institutions to address the skills shortage.

Segment Analysis

By Equipment Type: Thermal Processing Anchors Share

In 2025, ovens and proofers are set to command a dominant 32.56% share of the thermal-processing equipment market's total revenue. Their supremacy is bolstered by a diverse product lineup, featuring deck, rack, tunnel, spiral, and hybrid fuel systems, each tailored for distinct throughput and formulation needs. These systems are indispensable in bakery production, underscoring the segment's robust demand. Furthermore, innovations like hybrid-fuel tunnels, heat-recovery modules, and rapid belt-change systems not only boost operational efficiency but also curtail costs, perpetuating a cycle of equipment upgrades. While Chinese OEMs exert pricing pressures, discerning premium buyers remain steadfast, emphasizing lifecycle costs, reliability, and after-sales service.

Molders and sheeters are on a rapid ascent, eyeing a 14% market share by 2031. This surge is fueled by the rising industrial-scale production of laminated delicacies like croissants and pastries. Anticipating a CAGR of 5.08% until 2031, the segment's growth is a testament to its adoption in high-volume bakery operations. The push for automation and uniformity in dough handling, especially in large-scale and export-focused facilities, drives this expansion. Moreover, advancements in precision forming and seamless integration with continuous production lines are hastening the adoption. As bakery producers broaden their laminated offerings, the momentum for investing in cutting-edge molding and sheeting equipment is poised to escalate.

Note: Segment shares of all individual segments available upon report purchase

By Application: Bread Dominates, Cakes Accelerate

In 2025, bread is set to dominate the market, capturing 36.05% of total revenue. This is largely due to its status as a staple food and its consistent consumption growth, bolstered by urbanization and the increasing popularity of packaged foods. Bread's stronghold is evident in both developed and emerging markets, where it remains a daily dietary essential. The demand for equipment in this segment is stable, driven by the need for high-volume production and standardized processing. Manufacturers are also channeling investments into efficient baking and proofing technologies, aiming to enhance throughput and reduce energy consumption. This blend of scale, necessity, and consistent processing cements bread's top position in the market.

Cakes and pastries are on a rapid ascent, with projections indicating a CAGR of 8.14% through 2031. This surge is largely attributed to a growing appetite for premium and artisanal baked goods. The momentum is further bolstered by the rising adoption of robotic depositing and decorating systems. Notably, desktop solutions priced under USD 5,000 are making automation a reality for smaller bakeries. Evolving consumer preferences, especially the tilt towards gluten-free and clean-label products, are also playing a pivotal role. These preferences necessitate specialized equipment like advanced mixers, extended proofers, and gentle sheeters. Moreover, the booming production of frozen pizza crusts, driven by the expansion of quick-service restaurants (QSRs) and the home delivery trend, is amplifying equipment demand. Collectively, these dynamics position cakes and pastries as the market's primary growth driver.

Geography Analysis

In 2025, the Asia-Pacific region is projected to hold a leading 39.53% revenue share, driven by the development of greenfield capacities in China, India, and various ASEAN nations. Domestic OEMs offer price advantages that enable local bakers to achieve faster returns on investment, although premium imports remain preferred in scenarios where recipe precision and uptime are critical. The rise in urbanization and increasing demand for packaged bakery products are driving equipment investments in tier-2 and tier-3 cities. Additionally, government incentives supporting food processing infrastructure are accelerating the adoption of advanced baking technologies. Regional players are also increasingly adopting automation to enhance consistency and reduce reliance on skilled labor.

The Middle East and Africa are expected to record a strong 7.02% CAGR. In Saudi Arabia, sovereign wealth investments are focused on localizing staple bread production, while Egyptian producers are increasing output fivefold to meet the needs of North African supermarkets. Expanding retail chains and modern trade formats are boosting demand for standardized, high-volume baking solutions. Investments in food security programs across Gulf nations are further strengthening local production capabilities. Partnerships with European equipment suppliers are also enabling regional manufacturers to upgrade their technological capabilities. Population growth and evolving urban consumption patterns continue to support long-term market growth.

Europe and North America, which together account for a significant market share, are shifting their focus from capacity expansion to replacement spending. This shift is primarily driven by stringent hygiene and energy regulations. Manufacturers are prioritizing equipment upgrades to meet strict emissions and food safety standards. The adoption of digitalization, including IoT-enabled monitoring systems, is becoming a key factor in equipment procurement decisions. Retrofitting existing production lines with energy-efficient components is helping bakeries manage operational costs. Furthermore, labor shortages are accelerating the adoption of automation and remote diagnostics.

Competitive Landscape

The global bakery processing equipment market is moderately concentrated. The top four players - GEA, Bühler, JBT Marel, and Middleby - account for about one-third of the global revenue. In 2025, JBT acquired Marel for USD 4.18 billion, positioning itself as a cross-category supplier. With an eye on a projected USD 4 billion revenue in 2026, JBT is now integrating both protein and bakery portfolios. This trend of consolidation underscores a rising demand for comprehensive processing solutions among major industrial bakeries. These larger players, benefiting from scale advantages, are channeling more resources into R&D and global service networks. Meanwhile, mid-sized specialists carve out their niche by emphasizing tailored applications and customization.

In 2026, GEA bolstered its portfolio with the acquisition of Hydract, introducing water-hydraulic valves that mitigate contamination risks. Rademaker's simultaneous 2025 investments in tooling and AI vision underscore a strategic pivot towards modular, software-driven lines that minimize changeovers and defects. While Chinese entrants compete aggressively on pricing, they fall short in the sophistication of control software and global service reach. European firms are carving a niche through engineering precision and comprehensive lifecycle services. Many are also leveraging strategic acquisitions to bridge portfolio gaps and venture into related processing areas. Collaborations with software companies are further propelling the shift towards smart manufacturing.

Technology stands as the primary differentiator: premium vendors are setting themselves apart with hydrogen-ready ovens, AI-driven inspections, and predictive maintenance SaaS. Criteria like ISO 50001 readiness and ENERGY STAR metrics are becoming pivotal in tender evaluations. Clients are shifting their focus from mere upfront costs to the overall total cost of ownership. Tools like digital twins and simulations are being embraced to fine-tune line performance pre-installation. Moreover, real-time data analytics empower operators to boost yields, minimize waste, and maintain consistent product quality.

Bakery Processing Equipment Industry Leaders

-

Bühler Holding AG

-

GEA Group Aktiengesellschaft

-

The Middleby Corporation

-

AMF Bakery Systems

-

Mecatherm S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: In Pennsauken, New Jersey, Puratos and AMF Bakery Systems unveiled a pilot bakery plant. This facility aims to drive innovation and product development in the realm of industrial baking, doubling as a collaborative hub for testing cutting-edge bakery processing technologies.

- May 2025: Rademaker, bolstering its capabilities, acquired Form & Frys and made a strategic investment in AI-vision firm Sensure, enhancing its offerings with 3D depositing and defect detection technologies.

- May 2022: At Interpack, GEA unveiled its sustainable bakery solutions, featuring the energy-efficient Bake Depositor MO, designed for heightened hygiene. The company also rolled out an electric oven retrofit kit, promising a 20% energy savings. Additionally, the newly introduced SmartControl interface aims to simplify real-time monitoring of bakery lines.

Global Bakery Processing Equipment Market Report Scope

| Mixers and Blenders |

| Dividers and Rounder |

| Molders and Sheeters |

| Ovens and Proofers |

| Others |

| Bread |

| Cakes and Pastries |

| Cookies and Biscuits |

| Pizza Crusts |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Rest of Middle East and Africa |

| By Equipment Type | Mixers and Blenders | |

| Dividers and Rounder | ||

| Molders and Sheeters | ||

| Ovens and Proofers | ||

| Others | ||

| By Application | Bread | |

| Cakes and Pastries | ||

| Cookies and Biscuits | ||

| Pizza Crusts | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the bakery processing equipment market?

Revenue is valued at USD 12.75 billion in 2026, on track to reach USD 16.34 billion by 2031.

Which equipment type leads sales?

Ovens and Proofers account for a 32.56% share of 2025 turnover and post a 5.08% CAGR over 2026-2031.

Where is demand growing fastest?

The Middle East and Africa region records a 7.02% CAGR as sovereign funds finance high-capacity bakeries.

What is the main growth driver?

Rising artisanal and specialty product demand pushes investment in flexible, hygienic, and energy-efficient thermal lines.