| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 9.78 Billion |

| Market Size (2030) | USD 12.96 Billion |

| CAGR (2025 - 2030) | 5.78 % |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | High |

Major Players*Disclaimer: Major Players sorted in no particular order |

Autonomous Train Market Analysis

The Autonomous Train Market size is estimated at USD 9.78 billion in 2025, and is expected to reach USD 12.96 billion by 2030, at a CAGR of 5.78% during the forecast period (2025-2030).

The autonomous train industry is experiencing significant technological transformation driven by the integration of advanced digital technologies, including artificial intelligence, machine learning, and the Internet of Things (IoT). This digital revolution is particularly evident in recent developments such as the March 2023 initiative by SNCF, the French national railway, which launched two autonomous trains incorporating advanced AI technologies. The industry's commitment to technological advancement is further demonstrated by the implementation of sophisticated communication-based train control systems, automated safety protocols, and real-time monitoring capabilities that enhance operational efficiency and safety standards.

Infrastructure development continues to be a cornerstone of market expansion, with governments worldwide investing heavily in railway automation and network modernization. China exemplifies this trend, having expanded its railway network to reach 159,000 kilometers by the end of 2023, an increase from 155,000 kilometers in 2022. This infrastructure growth is complemented by the development of smart railway systems, as evidenced by Delhi Metro's launch of India's first indigenous Train Control System & Supervision System in February 2023, marking a significant milestone in domestic technological capabilities.

The industry is witnessing a notable shift towards sustainable and efficient transportation solutions, with major manufacturers focusing on developing energy-efficient autonomous systems. Hitachi Rail's significant presence in the market, manufacturing more than 30% of all autonomous rolling stock products globally, demonstrates the industry's scale and technological maturity. This trend is further reinforced by substantial contracts such as Alstom's March 2023 agreement to provide digital railway signaling for the Chennai Metro Rail Project, valued at approximately USD 200 million, which includes the implementation of communication-based train control systems paired with Automatic Train Operation.

Cross-border collaboration and international expansion are becoming increasingly prominent in the autonomous train market, as evidenced by recent developments in Southeast Asia. In January 2024, CRRC announced plans to introduce autonomous trains in Indonesia's new capital, Nusantara, highlighting the growing international demand for railway automation solutions. The success of cross-border rail operations is demonstrated by the China-Europe freight train service, which saw remarkable growth in early 2023, with 5,611 trains operating between January and April, achieving a 32% year-on-year increase in container transport volume, showcasing the expanding role of autonomous and semi-autonomous trains in international trade.

Autonomous Train Market Trends

Growing Demand for Autonomous Trains in Rapid Transportation

The increasing traffic congestion across urban centers globally has created a strong need for faster, more efficient, and reliable transportation systems, driving the adoption of autonomous trains. Rail has emerged as one of the most energy-efficient transport modes, accounting for 8% of global motorized passenger movements while consuming only 2% of transport energy, making it an attractive solution for urban mobility challenges. The integration of advanced technologies like 5G, big data, the Internet of Things, artificial intelligence, and blockchain has enabled driverless trains to enhance capacity, improve safety, and offer significant cost savings through reduced labor and maintenance requirements.

Recent developments demonstrate the accelerating adoption of autonomous train technology across major metropolitan areas. In June 2023, Alstom launched operations of the MRT Yellow Line in Bangkok, featuring a fully driverless train system with 30 four-car monorail trains capable of operating at speeds up to 80 km/h. Similarly, in January 2024, East Japan Railway announced plans to introduce largely automated bullet trains by the mid-2030s, aiming to achieve Grade of Automation 3 (GoA3) for enhanced operational efficiency. The implementation of advanced technologies like Communication-Based Train Control (CBTC) systems has enabled features such as automatic train operation, automatic train protection, and remote diagnostics, significantly improving the overall passenger experience and operational reliability.

Understand The Key Trends Shaping This Market

Download PDF

Increasing Demand for Efficient Logistics Support

The transformation in the global supply chain industry is creating mounting pressure to deliver fast and flexible services at lower costs, driving the adoption of autonomous transportation in the logistics sector. The mining industry has been at the forefront of implementing autonomous rail solutions, with major companies leveraging automated rail networks to optimize their operations and reduce costs. For instance, in May 2023, Inmatovev received a grant from the U.S. Department of Energy's Advanced Research Projects Agency-Energy to deploy self-propelled rail cars at mining sites, demonstrating the growing integration of autonomous technology in industrial applications.

The logistics industry's demand for autonomous transportation is further fueled by their potential to improve transportation efficiency through optimized routes, shorter transit times, and improved coordination with other transportation modes. AutoHaul, the world's first fully automated rail system, exemplifies these benefits by operating 220 trains across a 1,866-kilometer rail network from mines to ports, being remotely monitored from an operations center in Perth. The system has demonstrated significant operational improvements by eliminating the need for upwards of 500 drivers while delivering substantial annual cost savings. The scalability and flexibility of autonomous trains allow them to easily integrate into existing logistics networks, handle large volumes of freight, and adapt to changing demand patterns, making them an increasingly attractive solution for modern logistics operations.

Segment Analysis: By Automation Grade

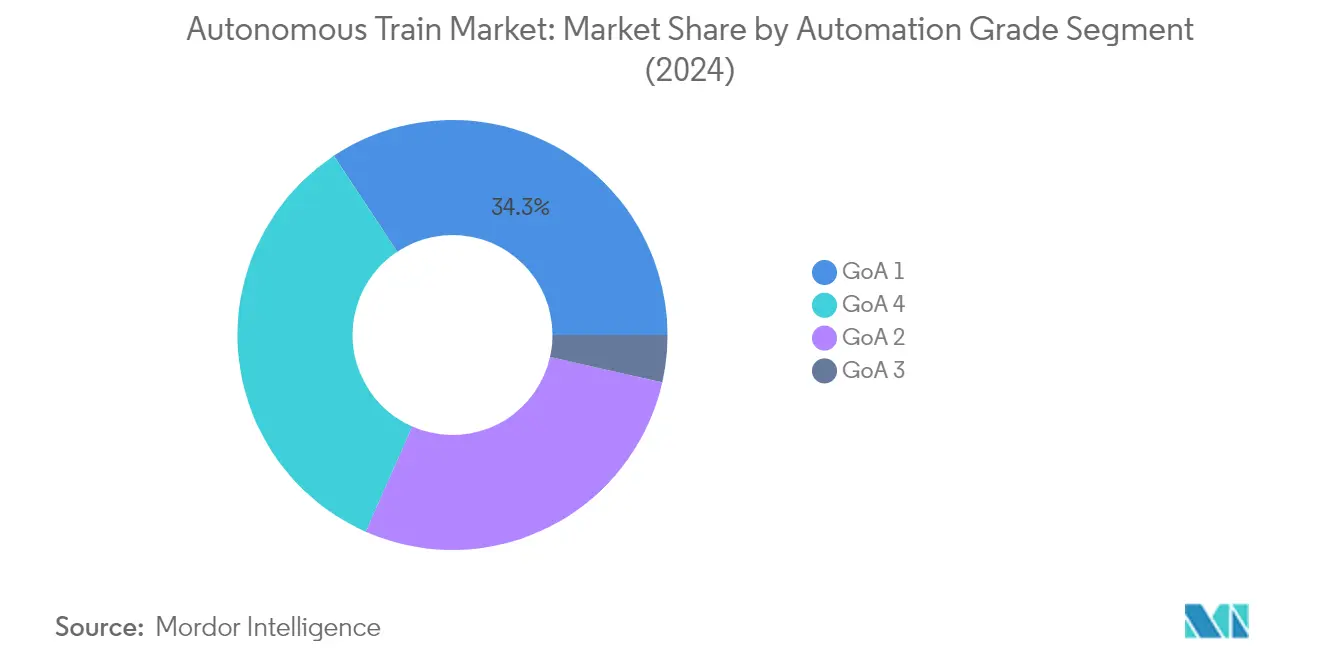

GoA 1 Segment in Autonomous Train Market

The Grade of Automation 1 (GoA 1) segment maintains its leadership position in the autonomous train market, commanding approximately 34% market share in 2024. This dominance is primarily attributed to GoA 1's role as the foundational level of train automation, which includes automated train operation while maintaining manual driving operations. The system's widespread adoption is driven by its proven reliability, cost-effectiveness, and the ability to provide essential safety features while allowing human operators to maintain control of critical functions. Train operators utilizing GoA 1 systems benefit from enhanced safety through automatic train protection, which protects against specified hazards by applying brakes when necessary, while still maintaining the flexibility of manual operations for complex situations requiring human judgment.

GoA 4 Segment in Autonomous Train Market

The Grade of Automation 4 (GoA 4) segment is experiencing the fastest growth trajectory in the autonomous train market, with projections indicating robust expansion through 2024-2029. This accelerated growth is driven by increasing demand for fully driverless train operations that eliminate the need for onboard staff. The segment's growth is further propelled by its ability to optimize operational efficiency, reduce human error, and deliver consistent performance across various operating conditions. Major railway operators are increasingly investing in GoA 4 technology due to its potential to significantly reduce operational costs while improving service frequency and reliability. The technology's advancement in obstacle detection, automated decision-making, and safety protocols has made it particularly attractive for metro systems and urban rail networks seeking to modernize their operations.

Remaining Segments in Automation Grade

The autonomous train market's intermediate automation grades, GoA 2 and GoA 3, play crucial roles in bridging the gap between basic and full automation. GoA 2 provides semi-automatic train operation where acceleration and braking are automated while a driver remains present for supervision and emergency situations. This grade is particularly popular in metro systems where a balance between automation and human oversight is desired. Meanwhile, GoA 3 represents a higher level of automation where trains can operate without onboard staff but still maintain a train attendant for emergency situations. These intermediate grades serve as important stepping stones for operators transitioning from manual to fully autonomous operations, allowing them to gradually implement more advanced automation features while maintaining operational flexibility.

Segment Analysis: By Application

Passenger Segment in Autonomous Train Market

The passenger segment dominates the autonomous train market, commanding approximately 93% of the market share in 2024, while also emerging as the fastest-growing segment. This commanding position is attributed to the increasing adoption of autonomous trains in public transportation systems worldwide, particularly in urban metro networks and intercity rail services. The segment's growth is driven by the rising demand for efficient, safe, and reliable public transportation solutions in metropolitan areas, coupled with government initiatives to modernize railway infrastructure. The implementation of automated train operation technology in passenger trains has demonstrated significant benefits in terms of enhanced operational efficiency, improved safety through reduced human error, and increased service frequency. Additionally, the integration of advanced technologies such as CBTC (Communications-Based Train Control) and ERTMS (European Rail Traffic Management System) has further strengthened the passenger segment's position by enabling more precise train control and better service reliability.

Freight Segment in Autonomous Train Market

The freight segment of the autonomous train market represents a crucial component of the railway industry's automation journey, particularly in mining operations and long-distance cargo transportation. This segment has shown significant potential for growth due to the increasing need for efficient logistics support and the rising demand for automated solutions in freight operations. The implementation of autonomous technology in freight trains has demonstrated notable advantages in terms of operational efficiency, reduced labor costs, and enhanced safety protocols. The segment is witnessing increased adoption in mining operations, where autonomous trains are being deployed for the transportation of minerals and other raw materials. Furthermore, the integration of advanced technologies such as GPS tracking, automated loading and unloading systems, and real-time monitoring capabilities has enhanced the appeal of autonomous freight trains for logistics companies seeking to optimize their operations and reduce operational costs.

Segment Analysis: By Technology

CBTC Segment in Autonomous Train Market

Communication-Based Train Control (CBTC) holds a dominant position in the autonomous train market, commanding approximately 32% market share in 2024. This technology's leadership position stems from its advanced capabilities in providing precise train positioning and real-time communication between trains and wayside equipment. CBTC systems enable railways to improve operational efficiency by maintaining optimal headways while ensuring maximum safety standards. The technology's ability to continuously calculate and communicate train status, including exact position, speed, travel direction, and braking distance, makes it particularly valuable for urban rail transit networks. Modern CBTC systems utilize radio communications to enable trains to automatically and continuously adjust their speed while maintaining safety and comfort requirements. The technology's widespread adoption is further driven by its ability to enhance network capacity and reduce operational costs through improved signaling and control systems.

PTC Segment in Autonomous Train Market

The Positive Train Control (PTC) segment is emerging as the fastest-growing technology in the autonomous train market, projected to grow at approximately 8% during 2024-2029. This robust growth is primarily driven by increasing safety regulations and the technology's crucial role in preventing train-to-train collisions, over-speed derailments, and unauthorized train movements. PTC systems are becoming increasingly sophisticated, incorporating advanced features such as real-time monitoring, automated brake applications, and comprehensive track condition assessment capabilities. The technology's ability to integrate with other railway systems and provide comprehensive safety solutions has made it particularly attractive for railway operators looking to modernize their networks. The growth is further supported by ongoing technological advancements in PTC systems, including improved communication protocols, enhanced data analytics capabilities, and more efficient integration with existing railway infrastructure. Railway operators are increasingly recognizing PTC's value in reducing operational risks while improving overall system efficiency and reliability.

Remaining Segments in Autonomous Train Technology Market

The European Rail Traffic Management System (ERTMS) and Automatic Train Control (ATC) segments continue to play vital roles in shaping the autonomous train market landscape. ERTMS stands out for its contribution to cross-border interoperability and standardization of railway operations across different regions, particularly in Europe. The system's comprehensive approach to train control and safety management makes it an essential technology for international railway networks. Meanwhile, ATC systems provide fundamental safety and control functions, offering various levels of automation and train protection capabilities. These technologies complement each other in the market, with ERTMS focusing on standardization and international compatibility, while ATC systems provide robust local control and safety features. Both segments continue to evolve with technological advancements, incorporating new features such as improved communication systems, enhanced safety protocols, and better integration capabilities with other railway systems.

Segment Analysis: By Train Type

Metro/Monorail Segment in Autonomous Train Market

The Metro/Monorail segment dominates the autonomous train market, holding approximately 68% market share in 2024. This significant market position is driven by the growing need for reliable transportation solutions and increasing traffic congestion in urban areas. The segment's dominance is further strengthened by its ability to provide clean transport systems with high volume capacity, making it an ideal solution for densely populated urban centers. Metro and monorail systems are increasingly adopting autonomous technologies to enhance operational efficiency, improve safety, and reduce human error in operations. The implementation of advanced signaling systems and automated train operation technologies in metro/monorail networks has made them more attractive to city planners and transport authorities. Additionally, the segment benefits from ongoing infrastructure development projects and urbanization initiatives across major global markets, particularly in Asia-Pacific and European regions.

High-Speed Rail Segment in Autonomous Train Market

The High-Speed Rail segment is projected to experience the strongest growth in the autonomous train market from 2024 to 2029, with an expected growth rate of approximately 8%. This accelerated growth is attributed to increasing investments in high-speed rail infrastructure and the rising demand for faster, more efficient intercity transportation solutions. The segment's growth is further driven by technological advancements in autonomous train control systems, which enable safer and more efficient operations at high speeds. Environmental concerns and the push for sustainable transportation alternatives have also contributed to the increased adoption of high-speed rail solutions. The segment is witnessing significant developments in autonomous technology integration, including advanced signaling systems, automatic train operation capabilities, and sophisticated safety features. Additionally, government initiatives promoting high-speed rail networks as part of their sustainable transportation strategies are expected to fuel the segment's growth during the forecast period.

Remaining Segments in Train Type

The Light Rail segment represents an important component of the autonomous train market, offering unique advantages for urban and suburban transportation needs. Light rail systems serve as an intermediate solution between heavy rail and traditional tram systems, providing flexibility in implementation and operation. These systems are particularly valuable in medium-sized cities and suburban areas where full metro systems might be excessive. The segment benefits from technological advancements in autonomous operations, including improved safety features and enhanced passenger comfort. Light rail systems are increasingly incorporating autonomous technologies to improve operational efficiency and reduce operating costs, while maintaining their characteristic flexibility and adaptability to various urban environments. The segment continues to evolve with the integration of new autonomous features and smart technologies, making it an essential part of modern urban transit solutions.

Autonomous Train Market Geography Segment Analysis

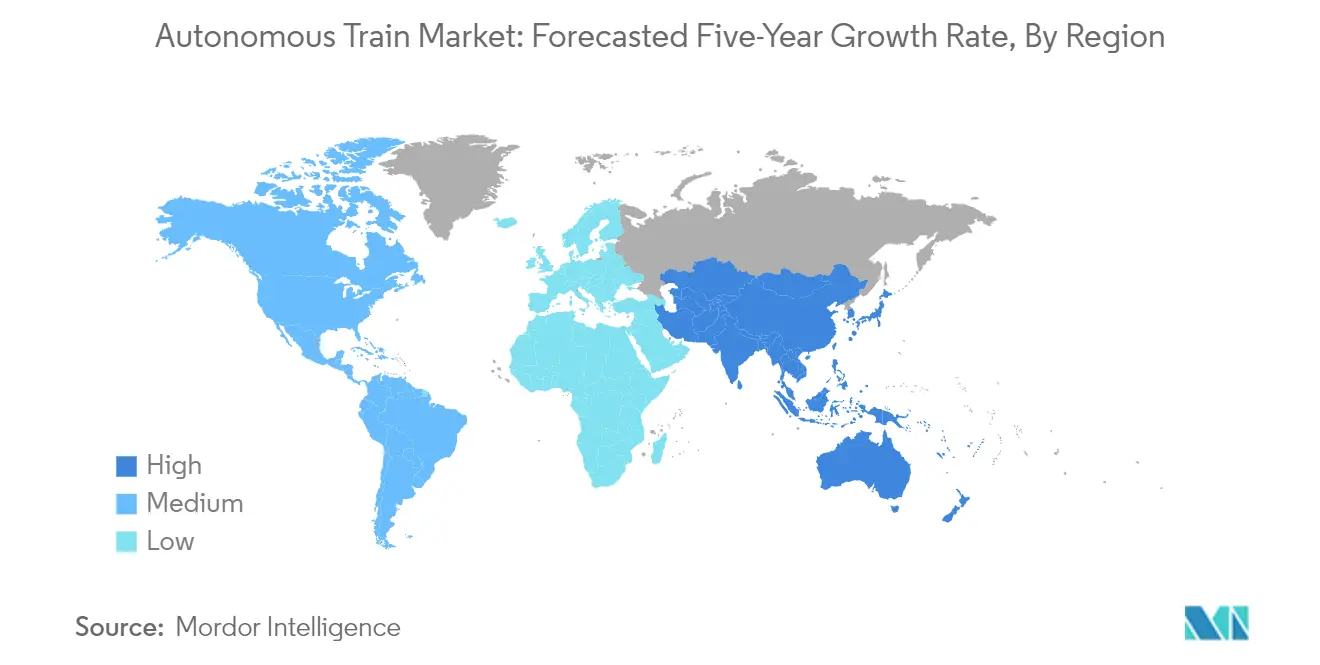

Autonomous Train Market in North America

The North American autonomous train market holds approximately 15% of the global market share in 2024, driven by significant technological advancements in train mobility systems. The United States and Canada continue to be at the forefront of implementing autonomous train technologies, with Canada's extensive 41,711 route km network providing substantial opportunities for market expansion. The region's emphasis on freight transportation, where rail accounts for 28% of all freight movement, has created a strong foundation for autonomous train adoption. The market is particularly robust in areas of coal transportation, raw metal ores movement, and agricultural product logistics, with the network handling significant volumes of intermodal containers and trailers for consumer goods transportation. The growing focus on electric autonomous trains and the integration of advanced safety systems has further strengthened the market position. The region's commitment to enhancing operational efficiency through automation, coupled with increasing demand for efficient logistics support, continues to drive market growth. Additionally, the emphasis on reducing emissions from freight transportation has led to increased investment in autonomous train technologies, particularly in the development of battery-electric rail vehicles.

Autonomous Train Market in Europe

The European autonomous train market has demonstrated steady growth, recording approximately 3% growth from 2019 to 2024, establishing itself as a crucial hub for rail innovation and railway automation. The region boasts one of the most extensive rail networks globally, with countries like Germany leading the adoption of advanced train technologies. Europe's commitment to sustainable mobility has driven significant investments in autonomous train systems, particularly in urban transit solutions. The market's growth is underpinned by robust infrastructure development and modernization initiatives across multiple countries. The region's focus on cross-border connectivity and standardization of rail systems has created a favorable environment for autonomous train technology deployment. European railways' emphasis on passenger comfort, operational efficiency, and environmental sustainability has led to increased adoption of autonomous solutions. The market has also benefited from strong collaboration between industry stakeholders and research institutions, fostering technological innovation. The presence of major railway equipment manufacturers and technology providers has further strengthened the region's position in the global autonomous train market.

Autonomous Train Market in Asia-Pacific

The Asia-Pacific autonomous train market is projected to grow at approximately 7% during 2024-2029, positioning itself as the most dynamic region in the global market. The region's dominance is attributed to the presence of major economies like China, Japan, and India, which are making substantial investments in rail infrastructure and autonomous technologies. The market is characterized by rapid urbanization and increasing demand for efficient public transportation systems, particularly in metropolitan areas. Japan's leadership in autonomous train technology, especially in high-speed rail systems, continues to set benchmarks for the industry. China's massive rail network and aggressive expansion plans have created significant opportunities for autonomous train implementations. The region's focus on developing indigenous manufacturing capabilities for rail components has strengthened the local supply chain. India's growing emphasis on modernizing its rail infrastructure and implementing autonomous solutions has opened new avenues for market growth. The integration of advanced technologies such as artificial intelligence and IoT in train operations has further accelerated market expansion.

Autonomous Train Market in Rest of the World

The Rest of the World region represents an emerging market for autonomous train technologies, with countries in Latin America, Africa, and the Middle East showing increasing interest in rail automation. Brazil's significant focus on expanding and modernizing its cargo rail infrastructure has created new opportunities for autonomous train implementations. The South African market, with the largest railway network in Africa, continues to evolve with new investments in transportation infrastructure. Middle Eastern countries are increasingly adopting autonomous train technologies, particularly in urban transit systems, as part of their smart city initiatives. The region's growing emphasis on improving public transportation efficiency and reducing operational costs has driven the adoption of autonomous solutions. The market is characterized by increasing collaboration between local operators and global technology providers, facilitating knowledge transfer and technological advancement. Countries in these regions are particularly focused on implementing autonomous solutions that can withstand diverse geographical and climatic conditions while maintaining operational efficiency.

Get Analysis on Important Geographic Markets

Download PDF

Autonomous Train Industry Overview

Top Companies in Autonomous Train Market

The autonomous train market is characterized by the strong presence of established players like Hitachi Rail STS, Thales Group, Alstom SA, Siemens AG, and Mitsubishi Heavy Industries, who are driving innovation through significant R&D investments. These companies focus on developing advanced railway signaling systems, communication-based train control system technologies, and automated operation solutions to enhance safety and operational efficiency. Strategic partnerships and collaborations with technology providers are becoming increasingly common as companies seek to strengthen their autonomous capabilities. Market leaders are expanding their geographical presence through regional manufacturing facilities and service centers while simultaneously investing in next-generation railway automation technologies. The industry is witnessing a trend toward integrated solutions that combine hardware, software, and services to provide comprehensive autonomous train systems.

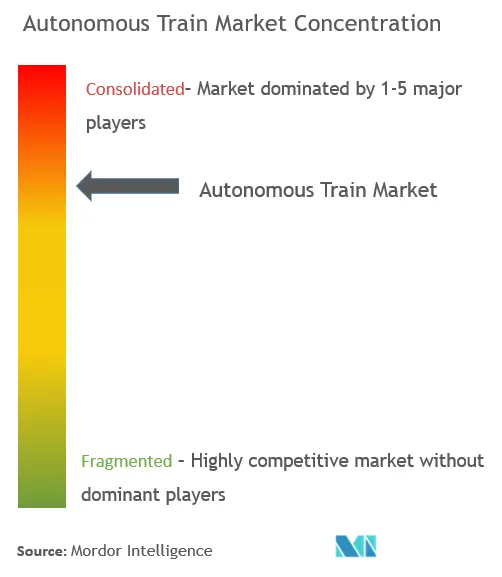

Consolidated Market with High Entry Barriers

The autonomous train market exhibits a highly consolidated structure dominated by large multinational conglomerates with extensive technological capabilities and established market presence. These companies leverage their broad product portfolios, strong financial resources, and deep industry expertise to maintain their competitive positions. The market is characterized by high entry barriers due to substantial capital requirements, complex regulatory compliance needs, and the necessity for proven safety track records. Regional players typically focus on specific market segments or geographical areas, often collaborating with global leaders to access advanced technologies and expand their market reach.

The industry is experiencing strategic consolidation through mergers and acquisitions, as companies seek to enhance their technological capabilities and expand their geographical footprint. Major players are acquiring specialized technology firms to strengthen their autonomous solutions portfolio and gain access to innovative technologies. The trend toward vertical integration is evident as companies aim to control critical components of the value chain, from signaling systems to maintenance services. Joint ventures and strategic alliances are becoming increasingly common, particularly in emerging markets where local expertise and market access are crucial for success.

Innovation and Adaptation Drive Market Success

Success in the autonomous train market increasingly depends on companies' ability to innovate while maintaining the highest safety standards and operational reliability. Incumbent players must focus on continuous technological advancement, particularly in areas such as artificial intelligence, machine learning, and advanced sensors, while simultaneously expanding their service offerings to include predictive maintenance and remote monitoring capabilities. Building strong relationships with rail operators and transport authorities through long-term service contracts and collaborative development programs is becoming crucial for maintaining market position. Companies need to demonstrate clear value propositions that address both operational efficiency and safety requirements while managing the high costs associated with autonomous technology development.

For new entrants and challenger companies, success lies in identifying and exploiting specific market niches while building strategic partnerships with established players. Companies must navigate complex regulatory environments and focus on developing specialized solutions that complement existing systems. The ability to offer cost-effective solutions while maintaining high safety standards will be crucial for gaining market share. Future success will also depend on companies' ability to address cybersecurity concerns and adapt to evolving regulatory frameworks governing autonomous train operations. Building trust with end-users through transparent communication about safety features and performance capabilities will be essential for market acceptance and growth. The ongoing railway digitalization efforts are expected to play a pivotal role in shaping the future of the autonomous train industry.

Autonomous Train Market Leaders

-

Hitachi Rail STS (Ansaldo)

-

Alstom SA

-

Thales Group

-

Siemens AG

-

Mitsubishi Heavy Industries Ltd

-

CRCC Corporation Limited

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Autonomous Train Market News

- April 2024: Danish State Railways (DSB) and railway infrastructure operator Banedanmark signed a contract with leading transport technology manufacturer Siemens Mobility for equipment for autonomous trains totaling USD 288 million. The two entities announced the launch of fully autonomous trains by 2030 as part of an ambitious program to modernize the suburban S-Bane network in Copenhagen.

- July 2023: The newly launched light rail train LRT service in Jakarta, the first autonomous train designed by Indonesian engineers, began operation in 2023. The LRT service has a total of 31 trainsets, with one trainset consisting of six cars that can hold between 740 and 1,480 people. Each car has 174 seats for around 700 people and provides standing spaces for up to 56 people.

Autonomous Train Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

-

4.1 Market Drivers

- 4.1.1 Increased Focus on Safety

-

4.2 Market Restraints

- 4.2.1 High Initial Investment in the Launch of New Projects

-

4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION

-

5.1 By Automation Grade

- 5.1.1 GoA 1

- 5.1.2 GoA 2

- 5.1.3 GoA 3

- 5.1.4 GoA 4

-

5.2 By Application

- 5.2.1 Passenger

- 5.2.2 Freight

-

5.3 By Technology

- 5.3.1 CBTC

- 5.3.2 ERTMS

- 5.3.3 ATC

- 5.3.4 PTC

-

5.4 By Train Type

- 5.4.1 Metro/Monorail

- 5.4.2 Light Rail

- 5.4.3 High-speed Rail

-

5.5 By Geography

- 5.5.1 North America

- 5.5.2 Europe

- 5.5.3 Asia-Pacific

- 5.5.4 Rest of the World

6. COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share**

-

6.2 Company Profiles*

- 6.2.1 Siemens AG

- 6.2.2 Alstom SA

- 6.2.3 Thales Group

- 6.2.4 Hitachi Rail STS (Ansaldo STS)

- 6.2.5 Mitsubishi Heavy Industries Ltd

- 6.2.6 Kawasaki Heavy Industries

- 6.2.7 Construcciones y Auxiliar de Ferrocarriles (CAF)

- 6.2.8 CRRC Corporation Limited

- 6.2.9 Wabtec Corporation

- 6.2.10 Ingeteam Corporation SA

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Expansion of Autonomous Train Networks

- 7.2 Integration of Intelligent Transportation Systems (ITS)

- 7.3 Development of Hyperloop and Maglev Technologies

- 7.4 Adoption of Artificial Intelligence (AI) and Machine Learning (ML)

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Autonomous Train Industry Segmentation

An autonomous train is a driverless train that operates without human intervention. Equipped with advanced technology, such as AI and sensors, it navigates, controls speed, and makes decisions on its own. Benefits include improved efficiency, safety, and capacity. However, safety standards and testing are crucial for public integration.

The autonomous train market is segmented by automation grade, application, technology, train type, and geography. By automation grade, the market is segmented by GoA 1, GoA 2, GoA 3, and GoA 4. By application, the market is segmented by passenger and freight. By technology, the market is segmented by CBTC, ERTMS, ATC, and PTC. By train type, the market is segmented into metro/monorail, light rail, and high-speed rail. By geography, the market is segmented by North America, Europe, Asia-Pacific, and Rest of the World.

The report covers the market size in value (USD) for all the above segments.

| By Automation Grade | GoA 1 |

| GoA 2 | |

| GoA 3 | |

| GoA 4 | |

| By Application | Passenger |

| Freight | |

| By Technology | CBTC |

| ERTMS | |

| ATC | |

| PTC | |

| By Train Type | Metro/Monorail |

| Light Rail | |

| High-speed Rail | |

| By Geography | North America |

| Europe | |

| Asia-Pacific | |

| Rest of the World |

Need A Different Region or Segment?

Customize Now

Autonomous Train Market Research FAQs

How big is the Autonomous Train Market?

The Autonomous Train Market size is expected to reach USD 9.78 billion in 2025 and grow at a CAGR of 5.78% to reach USD 12.96 billion by 2030.

What is the current Autonomous Train Market size?

In 2025, the Autonomous Train Market size is expected to reach USD 9.78 billion.

Who are the key players in Autonomous Train Market?

Hitachi Rail STS (Ansaldo), Alstom SA, Thales Group, Siemens AG, Mitsubishi Heavy Industries Ltd and CRCC Corporation Limited are the major companies operating in the Autonomous Train Market.

Which is the fastest growing region in Autonomous Train Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Autonomous Train Market?

In 2025, the Asia-Pacific accounts for the largest market share in Autonomous Train Market.

What years does this Autonomous Train Market cover, and what was the market size in 2024?

In 2024, the Autonomous Train Market size was estimated at USD 9.21 billion. The report covers the Autonomous Train Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Autonomous Train Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Autonomous Train Market Research

Mordor Intelligence provides a comprehensive analysis of the autonomous train market. We leverage deep expertise in railway automation and railway digitalization trends. Our extensive research covers automatic train operation (ATO) systems, unattended train operation (UTO), and driverless train operation (DTO) technologies. The report offers detailed insights into railway signaling systems and train control system implementations. It also explores emerging smart rail solutions. This information is available in an easy-to-read report PDF format for download.

Our analysis benefits stakeholders across the connected rail ecosystem. This includes manufacturers of automated people mover systems and operators implementing metro automation solutions. The report examines intelligent train technologies and automated guided transit developments. It also explores the evolution of autonomous transportation systems. Comprehensive coverage includes railway automation trends and connected rail market dynamics. Additionally, it highlights technological advancements in driverless train operations. These insights are valuable for industry decision-makers navigating the rapidly evolving autonomous train landscape.