Autonomous Delivery Robots Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

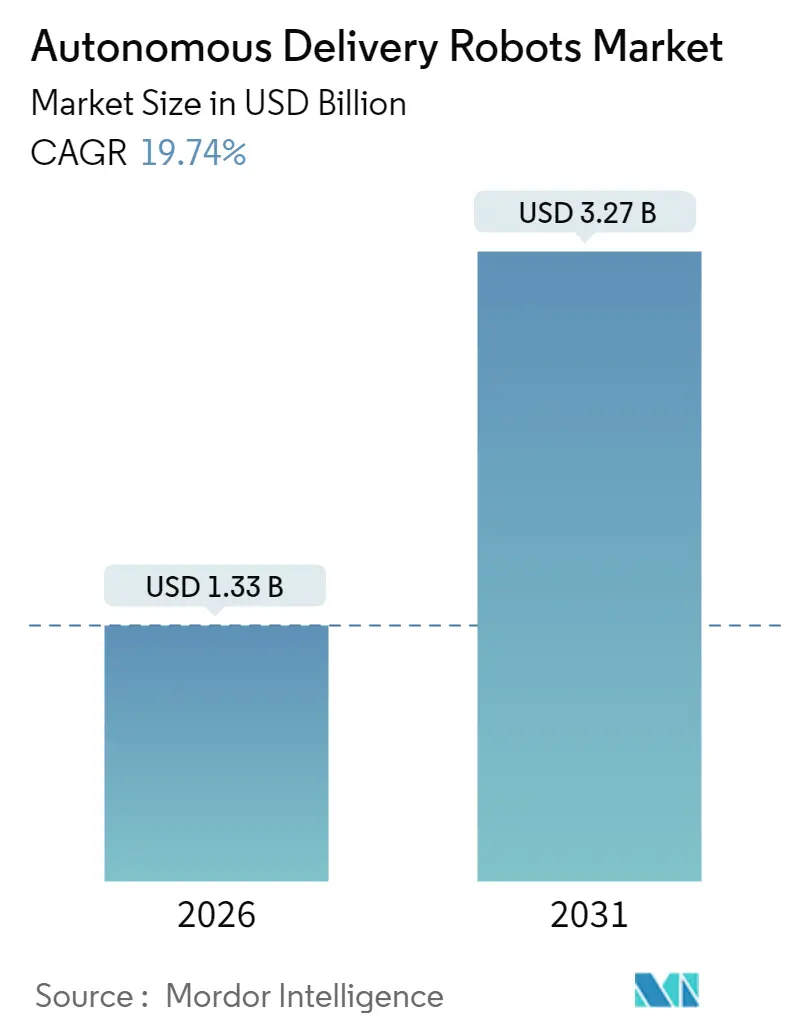

| Market Size (2026) | USD 1.33 Billion |

| Market Size (2031) | USD 3.27 Billion |

| Growth Rate (2026 - 2031) | 19.74% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Autonomous Delivery Robots Market Analysis by Mordor Intelligence

The autonomous delivery robots market is expected to grow from USD 1.11 billion in 2025 to USD 1.33 billion in 2026 and is forecast to reach USD 3.27 billion by 2031 at 19.74% CAGR over 2026-2031. Growth is grounded in rising labor shortages, swift technological maturation, and supportive regulations that ease sidewalk deployments. Major logistics spenders continue to view the technology as mission-critical; Amazon alone targets USD 200 billion of automation savings through robotic solutions. North America leads adoption thanks to 32.1% 2024 share, while Asia-Pacific follows at 25% as aging populations increase demand for contact-free healthcare logistics. Outdoor sidewalk robots dominate with 58% share, and hybrid all-terrain units post the fastest 27.8% CAGR, signaling a clear preference for platforms that handle both urban and indoor routes. Competitive activity remains intense as venture-backed specialists scale fleets in partnership with delivery platforms, while automotive incumbents pursue healthcare and industrial niches. Headwinds tied to payload limits and high LiDAR costs persist, yet rapid sensor price declines and new community-engagement strategies point to a wider addressable base over the forecast horizon.

Key Report Takeaways

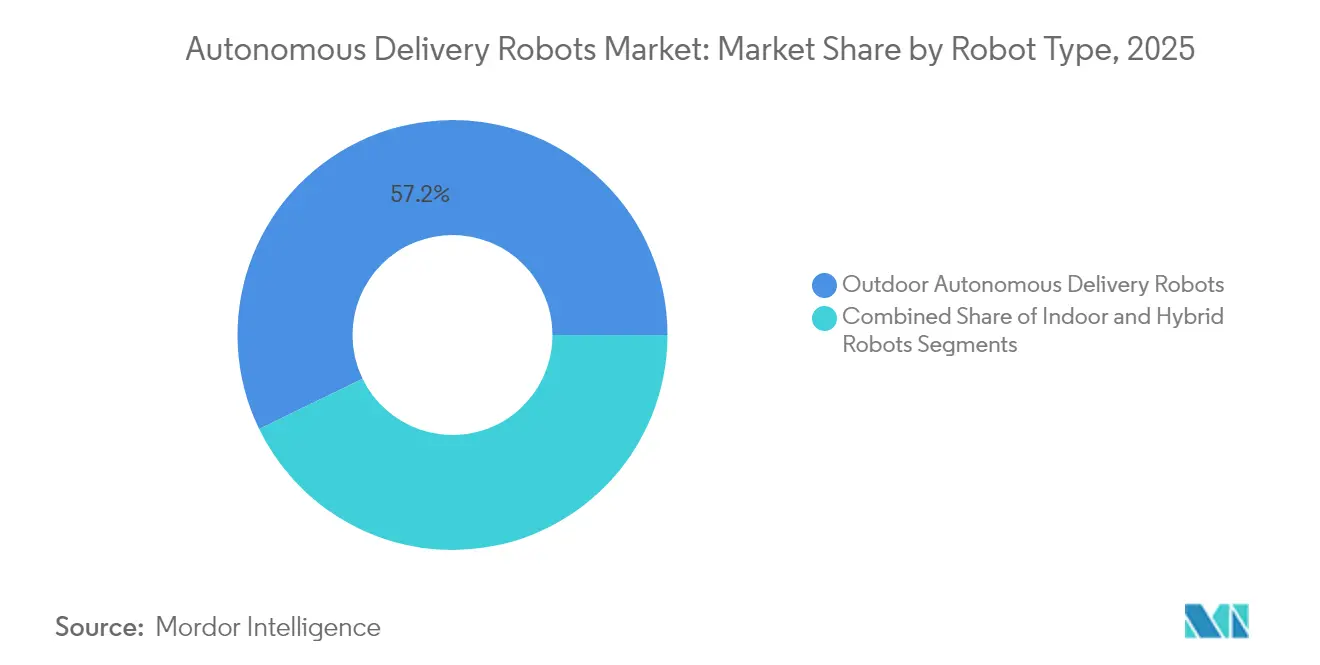

- By robot type, outdoor models held 57.20% of the autonomous delivery robots market share in 2025; hybrid all-terrain robots are forecast to expand at a 26.65% CAGR through 2031.

- By application, food delivery led with 42.10% revenue share in 2025; grocery and convenience deliveries are projected to record a 23.70% CAGR to 2031.

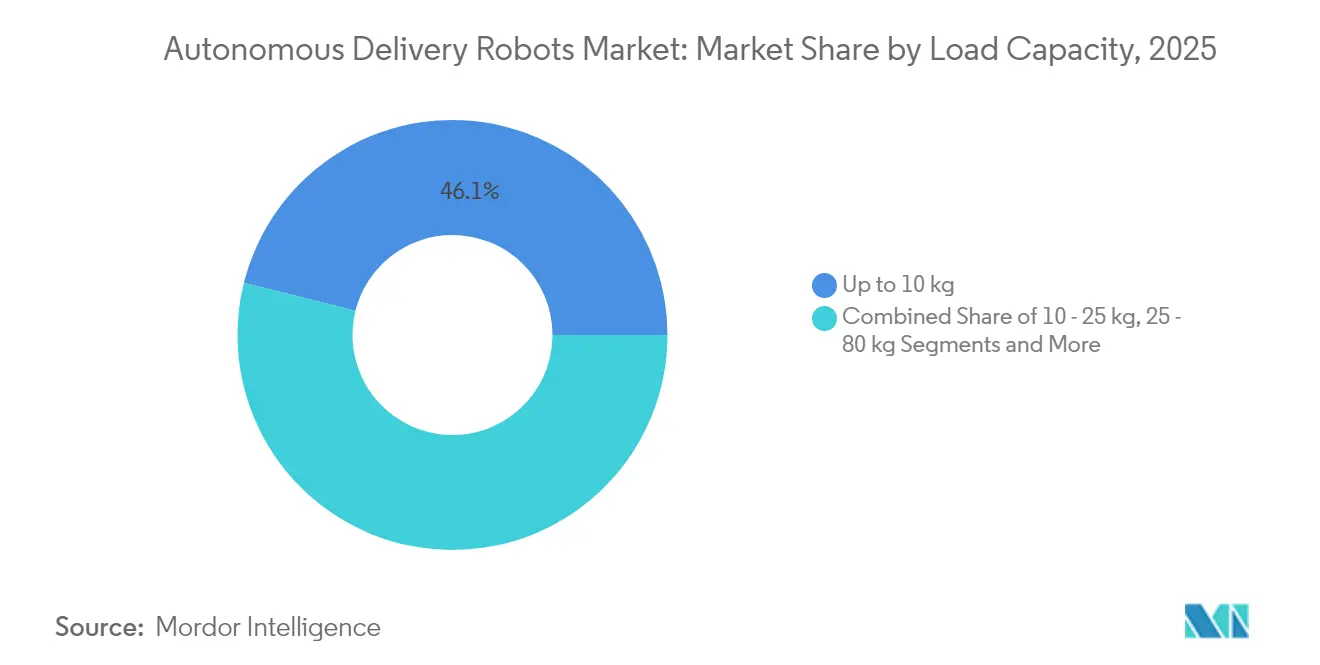

- By load capacity, units up to 10 kg accounted for 46.10% share of the autonomous delivery robots market size in 2025; robots above 80 kg show the highest 22.60% CAGR outlook.

- By end-user industry, retail and e-commerce logistics commanded 48.60% share in 2025, while healthcare facilities are advancing at a 24.90% CAGR to 2031.

- By propulsion, battery-electric systems captured 93.10% share in 2025; hydrogen fuel-cell platforms post a 30.20% CAGR from a small base.

- Serve Robotics, Starship Technologies, and Nuro collectively controlled 18% of global fleet deployments in 2024.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Autonomous Delivery Robots Market Trends and Insights

Drivers Impact Analysis

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rapid expansion of on-demand grocery delivery | +3.2% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Rising labor shortages & wage inflation in North-American fulfillment | +4.1% | North America, spillover to Europe | Short term (≤ 2 years) |

| ESG-driven push for zero-emission last-mile vehicles in the EU | +2.8% | Europe, expanding to APAC | Long term (≥ 4 years) |

| Aging population spurring intra-hospital delivery automation in Japan | +1.9% | APAC core, particularly Japan & South Korea | Medium term (2-4 years) |

| 24/7 contact-free services demand in Middle-East luxury hotels | +1.4% | Middle East & Africa, premium segments globally | Short term (≤ 2 years) |

| 5G edge-compute enabling higher robot autonomy in dense city cores | +2.7% | Global, concentrated in tier-1 cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Expansion of On-Demand Grocery Delivery

On-demand grocery services now anchor sustainable unit economics for autonomous fleets because high order density offsets traditional driver costs. Kroger integrated driverless trucks into its Dallas operations to accelerate fulfillment and trim logistics spend. Retailers also embed in-store shelf-scanning robots to reduce the documented 4.5% revenue leakage linked to stock-outs, as shown by Simbe Robotics’ rollout across 60 SpartanNash stores. Together these moves confirm that grocery chains are shifting robotics from pilot status to core infrastructure, widening order volumes available to last-mile robots.[1]Caitlin Mullen, “Kroger Rolls Out Autonomous Trucks to Aid Fast Delivery,” chainstoreage.com

Rising Labor Shortages and Wage Inflation

North American fulfillment centers face acute staffing gaps that push companies toward automated alternatives. The U.S. manufacturing sector projects a 2 million-worker shortage by 2030, and last-mile driver turnover amplifies cost pressure. Falling industrial robot prices—down 50% in the past decade—and further declines predicted by EY strengthen the investment case. High urban delivery density then allows operators to hit utilization targets that yield faster payback on autonomous assets.

ESG-Driven Push for Zero-Emission Last-Mile Vehicles

European rules that mandate carbon cuts in urban freight create structural advantages for compact electric robots over vans. Academic studies show potential energy savings above 40% when sidewalk robots replace traditional couriers. Starship Technologies already records 1.8 million kg of avoided CO₂ from more than 6 million completed orders, highlighting environmental payoffs aligned with EU climate goals. This alignment accelerates municipal permitting for zero-emission fleets.

Aging Population Spurring Intra-Hospital Delivery Automation

Japan’s demographic realities magnify nurse workload pressures, prompting hospitals to deploy autonomous couriers. Toyota’s Potaro robot now averages 170 medication runs per day by navigating ceilings-mounted cameras, freeing staff for patient care. South Korea complements the trend by legalizing sidewalk robots that meet strict safety caps, opening a path for wider healthcare and residential adoption.

Restraints Impact Analysis

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Limited payload capacity restricting ROI for bulk goods | -2.8% | Global, particularly affecting rural & suburban markets | Medium term (2-4 years) |

| High upfront cost of LiDAR & sensor suites | -3.4% | Global, with greater impact in price-sensitive markets | Short term (≤ 2 years) |

| Vandalism & theft incidents in S-American metros | -1.2% | Latin America, urban centers with security challenges | Short term (≤ 2 years) |

| Complex regulatory frameworks across jurisdictions | -2.1% | Global, particularly Europe & North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost of LiDAR and Sensor Suites

Navigation hardware often accounts for the largest capital item in a delivery robot. Emerging ultrasonic alternatives such as Sonair cut sensor spend by up to 80% while keeping a 180 × 180 degree detection envelope. Cartken’s lidar-free vision stack already operates profitably on public sidewalks, proving that cost-efficient sensing can meet reliability thresholds. Even so, broad rollout waits on regulatory validation of these novel sensor mixes.[2]Machine Design Editors, “3D Ultrasonic Sensor Technology Cuts Costs,” machinedesign.com

Vandalism and Theft Incidents in South-American Metros

Security breaches increase operating costs through repairs, recovery, and real-time monitoring. Serve Robotics experienced vandalism during Uber Eats trials in Los Angeles, requiring police footage for incident resolution. Latin American cities pose similar challenges, where elevated theft risk necessitates hardened enclosures, GPS-locked cargo bays, and privacy-sensitive camera feeds—raising both capex and stakeholder engagement needs.

Segment Analysis

By Robot Type: Outdoor Dominance Drives Market Evolution

Outdoor robots generated 57.20% of 2025 revenue, anchoring the autonomous delivery robots market through well-tested sidewalk operations. This dominance reflects reliable partnerships with food aggregators and local regulators that allow scalable city deployments. Operators continue to refine chassis for curbs, crosswalks, and pedestrian interaction, reinforcing their urban stronghold.

Hybrid all-terrain units expand rapidly at 26.65% CAGR because retail and hospitality customers ask for seamless door-to-door service that crosses thresholds. Suppliers respond by integrating four-wheel steering, modular cargo pods, and ruggedized suspension, a trend evident in Avride’s pivot to NVIDIA-powered four-wheel platforms. Indoor service robots maintain niche roles in campuses and hospitals where controlled corridors permit higher autonomy without full street-grade sensing.

Note: Segment shares of all individual segments available upon report purchase

By Application: Food Delivery Leadership Faces Grocery Challenge

Food delivery retained 42.10% revenue share in 2025, proving that frequent small-ticket orders still underpin the autonomous delivery robots market. High repetition optimizes asset utilization and simplifies route learning, supporting fleet-level profitability for platforms such as Serve Robotics.

Grocery and convenience segments rise 23.70% annually as retailers chase sub-hour fulfillment. Robots accommodate temperature-controlled totes and door-step protocols that boost basket size and tip-influenced economics. Parcel courier services also advance, but payload ceilings still limit heavier SKUs, keeping focus on lightweight e-commerce orders for now.

By Load Capacity: Weight Limits Shape Market Boundaries

Units carrying ≤ 10 kg held 46.10% share of the autonomous delivery robots market size in 2025 because most meals and small parcels fall inside that envelope. Lightweight frames enable longer ranges on standard batteries and comply with sidewalk weight caps.

Demand for 80 kg-plus robots grows 22.60% per year as retailers test bulk grocery drops and campus mailcart equivalents. Development hinges on stronger drivetrains and denser batteries that do not breach curb weight laws. Mid-range categories stay important for pharmacy and multi-meal orders where single-trip value offsets additional energy draw.

Note: Segment shares of all individual segments available upon report purchase

By End-User Industry: Retail Leadership Drives Ecosystem Development

Retail and e-commerce companies captured 48.60% share in 2025, validating that shopper expectations for same-day delivery favor robotic help. Deployment at big-box grocers, convenience chains, and dark stores cements this segment’s primacy and steers vendor roadmaps toward food-safe containers and dynamic rerouting.

Healthcare facilities, rising at 24.90% CAGR, illustrate a premium niche where service reliability outweighs cost. Robots ferry medication, lab samples, and meals along predictable corridors, freeing staff and reducing infection exposure. Early wins at Japanese hospitals signal similar adoption prospects in Europe and North America as regulations mature.

Geography Analysis

North America retained 31.60% share in 2025, reflecting high wage inflation and a supportive patchwork of state-level rules. California and Texas host the largest urban pilots, with Serve Robotics targeting 2,000 units by year-end 2025 under an Uber Eats framework. College-town deployments add scale; Grubhub and Yandex plan rollouts across 250 campuses, potentially forming the world’s densest robot network.

Asia-Pacific followed with a 25.40% stake as Japan and South Korea accelerate healthcare and smart-city programs. South Korea’s sidewalk-friendly legislation caps robot speed at 15 km/h and weight at 500 kg, unlocking commercial trials in apartment complexes and hospitals. Toyota’s Potaro system shows the model for intra-hospital use, highlighting APAC’s focus on aging-related logistics.

Europe contributes a solid revenue base, aided by stringent ESG mandates that penalize diesel vans in city centers. Starship Technologies operates in Germany and the UK under regulatory exemptions that let slow-moving robots share pedestrian zones. Operators still navigate complex, multi-jurisdiction approval processes, slowing scale, yet the environmental tailwinds keep adoption on a steady path.

Competitive Landscape

The autonomous delivery robots market remains fragmented, with top five vendors holding just under 25% of installed fleets. Venture-funded disrupters rely on rapid capital injections to finance production tooling and city launch costs. Serve Robotics raised USD 80 million in January 2025, lifting total funding above USD 247 million as it aims for breakeven on a 2,000-unit fleet. Starship Technologies secured USD 90 million in February 2024 to expand global operations and has logged 11 million robot miles to date.

Sensor strategy differentiates rivals. LiDAR-centric players tout millimeter-level mapping, while Cartken proves that computer-vision stacks without LiDAR can still achieve urban reliability at lower cost, having reached profitability with under USD 25 million raised. Automotive OEM entrants such as Toyota leverage deep manufacturing know-how to produce hospital-grade platforms and exploit existing service networks.

Partnerships with food aggregators or retailers often dictate deployment velocity. Uber Eats, Grubhub, Walmart, and Kroger each select hardware partners to secure exclusive city zones, creating de-facto geographic strongholds. In parallel, software-only firms license navigation stacks to white-label hardware made by contract manufacturers, signaling a move toward modular value chains.

Autonomous Delivery Robots Industry Leaders

Starship Technologies

Ottonomy.IO

Nuro Inc.

Serve Robotics Inc.

Kiwibot

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Serve Robotics secured USD 80 million in funding to expand its sidewalk delivery robot fleet from 100 to 2,000 units by the end of 2025, bringing total funding to over USD 247 million. The expansion aims to achieve operational cash-flow positivity while serving Uber Eats and 7-Eleven partnerships across multiple urban markets.

- November 2024: Serve Robotics announced third quarter 2024 results showing plans for geographic expansion into Dallas Fort Worth metro area and a capital raise of USD 32.3 million, bringing cash balance to USD 50.9 million. The company reported 108% year-over-year increase in daily supply hours and 97% increase in daily active robots.

- November 2024: Nuro expanded driverless delivery robot testing in Mountain View and Houston following a strategic pivot to license its autonomous vehicle technology to other companies. The expansion reflects the company's focus on partnerships to leverage its technology for broader market applications.

- October 2024: Avride unveiled a next-generation four-wheel delivery robot design powered by NVIDIA AI, improving maneuverability, speed, and parking capabilities on inclines. The new model features a detachable storage section and utilizes the NVIDIA Jetson Orin platform for enhanced autonomous navigation.

Global Autonomous Delivery Robots Market Report Scope

Autonomous delivery robots perform autonomously and are generally utilized for delivery and service applications. These robots are electric-powered vehicles that deliver items or packages to customers without a delivery person. The studied Market is segmented by various end users such as Healthcare, Hospitality, Retail & Logistics among multiple geographies. The impact of macroeconomic trends on the Market is also covered under the scope of the study. Further, the disturbance of the factors affecting the Market's evolution in the near future has been covered in the study regarding drivers and constraints. The market sizes and predictions are provided in terms of value (USD) for all the above segments.

| Indoor Service Robots |

| Outdoor Autonomous Delivery Robots |

| Hybrid All-Terrain Robots |

| Food Delivery |

| Grocery and Convenience Deliveries |

| Parcel and Courier (E-commerce) |

| Healthcare Supply and Medication |

| Hospitality Room-Service |

| Industrial Campus Logistics |

| Up to 10 kg |

| 10 - 25 kg |

| 25 - 80 kg |

| Above 80 kg |

| Healthcare Facilities |

| Hospitality and Hotels |

| Retail and E-commerce Logistics |

| Corporates and Academic Campuses |

| Airports and Transportation Hubs |

| Smart Cities and Municipal Agencies |

| Hardware |

| Software / AI Stack |

| After-Sales Services and Fleet Management |

| Electric Battery |

| Hydrogen Fuel Cell |

| Hybrid Energy Harvesting |

| Semi-Autonomous (Human-Supervised) |

| Fully Autonomous (Level 4) |

| Swarm/Clustered Autonomous Network (Level 5) |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Africa | South Africa |

| Kenya | |

| Asia-Pacific | China |

| Australia | |

| Japan | |

| Singapore | |

| India | |

| South Korea |

| By Robot Type | Indoor Service Robots | |

| Outdoor Autonomous Delivery Robots | ||

| Hybrid All-Terrain Robots | ||

| By Application | Food Delivery | |

| Grocery and Convenience Deliveries | ||

| Parcel and Courier (E-commerce) | ||

| Healthcare Supply and Medication | ||

| Hospitality Room-Service | ||

| Industrial Campus Logistics | ||

| By Load Capacity | Up to 10 kg | |

| 10 - 25 kg | ||

| 25 - 80 kg | ||

| Above 80 kg | ||

| By End-User Industry | Healthcare Facilities | |

| Hospitality and Hotels | ||

| Retail and E-commerce Logistics | ||

| Corporates and Academic Campuses | ||

| Airports and Transportation Hubs | ||

| Smart Cities and Municipal Agencies | ||

| By Component | Hardware | |

| Software / AI Stack | ||

| After-Sales Services and Fleet Management | ||

| By Propulsion Type | Electric Battery | |

| Hydrogen Fuel Cell | ||

| Hybrid Energy Harvesting | ||

| By Level of Autonomy | Semi-Autonomous (Human-Supervised) | |

| Fully Autonomous (Level 4) | ||

| Swarm/Clustered Autonomous Network (Level 5) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Africa | South Africa | |

| Kenya | ||

| Asia-Pacific | China | |

| Australia | ||

| Japan | ||

| Singapore | ||

| India | ||

| South Korea | ||

Key Questions Answered in the Report

What is the current autonomous delivery robots market size?

The autonomous delivery robots market stands at USD 1.33 billion in 2026 and is projected to reach USD 3.27 billion by 2031 at a 19.74% CAGR.

Which segment holds the largest autonomous delivery robots market share?

Outdoor sidewalk robots led with 57.20% share in 2025, reflecting mature urban deployments.

How fast is the grocery segment growing within the autonomous delivery robots market?

Grocery and convenience deliveries are expanding at a 23.70% CAGR through 2031 as retailers seek faster, cost-efficient last-mile options.

Why are LiDAR costs viewed as a restraint for the autonomous delivery robots industry?

Traditional LiDAR units significantly raise robot price tags; although new ultrasonic and vision-based sensors can cut costs up to 80%, they still await wide regulatory acceptance.

Which regions are expected to adopt autonomous delivery robots most rapidly?

North America leads today due to labor shortages, while Asia-Pacific and Europe follow closely on the back of healthcare automation and zero-emission mandates, respectively.

What level of autonomy is most common in commercial fleets?

Semi-autonomous Level 3 robots with remote oversight account for 71% of active deployments, balancing operational readiness with current regulatory requirements.