Market Size of Automotive Suspension System Industry

| Study Period | 2019 - 2029 |

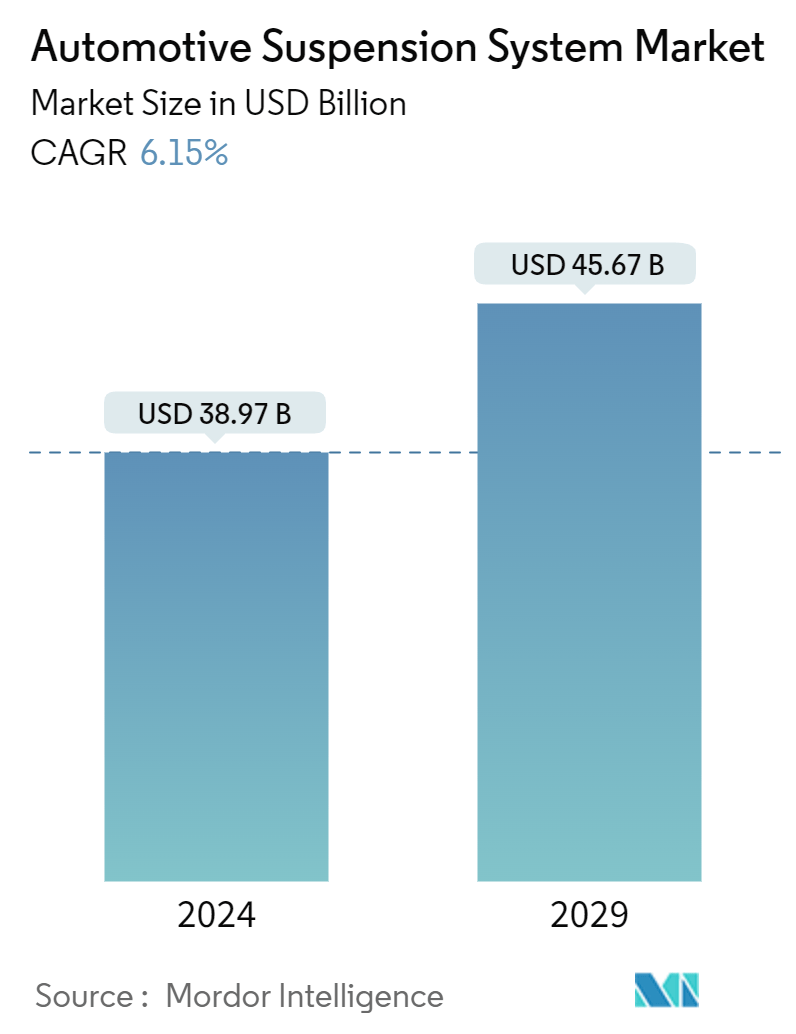

| Market Size (2024) | USD 38.97 Billion |

| Market Size (2029) | USD 45.67 Billion |

| CAGR (2024 - 2029) | 6.15 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Automotive Suspension System Market Analysis

The Automotive Suspension System Market size is estimated at USD 38.97 billion in 2024, and is expected to reach USD 45.67 billion by 2029, growing at a CAGR of 6.15% during the forecast period (2024-2029).

The automotive suspension systems market exhibits a consolidated landscape, dominated by a few major global players such as ZF Friedrichshafen AG, Continental AG, and Hyundai Mobis. These companies have established a stronghold in the market through extensive product portfolios, technological advancements, and strategic collaborations. One of the primary growth drivers in this market is the increasing demand for fuel-efficient and eco-friendly vehicles. Advanced suspension systems play a crucial role in optimizing vehicle fuel efficiency by reducing air resistance and improving overall performance. The growing preference for comfortable and smooth rides has led to a surge in demand for advanced suspension systems across various vehicle segments. In 2022, approximately 85 million motor vehicles were produced globally. China emerged as the global leader in passenger car production, manufacturing approximately 23.84 million vehicles alongside 3.19 million commercial vehicles, solidifying its position as the foremost producer of passenger cars worldwide. Over the medium term, demand for luxury cars and the penetration of active suspension systems are expected to drive the market’s growth. The rise in vehicle autonomy is also anticipated to drive the market’s growth for sensor- and electronic-based suspension systems.

One of the primary challenges faced by the market is the increasing complexity of vehicle suspension systems, which requires significant investments in R&D to maintain competitiveness. Additionally, the high cost of advanced suspension systems can act as a barrier to their widespread adoption, particularly in emerging markets where affordability remains a key concern. The fluctuating prices of raw materials, such as steel and aluminum, can significantly impact the production costs of suspension systems, leading to margin pressures for manufacturers. Lastly, stringent regulatory norms and environmental concerns related to the production and disposal of suspension components can pose challenges for market players in terms of compliance and sustainability.

Several OEMs have recently introduced innovative suspension systems to cater to evolving consumer preferences and regulatory requirements. OEMs are investing in R&D to integrate novel technologies into suspension systems to improve steering stability and provide a comfortable ride. Such developments will drive the vehicle suspension market forward. For instance, in April 2023, EXT developed an updated adaptation of the Era fork's pioneering dual-positive air chamber design, specifically tailored to meet the unique demands of the Aria application. Similarly, in November 2022, Monroe launched new Intelligent Suspension RideSense products in North America designed for luxury European vehicles equipped with electronic suspensions as a direct replacement for OE electronic units.

Asia-Pacific and Europe are projected to be the fastest-growing automotive suspension system markets. In Asia-Pacific, China is expected to continue to drive market growth during the forecast period.

Automotive Suspension System Industry Overview

Automotive suspension systems are mechanical assemblies in vehicles that connect the wheels to the vehicle body, providing stability, control, and comfort during operation. They are vital in optimizing fuel efficiency, handling, and ride quality by absorbing road shocks and maintaining tire contact with the road surface. Advanced suspension systems incorporate various technologies, such as sensors and electronics, to enhance performance and cater to evolving consumer preferences and regulatory requirements.

The automotive suspension systems market is segmented into component type, vehicle type, and geography. Based on the component type, the market is segmented into coil springs, leaf springs, air springs, shock absorbers, and other components. By vehicle type, the market is segmented into passenger cars and commercial vehicles. By type, the market is segmented into passive suspension, semi-active suspension, and active suspension. By geography, the market is segmented into North America, Europe, Asia-Pacific, and Rest of the World.

For each segment, market size and forecast have been done based on the value (USD).

| Component Type | |

| Coil Spring | |

| Leaf Spring | |

| Air Spring | |

| Shock Absorber | |

| Other Component Types |

| Type | |

| Passive Suspension | |

| Semi-active Suspension | |

| Active Suspension |

| Vehicle Type | |

| Passenger Cars | |

| Commercial Vehicles |

| Geography | |||||||

| |||||||

| |||||||

| |||||||

|

Automotive Suspension System Market Size Summary

The automotive suspension systems market is poised for significant growth, driven by the increasing demand for fuel-efficient and eco-friendly vehicles. Major global players like ZF Friedrichshafen AG, Continental AG, and Hyundai Mobis dominate the market, leveraging extensive product portfolios and technological advancements. The market's expansion is fueled by the rising preference for comfortable rides and the growing demand for luxury cars and active suspension systems. The Asia-Pacific region, particularly China, is expected to lead this growth, supported by the surge in vehicle production and sales. The infrastructure and logistics industry's expansion further boosts the demand for commercial vehicles, thereby increasing the need for reliable suspension systems.

Despite the promising growth prospects, the market faces challenges such as the complexity and high cost of advanced suspension systems, which may hinder widespread adoption, especially in emerging markets. Fluctuating raw material prices and stringent regulatory norms also pose challenges. However, ongoing technological advancements and strategic partnerships among key players are expected to drive innovation and market expansion. Initiatives like the development of electric commercial vehicles and the introduction of novel suspension technologies are set to propel the market forward, with significant contributions from regions like Asia-Pacific and Europe.

Automotive Suspension System Market Size - Table of Contents

-

1. MARKET DYNAMICS

-

1.1 Market Drivers

-

1.1.1 Increasing Demand for Enhanced Ride Comfort

-

-

1.2 Market Restraints

-

1.2.1 High Upfront Cost of Advanced Suspension Systems

-

-

1.3 Industry Attractiveness - Porter's Five Forces Analysis

-

1.3.1 Bargaining Power of Suppliers

-

1.3.2 Bargaining Power of Buyers/Consumers

-

1.3.3 Threat of New Entrants

-

1.3.4 Threat of Substitute Products

-

1.3.5 Intensity of Competitive Rivalry

-

-

-

2. MARKET SEGMENTATION (Market Size in Value (USD))

-

2.1 Component Type

-

2.1.1 Coil Spring

-

2.1.2 Leaf Spring

-

2.1.3 Air Spring

-

2.1.4 Shock Absorber

-

2.1.5 Other Component Types

-

-

2.2 Type

-

2.2.1 Passive Suspension

-

2.2.2 Semi-active Suspension

-

2.2.3 Active Suspension

-

-

2.3 Vehicle Type

-

2.3.1 Passenger Cars

-

2.3.2 Commercial Vehicles

-

-

2.4 Geography

-

2.4.1 North America

-

2.4.1.1 United States

-

2.4.1.2 Canada

-

2.4.1.3 Rest of North America

-

-

2.4.2 Europe

-

2.4.2.1 Germany

-

2.4.2.2 United Kingdom

-

2.4.2.3 Italy

-

2.4.2.4 France

-

2.4.2.5 Rest of Europe

-

-

2.4.3 Asia-Pacific

-

2.4.3.1 China

-

2.4.3.2 India

-

2.4.3.3 Japan

-

2.4.3.4 South Korea

-

2.4.3.5 Rest of Asia-Pacific

-

-

2.4.4 Rest of the World

-

2.4.4.1 South America

-

2.4.4.2 Middle East and Africa

-

-

-

Automotive Suspension System Market Size FAQs

How big is the Automotive Suspension System Market?

The Automotive Suspension System Market size is expected to reach USD 38.97 billion in 2024 and grow at a CAGR of 6.15% to reach USD 45.67 billion by 2029.

What is the current Automotive Suspension System Market size?

In 2024, the Automotive Suspension System Market size is expected to reach USD 38.97 billion.