Market Trends of Automotive Special Purpose Logic IC Industry

This section covers the major market trends shaping the Automotive Special Purpose Logic IC Market according to our research experts:

Electric cars will drive the Market

- Electric vehicle (EV) sales doubled in 2021 from the previous year, reaching a new high of 6.6 million, according to EV Outlook 2022. This increased the overall number of electric automobiles on the road to around 16.5 million, more than tripling the number in 2018. Electric car sales have continued to grow substantially in 2022, with 2 million sold in the first quarter, up 75% over the same period in 2021.

- The Electric Vehicles Initiative (EVI) is a multi-government policy forum founded in 2010 as part of the Clean Energy Ministerial (CEM). Recognizing the benefits of electric vehicles, the EVI is committed to accelerating their adoption around the world. To that end, it aims to better understand the policy difficulties surrounding electric mobility, assist governments in addressing them, and serve as a knowledge-sharing platform. The EVI encourages dialogues between government policymakers and a variety of partners who are devoted to EV development by bringing them together twice a year. In the anticipated term, the Electric Vehicles Initiative aims to boost EV adoption and the investigated market.

- Despite the Covid-19 epidemic and supply chain issues, like as semiconductor chip shortages, electric car sales hit a new high in 2021. In 2012, over 120,000 electric automobiles were sold worldwide. That many were sold in a week in 2021.

- Because of rising consumer awareness about environmental pollution and rising oil prices, the demand for electric vehicles is expanding globally, which is driving the market for communication logic IC to rise. The potential of vehicle-to-vehicle (V2V) communication to wirelessly transmit information on the speed and position of nearby cars holds enormous promise for reducing traffic congestion, avoiding crashes, and improving the environment.

- Increased sales of autos as a result of increased connectivity options in vehicles are positively impacting the industry growth. Furthermore, the market is expected to develop in the forecast period due to the rapid growth of the automotive sector.

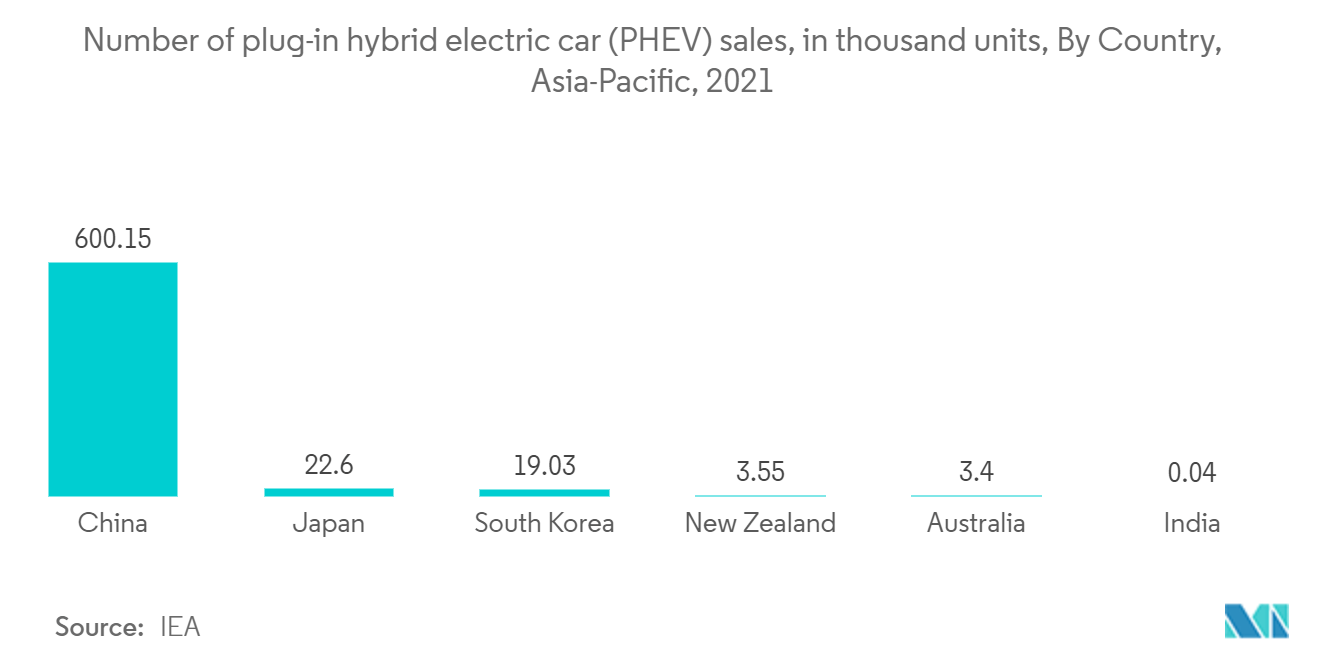

- Asia-Pacific is the home of major automobile manufacturers such as Honda, Hyundai, Toyota, TATA, etc. The region is also a huge market for the automobile industry, with consumers of all classes. According to the 2022 data by OICA, in 2021, China produced approximately 21.4 million passenger cars, while Japan and India produced approx. 6.6 and 3.6 million cars. While China has partnerships and collaborations with global automobile manufacturers, making it the biggest auto producer in the region, ahead of South Korea, Japan, and India, these countries enjoy a strong domestic automotive sector. With the rise of the auto industry in such high growth regions, the demand for the studied market is also expected to grow.

Understand The Key Trends Shaping This Market

Download PDF

China to hold a significant share in the Market

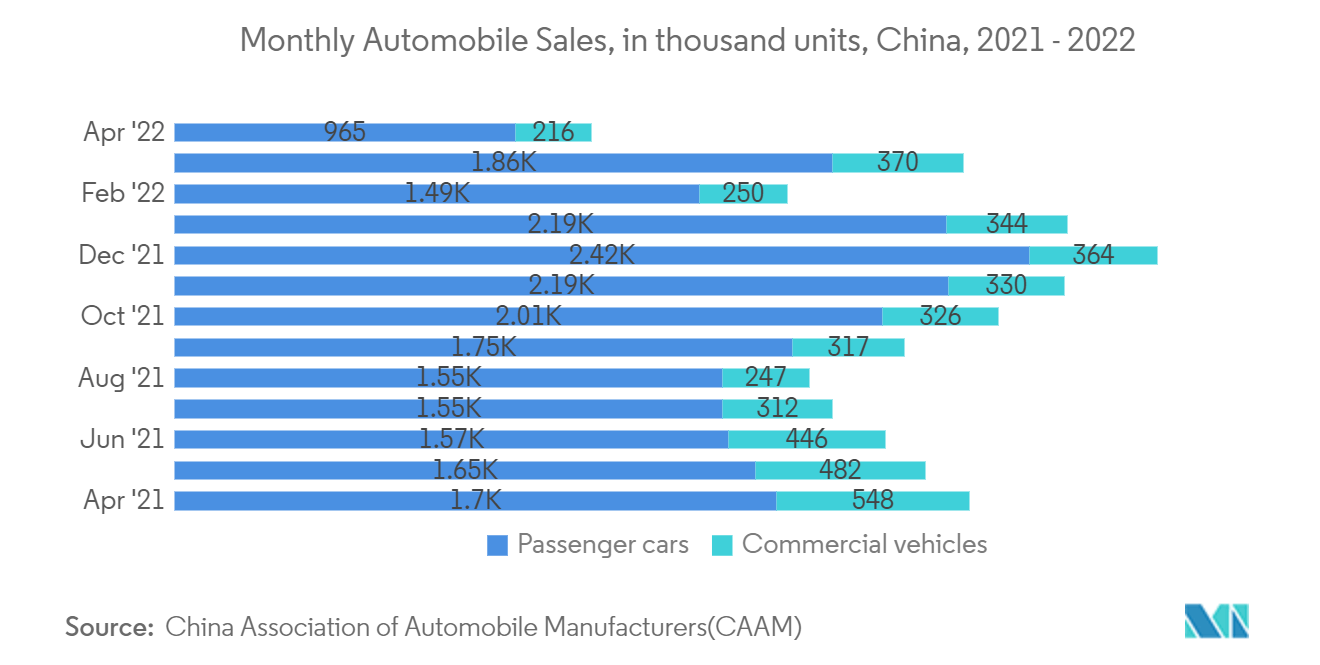

- According to the Global EV Outlook 2022, the People's Republic of China led the increase in EV sales in 2021, accounting for half of the growth. In 2021, China sold 3.3 million more vehicles than the rest of the world combined.

- Electric vehicles in China are often smaller than those in other regions. This, combined with cheaper development and production costs, has helped to close the price gap with traditional automobiles. In 2021, the sales-weighted median price of electric vehicles in China was just 10% higher than conventional vehicles, compared to 45-50% in other key countries. China accounts for 95% of new electric two- and three-wheeler vehicle registrations, as well as 90% of new electric bus and truck registrations worldwide.

- China intends to create a special agency to encourage collaboration between domestic enterprises and international semiconductor powerhouses, like Intel, in order to build software, material, and manufacturing equipment development centers. Beijing is rushing to develop a domestic supply chain for semiconductors that is not subject to US sanctions. Foreign governments, on the other hand, are likely to be suspicious of this initiative, fearing the transfer of vital technology to China.

- In September 2021, Semiconductor Manufacturing International Corp. (SMIC), China's largest contract chipmaker, announced the establishment of a new plant in the Lin-Gang Special Area, which is part of Shanghai's free trade zone. The proposed USD 8.87 billion foundry is expected to produce 100,000 12-inch wafers per month. SMIC will own at least 51% of the joint venture, with a 25% interest held by a Shanghai, government-designated investment company. SMIC stated in March that it would partner with the Shenzhen government to invest USD 2.35 billion in a project to produce 40,000 12-inch wafers per month using 28nm and higher integrated circuits.

- China has enacted plenty of beneficial regulations for the semiconductor and software industries, including tax rebates, attractive financing, IP protection, and support for R&D, import and export, and talent development, among other things. Tax exemptions and discounts will be available to IC manufacturing companies, as well as IC design, equipment, materials, packaging, testing, and software companies.

Get Analysis on Important Geographic Markets

Download PDF