| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 80.81 Billion |

| Market Size (2030) | USD 137.03 Billion |

| CAGR (2025 - 2030) | 11.14 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order |

Automotive Semiconductor Market Analysis

The Automotive Semiconductor Market size is estimated at USD 80.81 billion in 2025, and is expected to reach USD 137.03 billion by 2030, at a CAGR of 11.14% during the forecast period (2025-2030).

The automotive semiconductor industry is undergoing a profound transformation driven by technological advancement and changing consumer preferences. According to the International Organization of Motor Vehicle Manufacturers (OICA), global automobile production reached over 93 million units in 2023, marking a significant 10% increase from the previous year. This surge in production has been accompanied by the integration of advanced technologies such as 3D mapping applications, sophisticated infotainment systems, and enhanced connectivity features. The industry's evolution is particularly evident in the standardization of connectivity solutions, with A-PHY (serializer-deserializer physical layer interface) emerging as the dominant solution for in-vehicle communications.

The electrification of vehicles continues to reshape the automotive semiconductor landscape, with manufacturers incorporating increasingly sophisticated electronic components. According to the International Energy Agency, electric car sales reached approximately 14 million units in 2023, with 95% of these sales concentrated in China, Europe, and the United States. This shift towards electrification has catalyzed the development of advanced power management systems, battery management solutions, and enhanced motor control units, all requiring specialized electric vehicle semiconductor components designed to optimize performance and efficiency.

The integration of semiconductors in modern vehicles extends far beyond basic functionalities, encompassing complex systems for safety, entertainment, and vehicle management. These vehicles now feature sophisticated electronic control units (ECUs), advanced driver assistance systems (ADAS), and high-performance computing platforms. According to Intel, a single autonomous vehicle can generate an average of 4 terabytes of daily data, necessitating robust automotive semiconductor solutions capable of processing and analyzing vast amounts of information in real-time.

The industry is witnessing a significant push toward autonomous driving capabilities, with manufacturers investing heavily in semiconductor technologies that enable advanced sensing, processing, and decision-making capabilities. The World Economic Forum projects that by 2035, more than 12 million fully autonomous cars will be sold annually, representing approximately 25% of the global automotive market. This transition is driving demand for specialized semiconductors in applications such as LiDAR sensors, radar systems, and sophisticated image processing units, while also necessitating the development of more powerful and efficient semiconductor solutions to handle the increasing computational requirements of autonomous vehicles.

Automotive Semiconductor Market Trends

Increasing Vehicle Production

The automotive industry is experiencing substantial growth in vehicle production, driving increased demand for automotive electronics and automotive semiconductor components across various applications. According to the International Organization of Motor Vehicle Manufacturers (OICA), global vehicle production reached 93,546,599 units in 2023, demonstrating the industry's robust manufacturing capabilities. This surge in production is complemented by the rapid advancement of electric vehicles, with global electric car sales reaching nearly 14 million in 2023, representing a 35% year-on-year growth. The first quarter of 2024 continued this momentum, with electric car sales surpassing the previous year's figures by approximately 25%, totaling over 3 million units sold.

The transformation of the automotive sector is further evidenced by manufacturers' increasing focus on incorporating advanced electronics and semiconductor-dependent features in their vehicles. For instance, modern vehicles require between 200 to 300 semiconductors for gas and diesel-powered vehicles, while self-driving cars of autonomous level 3 or above may require up to 2,000 chips. The industry is witnessing significant investments in production capabilities, with companies like Continental launching new plants and expanding their manufacturing footprint. In June 2023, Continental and its joint venture partner Nisshinbo Holdings inaugurated a new plant in Gurugram to produce valve blocks for Continental's electronic brake systems, demonstrating the industry's commitment to expanding semiconductor-dependent component production.

Understand The Key Trends Shaping This Market

Download PDF

Rising Demand for Advanced Safety and Comfort Systems

The automotive industry is experiencing a paradigm shift as consumer preferences evolve towards vehicles equipped with advanced safety features and enhanced comfort systems, driving substantial demand for automotive semiconductors. The European Union's mandate for ADAS systems beginning mid-2024, coupled with the United Nations' introduction of new regulations for additional driver assistance systems (DCAS and ADAS) in January 2025, is creating a robust framework for safety system adoption. These regulatory changes are compelling automotive manufacturers to integrate more sophisticated ADAS semiconductor solutions into their vehicles, particularly in the realm of sensors and processors that enable critical safety features such as adaptive cruise control and automatic emergency braking systems.

The increasing emphasis on vehicle comfort and luxury features is further accelerating semiconductor demand in the automotive sector. Modern vehicles are increasingly incorporating advanced entertainment and data connectivity systems, either through built-in communication modules or smart device integration. This trend is particularly evident in the rising adoption of sophisticated infotainment systems, premium audio solutions, and enhanced user interfaces. For instance, in September 2023, Dolby expanded its presence in the automotive sector, partnering with prestigious brands like Maybach, Mercedes-Benz, Volvo, Polestar, and Lotus to integrate advanced audio systems. Additionally, the industry is witnessing innovations in comfort-oriented technologies, as exemplified by Honda's launch of the AI-based Scenic Audio App in April 2024, designed to enhance travel experiences for visually impaired passengers, demonstrating the industry's commitment to developing inclusive comfort features. The integration of automotive microcontroller and automotive integrated circuit technologies is pivotal in supporting these advancements.

Segment Analysis: By Vehicle Type

Passenger Vehicle Segment in Automotive Semiconductor Market

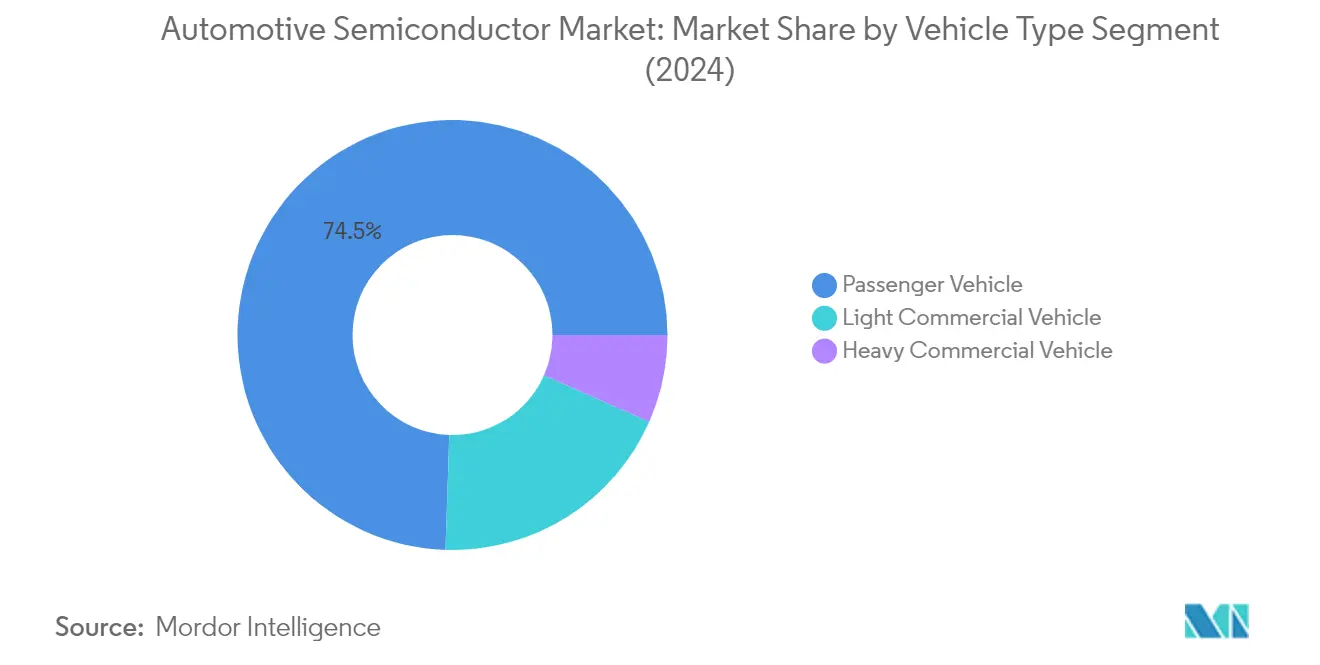

The passenger vehicle segment dominates the automotive semiconductor market, commanding approximately 75% market share in 2024. This substantial market presence is primarily driven by the increasing integration of advanced electronics and semiconductor components in modern passenger vehicles. The rising demand for safety technologies in passenger vehicles is propelling the global demand for automotive semiconductors, particularly with the broad implementation of advanced driver assistance systems (ADAS). Additionally, the segment's growth is further bolstered by the rapid adoption of electric vehicles, which require a significantly higher number of semiconductors compared to traditional vehicles. The integration of sophisticated features such as infotainment systems, advanced safety features, and electrification solutions has made passenger vehicles the primary consumer of automotive semiconductors, including automotive microcontrollers and automotive processors.

Heavy Commercial Vehicle Segment in Automotive Semiconductor Market

The heavy commercial vehicle segment is projected to exhibit the highest growth rate in the automotive semiconductor market, with an expected CAGR of approximately 14% during the forecast period 2024-2029. This remarkable growth is primarily attributed to the increasing adoption of advanced technology solutions, including accident prevention systems, ADAS, efficient driving systems, and engine management systems. The segment's growth is further accelerated by stringent emission regulations and safety standards, compelling manufacturers to incorporate more sophisticated semiconductor solutions. The integration of automated emergency braking systems and forward-collision warnings in heavy-duty vehicles has become increasingly prevalent, as these features have demonstrated significant potential in reducing rear-end incidents involving large trucks.

Remaining Segments in Vehicle Type

The light commercial vehicle segment represents a significant portion of the automotive semiconductor market, bridging the gap between passenger vehicles and heavy commercial vehicles. This segment is experiencing substantial transformation with the integration of real-time delivery tracking systems, in-vehicle communication systems, and advanced safety features. The growth in e-commerce and last-mile delivery services has particularly influenced the demand for semiconductors in light commercial vehicles. Additionally, the segment is witnessing increased adoption of electric powertrains and advanced driver assistance systems, further driving the demand for semiconductor components in these vehicles.

Segment Analysis: By Component

Integrated Circuits Segment in Automotive Semiconductor Market

The integrated circuits segment dominates the automotive semiconductor market, commanding approximately 34% market share in 2024. This significant market presence is driven by the growing adoption of integrated circuits in various automotive applications, from power electronics to advanced driver assistance systems. The increasing demand for automotive ICs is particularly fueled by the rising popularity of eco-friendly electric vehicles, including hybrid electric vehicles (HEV), electric vehicles (EV), and idle reduction vehicles. The automotive sector employs different types of ICs, including monolithic ICs, hybrid ICs, analog ICs, digital ICs, and digital signal processors (DSPs). The integration of IoT in the automotive sector and the growing investments in EV production are further strengthening the segment's market position.

Sensors Segment in Automotive Semiconductor Market

The sensors segment is emerging as the fastest-growing component in the automotive semiconductor market, projected to grow at approximately 13% during 2024-2029. This remarkable growth is driven by the increasing integration of advanced sensing technologies in modern vehicles, particularly for safety applications and autonomous driving features. The automotive sector relies on various sensors, including airbag deployment sensors, collision-avoidance sensors, temperature sensors, pressure sensors, magnetic sensors, accelerometers, image sensors, actuators, and radars. The rising requirement for features like vehicle stability control, ADAS units, and crash detection systems has directly influenced the demand for sensors. Furthermore, numerous companies are making substantial investments in the development of cutting-edge sensors for the automotive sector, which is projected to boost the growth potential of this segment.

Remaining Segments in Component Segmentation

The automotive semiconductor market encompasses several other vital components, each serving crucial functions in modern vehicles. Automotive processors play a fundamental role in managing vehicle operations and processing data from various systems. Memory devices are essential for storing and accessing critical vehicle data and supporting advanced infotainment systems. Discrete power devices are crucial for power management and control applications, particularly in electric vehicles. RF devices enable various wireless communication capabilities, including vehicle-to-everything (V2X) communication and connectivity features. These components collectively contribute to the advancement of automotive technology, supporting everything from basic vehicle operations to sophisticated autonomous driving features.

Segment Analysis: By Application

Safety Segment in Automotive Semiconductor Market

The safety segment dominates the automotive semiconductor market, commanding approximately 26% of the total market share in 2024. This significant market position is driven by the increasing integration of semiconductor technology in advanced safety and driver assistance systems. The segment's growth is fueled by the rising demand for features like backup cameras, blind-spot detection, adaptive cruise control, lane change assistance, airbag deployment, and emergency braking systems. Many governments worldwide are implementing crucial safety standards to standardize systems across all vehicles, with several countries mandating advanced driver assistance systems (ADAS) in new vehicles. The integration of semiconductor technology enables intelligent features and enhanced safety capabilities, making vehicles safer and more reliable on the roads.

Power Electronics Segment in Automotive Semiconductor Market

The automotive power electronics segment is experiencing remarkable growth, projected to expand at approximately 13% CAGR from 2024 to 2029. This growth is primarily driven by the increasing adoption of electric vehicles and their heavy reliance on power electronics compared to traditional gasoline vehicles. These vehicles require a greater number of semiconductors to manage various functionalities related to power flow and conversion, including electric motors, battery management systems, and converters. The segment's growth is further supported by compliance with forthcoming safety and vehicle emission norms, rising demand for vehicle connectivity, infotainment, and powertrain electrification. The Asia-Pacific region is particularly driving this growth through its established semiconductor industry, government support, and presence of EV manufacturing hubs.

Remaining Segments in Application Segmentation

The automotive semiconductor market encompasses several other vital segments including body electronics, comfort/entertainment units, and chassis applications. The body electronics segment plays a crucial role in vehicle personalization and advanced user interfaces, while the comfort/entertainment unit segment focuses on enhancing the in-vehicle experience through sophisticated infotainment systems. The chassis segment contributes to vehicle stability and performance through electronic stability control and anti-lock braking systems. Each of these segments serves specific functions in modern vehicles, from controlling basic operations to providing advanced features that enhance the overall driving experience. The continuous evolution of these segments reflects the automotive industry's shift towards more sophisticated and electronically-controlled vehicles.

Automotive Semiconductor Market Geography Segment Analysis

Automotive Semiconductor Market in North America

The North American automotive semiconductor market holds approximately 19% of the global market share in 2024, establishing itself as a crucial region in the global landscape. The region's prominence is largely driven by the United States' push for safer vehicles through advancing technology, with Texas Instruments leading the way in ultrasound, lidar, cameras, radar, and sensor technology offerings. The steady expansion of the automotive sector is fueling increased demand for semiconductors across various vehicle components. The presence of major automotive semiconductor companies in the US market acts as a significant catalyst for growth, with companies heavily investing in innovative technologies specifically designed for automotive semiconductors. The region's semiconductor manufacturers must adhere to stringent ISO 26262 standards, particularly for electric and electronic control systems in vehicles. This standard focuses on ensuring the functional safety of automotive systems, encompassing both electronic and software elements. The automotive industry's increased reliance on semiconductors is primarily driven by the shift toward autonomous, connected, electric, and shared mobility, with most new vehicles featuring advanced driver assistance systems and connectivity features.

Automotive Semiconductor Market in Europe

Europe's automotive semiconductor market landscape has demonstrated robust growth, with an approximate growth rate of 10% from 2019 to 2024, reflecting the region's strong manufacturing capabilities and technological innovation. The region's semiconductor production is characterized by a significant presence of small and medium-sized enterprises, with chip production facilities distributed evenly across European nations. German automobile manufacturers are strengthening their positions through the integration of connected vehicle technologies, with companies like Audi and Mercedes establishing cutting-edge R&D hubs. The European Commission's Digital Compass Plan aims to double the current chip manufacturing capacity while securing a 20% share of the global chip market. The region benefits from the presence of key players like Infineon Technologies AG, which maintains a comprehensive presence across the entire semiconductor ecosystem. Multiple initiatives across the European Union are actively working to increase local production of computer chips and semiconductors, demonstrating the region's commitment to semiconductor independence and technological advancement.

Automotive Semiconductor Market in Asia-Pacific

The Asia-Pacific automotive semiconductor market is projected to grow at a robust CAGR of approximately 12% during 2024-2029, positioning itself as the fastest-growing region globally. The increased automotive manufacturing and deepening partnerships between automotive OEMs and semiconductor manufacturers are driving the market's expansion. The region's buyers are increasingly prioritizing vehicle comfort and luxury features over traditional factors like cost and fuel efficiency. Global automakers are responding to the rising demand for luxury and semi-luxury vehicles by incorporating more electronic components. The surge in demand for electric vehicles is further propelling the sector's growth, with manufacturers facing pressure to innovate and introduce self-driving technologies. Both the automotive and semiconductor sectors are intensifying their focus on technology enhancements and raw material negotiations, with companies like NVIDIA collaborating with Toyota to enhance autonomous driving capabilities. China's emphasis on safety features, the rise of infotainment applications, and the growing popularity of ADAS systems are significant drivers of market growth.

Automotive Semiconductor Market in Latin America

The Latin American automotive semiconductor industry is experiencing significant transformation, particularly in key markets like Argentina, Brazil, Mexico, and Colombia. The region is witnessing substantial technological advancements, evolving market trends, and economic developments that are reshaping its automotive landscape. The automotive sector serves both local markets and demonstrates significant export potential, with major OEMs and suppliers rapidly adjusting to industry shifts. The adoption rates of electric vehicles, both historical and projected, paint a promising picture for the region's semiconductor industry. Government policies across these nations are increasingly pushing for a transition to battery-powered vehicles, each with its unique approach, collectively steering Latin America's automotive semiconductor industry toward a more sustainable future. The region's transportation infrastructure is showing positive development, with manufacturers demonstrating resilience in production capacity despite global challenges. These enhancements in the automotive landscape are amplifying semiconductor demand, contributing to the overall growth of the automotive semiconductor sector in Latin America.

Automotive Semiconductor Market in Middle East & Africa

The Middle East & Africa region's automotive semiconductor market is experiencing dynamic growth driven by anticipated high discretionary income among the population. The automotive sector in this region is witnessing rapid development, directly impacting car adoption rates and semiconductor demand. Automakers are increasingly equipping their new vehicles with advanced entertainment and data connectivity systems, either through in-built communication modules or smart gadgets. The United Arab Emirates' automotive landscape, dominated by passenger cars, is attracting foreign manufacturers to establish local operations. Sub-Saharan African nations are showing a pressing need for alternative transportation energy sources, particularly given their abundant renewable energy resources. This shift is crucial to reduce the mounting burden of fuel dependency and subsidies, with electric vehicles emerging as a promising solution to these challenges. Looking ahead, a significant uptick in power generation investments is anticipated for many Sub-Saharan African countries, opening numerous opportunities for semiconductor applications within the automotive sector.

Get Analysis on Important Geographic Markets

Download PDF

Automotive Semiconductor Industry Overview

Top Companies in Automotive Semiconductor Market

The automotive semiconductor companies market is led by prominent players including NXP Semiconductors, Infineon Technologies, Renesas Electronics, STMicroelectronics, Texas Instruments, and Robert Bosch GmbH. These leading automotive semiconductor companies are driving innovation through extensive R&D investments in advanced driver assistance systems (ADAS), electric vehicle technologies, and autonomous driving capabilities. Operational agility is demonstrated through strategic manufacturing expansions and supply chain optimizations, with companies like TSMC and major players establishing new fabrication facilities globally. The industry is witnessing increased strategic partnerships and collaborations, particularly in developing specialized chips for electric vehicles and autonomous driving applications. Market leaders are also expanding their geographical presence through strategic acquisitions and joint ventures, especially in emerging markets, while simultaneously strengthening their product portfolios in areas such as power management, sensors, and microcontrollers.

Market Consolidation Drives Industry Evolution Forward

The automotive semiconductor landscape is characterized by a mix of global technology conglomerates and specialized semiconductor manufacturers, with major players maintaining significant market share in automotive semiconductors through their established technological capabilities and extensive distribution networks. The market structure shows a high degree of consolidation, particularly among top-tier manufacturers who possess advanced manufacturing capabilities and strong intellectual property portfolios. The industry has witnessed numerous strategic mergers and acquisitions, with companies seeking to enhance their technological capabilities, expand their product offerings, and strengthen their market position in specific geographic regions. These consolidation activities have been particularly focused on acquiring expertise in emerging technologies such as artificial intelligence, machine learning, and advanced sensor technologies.

The competitive dynamics are further shaped by the presence of regional players who specialize in specific semiconductor components or serve particular geographic markets. Major semiconductor manufacturers are increasingly forming strategic alliances with automotive OEMs and tier-1 suppliers to develop customized solutions and secure long-term supply agreements. The industry also sees significant collaboration between established players and technology startups, particularly in developing innovative solutions for electric vehicles and autonomous driving applications. The market's competitive intensity is heightened by the entry of new players from adjacent industries, especially in emerging markets where government support and increasing domestic demand create favorable conditions for market entry.

Innovation and Adaptability Key to Success

Success in the automotive semiconductor market increasingly depends on companies' ability to innovate while maintaining operational efficiency and supply chain resilience. Incumbent automotive semiconductor companies are focusing on strengthening their market position through increased R&D investments, particularly in developing advanced semiconductor technologies for electric vehicles and autonomous driving systems. Companies are also emphasizing the importance of building strong relationships with automotive manufacturers and tier-1 suppliers, while simultaneously expanding their manufacturing capabilities to meet growing demand. The ability to adapt to rapidly changing technological requirements and maintain high-quality standards while meeting stringent automotive safety regulations has become crucial for market success.

For contenders looking to gain market share, the focus needs to be on developing specialized solutions for specific applications or regional markets while building strong partnerships with established automotive manufacturers. The concentration of end-users in the automotive industry necessitates a strategic approach to customer relationship management and long-term supply agreements. While the risk of substitution is relatively low due to the specialized nature of automotive semiconductors, companies must continue to innovate to maintain their competitive edge. Regulatory requirements, particularly regarding vehicle safety and emissions, continue to drive demand for advanced semiconductor solutions, making compliance capabilities a critical success factor. The ability to navigate complex supply chains and maintain reliable production capabilities has become increasingly important in light of recent global supply chain disruptions.

Automotive Semiconductor Market Leaders

-

NXP Semiconductor NV

-

Infineon Technologies AG

-

Renesas Electronics Corporation

-

STMicroelectronics NV

-

Toshiba Electronic Devices & Storage Corporation (Toshiba Corporation)

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Automotive Semiconductor Market News

- April 2024: Infineon Technologies AG solidified its dominance in the automotive semiconductor market. TechInsights reported that Infineon bolstered its market share across all regions and maintained its top position in South Korea and China. Notably, Infineon achieved substantial progress in the Japanese automotive semiconductor sector. Infineon reinforced its standing as the second-largest player in Europe and secured a spot in the top three in North America.

- April 2024: Renesas Electronics Corporation, a premier supplier of advanced semiconductor solutions, announced that it started operations at its Kofu Factory, located in Kai City, Yamanashi Prefecture, Japan. Renesas aims to boost its production capacity of power semiconductors in anticipation of the growing demand for electric vehicles (EVs).

Automotive Semiconductor Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

- 4.1 Market Overview

-

4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Intensity of Competitive Rivalry

- 4.2.5 Threat of Substitute Products

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of the Impact of COVID-19 and Other Macroeconomic Trends on the Market

- 4.5 Overview of RF Device Demand in Autonomous Vehicles

5. MARKET DYNAMICS

-

5.1 Market Drivers

- 5.1.1 Increasing Vehicle Production

- 5.1.2 Rising Demand for Advanced Safety and Comfort Systems

-

5.2 Market Restraints

- 5.2.1 Higher Cost of Advanced Featured Vehicles

6. MARKET SEGMENTATION

-

6.1 By Vehicle Type

- 6.1.1 Passenger Vehicle

- 6.1.2 Light Commercial Vehicle

- 6.1.3 Heavy Commercial Vehicle

-

6.2 By Component

- 6.2.1 Processors

- 6.2.2 Sensors

- 6.2.3 Memory Devices

- 6.2.4 Integrated Circuits

- 6.2.5 Discrete Power Devices

- 6.2.6 RF Devices

-

6.3 By Application

- 6.3.1 Chassis

- 6.3.2 Power Electronics

- 6.3.3 Safety

- 6.3.4 Body Electronics

- 6.3.5 Comforts/Entertainment Unit

- 6.3.6 Other Applications

-

6.4 By Geography***

- 6.4.1 North America

- 6.4.2 Europe

- 6.4.3 Asia

- 6.4.4 Australia and New Zealand

- 6.4.5 Latin America

- 6.4.6 Middle East and Africa

7. COMPETITIVE LANDSCAPE

-

7.1 Company Profiles*

- 7.1.1 NXP Semiconductor NV

- 7.1.2 Infineon Technologies AG

- 7.1.3 Renesas Electronics Corporaton

- 7.1.4 STMicroelectronics NV

- 7.1.5 Toshiba Electronic Devices & Storage Corporation (Toshiba Corporation)

- 7.1.6 Texas Instrument Inc.

- 7.1.7 Robert Bosch GmbH

- 7.1.8 Micron Technology

- 7.1.9 Onsemi (Semiconductor Components Industries LLC)

- 7.1.10 Analog Devices Inc.

- 7.1.11 ROHM Co. Ltd

8. INVESTMENT ANALYSIS

9. FUTURE TRENDS

**Subject to Availability

***In the final report, Asia, Australia, and New Zealand will be studied together as 'Asia Pacific'

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Automotive Semiconductor Industry Segmentation

The market for automotive semiconductors was evaluated by analyzing the market sizes of different components used in the automotive industry, such as sensors, processors, memory devices, discrete power devices, and integrated circuits. The report’s scope comprises analyzing various vehicle types worldwide, including light commercial vehicles, heavy commercial vehicles, and passenger vehicles.

The automotive semiconductor is segmented by vehicle type (passenger vehicle, light commercial vehicle, and heavy commercial vehicle), component (processors, sensors, memory devices, integrated circuits, discrete power devices, and RF devices), application (chassis, power electronics, safety, body electronics, comfort/entertainment unit, and other applications), and geography (North America, Europe, Asia-Pacific, Latina America, and Middle East & Africa). The report offers the market size in value terms in USD for all the abovementioned segments.

| By Vehicle Type | Passenger Vehicle |

| Light Commercial Vehicle | |

| Heavy Commercial Vehicle | |

| By Component | Processors |

| Sensors | |

| Memory Devices | |

| Integrated Circuits | |

| Discrete Power Devices | |

| RF Devices | |

| By Application | Chassis |

| Power Electronics | |

| Safety | |

| Body Electronics | |

| Comforts/Entertainment Unit | |

| Other Applications | |

| By Geography*** | North America |

| Europe | |

| Asia | |

| Australia and New Zealand | |

| Latin America | |

| Middle East and Africa |

Need A Different Region or Segment?

Customize Now

Automotive Semiconductor Market Research FAQs

How big is the Automotive Semiconductor Market?

The Automotive Semiconductor Market size is expected to reach USD 80.81 billion in 2025 and grow at a CAGR of 11.14% to reach USD 137.03 billion by 2030.

What is the current Automotive Semiconductor Market size?

In 2025, the Automotive Semiconductor Market size is expected to reach USD 80.81 billion.

Who are the key players in Automotive Semiconductor Market?

NXP Semiconductor NV, Infineon Technologies AG, Renesas Electronics Corporation, STMicroelectronics NV and Toshiba Electronic Devices & Storage Corporation (Toshiba Corporation) are the major companies operating in the Automotive Semiconductor Market.

Which is the fastest growing region in Automotive Semiconductor Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Automotive Semiconductor Market?

In 2025, the Asia Pacific accounts for the largest market share in Automotive Semiconductor Market.

What years does this Automotive Semiconductor Market cover, and what was the market size in 2024?

In 2024, the Automotive Semiconductor Market size was estimated at USD 71.81 billion. The report covers the Automotive Semiconductor Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Automotive Semiconductor Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Automotive Semiconductor Market Research

Mordor Intelligence delivers a comprehensive analysis of the automotive semiconductor industry. We leverage decades of expertise in automotive electronics research and consulting. Our detailed examination covers crucial segments, including automotive SoC technologies, automotive MCU implementations, and automotive power electronics systems. The report provides an in-depth analysis of automotive processor developments and automotive microcontroller innovations. It also highlights emerging trends in vehicle semiconductor technologies, with a particular emphasis on automotive integrated circuit advancements.

Stakeholders across the automotive electronics industry benefit from our thorough investigation of electric vehicle semiconductor applications and ADAS semiconductor technologies. The report is available as an easy-to-download PDF and delivers actionable insights into automotive power electronics market dynamics and the evolution of the automotive SoC market. Our analysis encompasses the entire spectrum of car semiconductor companies, offering valuable intelligence on automotive microcontroller market trends and automotive electronics market developments. The comprehensive coverage includes a detailed examination of automotive MCU market opportunities and emerging segments in the ADAS semiconductor market.