Market Size of Automotive Passive Electronic Components Industry

| Study Period | 2019 - 2029 |

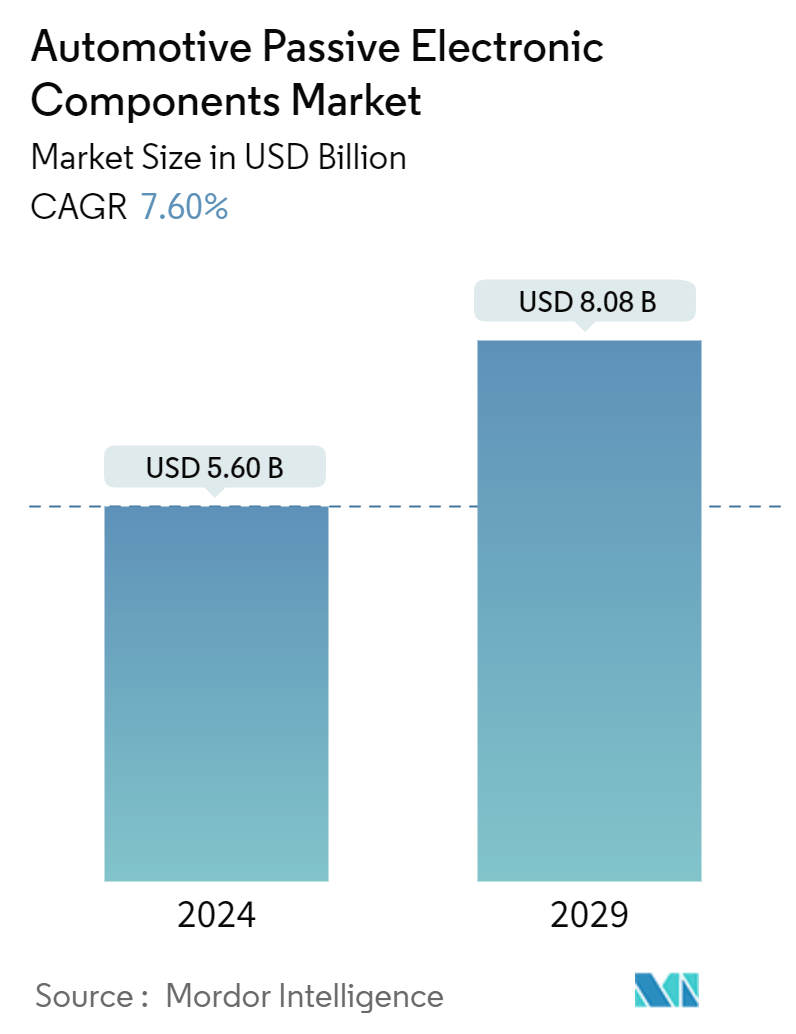

| Market Size (2024) | USD 5.60 Billion |

| Market Size (2029) | USD 8.08 Billion |

| CAGR (2024 - 2029) | 7.60 % |

| Fastest Growing Market | Europe |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Automotive Passive Electronic Components Market Analysis

The Automotive Passive Electronic Components Market size is estimated at USD 5.60 billion in 2024, and is expected to reach USD 8.08 billion by 2029, growing at a CAGR of 7.60% during the forecast period (2024-2029).

- The automotive industry is leading the way in the increasing need for passive components. The demand for electronic vehicle systems is rising for various uses, such as electronic control units (ECUs) under the hood, infotainment systems, and advanced driver assistance systems (ADASs). Automotive electronic systems require high-quality components to guarantee dependable performance, like capacitors for filtering and storing energy, varistors for circuit protection, connectors for small ECUs, and RF and microwave passive components and antennas for connectivity support.

- Automobile manufacturers increasingly integrate electronic components into traditional combustion engine vehicles to enhance fuel efficiency, reduce emissions, and improve overall vehicle performance. This trend drives the demand for passive electronic components like resistors, capacitors, and inductors. For instance, according to SIAM India, during the fiscal year 2023, more than 3.89 million passenger vehicles were sold in the domestic market.

- ADAS (advanced driver assistance systems), such as collision avoidance systems and adaptive cruise control, rely heavily on passive electronic components like capacitors for sensor signal processing, filtering, and data transmission. Modern vehicles feature advanced infotainment systems, telematics, and connectivity solutions that require passive components for wireless communication, signal processing, and data transmission.

- As automotive electronics become more compact and integrated, passive components must meet increasingly stringent size and weight requirements. Miniaturization challenges, such as maintaining performance while reducing package size, can limit market growth. In addition, designing and manufacturing automotive-grade passive electronic components require significant research, development, and testing. High development costs limit innovation in the market.

- Environmental concerns, including sustainability and climate change, influence automotive industry trends and regulations. Growing emphasis on ecological sustainability may drive the adoption of vehicles' energy-efficient and environmentally friendly electronic components. Moreover, trade policies, tariffs, and trade agreements can impact the cost and availability of automotive components. Changes in trade policies may disrupt supply chains, affect pricing, and influence market competition.

Automotive Passive Electronic Components Industry Segmentation

For market estimation, the revenue generated from the sale of automotive passive electronic components offered by various market players for a wide range of applications is considered. Market trends are evaluated by analyzing product innovation, diversification, and expansion investments. Further, advancements in inductors, resistors, and MEC filters are crucial in determining the market's growth.

The automotive passive electronic components market is segmented by type (capacitors [ceramic capacitors, tantalum capacitors, aluminum electrolytic capacitors, paper and plastic film capacitors, supercapacitors], inductors, and resistors [surface-mounted chips, network and array, and other specialty], and EMC filters)) and geography (North America, Europe, Asia-Pacific, Middle East & Africa, and Latin America). The report offers the market size and forecasts for all the above segments in value (USD).

| By Type | |||||||

| |||||||

| Inductors | |||||||

| |||||||

| EMC Filters |

| By Geography*** | |

| North America | |

| Europe | |

| Asia | |

| Australia and New Zealand | |

| Middle East and Africa | |

| Latin America |

Automotive Passive Electronic Components Market Size Summary

The automotive passive electronic components market is experiencing significant growth, driven by the increasing integration of electronic systems in vehicles. This trend is fueled by the rising demand for advanced vehicle technologies such as electronic control units, infotainment systems, and advanced driver assistance systems. These systems require high-quality passive components like capacitors, varistors, and connectors to ensure reliable performance. The automotive industry is also focusing on enhancing fuel efficiency and reducing emissions by incorporating electronic components into traditional combustion engine vehicles. This has led to a growing demand for resistors, capacitors, and inductors, which are essential for optimizing energy usage and minimizing power losses. The market is characterized by rapid advancements in capacitor technology, enabling the development of smaller and more efficient components that support the compact and lightweight design of modern vehicles.

The market landscape is highly competitive, with major players like Yageo Corporation, Panasonic Corporation, and TDK Corporation holding significant market shares. These companies are actively expanding their global presence through collaborations, partnerships, and acquisitions to gain a competitive edge. The European market, in particular, is witnessing rapid growth due to the increasing adoption of electric and hybrid vehicles, driven by government incentives and technological advancements. This shift towards electrified powertrains is boosting the demand for passive electronic components used in electric drivetrains and battery management systems. Additionally, environmental concerns and stringent government regulations are influencing market trends, encouraging the adoption of energy-efficient and environmentally friendly components. The market's growth is further supported by strategic investments and expansions by key players, aiming to meet the evolving demands of the automotive industry.

Automotive Passive Electronic Components Market Size - Table of Contents

-

1. MARKET INSIGHTS

-

1.1 Market Overview

-

1.2 Industry Attractiveness - Porter's Five Forces Analysis

-

1.2.1 Threat of New Entrants

-

1.2.2 Bargaining Power of Buyers/Consumers

-

1.2.3 Bargaining Power of Suppliers

-

1.2.4 Threat of Substitute Products

-

1.2.5 Intensity of Competitive Rivalry

-

-

1.3 Technology Snapshot

-

1.4 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

-

-

2. MARKET SEGMENTATION

-

2.1 By Type

-

2.1.1 Capacitors

-

2.1.1.1 Ceramic Capacitors

-

2.1.1.2 Tantalum Capacitors

-

2.1.1.3 Aluminum Electrolytic Capacitors

-

2.1.1.4 Paper and Plastic Film Capacitors

-

2.1.1.5 Supercapacitors

-

-

2.1.2 Inductors

-

2.1.3 Resistors

-

2.1.3.1 Surface-mounted Chips

-

2.1.3.2 Network and Array

-

2.1.3.3 Other Specialty

-

-

2.1.4 EMC Filters

-

-

2.2 By Geography***

-

2.2.1 North America

-

2.2.2 Europe

-

2.2.3 Asia

-

2.2.4 Australia and New Zealand

-

2.2.5 Middle East and Africa

-

2.2.6 Latin America

-

-

Automotive Passive Electronic Components Market Size FAQs

How big is the Automotive Passive Electronic Components Market?

The Automotive Passive Electronic Components Market size is expected to reach USD 5.60 billion in 2024 and grow at a CAGR of 7.60% to reach USD 8.08 billion by 2029.

What is the current Automotive Passive Electronic Components Market size?

In 2024, the Automotive Passive Electronic Components Market size is expected to reach USD 5.60 billion.