| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 48.99 Billion |

| Market Size (2030) | USD 66.14 Billion |

| CAGR (2025 - 2030) | 6.19 % |

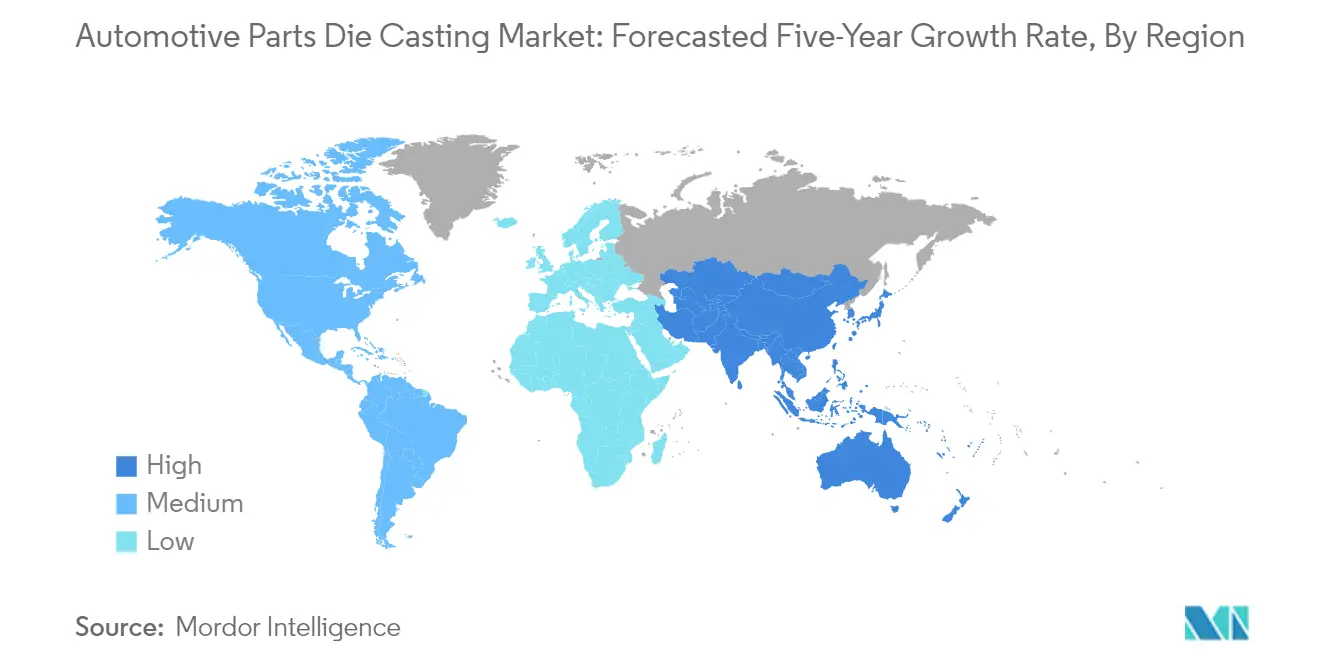

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Automotive Parts Die Casting Market Analysis

The Automotive Parts Die Casting Market size is estimated at USD 48.99 billion in 2025, and is expected to reach USD 66.14 billion by 2030, at a CAGR of greater than 6.19% during the forecast period (2025-2030).

The automotive parts die casting market is experiencing significant transformation driven by technological advancements and changing manufacturing paradigms. Global vehicle production reached approximately 85 million units in 2022, highlighting the robust demand for automotive metal components and die-cast parts. The industry has witnessed substantial innovations in automotive die casting technologies, particularly in machine design, process control, and mold technologies, leading to improved efficiency and quality of die casting operations. The integration of automation and digital technologies, including computer-aided engineering (CAE) and the Internet of Things (IoT), has revolutionized production processes, resulting in reduced lead times and enhanced productivity across manufacturing facilities.

The industry landscape is being reshaped by significant investments and technological collaborations among key players. In January 2024, Neta announced its collaboration with LK Technology to develop a die-casting machine exceeding 20,000 tons, aimed at streamlining manufacturing processes and reducing production costs. This trend is further exemplified by Minglida Precision Technology's USD 100 million investment in December 2023 to establish a new production facility in Mexico, focusing on manufacturing aluminum profiles and die-cast components for various sectors, including automotive and energy storage.

The market is witnessing a notable shift towards advanced manufacturing techniques and material optimization. According to the World Bank, aluminum die casting prices reached USD 2,705 per metric ton in 2022, influencing manufacturing strategies and material selection processes. Companies are increasingly adopting innovative die-casting solutions, as demonstrated by Tesla's implementation of die-casting technology for rear underbody assembly in September 2023, which achieved a 40% reduction in manufacturing costs and a 10% decrease in vehicle body system weight compared to traditional methods. These advancements are driving the industry towards more efficient and cost-effective production processes.

The industry is experiencing a significant evolution in terms of global manufacturing footprint and capacity expansion. In 2023, Xusheng, a prominent die-casting company, initiated the construction of a new facility in Mexico's Alianza Derramadero Industrial Park, specifically designed for manufacturing aluminum alloy auto parts for the automotive and e-mobility sectors. This expansion trend is complemented by the integration of smart manufacturing practices, including real-time monitoring systems and advanced quality control mechanisms. The implementation of these technologies has significantly enhanced the precision and reliability of die-cast components, meeting the increasingly stringent quality standards of the automotive industry.

Automotive Parts Die Casting Market Trends

Increasing Electric Vehicle Production

The rapid acceleration of electric vehicle production has emerged as a primary driver for the automotive parts die-casting market, fundamentally transforming manufacturing requirements and component designs. Global battery electric vehicle sales reached 7.3 million units in 2022, demonstrating the industry's dramatic shift toward electrification. This transition has intensified the demand for lightweight, high-performance components, as electric vehicles require specialized parts like battery housings, motor housings, and structural components that are particularly suited to aluminum die casting processes.

The industry has witnessed significant technological advancement in response to EV manufacturing needs, exemplified by recent developments in 2023. In January 2024, Neta, the Chinese electric vehicle brand, announced plans to collaborate with Hong Kong-based LK Technology to develop die-casting machines exceeding 20,000 tons, aiming to streamline manufacturing processes and reduce production costs. Additionally, electric vehicles are projected to use 25-27% more aluminum by weight compared to traditional combustion engine vehicles, with each EV requiring an average of 250 kg of aluminum, highlighting the growing importance of aluminum die casting in the electric vehicle manufacturing ecosystem.

Understand The Key Trends Shaping This Market

Download PDF

Material Versatility Promoting the Industry

The die-casting industry's growth is significantly driven by the versatility of materials available for manufacturing processes, particularly aluminum die casting, zinc die casting, and magnesium die casting, each offering unique properties suited for specific automotive applications. Aluminum die casting enables the production of complex designs with intricate shapes and details, making it ideal for manufacturing lightweight structural components and powertrain parts. Meanwhile, zinc die casting provides superior thermal and electrical conductivity properties, making it particularly valuable for manufacturing power steering systems and brake pad systems.

Recent industry developments highlight the increasing importance of material versatility in die-casting applications. In November 2023, Sinyuan ZM Technology unveiled plans to invest approximately USD 138 million to expand its magnesium alloy parts production capacity for new energy vehicles, demonstrating the industry's commitment to leveraging diverse materials. The ability to utilize different materials allows manufacturers to optimize component design based on specific requirements for strength, weight, and thermal properties, thereby enabling more efficient and innovative automotive solutions.

Improved Production Efficiency

Advanced die-casting techniques have revolutionized automotive manufacturing by significantly enhancing production efficiency through automated processes and innovative technologies. The implementation of high-pressure die-casting (HPDC) technology has enabled manufacturers to replace 70 to 100 individual parts with a single cast component, dramatically reducing assembly complexity and manufacturing time. This advancement has been particularly evident in recent developments, such as Tesla's successful integration of die-casting technology in their Model Y vehicle production in China, which achieved a 40% reduction in manufacturing costs and a 10% reduction in vehicle body system weight.

The industry continues to witness significant investments in improving production efficiency through advanced die-casting technologies. In July 2023, Ryobi, a major Japanese provider of aluminum automotive components, announced its plans to manufacture large electric vehicle body parts through "giga casting," promising to decrease car body production costs by 20%. Additionally, in May 2023, UBE Corporation developed an ultra-large die-casting machine specifically designed to reduce production costs for electric vehicle components, demonstrating the industry's ongoing commitment to enhancing manufacturing efficiency through technological innovation. These advancements underscore the critical role of automotive metal casting and automotive foundry processes in the modern automotive industry.

Segment Analysis: Market Size and Growth Rates by Production Process Type

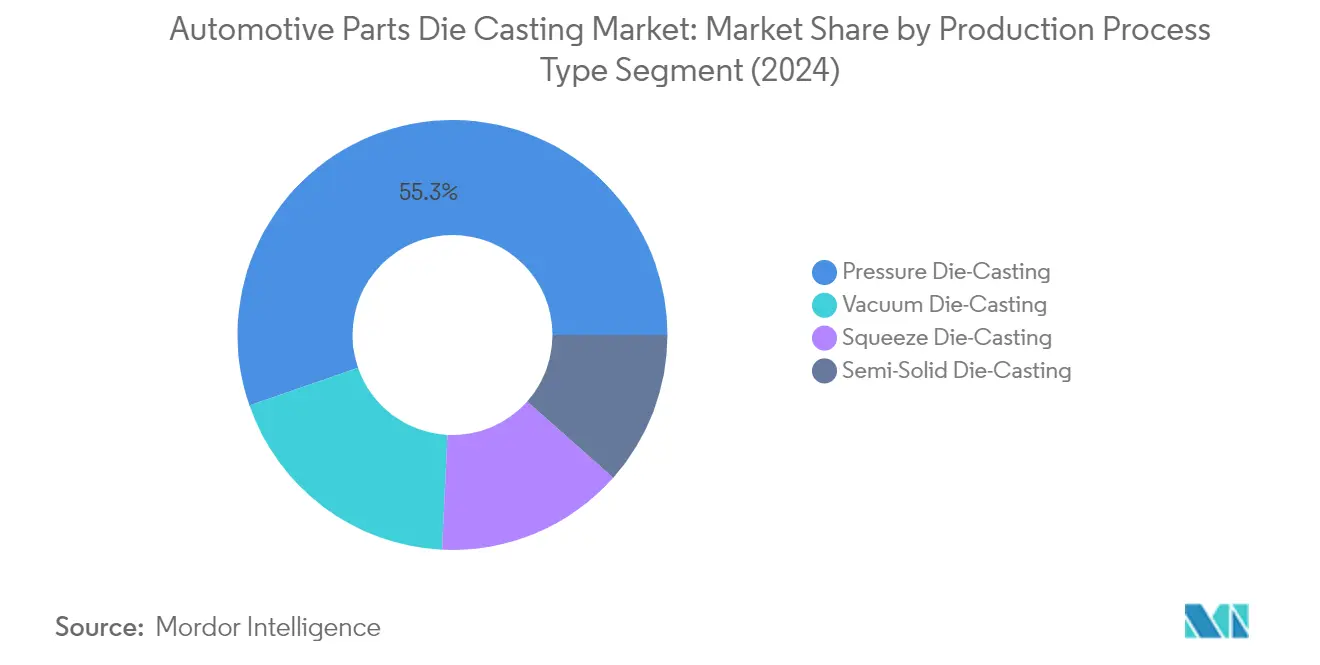

Pressure Die-Casting Segment in Automotive Parts Die Casting Market

Pressure die-casting maintains its dominant position in the automotive parts die casting market, commanding approximately 55% market share in 2024. This significant market presence can be attributed to its superior capabilities in producing intricate and complex components with high precision, making it particularly suitable for manufacturing modern, lightweight vehicle components. The process offers faster cycle times and tighter tolerances compared to other casting methods, enabling manufacturers to produce thin-walled, complex parts efficiently. The segment's leadership is further strengthened by its extensive application in manufacturing engine boxes, gearbox casings, and engine mounts, components that are crucial for both traditional and electric vehicles.

Vacuum Die-Casting Segment in Automotive Parts Die Casting Market

The vacuum die-casting segment demonstrates the strongest growth trajectory in the automotive parts die casting market, projected to grow at approximately 7% during 2024-2029. This robust growth is driven by the increasing demand for high-quality automotive components with minimal porosity, particularly in critical applications such as cylinder heads, stators, and motor covers. The segment's growth is further accelerated by the automotive industry's shift toward electric vehicles, where vacuum die-casting's capability to produce components with superior structural integrity and void-free characteristics becomes particularly valuable. Manufacturers are increasingly adopting this technology for its ability to produce complex components with enhanced mechanical properties and improved surface finish.

Remaining Segments in Production Process Type Market Segmentation

The squeeze die-casting and semi-solid die-casting segments complete the market landscape, each offering unique advantages for specific automotive applications. Squeeze die-casting excels in producing high-density components like aluminum chassis frames and front steering knuckles, combining both casting and forging processes for enhanced durability. Meanwhile, semi-solid die-casting has carved its niche in manufacturing specialized components such as wheels, brake master cylinders, and engine brackets, offering a unique balance between solid metal forging and liquid casting capabilities. Both segments continue to evolve with technological advancements, contributing to the overall market's diversification and technological progression.

Segment Analysis: Market Size and Growth Rates by Raw Material

Aluminum Segment in Automotive Parts Die Casting Market

The aluminum die casting segment continues to dominate the automotive parts die casting market, commanding approximately 82% of the total market share in 2024, driven by the material's exceptional strength-to-weight ratio and superior corrosion resistance capabilities. The segment's prominence is further reinforced by the growing emphasis on vehicle lightweighting to enhance fuel efficiency and reduce carbon emissions, with aluminum die casting being increasingly preferred for manufacturing critical components like engine blocks, transmission housings, and structural parts. The segment is also experiencing the highest growth trajectory with a projected growth rate of nearly 7% from 2024 to 2029, primarily fueled by the rapid expansion of the electric vehicle market, where aluminum die casting components play a crucial role in battery housings and motor casings. Major automotive manufacturers are increasingly incorporating aluminum die-cast parts in their production processes, particularly for electric vehicle components, owing to the material's ability to provide optimal thermal management and structural integrity while maintaining lightweight properties.

Remaining Segments in Raw Material Market Segmentation

The zinc die casting and magnesium die casting segments, along with other raw materials, constitute the remaining portion of the automotive parts die casting market, each serving specific applications based on their unique material properties. Zinc die casting components are particularly valued for their excellent thermal and electrical conductivity properties, making them ideal for power steering systems and brake pad systems. Magnesium die casting parts have gained traction in applications requiring ultra-lightweight solutions, such as steering wheels, roof frames, and engine cradles, benefiting from the material's superior vibration dampening characteristics. Other raw materials, including copper and various alloys, serve niche applications where specific material properties are required, though their market presence remains relatively small compared to the primary materials.

Segment Analysis: Market Size and Growth Rates by Application Type

Body Assemblies Segment in Automotive Parts Die Casting Market

Body assemblies have emerged as the dominant segment in the automotive parts die casting market, commanding approximately 44% market share in 2024. This segment's leadership position is driven by the increasing demand for lightweight vehicle components, particularly door frames, roof panels, and other structural elements that require precision die casting. The growing emphasis on vehicle weight reduction to improve fuel efficiency and meet stringent environmental regulations has further solidified the segment's market position. Additionally, the integration of advanced die-casting techniques such as high-pressure die-casting (HPDC) in automotive body assembly systems has enabled manufacturers to achieve superior dimensional accuracy and structural integrity while reducing manufacturing costs significantly.

Engine Parts Segment in Automotive Parts Die Casting Market

The engine parts segment is projected to demonstrate the strongest growth trajectory in the automotive parts die casting market, with an anticipated growth rate of approximately 8% during the forecast period 2024-2029. This remarkable growth is primarily attributed to the increasing adoption of electric vehicles worldwide and the subsequent demand for specialized engine components and electric battery housings. The segment's expansion is further supported by technological advancements in engine design that require more complex and precise die-cast components. Manufacturers are increasingly investing in advanced die-casting technologies to produce lightweight engine parts that contribute to overall vehicle efficiency while maintaining structural integrity and performance standards.

Remaining Segments in Market Size and Growth Rates by Application Type

The transmission parts and other application types segments continue to play vital roles in shaping the automotive parts die casting market landscape. The transmission parts segment maintains its significance through the production of essential components like gear sets, valve bodies, and transmission housing parts, particularly gaining prominence with the rising adoption of electric and hybrid vehicles. The other application types segment, encompassing suspension, steering, and interior parts, contributes to market diversity by catering to specific automotive manufacturing requirements and emerging technological trends in vehicle design and functionality.

Automotive Parts Die Casting Market Geography Segment Analysis

Automotive Parts Die Casting Market in North America

The North American automotive parts die-casting market demonstrates robust growth driven by technological advancements and increasing demand for lightweight vehicle components. The United States, Canada, and Mexico form the core markets in this region, with each country contributing uniquely to the regional landscape. The region benefits from a well-established automotive manufacturing infrastructure, stringent emission regulations promoting lightweight materials, and increasing electric vehicle adoption. The presence of major automotive manufacturers and their supplier networks further strengthens the market dynamics, while continuous investments in research and development enhance manufacturing capabilities.

Automotive Parts Die Casting Market in United States

The United States dominates the North American automotive parts die-casting market, commanding approximately 82% of the regional market share in 2024. The country's market leadership is supported by its extensive automotive manufacturing base and technological expertise in die-casting processes. The implementation of Corporate Average Fuel Economy (CAFE) standards and EPA regulations continues to drive the demand for lightweight components. The country's robust electric vehicle manufacturing initiatives, coupled with significant investments in die-casting facilities by major automotive manufacturers, further solidify its market position. The presence of advanced research and development centers and continuous technological innovations in die-casting processes contribute to the market's sustained growth.

Automotive Parts Die Casting Market in Mexico

Mexico emerges as the fastest-growing market in North America, with a projected CAGR of approximately 6% during 2024-2029. The country's growth is driven by increasing foreign direct investments in automotive manufacturing facilities and expanding die-casting capabilities. Mexico's strategic geographical location, competitive labor costs, and strong trade relationships with the United States and Canada enhance its market position. The country's focus on developing its metalworking industry processes, particularly in automotive parts manufacturing, contributes to its rapid growth. The presence of tier 1, tier 2, and tier 3 suppliers, along with their increasing adoption of aluminum materials for manufacturing, supports the market's expansion.

Automotive Parts Die Casting Market in Europe

The European automotive parts die-casting market showcases significant development driven by stringent emission regulations and an increasing focus on vehicle electrification. The region encompasses key markets including Germany, the United Kingdom, France, Spain, and Italy, each contributing distinctively to the market landscape. The strong presence of luxury and premium automotive manufacturers, coupled with increasing investments in electric vehicle production, shapes the market dynamics. The region's emphasis on sustainable manufacturing practices and technological innovations in die-casting processes further strengthens its market position.

Automotive Parts Die Casting Market in Germany

Germany maintains its position as the largest market in Europe, holding approximately 21% of the regional market share in 2024. The country's leadership is underpinned by its excellence in automotive manufacturing and significant investments in die-casting technologies. Germany's automotive industry, being one of the most innovative and competitive globally, drives the demand for advanced die-casting components. The country's strong focus on electric vehicle development and production, supported by a well-established research and development infrastructure, contributes to market growth. The presence of major automotive manufacturers and their supplier networks further reinforces Germany's market dominance.

Automotive Parts Die Casting Market in Spain

Spain emerges as the fastest-growing market in Europe, with a projected CAGR of approximately 6% during 2024-2029. The country's growth is driven by increasing investments in automotive manufacturing capabilities and rising adoption of electric vehicles. Spain's strategic focus on developing advanced manufacturing facilities and implementing innovative die-casting techniques contributes to its rapid market expansion. The country's strong automotive component manufacturing base, coupled with government support for electric vehicle adoption, creates favorable conditions for market growth. The presence of established automotive manufacturers and their increasing focus on lightweight components further accelerates market development.

Automotive Parts Die Casting Market in Asia-Pacific

The Asia-Pacific region represents a dynamic market for automotive die casting, characterized by rapid industrialization and expanding automotive manufacturing capabilities. Key markets include China, Japan, India, and South Korea, each contributing significantly to regional growth. The region benefits from increasing investments in electric vehicle production, growing domestic demand for automobiles, and the presence of major automotive manufacturers. The focus on developing advanced die-casting technologies and expanding manufacturing capabilities strengthens the market position of countries within this region.

Automotive Parts Die Casting Market in China

China maintains its position as the dominant force in the Asia-Pacific region's automotive casting market. The country's leadership is supported by its extensive automotive manufacturing infrastructure and significant investments in die-casting technologies. China's position as the world's leading exporter of aluminum and aluminum products, coupled with its strong automotive components manufacturing base, reinforces its market dominance. The country's rapid advancement in electric vehicle production and continuous technological innovations in die-casting processes contribute to its market leadership.

Automotive Parts Die Casting Market in India

India emerges as the fastest-growing market in the Asia-Pacific region. The country's growth is driven by expanding automotive production capabilities, increasing domestic demand, and rising exports of automotive components. India's focus on developing its die-casting capabilities, supported by government initiatives promoting manufacturing excellence, contributes to market expansion. The country's growing electric vehicle market and increasing investments in advanced manufacturing technologies further accelerate market development.

Automotive Parts Die Casting Market in Rest of the World

The Rest of the World region, encompassing the Middle East & Africa and South America, demonstrates growing potential in the automotive metal casting market. These regions benefit from increasing investments in automotive manufacturing capabilities and rising domestic demand for vehicles. The Middle East & Africa region shows promise due to growing vehicle ownership rates and increasing adoption of electric vehicles, particularly in countries like Saudi Arabia and the United Arab Emirates. South America, led by Brazil's robust automotive industry, continues to attract investments in manufacturing facilities and die-casting capabilities. Brazil emerges as the largest market in this region, while Argentina shows the fastest growth potential due to its expanding automotive manufacturing sector.

Get Analysis on Important Geographic Markets

Download PDF

Automotive Parts Die Casting Industry Overview

Top Companies in Automotive Parts Die Casting Market

The automotive parts die-casting market features prominent players like Nemak, Rheinmetall Automotive, GF Casting Solutions, and Dynacast International leading the industry through continuous innovation and strategic expansion. Companies are increasingly focusing on developing independent technologies and breakthrough innovations in die design, casting machinery, and process control to enhance manufacturing efficiency. The industry witnesses significant investments in research and development, particularly in lightweight component solutions and electric vehicle-specific parts manufacturing. Strategic collaborations with major automakers, expansion of production facilities across key markets, and integration of smart manufacturing practices, including automation and real-time monitoring, have become crucial competitive differentiators. Market leaders are also emphasizing sustainability initiatives and environmental compliance while strengthening their global supply chain networks through strategic partnerships and localized manufacturing capabilities.

Global Leaders Amid Regional Market Dynamics

The automotive parts die-casting market exhibits a fragmented structure with a mix of global conglomerates and specialized regional players competing across different geographical markets. Major players are strengthening their market positions through vertical integration, offering comprehensive solutions from raw material processing to finished components, while regional specialists focus on serving specific market niches with customized solutions. The industry has witnessed increased consolidation through strategic acquisitions and joint ventures, particularly in emerging markets, as companies seek to expand their technological capabilities and geographic presence.

The market dynamics are characterized by strong regional manufacturing hubs, particularly in Asia-Pacific, Europe, and North America, where local players maintain significant market share through deep customer relationships and understanding of regional requirements. Companies are increasingly pursuing strategic alliances and technology partnerships to enhance their competitive position, with a notable trend towards cross-border collaborations to leverage complementary strengths. The industry also sees the emergence of new players, particularly in developing economies, who are investing in advanced manufacturing capabilities to capture growing market opportunities.

Innovation and Adaptability Drive Future Success

Success in the automotive casting market increasingly depends on companies' ability to adapt to evolving industry requirements, particularly in electric vehicle components and lightweight solutions. Market leaders are investing in advanced manufacturing technologies, including automation and digitalization, while developing specialized expertise in high-performance materials and complex component designs. Companies are also focusing on building strong relationships with automotive OEMs through early involvement in product development and design processes, while maintaining flexibility to address changing market demands.

For emerging players and market contenders, differentiation through specialized capabilities and niche market focus presents opportunities for growth. The industry's future success factors include developing sustainable manufacturing practices, maintaining cost competitiveness through operational efficiency, and building robust quality management systems. Companies must also navigate increasing regulatory pressures regarding environmental compliance and safety standards, while managing the risk of substitution from alternative manufacturing technologies. Building strong technical expertise, maintaining financial stability for continuous investment in technology upgrades, and developing agile supply chain networks are becoming critical for long-term success in the automotive metal casting industry.

Automotive Parts Die Casting Market Leaders

-

Castwel Auto parts Pvt. Ltd

-

Dynacast

-

Endurance Group

-

Gibbs Die-casting Group

-

Sandhar Technologies Limited

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Automotive Parts Die Casting Market News

- November 2023: General Motors Corp. acquired Tooling & Equipment International, a Livonia, MI, developer and manufacturer of casting molds and tooling, as well as prototypes and low-volume production castings. GM will use Tooling & Equipment International's experience in designing molds and core boxes for high-volume manufacturing of automotive castings, including tooling for cylinder heads, cylinder blocks, drivelines, chassis, and suspension castings.

- November 2023: Linamar revealed that it will supply its products to the EV industry from its new Ontario-based gigacasting plant. Linamar’s facility will be the first gigacasting plant owned and operated by a North American parts maker.

- November 2023: IDRA Group was awarded a contract by Volvo Cars for two 9,000-ton giga press machines installed at the automaker's future electric vehicle factory in Košice, Slovakia. According to the company, the 9,000-ton aluminum casting machines, among Europe's largest die casting machines, represent a remarkable leap forward in automotive manufacturing technology.

Automotive Parts Die Casting Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

-

4.1 Market Drivers

- 4.1.1 Increasing Demand for High-Performance Vehicles Will Drive the Market

-

4.2 Market Restraints

- 4.2.1 Supply Chain Disruption of Raw Materials Could be a Challenge

- 4.2.2 High Initial Cost Related to the Purchase of Raw Materials is a Challenge

-

4.3 Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION (Market Size in Value - USD Billion)

-

5.1 Production Process Type

- 5.1.1 Pressure Die Casting

- 5.1.2 Vacuum Die Casting

- 5.1.3 Squeeze Die Casting

- 5.1.4 Semi-solid Die Casting

-

5.2 Raw Material

- 5.2.1 Aluminum

- 5.2.2 Zinc

- 5.2.3 Magnesium

- 5.2.4 Other Raw Material Types

-

5.3 Application Type

- 5.3.1 Body Assemblies

- 5.3.2 Engine Parts

- 5.3.3 Transmission Parts

- 5.3.4 Other Application Types

-

5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Spain

- 5.4.2.5 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 India

- 5.4.3.2 China

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 Latin America

- 5.4.4.1 Mexico

- 5.4.4.2 Brazil

- 5.4.4.3 Argentina

- 5.4.5 Middle East and Africa

- 5.4.5.1 United Arab Emirates

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 Rest of Middle East and Africa

6. COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

-

6.2 Company Profiles

- 6.2.1 Castwel Auto Parts Pvt Ltd

- 6.2.2 Die-casting Solutions GmbH

- 6.2.3 Dynacast International Inc.

- 6.2.4 Endurance Group

- 6.2.5 Gibbs Die-casting Group

- 6.2.6 Kinetic Die-casting Company

- 6.2.7 Mino Industry USA Inc.

- 6.2.8 Ningbo Parison Die-casting Co. Ltd

- 6.2.9 Raltor Metal Technik India Pvt. Ltd

- 6.2.10 Rockman Industries Ltd

- 6.2.11 Ryobi Die-casting Inc.

- 6.2.12 Sandhar Technologies Limited

- 6.2.13 Sipra Engineers Pvt. Ltd

- 6.2.14 Spark Minda, Ashok Minda Group

- 6.2.15 Sunbeam Auto Pvt Ltd

- 6.2.16 Texas Die-casting

- 6.2.17 Tyche Diecast Private Limited

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Inclination Towards the Use of Lightweight and Sustainable Materials Will be Key Trend

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Automotive Parts Die Casting Industry Segmentation

Die casting is a metal casting process in which molten metal is forced into a mold cavity under high pressure. The machine used for that purpose is known as die casting.

The automotive die casting market is segmented by production, raw material, application, and geography. The market is segmented by production types, such as pressure die-casting, vacuum die-casting, squeeze die-casting, and semi-solid die-casting. By raw material type, the market is segmented as aluminum, zinc, magnesium, and other raw material types. The market is segmented by application type into body assemblies, engine parts, transmission parts, and other applications. The market is segmented by geography, such as North America, Europe, Asia-Pacific, Latin America, the Middle East, and Africa.

The report covers the market size and forecasts for the die-casting market for each segment in terms of value (USD).

| Production Process Type | Pressure Die Casting | ||

| Vacuum Die Casting | |||

| Squeeze Die Casting | |||

| Semi-solid Die Casting | |||

| Raw Material | Aluminum | ||

| Zinc | |||

| Magnesium | |||

| Other Raw Material Types | |||

| Application Type | Body Assemblies | ||

| Engine Parts | |||

| Transmission Parts | |||

| Other Application Types | |||

| Geography | North America | United States | |

| Canada | |||

| Rest of North America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | India | ||

| China | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Latin America | Mexico | ||

| Brazil | |||

| Argentina | |||

| Middle East and Africa | United Arab Emirates | ||

| Saudi Arabia | |||

| Rest of Middle East and Africa | |||

Need A Different Region or Segment?

Customize Now

Automotive Parts Die Casting Market Research FAQs

How big is the Automotive Parts Die Casting Market?

The Automotive Parts Die Casting Market size is expected to reach USD 48.99 billion in 2025 and grow at a CAGR of greater than 6.19% to reach USD 66.14 billion by 2030.

What is the current Automotive Parts Die Casting Market size?

In 2025, the Automotive Parts Die Casting Market size is expected to reach USD 48.99 billion.

Who are the key players in Automotive Parts Die Casting Market?

Castwel Auto parts Pvt. Ltd, Dynacast, Endurance Group, Gibbs Die-casting Group and Sandhar Technologies Limited are the major companies operating in the Automotive Parts Die Casting Market.

Which is the fastest growing region in Automotive Parts Die Casting Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Automotive Parts Die Casting Market?

In 2025, the North America accounts for the largest market share in Automotive Parts Die Casting Market.

What years does this Automotive Parts Die Casting Market cover, and what was the market size in 2024?

In 2024, the Automotive Parts Die Casting Market size was estimated at USD 45.96 billion. The report covers the Automotive Parts Die Casting Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Automotive Parts Die Casting Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Automotive Parts Die Casting Market Research

Mordor Intelligence provides a comprehensive analysis of the automotive parts die casting industry. We leverage our extensive expertise in automotive metal casting research to deliver detailed insights. Our study covers the complete spectrum of die casting processes, including aluminum die casting, zinc die casting, and magnesium die casting technologies. The report offers in-depth coverage of automotive foundry operations and automotive metal components manufacturing. It provides stakeholders with crucial insights into market dynamics and technological advancements in the automotive casting sector.

Our extensively researched report, available as an easy-to-download PDF, presents valuable insights into the evolution and future trajectory of the automotive die casting industry. The analysis addresses critical aspects of the aluminum die casting industry and broader automotive metal casting market size trends. Stakeholders gain access to detailed evaluations of metal casting for automotive applications, including production technologies, material innovations, and regional market dynamics. The report's comprehensive coverage of the automotive metal casting industry enables businesses to make informed decisions while navigating the complex landscape of automotive metal components manufacturing.