Automotive Optoelectronics Market Size

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

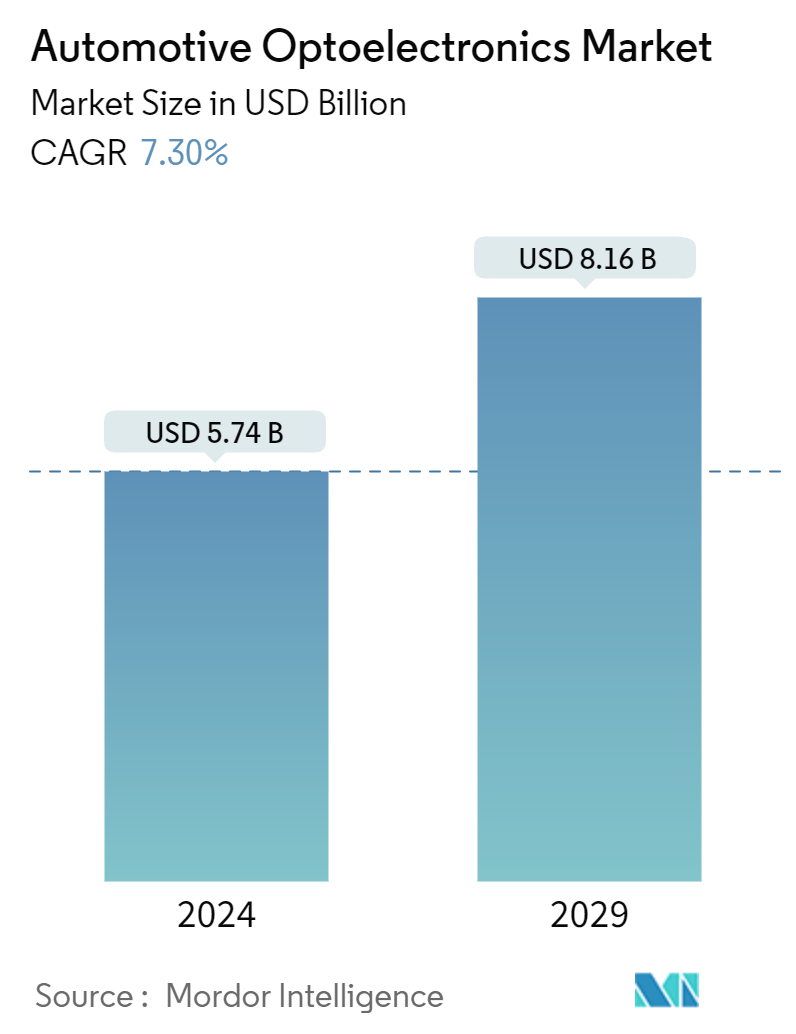

| Market Size (2024) | USD 5.74 Billion |

| Market Size (2029) | USD 8.16 Billion |

| CAGR (2024 - 2029) | 7.30 % |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Automotive Optoelectronics Market Analysis

The Automotive Optoelectronics Market size is estimated at USD 5.74 billion in 2024, and is expected to reach USD 8.16 billion by 2029, growing at a CAGR of 7.30% during the forecast period (2024-2029).

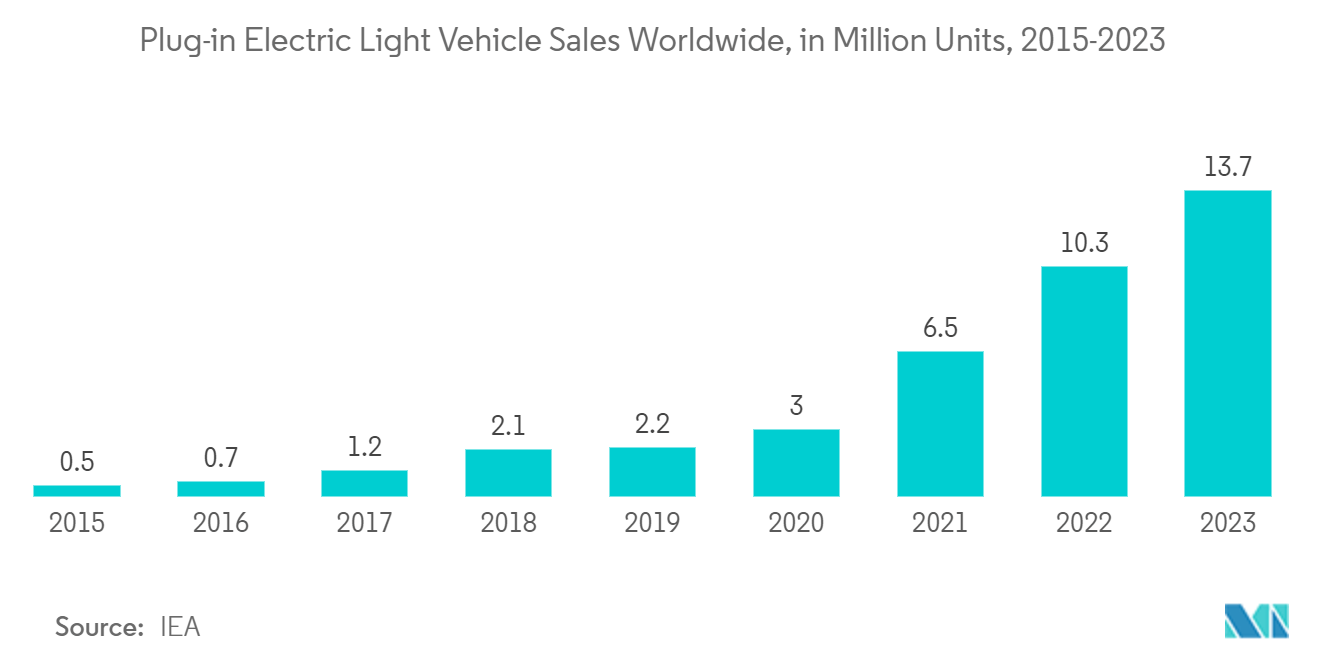

- The optoelectronics market is witnessing significant progress, propelled by the convergence of optical communication, optical storage, and optical imaging sectors. Additionally, the rising demand for electric vehicles further drives the optoelectronics market. For instance, the International Energy Agency (IEA) projected that electric vehicle (EV) sales will make up approximately 65% of total car sales by 2030 in the Net Zero Scenario. To achieve this, there should be an annual growth rate of around 25% in EV sales from 2023 to 2030.

- LEDs have emerged as the de facto standard in display technology for electronic devices. This shift is primarily due to heightened consumer expectations for improved performance and resolution. LED lighting finds diverse applications in automotive settings, from headlights to taillights and interior illumination. With the ongoing electrification of vehicles, managing power consumption has emerged as a pivotal concern. LED technology not only curtails power usage but also extends product lifecycles, provides design flexibility, and enhances control.

- Optoelectronics find numerous applications in various aspects of automotive technology, driving innovation and enhancing safety, efficiency, and connectivity. They are employed in advanced driver-assistance systems (ADAS). These systems rely on sensors, processors, and communication modules to enable features such as adaptive cruise control, lane departure warning, and collision avoidance.

- According to the National Safety Council, by 2026, approximately 71% of registered vehicles will be equipped with rear cameras, while 60% will have rear parking sensors. Such increasing adoption of ADAS (Advanced driver assistance systems) is expected to aid the growth of the market studied.

- Technological advancements in communication, controls, and embedded systems are shaping the emergence of an intelligent vehicle grid. Today's cars function as sophisticated sensor platforms, gathering data from their surroundings and other vehicles. This data is then relayed to drivers and infrastructure, aiding in tasks such as safe navigation, pollution control, and traffic management. Further, according to the World Economic Forum, over 12 million fully autonomous cars are anticipated to be sold annually by 2035, covering 25% of the global automotive market, further uplifting the scope of cameras and devices per vehicle.

- The increasing inflation and interest rates have reduced consumer purchasing power, which is expected to reduce the demand for vehicles and hamper market growth. Further, the Russia-Ukraine War increased the strain on the global supply chain, as Russia and Ukraine were the major exporters of metals and minerals, as well as oil and gas. Ukraine possessed significant deposits of natural resources, including coal, natural gas, iron ore, titanium, lithium, and rare Earth minerals, enabling a shift away from relying on China and Russia for energy resources.

- Geopolitical conflicts, such as the invasion of Ukraine by Russia, have further disrupted the semiconductor supply chain. For example, the production of neon, a critical component for chip manufacturing, was affected when Ukraine’s leading neon suppliers halted operations. Trade disputes, export controls, and regulatory changes have disrupted the flow of raw materials and components, further exacerbating the optoelectronics shortage.

Automotive Optoelectronics Market Trends

Image Sensors are Expected to Hold Major Market Share

- Image Sensors are expected to hold a significant market share. The growth of the segment is driven by the rising adoption of image sensors for automatic optical inspection (AOI) and the rising focus on camera quality in automobiles. Automotive image sensors are sophisticated electronic devices that capture visual data from a vehicle's surroundings. They are crucial for enhancing safety, enabling advanced driver assistance systems (ADAS), and supporting the development of autonomous vehicles. These sensors enable a broad range of functionalities, from basic safety features to the complex requirements of autonomous driving.

- The automobile industry is focusing on enabling safer driving experiences. This, in turn, has increased the use of frame-transfer CCD sensors and interline-transfer CCD sensors. CCD sensors, like all technologies, come with their set of pros and cons. However, the drawbacks associated with CCD sensors have led to a notable trend: CMOS sensors are progressively supplanting CCD sensors in specific applications. For instance, the advantages of CCD sensors include lower noise and higher sensitivity owing to their higher fill factor, fewer defective pixels owing to their simple structure, and better image homogeneity.

- The capacity of CMOS image sensors to work efficiently in various lighting conditions, such as dim light, darkness, and low light, has increased the use of CMOS image sensors, especially in security applications, bolstering the CMOS image sensors market in the automotive industry.

- For instance, in May 2024, Omnivision announced a new automotive image sensor lineup by introducing the OX05D10, a 5-MP CMOS sensor. This addition comes on the heels of the OX08D10, an 8-MP sensor unveiled in September at AutoSens Brussels. The OX05D10 is designed to excel in low-light conditions, specifically countering image flicker caused by LED traffic lights and signals in automotive exterior cameras. Targeted at advanced driver assistance systems (ADAS) and autonomous driving applications, the OX05D10 is equipped with Omnivision's cutting-edge 2.1 µm single-pixel TheiaCel technology.

- The rising demand for autonomous vehicles will likely foster market growth. For instance, according to Intel, worldwide car sales are projected to reach more than 101.4 million units in 2030, and autonomous vehicles are likely to account for around 12% of car registrations by 2030. These factors are projected to create new growth opportunities for image sensors.

China is Expected to Witness a High Market Growth Rate

- China is home to manufacturers of consumer electronics and automotive parts. Furthermore, increasing automotive light vehicle production drives market growth in China. The demand for passenger car sensors in this area has also been boosted by the growth of the economy and progress within the regulatory framework.

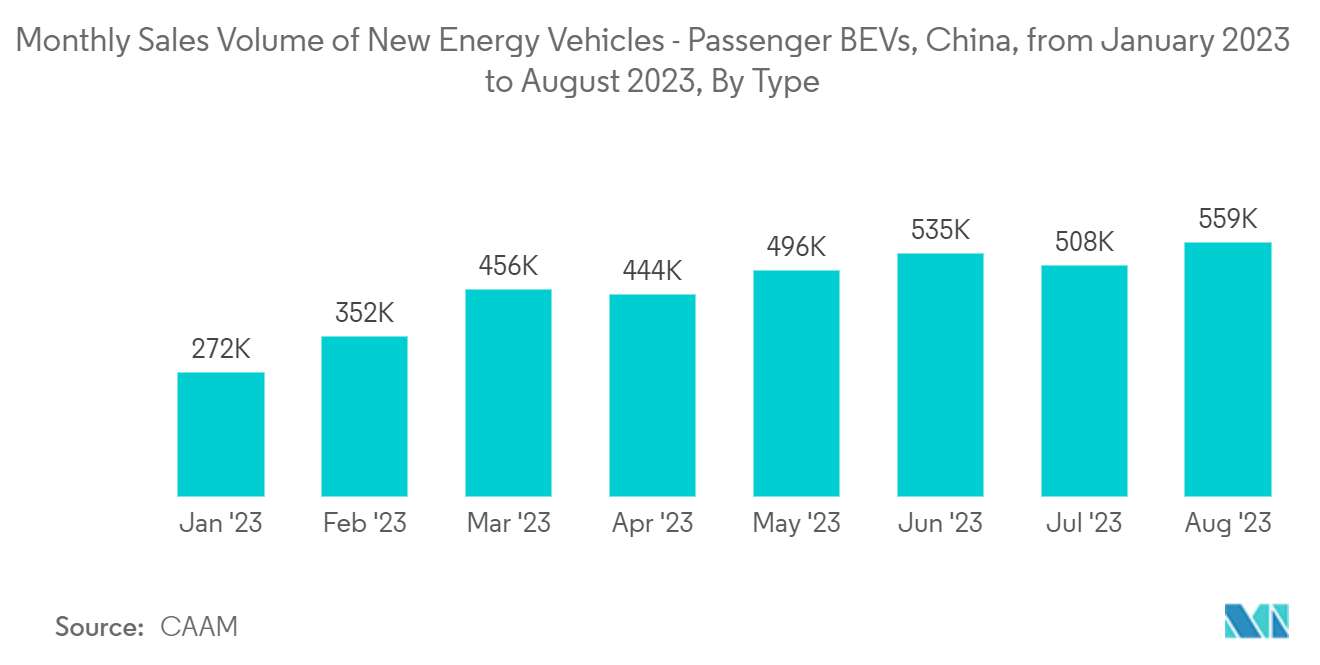

- The Chinese automotive sector is proliferating, and the region plays a more significant role in the global auto industry. China is one of the top countries that have adopted electric vehicles, which are becoming increasingly popular. In August 2023, China's new energy vehicle sales reached 846,000 units, with passenger electric vehicles accounting for 808,000 units and commercial electric vehicles for 39,000 units.

- Warehouses utilize optoelectronics for various applications, including automatic access control, remote sensing for inventory and environmental monitoring, high-bandwidth optical communications, lighting, and security systems. As pivotal hubs in the e-commerce revolution, retailers are continually innovating their warehouses to maintain a competitive edge.

- The region's manufacturing industry is on a rapid growth trajectory, increasingly adopting diverse manufacturing and telecommunications technologies, a trend poised to bolster the market's expansion. Moreover, initiatives like the 'Made in China 2025' plan underscore the Chinese government's commitment to advancing R&D in factory automation. While China currently imports a significant portion of its automation equipment, the 'Made in China' initiative seeks to boost domestic production of these essential tools.

Automotive Optoelectronics Industry Overview

The automotive optoelectronics market is consolidated and features key players like Vishay Intertechnology Inc., Omnivision Technologies Inc., Samsung Electronics, SK Hynix Inc., and Sony Corporation. Market participants strategically leverage partnerships and acquisitions to bolster their product portfolios and establish a sustainable competitive edge.

- In November 2023, ams OSRAM, a prominent player in intelligent sensors and emitters, unveiled the latest iteration of its well-received OSLON Submount PL LED family. This upgraded line promises enhanced brightness and increased design adaptability, specifically catering to manufacturers in the automotive forward lighting segment. According to internal metrics, the third-generation OSLON Submount PL LEDs boast a 9% brightness boost over their predecessors. This advancement not only elevates the lighting capabilities but also presents an opportunity for automotive manufacturers to potentially lower the overall system costs in their headlamp designs.

- In September 2023, Sony Semiconductor Solutions Corporation (SSS) unveiled its latest innovation, the IMX735. This CMOS image sensor, boasting an industry-leading pixel count of 17.42 effective megapixels, is tailored specifically for automotive cameras. The IMX735 is designed to empower automotive camera systems, enabling advanced sensing and recognition capabilities and ultimately enhancing the safety and reliability of automated driving.

Automotive Optoelectronics Market Leaders

-

Sony Corporation

-

Vishay Intertechnology Inc.

-

Omnivision Technologies Inc.

-

Samsung Electronics

-

SK Hynix Inc.

*Disclaimer: Major Players sorted in no particular order

Automotive Optoelectronics Market News

- February 2024: TSMC, Sony Semiconductor Solutions Corporation, DENSO Corporation, and Toyota Motor Corporation bolstered their investment in Japan Advanced Semiconductor Manufacturing Inc. ("JASM"), a subsidiary primarily owned by TSMC in Kumamoto Prefecture, Japan. This investment aims to establish a second fab, slated to commence operations by the end of 2027. Coupled with JASM's first fab, set to launch in 2024, the collective investment in JASM will surpass USD 20 billion, backed by substantial support from the Japanese government.

- January 2024: Osram Licht AG unveiled a new line of side-looker, low-power LEDs. These LEDs, known as SYNIOS P1515 sidelookers, offer a simplified design, are easier to integrate, and facilitate a uniform appearance in applications like extended light bars and other automotive rear lighting. By opting for these side-looker LEDs over traditional top-looker ones, automotive manufacturers can achieve a seamless, uniform look across the vehicle's width. Notably, even with the same number of LEDs, the RCL or turn indicator can be made with a significantly slimmer and more straightforward optical setup.

Automotive Optoelectronics Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumption and Market Definition

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

4.1 Market Overview

4.2 Industry Value Chain Analysis

4.3 Industry Attractiveness - Porter's Five Forces Analysis

4.3.1 Threat of New Entrants

4.3.2 Bargaining Power of Buyers/Consumers

4.3.3 Bargaining Power of Suppliers

4.3.4 Threat of Substitute Products

4.3.5 Intensity of Competitive Rivalry

4.4 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

5. MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Technology Advancements, and AI Developments will Drive the Growth

5.1.2 Growing Demand for Electric Vehicles

5.2 Market Restraints

5.2.1 High Manufacturing and Fabricating Costs

5.2.2 Challenges With Energy Loss and Heating of Optoelectronic Devices

6. MARKET SEGMENTATION

6.1 By Device Type

6.1.1 LED

6.1.2 Laser Diode

6.1.3 Image Sensors

6.1.4 Optocouplers

6.1.5 Photovoltaic cells

6.1.6 Other Device Types

6.2 By Geography***

6.2.1 United States

6.2.2 Europe

6.2.3 Japan

6.2.4 China

6.2.5 South Korea

6.2.6 Taiwan

7. COMPETITIVE LANDSCAPE

7.1 Company Profiles*

7.1.1 SK Hynix Inc.

7.1.2 Panasonic Corporation

7.1.3 Samsung Electronics

7.1.4 Omnivision Technologies Inc.

7.1.5 Sony Corporation

7.1.6 Ams Osram AG

7.1.7 Signify Holding

7.1.8 Vishay Intertechnology Inc.

7.1.9 Texas Instruments Inc.

7.1.10 LITE-ON Technology Corporation

7.1.11 Rohm Company Limited

7.1.12 Mitsubishi Electric Corporation

7.1.13 Broadcom Inc.

7.1.14 Sharp Corporation

8. MARKET OPPORTUNITIES AND FUTURE TRENDS

Automotive Optoelectronics Industry Segmentation

Optoelectronic devices are electronic devices and systems that involve the study, detection, and control of light. They are considered a sub-field of photonics and are used to convert electrical energy into light or vice versa. The study tracks the revenue accrued through the sale of automotive optoelectronics by various players worldwide. The study also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period. The study further analyses the overall impact of COVID-19 aftereffects and other macroeconomic factors on the market.

The automotive optoelectronics market is segmented by device type (LED, laser diode, image sensors, optocouplers, photovoltaic cells, and other device types) and geography (United States, Europe, China, Japan, Korea, Taiwan, and the Rest of the World). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| By Device Type | |

| LED | |

| Laser Diode | |

| Image Sensors | |

| Optocouplers | |

| Photovoltaic cells | |

| Other Device Types |

| By Geography*** | |

| United States | |

| Europe | |

| Japan | |

| China | |

| South Korea | |

| Taiwan |

Automotive Optoelectronics Market Research FAQs

How big is the Automotive Optoelectronics Market?

The Automotive Optoelectronics Market size is expected to reach USD 5.74 billion in 2024 and grow at a CAGR of 7.30% to reach USD 8.16 billion by 2029.

What is the current Automotive Optoelectronics Market size?

In 2024, the Automotive Optoelectronics Market size is expected to reach USD 5.74 billion.

Who are the key players in Automotive Optoelectronics Market?

Sony Corporation, Vishay Intertechnology Inc., Omnivision Technologies Inc., Samsung Electronics and SK Hynix Inc. are the major companies operating in the Automotive Optoelectronics Market.

What years does this Automotive Optoelectronics Market cover, and what was the market size in 2023?

In 2023, the Automotive Optoelectronics Market size was estimated at USD 5.32 billion. The report covers the Automotive Optoelectronics Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the Automotive Optoelectronics Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

Automotive Optoelectronics Industry Report

Statistics for the 2024 Automotive Optoelectronics market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. Automotive Optoelectronics analysis includes a market forecast outlook for 2024 to 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.

Automotive Optoelectronics Market Report Snapshots