| Study Period | 2017 - 2029 |

| Base Year For Estimation | 2023 |

| Forecast Data Period | 2024 - 2029 |

| Market Size (2024) | USD 2.94 Billion |

| Market Size (2029) | USD 15.36 Billion |

| CAGR (2024 - 2029) | 39.23 % |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order |

Automotive MLCC Market Analysis

The Automotive MLCC Market size is estimated at 2.94 billion USD in 2024, and is expected to reach 15.36 billion USD by 2029, growing at a CAGR of 39.23% during the forecast period (2024-2029).

The automotive MLCC industry is experiencing a transformative shift driven by the increasing sophistication of vehicle electronics and automation technologies. Modern vehicles require an unprecedented number of electronic components, with typical engine-driven vehicles utilizing approximately 3,000 MLCCs, while advanced vehicles with automated features require between 8,000 to 10,000 MLCCs per vehicle. This surge in electronic content per vehicle reflects the industry's evolution toward more complex and sophisticated automotive systems, particularly in areas such as advanced driver assistance systems (ADAS), infotainment, and power management systems. The integration of these technologies has fundamentally altered the automotive supply chain, compelling MLCC manufacturers to enhance their production capabilities and technological innovations.

The industry is witnessing substantial investments in research and development, particularly in the context of electric vehicle infrastructure and autonomous driving capabilities. A notable example is Volkswagen's commitment to invest USD 193 billion in electric vehicle development and software, highlighting the industry's trajectory toward electrification and digital transformation. This investment trend is reshaping the MLCC market, as manufacturers focus on developing components that can withstand higher voltages, temperatures, and reliability requirements. The collaboration between automotive manufacturers and MLCC suppliers has become increasingly strategic, as evidenced by recent partnerships such as Tesla's MLCC supply agreements for drive inverters.

Infrastructure development is playing a crucial role in shaping the MLCC market landscape, particularly in the context of charging networks for electric vehicles. Japan's ambitious plan to establish 150,000 charging stations by 2030, including 30,000 fast-charging stations, exemplifies the scale of infrastructure development underway globally. This expansion of charging infrastructure is driving demand for high-performance MLCCs capable of handling the specific requirements of charging systems, including high-voltage operations and thermal management. The trend is particularly significant in the development of DC fast-charging stations, which require sophisticated power management components.

The industry is experiencing a significant shift in manufacturing and quality standards, with a particular focus on automotive-grade MLCCs. The United Kingdom's robust automotive manufacturing sector, producing over 775,014 cars and 101,600 commercial vehicles in 2022, demonstrates the scale of potential demand for high-quality MLCCs. Manufacturers are increasingly adopting advanced production techniques and quality control measures to meet the stringent requirements of automotive applications. This includes compliance with automotive standards such as AEC-Q200, implementation of sophisticated testing procedures, and development of MLCCs with enhanced reliability features such as soft termination technology and improved thermal stability characteristics.

Global Automotive MLCC Market Trends

Infrastructure improvement for hydrogen stations continues to increase sales

- Fuel cell electric vehicles (FCEVs) use hydrogen energy stored as fuel, which is then converted into electricity by the fuel cell and has a propulsion mechanism similar to that of an electric vehicle. Compared to vehicles powered by conventional internal combustion engines, FCEVs do not emit any harmful exhaust emissions.

- Fuel cell electric vehicle shipments accounted for 0.043 million units in 2022, and these are expected to reach 0.071 million units in 2029. As renewable energies like wind and solar contribute increasingly to the hydrogen manufacturing process, there will be a huge increase in the demand for energy-efficient FCEVs.

- As the demand for low-emission vehicles rises, stricter carbon emission standards are being implemented, and more emphasis is being placed on the adoption of FCEVs due to benefits like quick refueling. To encourage the development of FCEVs, several government and commercial organizations are collaborating and investing in advancing fuel cell technology and the development of hydrogen refueling infrastructure. According to the IEA, at the end of 2021, there were about 730 hydrogen refueling stations (HRSs) globally providing fuel for about 51,600 FCEVs. This represents an increase of almost 50% in the global stock of FCEVs and a 35% increase in the number of HRSs from 2020. These factors contribute to the high growth of FCEVs in the future.

_Production__Thousand__Global__2017_-_2029.svg)

Understand The Key Trends Shaping This Market

Download PDF

Stringent government regulations are increasing the penetration of electric vehicles

- MLCCs have emerged as a perfect component for EV electronics and subsystems, offering high-temperature resistance and an easy surface-mount form factor. Approximately 8,000-10,000 MLCCs are used in an electric vehicle. MLCCs in electric vehicles are commonly used in battery management systems (BMS), onboard chargers (OBC), and DC/DC converters. In addition to meeting the general specifications required for these EV subsystems and having the ability to function reliably in harsh environments inside an EV, component manufacturers should also be IATF 16949-certified and compliant with AEC-Q200.

- Electric vehicle shipments accounted for 16.4 million units in 2022, and it is expected to rise to 25.52 million units in 2029. Several countries have implemented strict environmental regulations to reduce greenhouse gas emissions and combat climate change. As a result, automakers are under increasing pressure to produce more electric vehicles and reduce their reliance on fossil fuels. Consumers are becoming more environmentally conscious and are looking for more sustainable alternatives to traditional gasoline-powered vehicles.

- The COVID-19 pandemic and Russia’s war in Ukraine disrupted global supply chains, and the automotive industry has been heavily impacted. However, in the longer term, the EV market is witnessing sales growth in some regions of the world as government and corporate efforts to support the deployment of publicly available charging infrastructure are providing a solid basis for further increase in EV sales. Publicly accessible chargers worldwide approached 1.8 million, with nearly 500,000 chargers installed in 2021, of which a third were fast chargers, which accounted for more than the total number of public chargers installed in 2017.

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT

- Supportive government policies for the deployment of public charging infrastructure are expected to promote battery electric vehicle sales

- Hybrid and electric heavy-duty trucks are expected to have positive impact on the market

- Development of the e-commerce industry is expected to propel the sales of light commercial vehicles

- The advancements in battery technology are driving the demand for PHEV sales

- Increasing awareness of electric bikes is expected to surge the demand

- Increasing emission norms are expected to surge the demand for HEVs

- Technological developments, efficiency, and performance boost the demand for ICEVs

- The emergence of the global middle-class consumers propels the market

- The rise in technological advancements in vehicles is expected to boost passenger vehicles

Segment Analysis: Vehicle Type

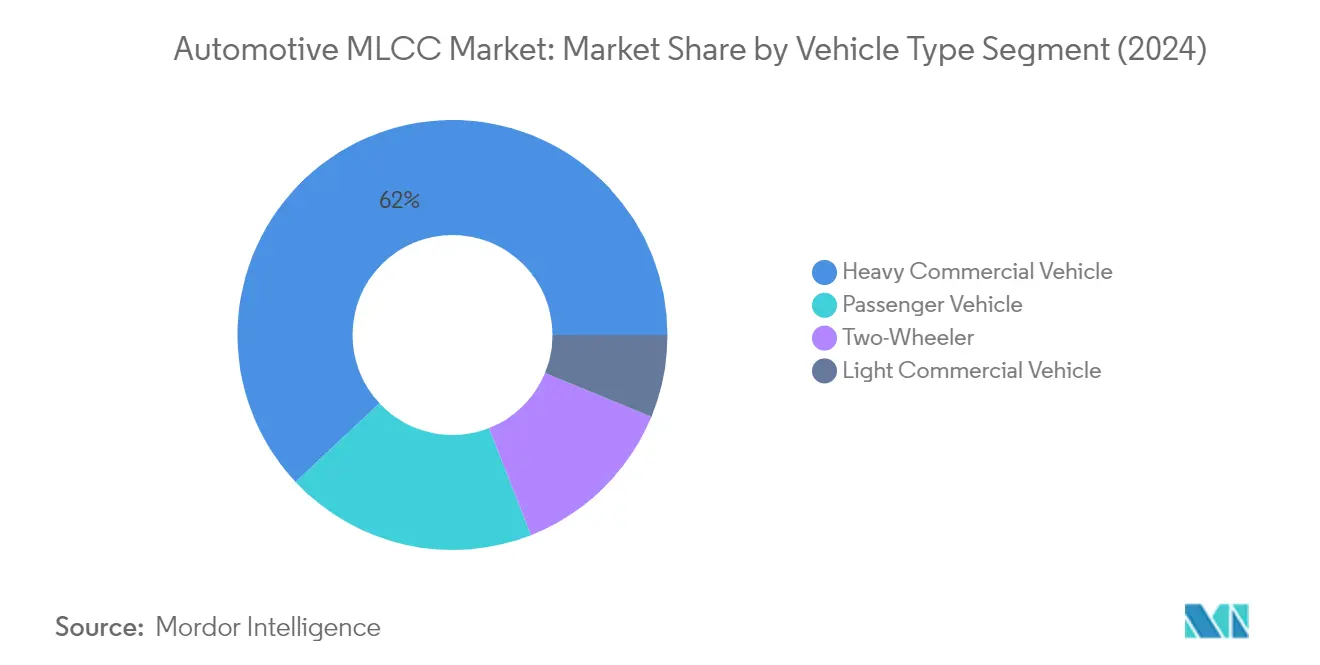

Heavy Commercial Vehicle Segment in Automotive MLCC Market

The Heavy Commercial Vehicle (HCV) segment dominates the automotive MLCC market, commanding approximately 62% market share in 2024. This significant market position is driven by the increasing integration of electronic systems in modern HCVs, particularly in areas such as powertrain control, safety systems, and advanced driver assistance features. The segment's prominence is further reinforced by stringent vehicle emission regulations and the booming logistics, retail, and e-commerce industries that fuel demand for new and advanced heavy commercial vehicles worldwide. The integration of sophisticated electronic components, including automotive capacitors like MLCCs, in HCV applications spans from engine management and exhaust emission control to braking systems and communication networks, making them indispensable for ensuring optimal vehicle performance and reliability.

HCV Segment Growth in Automotive MLCC Market

The Heavy Commercial Vehicle segment is projected to maintain its market leadership while also emerging as the fastest-growing segment, with an expected CAGR of approximately 45% during 2024-2029. This remarkable growth trajectory is attributed to several factors, including the rapid electrification of commercial fleets, increasing adoption of autonomous driving technologies, and the rising demand for advanced safety features in HCVs. The segment's growth is further propelled by the global push toward sustainable transportation solutions and the integration of connected vehicle technologies. As HCV manufacturers continue to innovate and incorporate more electronic systems for improved efficiency, safety, and connectivity, the demand for MLCCs in this segment is expected to surge significantly over the forecast period.

Remaining Segments in Vehicle Type

The passenger vehicle, light commercial vehicle, and two-wheeler segments collectively represent significant opportunities in the automotive MLCC market. The passenger vehicle segment maintains its position as the second-largest segment, driven by increasing consumer demand for advanced infotainment systems and safety features. Light commercial vehicles are experiencing steady growth due to the expansion of last-mile delivery services and urban logistics operations. The two-wheeler segment, while smaller in market share, is witnessing transformation through electrification and the integration of smart features, particularly in emerging markets where two-wheelers serve as primary modes of transportation.

Segment Analysis: Fuel Type

Non-Electric Vehicle Segment in Automotive MLCC Market

The non-electric vehicle segment maintains its dominance in the global automotive MLCC market, commanding approximately 65% market share in 2024. This substantial market position is attributed to the segment's extensive application base across traditional internal combustion engine vehicles, which continue to represent a significant portion of global vehicle production. The segment's strength is particularly evident in emerging markets where infrastructure for electric vehicles is still developing. Non-electric vehicles require sophisticated electronic systems for engine management, safety features, and infotainment systems, driving the demand for automotive capacitors like MLCCs. The integration of advanced driver assistance systems (ADAS) and enhanced connectivity features in conventional vehicles has further amplified the need for high-quality MLCCs, reinforcing the segment's market leadership.

Electric Vehicle Segment in Automotive MLCC Market

The electric vehicle segment is experiencing remarkable growth in the automotive MLCC market, with a projected CAGR of approximately 49% from 2024 to 2029. This exceptional growth trajectory is driven by increasing global initiatives toward vehicle electrification and stringent emission regulations. The segment's expansion is further supported by technological advancements in battery management systems, power electronics, and charging infrastructure, all of which require sophisticated MLCC applications. The rising consumer acceptance of electric vehicles, coupled with government incentives and subsidies worldwide, is accelerating the adoption of EVs. This transition necessitates advanced electronic components, particularly MLCCs, which play crucial roles in power distribution, voltage regulation, and noise suppression within electric vehicles.

Segment Analysis: Propulsion Type

ICEV Segment in Automotive MLCC Market

The Internal Combustion Engine Vehicle (ICEV) segment maintains its dominant position in the automotive MLCC market, commanding approximately 85% market share in 2024. This substantial market presence is attributed to the segment's established manufacturing infrastructure and ongoing technological advancements in engine efficiency and performance. ICE vehicles continue to integrate sophisticated electronic systems, including advanced engine management, emissions control, and various safety features, driving the demand for MLCCs. The segment's strength is further reinforced by the continuous development of hybrid technologies and the integration of start-stop systems, which require reliable and high-performance MLCCs for efficient power management and control applications. Additionally, stringent emission regulations have spurred innovations in ICE technology, leading to increased electronic content per vehicle and consequently higher MLCC usage.

BEV Segment in Automotive MLCC Market

The Battery Electric Vehicle (BEV) segment is experiencing remarkable growth, projected to expand at approximately 40% CAGR from 2024 to 2029. This exceptional growth trajectory is driven by increasing global emphasis on sustainable transportation solutions and supportive government policies promoting electric vehicle adoption. The segment's growth is further accelerated by continuous advancements in battery technology, expanding charging infrastructure, and decreasing battery costs. BEVs require significantly more MLCCs compared to traditional vehicles, particularly in critical applications such as battery management systems, power distribution units, and charging systems. The segment's expansion is also supported by major automotive manufacturers' commitments to electrification strategies and increasing consumer acceptance of electric vehicles as a viable alternative to conventional transportation.

Remaining Segments in Propulsion Type

The automotive MLCC market encompasses several other significant propulsion segments, including Hybrid Electric Vehicles (HEV), Plug-in Hybrid Electric Vehicles (PHEV), and Fuel Cell Electric Vehicles (FCEV). These segments represent varying approaches to vehicle electrification and alternative power sources, each with unique MLCC requirements. HEVs and PHEVs serve as transitional technologies, combining conventional internal combustion engines with electric powertrains, while FCEVs represent an emerging technology utilizing hydrogen fuel cells. Each of these segments contributes to the market's diversity and drives innovation in MLCC technology, particularly in areas such as power management, energy efficiency, and electronic control systems. The continued development of these alternative propulsion technologies ensures a dynamic and evolving market landscape for automotive MLCCs.

Segment Analysis: Component Type

Infotainment Segment in Automotive MLCC Market

The infotainment segment has emerged as the dominant force in the automotive MLCC market, commanding approximately 30% market share in 2024. This significant market position is driven by the increasing integration of sophisticated software and advanced infotainment features in modern vehicles. As car manufacturers strive to enhance user experiences through touchscreens, audio systems, GPS navigation, and connectivity features, the demand for high-quality MLCCs continues to surge. The segment's growth is further propelled by collaborations with tech giants like Google and Apple, who are introducing advanced in-vehicle software systems such as Android Automotive and CarPlay. These partnerships necessitate robust electronic components like MLCCs to ensure seamless integration of smartphone functionalities into vehicles. The push for standardization and integration in the infotainment space, exemplified by the widespread adoption of Android Automotive across various car models, has created opportunities for MLCC manufacturers to optimize their product offerings and streamline production processes.

ADAS Segment in Automotive MLCC Market

The Advanced Driver Assistance Systems (ADAS) segment is experiencing remarkable growth in the automotive MLCC market, with projections indicating an impressive growth rate of approximately 42% during the forecast period 2024-2029. This exceptional growth trajectory is driven by the increasing adoption of safety-critical features and autonomous driving capabilities in modern vehicles. MLCCs play a crucial role in ADAS module power management, signal processing, and sensor synchronization, making them indispensable components in various applications ranging from collision avoidance systems to adaptive cruise control. The fusion of multiple sensor technologies, including cameras, lidar, radar, and ultrasonic sensors, requires sophisticated and compact MLCCs to enable seamless integration. As automotive manufacturers continue to enhance their ADAS offerings and progress toward higher levels of autonomous driving, the demand for MLCCs in this segment is expected to accelerate significantly, supported by ongoing technological advancements and evolving safety regulations.

Remaining Segments in Component Type

The automotive MLCC market encompasses several other vital component segments, including powertrain, safety systems, and other miscellaneous applications. The powertrain segment maintains its significance by supporting efficient power distribution and management in both traditional and electric vehicles. Safety systems represent another crucial application area, where MLCCs enable reliable operation of critical components such as airbag control modules, anti-lock braking systems, and electronic stability control. The "others" category encompasses various applications including body electronics, lighting systems, and comfort features, contributing to the overall functionality and performance of modern vehicles. Each of these segments plays a unique role in advancing automotive electronics, with manufacturers continuously developing specialized MLCCs to meet the specific requirements of these diverse applications.

Segment Analysis: Case Size

0 603 Segment in Automotive MLCC Market

The 0 603 case size segment has established itself as the dominant force in the automotive MLCC market, commanding approximately 32% market share in 2024. This substantial market position is attributed to the segment's widespread adoption in advanced driver assistance systems (ADAS) and various automotive electronic applications. The compact form factor of 0 603 MLCCs makes them particularly suitable for space-constrained automotive modules, while their reliability and performance characteristics enable seamless integration into sophisticated automotive applications. These MLCCs are extensively utilized in various electronic systems and component applications, particularly in low-voltage applications such as sensors, control circuits, and communication modules, as well as in medium-voltage applications including powertrain control units, motor drives, DC-DC converters, and lighting systems.

1 812 Segment in Automotive MLCC Market

The 1 812 case size segment is experiencing remarkable growth momentum in the automotive MLCC market, with projections indicating an impressive growth rate of approximately 44% during the forecast period 2024-2029. This accelerated growth is driven by the increasing complexity of automotive electronic systems and the rising demand for high-reliability components in modern vehicles. The segment's growth is further fueled by its applications in critical automotive systems, including power distribution, filtering, and decoupling in electronic modules. The robust expansion is also supported by the automotive industry's continued focus on electrification and advanced automated driving features, where 1 812 MLCCs play a crucial role in ensuring stable power supply, noise reduction, and optimal performance of various electronic components.

Remaining Segments in Case Size

The automotive MLCC market encompasses several other important case sizes, including 0 805, 1 206, and 1 210, each serving specific applications within the automotive electronics ecosystem. The 0 805 case size is particularly valued in electric vehicle applications, offering an optimal balance between size and performance for power management systems. The 1 206 case size provides versatility across various automotive applications, while the 1 210 case size caters to high-power applications requiring robust performance characteristics. These segments collectively contribute to the diverse requirements of modern automotive electronics, from basic control systems to advanced safety features and powertrain applications, ensuring manufacturers can select the most appropriate MLCC specifications for their specific needs.

Segment Analysis: Voltage

Less than 50V Segment in Automotive MLCC Market

The less than 50V segment has established itself as the dominant force in the automotive MLCC market, commanding approximately 48% market share in 2024. This segment's prominence is driven by its extensive application across various automotive electronic systems, particularly in advanced driver assistance systems (ADAS), infotainment modules, and interior electronics. The increasing integration of sophisticated electronic features in modern vehicles has further cemented the position of less than 50V MLCCs, as they are essential for functions like sensor interfaces, digital control units, and communication modules. These capacitors excel in providing stable power distribution, effective noise suppression, and reliable voltage regulation for low-voltage automotive applications, making them indispensable in the evolving landscape of vehicle electronics.

More than 200V Segment in Automotive MLCC Market

The more than 200V segment is experiencing remarkable growth trajectory, projected to expand at approximately 38% CAGR from 2024 to 2029. This accelerated growth is primarily attributed to the increasing adoption of electric vehicles (EVs) and the evolution of high-voltage automotive systems. The segment's growth is further propelled by the rising demand for MLCCs in power conversion modules, charging infrastructure, and high-voltage safety systems. As automotive manufacturers continue to push the boundaries of electric vehicle technology and develop more sophisticated power management systems, the demand for high-voltage MLCCs is expected to surge. The segment's robust growth is also supported by advancements in MLCC technology, enabling better performance and reliability in high-voltage applications.

Remaining Segments in Voltage

The 50V to 200V segment serves as a crucial bridge between low and high-voltage applications in the automotive industry. This intermediate voltage range is particularly vital for hybrid vehicles, power management systems, and various powertrain applications. The segment plays a significant role in supporting the transition from traditional internal combustion engines to electrified powertrains, offering solutions for both conventional automotive electronics and emerging electric vehicle applications. These MLCCs are essential components in DC-DC converters, motor drives, and various control systems, contributing to the overall efficiency and performance of modern vehicles.

Segment Analysis: Capacitance

Less than 10 µF Segment in Automotive MLCC Market

The less than 10 μF segment maintains its dominant position in the automotive MLCC market, commanding approximately 48% of the market share in 2024. This segment's prominence is driven by its extensive application across various automotive electronic systems, particularly in infotainment setups and interior lighting components. These MLCCs are crucial for efficient filtering, noise suppression, and voltage stabilization in lower voltage functions, making them indispensable in modern vehicle electronics. The segment's leadership is further strengthened by the increasing integration of advanced driver assistance systems (ADAS) and sophisticated safety features in vehicles, which require reliable and high-performance capacitors in this range. Additionally, the growing trend toward vehicle electrification and the rising adoption of connected car technologies have significantly boosted the demand for less than 10 μF MLCCs, as they are essential components in various control modules and sensor interfaces.

More than 1000 µF Segment in Automotive MLCC Market

The more than 1000 μF segment is experiencing remarkable growth, projected to expand at approximately 38% CAGR from 2024 to 2029. This impressive growth trajectory is primarily attributed to the increasing adoption of electric and hybrid vehicles, where high-capacity MLCCs play a crucial role in power management and energy storage systems. The segment's growth is further fueled by the advancement of automotive powertrains and the integration of sophisticated electronic systems that require robust power handling capabilities. These high-capacity MLCCs are becoming increasingly important in applications such as DC-DC converters, battery management systems, and power distribution modules, where they help ensure stable and efficient power delivery. The segment's expansion is also supported by ongoing technological innovations in MLCC manufacturing, enabling the production of more efficient and reliable high-capacity components suitable for demanding automotive applications.

Remaining Segments in Capacitance

The 10 μF to 1000 μF segment serves as a crucial bridge between low and high capacitance applications in the automotive MLCC market. This intermediate range is particularly vital in power supply circuits, motor control systems, and various automotive control units. These MLCCs offer a balanced combination of size and performance, making them suitable for a wide range of automotive applications where moderate capacitance values are required. The segment plays a significant role in supporting both traditional automotive electronics and emerging technologies, particularly in hybrid vehicles where diverse capacitance requirements need to be met. Their versatility and reliability in managing intermediate power requirements make them essential components in the evolving automotive electronics landscape.

Segment Analysis: Dielectric Type

Class 2 Segment in Automotive MLCC Market

Class 2 MLCCs have emerged as the dominant force in the automotive MLCC market, commanding approximately 52% market share in 2024. These capacitors are extensively utilized across various automotive applications due to their superior performance characteristics and reliability. The surge in motor vehicle production, particularly featuring advanced technologies like ADAS, is significantly boosting the demand for Class 2 dielectric types like X5R, X7R, and Y5V. These components are crucial for ensuring stable and efficient operation in automotive electronic systems, from power management to safety features. The segment's growth is further propelled by the increasing integration of electronic components in modern vehicles, especially in electric and hybrid vehicles where reliable capacitor performance is essential. Class 2 MLCCs are particularly valued for their ability to maintain stable capacitance values across varying operating conditions, making them ideal for automotive applications where environmental factors can significantly impact component performance. The segment is expected to maintain its strong growth trajectory, with projections indicating an impressive growth rate of approximately 39% from 2024 to 2029, driven by the continuous evolution of automotive electronics and the increasing adoption of electric vehicles globally.

Class 1 Segment in Automotive MLCC Market

Class 1 MLCCs represent a crucial segment in the automotive MLCC market, characterized by their high precision and stability across varying temperatures. These capacitors are extensively deployed in automotive applications where precise timing and frequency control are paramount, such as in RF circuits and high-frequency applications. The segment's significance is particularly evident in advanced driver assistance systems (ADAS) and automotive radar applications, where stable capacitance values are essential for accurate signal processing and reliable system performance. Class 1 MLCCs are valued for their low dielectric absorption and excellent high-frequency characteristics, making them indispensable in modern automotive electronics. Their role in ensuring stable operation of critical safety systems and communication modules has become increasingly important as vehicles become more connected and automated. The demand for Class 1 MLCCs is being driven by the automotive industry's push toward more sophisticated electronic systems and the growing integration of advanced communication technologies in vehicles.

Automotive MLCC Market Geography Segment Analysis

Automotive MLCC Market in Asia-Pacific

Asia-Pacific stands as the dominant force in the global automotive MLCC market, commanding approximately 57% of the market share in 2024. The region's supremacy is anchored by key manufacturing powerhouses like Japan, China, and South Korea, which have established themselves as crucial hubs for automotive electronics production. The presence of major MLCC manufacturers and their extensive production facilities has created a robust supply chain ecosystem. The region's leadership is further strengthened by its advanced technological capabilities in electric vehicle production and autonomous driving systems. The growing emphasis on vehicle electrification, particularly in countries like China and Japan, continues to drive substantial demand for MLCCs. Additionally, the region's strong focus on research and development in automotive electronics, coupled with increasing investments in manufacturing capabilities, reinforces its position as the global leader in automotive MLCC production and consumption.

Automotive MLCC Market in Europe

Europe has emerged as a critical market for automotive MLCCs, demonstrating remarkable growth with an approximate 22% growth rate from 2019 to 2024. The region's market dynamics are shaped by its stringent environmental regulations and aggressive push toward vehicle electrification. European automotive manufacturers are increasingly incorporating advanced automotive electronic components in their vehicles, driving the demand for high-performance MLCCs. The region's commitment to reducing carbon emissions has accelerated the adoption of electric and hybrid vehicles, creating substantial opportunities for MLCC manufacturers. The presence of premium automotive manufacturers and their focus on luxury and high-performance vehicles has led to increased integration of sophisticated electronic systems. Furthermore, Europe's leadership in automotive safety standards and autonomous driving technology development continues to fuel the demand for reliable and high-quality MLCCs.

Automotive MLCC Market in North America

North America's automotive MLCC market is poised for substantial growth, with a projected growth rate of approximately 41% from 2024 to 2029. The region's market is characterized by its strong focus on technological innovation and the advanced automotive electronics industry. The increasing adoption of electric vehicles and the integration of sophisticated ADAS features are driving the demand for MLCCs across various automotive applications. The region's automotive industry is undergoing a significant transformation with the push toward vehicle electrification and autonomous driving capabilities. The presence of major automotive manufacturers and their commitment to developing next-generation vehicles has created a strong demand for high-performance electronic components. Additionally, the region's emphasis on vehicle safety and connectivity features continues to drive the integration of advanced electronic systems, further boosting the demand for MLCCs.

Automotive MLCC Market in Rest of the World

The Rest of the World region, encompassing markets in the Middle East, Africa, and Latin America, represents an emerging opportunity in the automotive MLCC landscape. These markets are experiencing a gradual shift toward advanced automotive technologies, driven by increasing consumer demand for modern vehicle features. The region's automotive sector is witnessing a transformation with the growing adoption of electric vehicles and connected car technologies. The Middle Eastern market, in particular, shows promising potential due to its focus on luxury vehicles and advanced automotive features. The increasing investments in automotive manufacturing capabilities and the growing emphasis on vehicle electrification are creating new opportunities for MLCC manufacturers. Furthermore, the region's improving economic conditions and rising consumer awareness about vehicle safety and comfort features are expected to drive the demand for automotive MLCCs in the coming years.

Get Analysis on Important Geographic Markets

Download PDF

Automotive MLCC Industry Overview

Top Companies in Automotive MLCC Market

The automotive MLCC market is characterized by intense competition and continuous innovation among key players like Murata Manufacturing, Yageo Corporation, Samsung Electro-Mechanics, and TDK Corporation. Product innovation remains a cornerstone strategy, with companies focusing on developing high-performance MLCCs specifically designed for electric vehicles, autonomous driving systems, and advanced safety features. Operational agility has become increasingly important as manufacturers adapt to rapidly changing automotive industry demands, particularly in electric vehicle and ADAS applications. Strategic partnerships with automotive OEMs and tier-1 suppliers have emerged as a crucial approach for market penetration and technology development. Companies are actively expanding their manufacturing capabilities, particularly in Asia-Pacific regions, to meet the growing demand and maintain competitive advantages through economies of scale and localized production.

Consolidated Market with Strong Regional Players

The automotive MLCC market exhibits a high degree of consolidation, with the top five companies commanding a significant market share. These dominant players are primarily large, diversified electronics conglomerates with extensive R&D capabilities and established global supply chains. Japanese and South Korean manufacturers maintain particularly strong positions, leveraging their technological expertise and long-standing relationships with automotive manufacturers. The market structure is characterized by high entry barriers due to stringent quality requirements, substantial capital investments, and the need for specialized technological capabilities.

Merger and acquisition activities in the sector are primarily driven by the need to acquire technological capabilities and expand geographic presence. Companies are increasingly focusing on vertical integration to secure supply chains and maintain quality control. Regional players, particularly in emerging markets, are gaining prominence through strategic partnerships and specialized product offerings. The competitive dynamics are further influenced by the increasing importance of local manufacturing capabilities and the need to maintain close proximity to key automotive manufacturing hubs.

Innovation and Adaptability Drive Market Success

Success in the automotive MLCC market increasingly depends on companies' ability to innovate and adapt to evolving automotive industry requirements. Incumbent players must focus on developing next-generation MLCCs that address the specific needs of electric vehicles, autonomous driving systems, and advanced safety features. Companies need to maintain robust R&D investments while simultaneously optimizing production costs and ensuring supply chain resilience. Building strong relationships with automotive OEMs through early engagement in vehicle development cycles and maintaining high quality standards are crucial for maintaining market position.

For contenders seeking to gain market share, specialization in specific applications or regional markets presents opportunities for growth. Success factors include developing innovative solutions for emerging automotive applications, establishing strong quality management systems, and building efficient distribution networks. The ability to navigate regulatory requirements, particularly those related to automotive safety and environmental standards, is becoming increasingly important. Companies must also consider the growing influence of electric vehicle manufacturers and their specific requirements while developing their market strategies. The risk of substitution remains relatively low due to the specialized nature of automotive electronics MLCCs, but companies must continue to innovate to maintain their competitive edge.

Automotive MLCC Market Leaders

-

Kyocera AVX Components Corporation (Kyocera Corporation)

-

Murata Manufacturing Co., Ltd

-

TDK Corporation

-

Walsin Technology Corporation

-

Yageo Corporation

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Automotive MLCC Market News

- July 2023: KEMET, part of the Yageo Corporation developed the X7R automotive grade MLCC X7R. This MLCC is designed to meet the high voltage requirements of automotive subsystems, ranging from 100pF-0.1uF and with a DC voltage range of 500V-1kV. The range of cases available is EIA 0603-1210, and is suitable for both automotive under hoods and in-cabin applications. These MLCCs demonstrate the essential and reliable nature of capacitors, which are essential for the mission and safety of automotive subsystems.

- June 2023: The growing demand for industrial equipments has driven the company to introduce NTS/NTF NTS/NTF Series of SMD type MLCC. These capacitors are rated with 25 to 500 Vdc with a capacitance ranging from 0.010 to 47µF. These MLCCs are used in on-board power supplies,voltage regulators for computers,smoothing circuit of DC-DC converters,etc.

- May 2023: Murata has introduced its EVA series MLCC's and these are suitable for a range of applications, including On-Board Charger (OBC), Inverter (Inverter/DC/DC Converter), Battery Management System (BMS) and Wireless Power Transfer (WPT) implementations. These MLCCs are suitable for the increased isolation required by the 800V Powertrain Migration, while also meeting the miniaturization needs of modern automotive systems.

Free With This Report

We provide a complimentary and exhaustive set of data points on the country and regional level metrics that present the fundamental structure of the industry. Presented in the form of 40+ free charts, the sections cover difficult to find data on various indicators including but not limited to smartphones sales, raw materials pricing trends, and EV sales etc

Automotive MLCC Market Report - Table of Contents

1. EXECUTIVE SUMMARY & KEY FINDINGS

2. REPORT OFFERS

3. INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4. KEY INDUSTRY TRENDS

-

4.1 Automotive Sales

- 4.1.1 Global BEV (Battery Electric Vehicle) Production

- 4.1.2 Global Electric Vehicles Sales

- 4.1.3 Global FCEV (Fuel Cell Electric Vehicle) Production

- 4.1.4 Global HEV (Hybrid Electric Vehicle) Production

- 4.1.5 Global Heavy Commercial Vehicles Sales

- 4.1.6 Global ICEV (Internal Combustion Engine Vehicle) Production

- 4.1.7 Global Light Commercial Vehicles Sales

- 4.1.8 Global Non-Electric Vehicle Sales

- 4.1.9 Global PHEV (Plug-in Hybrid Electric Vehicle) Production

- 4.1.10 Global Passenger Vehicles Sales

- 4.1.11 Global Two-Wheeler Sales

- 4.2 Regulatory Framework

- 4.3 Value Chain & Distribution Channel Analysis

5. MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

-

5.1 Vehicle Type

- 5.1.1 Heavy Commercial Vehicle

- 5.1.2 Light Commercial Vehicle

- 5.1.3 Passenger Vehicle

- 5.1.4 Two-Wheeler

-

5.2 Fuel Type

- 5.2.1 Electric Vehicle

- 5.2.2 Non-Electric Vehicle

-

5.3 Propulsion Type

- 5.3.1 BEV - Battery Electric Vehicle

- 5.3.2 FCEV - Fuel Cell Electric Vehicle

- 5.3.3 HEV - Hybrid Electric Vehicle

- 5.3.4 ICEV - Internal Combustion Engine Vehicle

- 5.3.5 PHEV - Plug-in Hybrid Electric Vehicle

- 5.3.6 Others

-

5.4 Component Type

- 5.4.1 ADAS

- 5.4.2 Infotainment

- 5.4.3 Powertrain

- 5.4.4 Safety System

- 5.4.5 Others

-

5.5 Case Size

- 5.5.1 0 603

- 5.5.2 0 805

- 5.5.3 1 206

- 5.5.4 1 210

- 5.5.5 1 812

- 5.5.6 Others

-

5.6 Voltage

- 5.6.1 50V to 200V

- 5.6.2 Less than 50V

- 5.6.3 More than 200V

-

5.7 Capacitance

- 5.7.1 10 µF to 1000 µF

- 5.7.2 Less than 10 µF

- 5.7.3 More than 1000µF

-

5.8 Dielectric Type

- 5.8.1 Class 1

- 5.8.2 Class 2

-

5.9 Region

- 5.9.1 Asia-Pacific

- 5.9.2 Europe

- 5.9.3 North America

- 5.9.4 Rest of the World

6. COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

-

6.4 Company Profiles

- 6.4.1 Kyocera AVX Components Corporation (Kyocera Corporation)

- 6.4.2 Maruwa Co ltd

- 6.4.3 Murata Manufacturing Co., Ltd

- 6.4.4 Nippon Chemi-Con Corporation

- 6.4.5 Samsung Electro-Mechanics

- 6.4.6 Samwha Capacitor Group

- 6.4.7 Taiyo Yuden Co., Ltd

- 6.4.8 TDK Corporation

- 6.4.9 Vishay Intertechnology Inc.

- 6.4.10 Walsin Technology Corporation

- 6.4.11 Würth Elektronik GmbH & Co. KG

- 6.4.12 Yageo Corporation

- *List Not Exhaustive

7. KEY STRATEGIC QUESTIONS FOR MLCC CEOS

8. APPENDIX

-

8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter’s Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

List of Tables & Figures

- Figure 1:

- SALES OF GLOBAL BEV (BATTERY ELECTRIC VEHICLE) PRODUCTION, MILLION, GLOBAL, 2017 - 2029

- Figure 2:

- SALES OF GLOBAL ELECTRIC VEHICLES , MILLION, GLOBAL, 2017 - 2029

- Figure 3:

- SALES OF GLOBAL FCEV (FUEL CELL ELECTRIC VEHICLE) PRODUCTION, THOUSAND, GLOBAL, 2017 - 2029

- Figure 4:

- SALES OF GLOBAL HEV (HYBRID ELECTRIC VEHICLE) PRODUCTION, MILLION, GLOBAL, 2017 - 2029

- Figure 5:

- SALES OF GLOBAL HEAVY COMMERCIAL VEHICLES , MILLION, GLOBAL, 2017 - 2029

- Figure 6:

- SALES OF GLOBAL ICEV (INTERNAL COMBUSTION ENGINE VEHICLE) PRODUCTION, MILLION, GLOBAL, 2017 - 2029

- Figure 7:

- SALES OF GLOBAL LIGHT COMMERCIAL VEHICLES , MILLION, GLOBAL, 2017 - 2029

- Figure 8:

- SALES OF GLOBAL NON-ELECTRIC VEHICLE , MILLION, GLOBAL, 2017 - 2029

- Figure 9:

- SALES OF GLOBAL PHEV (PLUG-IN HYBRID ELECTRIC VEHICLE) PRODUCTION, THOUSAND, GLOBAL, 2017 - 2029

- Figure 10:

- SALES OF GLOBAL PASSENGER VEHICLES , MILLION, GLOBAL, 2017 - 2029

- Figure 11:

- SALES OF GLOBAL TWO-WHEELER , MILLION, GLOBAL, 2017 - 2029

- Figure 12:

- VOLUME OF GLOBAL AUTOMOTIVE MLCC MARKET, USD, GLOBAL, 2017 - 2029

- Figure 13:

- VALUE OF GLOBAL AUTOMOTIVE MLCC MARKET, USD, GLOBAL, 2017 - 2029

- Figure 14:

- VOLUME OF GLOBAL AUTOMOTIVE MLCC MARKET BY VEHICLE TYPE, , GLOBAL, 2017 - 2029

- Figure 15:

- VALUE OF GLOBAL AUTOMOTIVE MLCC MARKET BY VEHICLE TYPE, USD, GLOBAL, 2017 - 2029

- Figure 16:

- VALUE SHARE OF GLOBAL AUTOMOTIVE MLCC MARKET BY VEHICLE TYPE, %, GLOBAL, 2017 - 2029

- Figure 17:

- VOLUME SHARE OF GLOBAL AUTOMOTIVE MLCC MARKET BY VEHICLE TYPE, %, GLOBAL, 2017 - 2029

- Figure 18:

- VOLUME OF HEAVY COMMERCIAL VEHICLE AUTOMOTIVE MLCC MARKET, NUMBER, , GLOBAL, 2017 - 2029

- Figure 19:

- VALUE OF HEAVY COMMERCIAL VEHICLE AUTOMOTIVE MLCC MARKET, USD, GLOBAL, 2017 - 2029

- Figure 20:

- VOLUME OF LIGHT COMMERCIAL VEHICLE AUTOMOTIVE MLCC MARKET, NUMBER, , GLOBAL, 2017 - 2029

- Figure 21:

- VALUE OF LIGHT COMMERCIAL VEHICLE AUTOMOTIVE MLCC MARKET, USD, GLOBAL, 2017 - 2029

- Figure 22:

- VOLUME OF PASSENGER VEHICLE AUTOMOTIVE MLCC MARKET, NUMBER, , GLOBAL, 2017 - 2029

- Figure 23:

- VALUE OF PASSENGER VEHICLE AUTOMOTIVE MLCC MARKET, USD, GLOBAL, 2017 - 2029

- Figure 24:

- VOLUME OF TWO-WHEELER AUTOMOTIVE MLCC MARKET, NUMBER, , GLOBAL, 2017 - 2029

- Figure 25:

- VALUE OF TWO-WHEELER AUTOMOTIVE MLCC MARKET, USD, GLOBAL, 2017 - 2029

- Figure 26:

- VOLUME OF GLOBAL AUTOMOTIVE MLCC MARKET BY FUEL TYPE, , GLOBAL, 2017 - 2029

- Figure 27:

- VALUE OF GLOBAL AUTOMOTIVE MLCC MARKET BY FUEL TYPE, USD, GLOBAL, 2017 - 2029

- Figure 28:

- VALUE SHARE OF GLOBAL AUTOMOTIVE MLCC MARKET BY FUEL TYPE, %, GLOBAL, 2017 - 2029

- Figure 29:

- VOLUME SHARE OF GLOBAL AUTOMOTIVE MLCC MARKET BY FUEL TYPE, %, GLOBAL, 2017 - 2029

- Figure 30:

- VOLUME OF ELECTRIC VEHICLE AUTOMOTIVE MLCC MARKET, NUMBER, , GLOBAL, 2017 - 2029

- Figure 31:

- VALUE OF ELECTRIC VEHICLE AUTOMOTIVE MLCC MARKET, USD, GLOBAL, 2017 - 2029

- Figure 32:

- VALUE SHARE(%), OF ELECTRIC VEHICLE AUTOMOTIVE MLCC MARKET, %, GLOBAL, 2017 - 2029

- Figure 33:

- VOLUME OF NON-ELECTRIC VEHICLE AUTOMOTIVE MLCC MARKET, NUMBER, , GLOBAL, 2017 - 2029

- Figure 34:

- VALUE OF NON-ELECTRIC VEHICLE AUTOMOTIVE MLCC MARKET, USD, GLOBAL, 2017 - 2029

- Figure 35:

- VOLUME OF GLOBAL AUTOMOTIVE MLCC MARKET BY PROPULSION TYPE, , GLOBAL, 2017 - 2029

- Figure 36:

- VALUE OF GLOBAL AUTOMOTIVE MLCC MARKET BY PROPULSION TYPE, USD, GLOBAL, 2017 - 2029

- Figure 37:

- VALUE SHARE OF GLOBAL AUTOMOTIVE MLCC MARKET BY PROPULSION TYPE, %, GLOBAL, 2017 - 2029

- Figure 38:

- VOLUME SHARE OF GLOBAL AUTOMOTIVE MLCC MARKET BY PROPULSION TYPE, %, GLOBAL, 2017 - 2029

- Figure 39:

- VOLUME OF BEV - BATTERY ELECTRIC VEHICLE AUTOMOTIVE MLCC MARKET, NUMBER, , GLOBAL, 2017 - 2029

- Figure 40:

- VALUE OF BEV - BATTERY ELECTRIC VEHICLE AUTOMOTIVE MLCC MARKET, USD, GLOBAL, 2017 - 2029

- Figure 41:

- VOLUME OF FCEV - FUEL CELL ELECTRIC VEHICLE AUTOMOTIVE MLCC MARKET, NUMBER, , GLOBAL, 2017 - 2029

- Figure 42:

- VALUE OF FCEV - FUEL CELL ELECTRIC VEHICLE AUTOMOTIVE MLCC MARKET, USD, GLOBAL, 2017 - 2029

- Figure 43:

- VOLUME OF HEV - HYBRID ELECTRIC VEHICLE AUTOMOTIVE MLCC MARKET, NUMBER, , GLOBAL, 2017 - 2029

- Figure 44:

- VALUE OF HEV - HYBRID ELECTRIC VEHICLE AUTOMOTIVE MLCC MARKET, USD, GLOBAL, 2017 - 2029

- Figure 45:

- VOLUME OF ICEV - INTERNAL COMBUSTION ENGINE VEHICLE AUTOMOTIVE MLCC MARKET, NUMBER, , GLOBAL, 2017 - 2029

- Figure 46:

- VALUE OF ICEV - INTERNAL COMBUSTION ENGINE VEHICLE AUTOMOTIVE MLCC MARKET, USD, GLOBAL, 2017 - 2029

- Figure 47:

- VOLUME OF PHEV - PLUG-IN HYBRID ELECTRIC VEHICLE AUTOMOTIVE MLCC MARKET, NUMBER, , GLOBAL, 2017 - 2029

- Figure 48:

- VALUE OF PHEV - PLUG-IN HYBRID ELECTRIC VEHICLE AUTOMOTIVE MLCC MARKET, USD, GLOBAL, 2017 - 2029

- Figure 49:

- VOLUME OF OTHERS AUTOMOTIVE MLCC MARKET, NUMBER, , GLOBAL, 2017 - 2029

- Figure 50:

- VALUE OF OTHERS AUTOMOTIVE MLCC MARKET, USD, GLOBAL, 2017 - 2029

- Figure 51:

- VOLUME OF GLOBAL AUTOMOTIVE MLCC MARKET BY COMPONENT TYPE, , GLOBAL, 2017 - 2029

- Figure 52:

- VALUE OF GLOBAL AUTOMOTIVE MLCC MARKET BY COMPONENT TYPE, USD, GLOBAL, 2017 - 2029

- Figure 53:

- VALUE SHARE OF GLOBAL AUTOMOTIVE MLCC MARKET BY COMPONENT TYPE, %, GLOBAL, 2017 - 2029

- Figure 54:

- VOLUME SHARE OF GLOBAL AUTOMOTIVE MLCC MARKET BY COMPONENT TYPE, %, GLOBAL, 2017 - 2029

- Figure 55:

- VOLUME OF ADAS AUTOMOTIVE MLCC MARKET, NUMBER, , GLOBAL, 2017 - 2029

- Figure 56:

- VALUE OF ADAS AUTOMOTIVE MLCC MARKET, USD, GLOBAL, 2017 - 2029

- Figure 57:

- VOLUME OF INFOTAINMENT AUTOMOTIVE MLCC MARKET, NUMBER, , GLOBAL, 2017 - 2029

- Figure 58:

- VALUE OF INFOTAINMENT AUTOMOTIVE MLCC MARKET, USD, GLOBAL, 2017 - 2029

- Figure 59:

- VOLUME OF POWERTRAIN AUTOMOTIVE MLCC MARKET, NUMBER, , GLOBAL, 2017 - 2029

- Figure 60:

- VALUE OF POWERTRAIN AUTOMOTIVE MLCC MARKET, USD, GLOBAL, 2017 - 2029

- Figure 61:

- VOLUME OF SAFETY SYSTEM AUTOMOTIVE MLCC MARKET, NUMBER, , GLOBAL, 2017 - 2029

- Figure 62:

- VALUE OF SAFETY SYSTEM AUTOMOTIVE MLCC MARKET, USD, GLOBAL, 2017 - 2029

- Figure 63:

- VOLUME OF OTHERS AUTOMOTIVE MLCC MARKET, NUMBER, , GLOBAL, 2017 - 2029

- Figure 64:

- VALUE OF OTHERS AUTOMOTIVE MLCC MARKET, USD, GLOBAL, 2017 - 2029

- Figure 65:

- VOLUME OF GLOBAL AUTOMOTIVE MLCC MARKET BY CASE SIZE, , GLOBAL, 2017 - 2029

- Figure 66:

- VALUE OF GLOBAL AUTOMOTIVE MLCC MARKET BY CASE SIZE, USD, GLOBAL, 2017 - 2029

- Figure 67:

- VALUE SHARE OF GLOBAL AUTOMOTIVE MLCC MARKET BY CASE SIZE, %, GLOBAL, 2017 - 2029

- Figure 68:

- VOLUME SHARE OF GLOBAL AUTOMOTIVE MLCC MARKET BY CASE SIZE, %, GLOBAL, 2017 - 2029

- Figure 69:

- VOLUME OF 0 603 AUTOMOTIVE MLCC MARKET, NUMBER, , GLOBAL, 2017 - 2029

- Figure 70:

- VALUE OF 0 603 AUTOMOTIVE MLCC MARKET, USD, GLOBAL, 2017 - 2029

- Figure 71:

- VOLUME OF 0 805 AUTOMOTIVE MLCC MARKET, NUMBER, , GLOBAL, 2017 - 2029

- Figure 72:

- VALUE OF 0 805 AUTOMOTIVE MLCC MARKET, USD, GLOBAL, 2017 - 2029

- Figure 73:

- VOLUME OF 1 206 AUTOMOTIVE MLCC MARKET, NUMBER, , GLOBAL, 2017 - 2029

- Figure 74:

- VALUE OF 1 206 AUTOMOTIVE MLCC MARKET, USD, GLOBAL, 2017 - 2029

- Figure 75:

- VOLUME OF 1 210 AUTOMOTIVE MLCC MARKET, NUMBER, , GLOBAL, 2017 - 2029

- Figure 76:

- VALUE OF 1 210 AUTOMOTIVE MLCC MARKET, USD, GLOBAL, 2017 - 2029

- Figure 77:

- VOLUME OF 1 812 AUTOMOTIVE MLCC MARKET, NUMBER, , GLOBAL, 2017 - 2029

- Figure 78:

- VALUE OF 1 812 AUTOMOTIVE MLCC MARKET, USD, GLOBAL, 2017 - 2029

- Figure 79:

- VOLUME OF OTHERS AUTOMOTIVE MLCC MARKET, NUMBER, , GLOBAL, 2017 - 2029

- Figure 80:

- VALUE OF OTHERS AUTOMOTIVE MLCC MARKET, USD, GLOBAL, 2017 - 2029

- Figure 81:

- VOLUME OF GLOBAL AUTOMOTIVE MLCC MARKET BY VOLTAGE, , GLOBAL, 2017 - 2029

- Figure 82:

- VALUE OF GLOBAL AUTOMOTIVE MLCC MARKET BY VOLTAGE, USD, GLOBAL, 2017 - 2029

- Figure 83:

- VALUE SHARE OF GLOBAL AUTOMOTIVE MLCC MARKET BY VOLTAGE, %, GLOBAL, 2017 - 2029

- Figure 84:

- VOLUME SHARE OF GLOBAL AUTOMOTIVE MLCC MARKET BY VOLTAGE, %, GLOBAL, 2017 - 2029

- Figure 85:

- VOLUME OF 50V TO 200V AUTOMOTIVE MLCC MARKET, NUMBER, , GLOBAL, 2017 - 2029

- Figure 86:

- VALUE OF 50V TO 200V AUTOMOTIVE MLCC MARKET, USD, GLOBAL, 2017 - 2029

- Figure 87:

- VOLUME OF LESS THAN 50V AUTOMOTIVE MLCC MARKET, NUMBER, , GLOBAL, 2017 - 2029

- Figure 88:

- VALUE OF LESS THAN 50V AUTOMOTIVE MLCC MARKET, USD, GLOBAL, 2017 - 2029

- Figure 89:

- VOLUME OF MORE THAN 200V AUTOMOTIVE MLCC MARKET, NUMBER, , GLOBAL, 2017 - 2029

- Figure 90:

- VALUE OF MORE THAN 200V AUTOMOTIVE MLCC MARKET, USD, GLOBAL, 2017 - 2029

- Figure 91:

- VOLUME OF GLOBAL AUTOMOTIVE MLCC MARKET BY CAPACITANCE, , GLOBAL, 2017 - 2029

- Figure 92:

- VALUE OF GLOBAL AUTOMOTIVE MLCC MARKET BY CAPACITANCE, USD, GLOBAL, 2017 - 2029

- Figure 93:

- VALUE SHARE OF GLOBAL AUTOMOTIVE MLCC MARKET BY CAPACITANCE, %, GLOBAL, 2017 - 2029

- Figure 94:

- VOLUME SHARE OF GLOBAL AUTOMOTIVE MLCC MARKET BY CAPACITANCE, %, GLOBAL, 2017 - 2029

- Figure 95:

- VOLUME OF 10 ΜF TO 1000 ΜF AUTOMOTIVE MLCC MARKET, NUMBER, , GLOBAL, 2017 - 2029

- Figure 96:

- VALUE OF 10 ΜF TO 1000 ΜF AUTOMOTIVE MLCC MARKET, USD, GLOBAL, 2017 - 2029

- Figure 97:

- VOLUME OF LESS THAN 10 ΜF AUTOMOTIVE MLCC MARKET, NUMBER, , GLOBAL, 2017 - 2029

- Figure 98:

- VALUE OF LESS THAN 10 ΜF AUTOMOTIVE MLCC MARKET, USD, GLOBAL, 2017 - 2029

- Figure 99:

- VOLUME OF MORE THAN 1000 ΜF AUTOMOTIVE MLCC MARKET, NUMBER, , GLOBAL, 2017 - 2029

- Figure 100:

- VALUE OF MORE THAN 1000 ΜF AUTOMOTIVE MLCC MARKET, USD, GLOBAL, 2017 - 2029

- Figure 101:

- VOLUME OF GLOBAL AUTOMOTIVE MLCC MARKET BY DIELECTRIC TYPE, , GLOBAL, 2017 - 2029

- Figure 102:

- VALUE OF GLOBAL AUTOMOTIVE MLCC MARKET BY DIELECTRIC TYPE, USD, GLOBAL, 2017 - 2029

- Figure 103:

- VALUE SHARE OF GLOBAL AUTOMOTIVE MLCC MARKET BY DIELECTRIC TYPE, %, GLOBAL, 2017 - 2029

- Figure 104:

- VOLUME SHARE OF GLOBAL AUTOMOTIVE MLCC MARKET BY DIELECTRIC TYPE, %, GLOBAL, 2017 - 2029

- Figure 105:

- VOLUME OF CLASS 1 AUTOMOTIVE MLCC MARKET, NUMBER, , GLOBAL, 2017 - 2029

- Figure 106:

- VALUE OF CLASS 1 AUTOMOTIVE MLCC MARKET, USD, GLOBAL, 2017 - 2029

- Figure 107:

- VOLUME OF CLASS 2 AUTOMOTIVE MLCC MARKET, NUMBER, , GLOBAL, 2017 - 2029

- Figure 108:

- VALUE OF CLASS 2 AUTOMOTIVE MLCC MARKET, USD, GLOBAL, 2017 - 2029

- Figure 109:

- VOLUME OF AUTOMOTIVE MLCC MARKET, BY REGION, NUMBER, , 2017 - 2029

- Figure 110:

- VALUE OF AUTOMOTIVE MLCC MARKET, BY REGION, USD, 2017 - 2029

- Figure 111:

- CAGR OF AUTOMOTIVE MLCC MARKET, BY REGION, %, 2017 - 2029

- Figure 112:

- CAGR OF AUTOMOTIVE MLCC MARKET, BY REGION, %, 2017 - 2029

- Figure 113:

- VOLUME OF GLOBAL AUTOMOTIVE MLCC MARKET,NUMBER, IN ASIA-PACIFIC, 2017 - 2029

- Figure 114:

- VALUE OF GLOBAL AUTOMOTIVE MLCC MARKET, IN ASIA-PACIFIC, 2017 - 2029

- Figure 115:

- VOLUME OF GLOBAL AUTOMOTIVE MLCC MARKET,NUMBER, IN EUROPE, 2017 - 2029

- Figure 116:

- VALUE OF GLOBAL AUTOMOTIVE MLCC MARKET, IN EUROPE, 2017 - 2029

- Figure 117:

- VOLUME OF GLOBAL AUTOMOTIVE MLCC MARKET,NUMBER, IN NORTH AMERICA, 2017 - 2029

- Figure 118:

- VALUE OF GLOBAL AUTOMOTIVE MLCC MARKET, IN NORTH AMERICA, 2017 - 2029

- Figure 119:

- VOLUME OF GLOBAL AUTOMOTIVE MLCC MARKET,NUMBER, IN REST OF THE WORLD, 2017 - 2029

- Figure 120:

- VALUE OF GLOBAL AUTOMOTIVE MLCC MARKET, IN REST OF THE WORLD, 2017 - 2029

- Figure 121:

- MOST ACTIVE COMPANIES BY NUMBER OF STRATEGIC MOVES, COUNT, GLOBAL, 2017 - 2029

- Figure 122:

- MOST ADOPTED STRATEGIES, COUNT, GLOBAL, 2017 - 2029

- Figure 123:

- VALUE SHARE OF MAJOR PLAYERS, %, GLOBAL, 2017 - 2029

Automotive MLCC Industry Segmentation

Heavy Commercial Vehicle, Light Commercial Vehicle, Passenger Vehicle, Two-Wheeler are covered as segments by Vehicle Type. Electric Vehicle, Non-Electric Vehicle are covered as segments by Fuel Type. BEV - Battery Electric Vehicle, FCEV - Fuel Cell Electric Vehicle, HEV - Hybrid Electric Vehicle, ICEV - Internal Combustion Engine Vehicle, PHEV - Plug-in Hybrid Electric Vehicle, Others are covered as segments by Propulsion Type. ADAS, Infotainment, Powertrain, Safety System, Others are covered as segments by Component Type. 0 603, 0 805, 1 206, 1 210, 1 812, Others are covered as segments by Case Size. 50V to 200V, Less than 50V, More than 200V are covered as segments by Voltage. 10 µF to 1000 µF, Less than 10 µF, More than 1000µF are covered as segments by Capacitance. Class 1, Class 2 are covered as segments by Dielectric Type. Asia-Pacific, Europe, North America are covered as segments by Region.| Vehicle Type | Heavy Commercial Vehicle |

| Light Commercial Vehicle | |

| Passenger Vehicle | |

| Two-Wheeler | |

| Fuel Type | Electric Vehicle |

| Non-Electric Vehicle | |

| Propulsion Type | BEV - Battery Electric Vehicle |

| FCEV - Fuel Cell Electric Vehicle | |

| HEV - Hybrid Electric Vehicle | |

| ICEV - Internal Combustion Engine Vehicle | |

| PHEV - Plug-in Hybrid Electric Vehicle | |

| Others | |

| Component Type | ADAS |

| Infotainment | |

| Powertrain | |

| Safety System | |

| Others | |

| Case Size | 0 603 |

| 0 805 | |

| 1 206 | |

| 1 210 | |

| 1 812 | |

| Others | |

| Voltage | 50V to 200V |

| Less than 50V | |

| More than 200V | |

| Capacitance | 10 µF to 1000 µF |

| Less than 10 µF | |

| More than 1000µF | |

| Dielectric Type | Class 1 |

| Class 2 | |

| Region | Asia-Pacific |

| Europe | |

| North America | |

| Rest of the World |

Need A Different Region or Segment?

Customize Now

Market Definition

- MLCC (Multilayer Ceramic Capacitor) - A type of capacitor that consists of multiple layers of ceramic material, alternating with conductive layers, used for energy storage and filtering in electronic circuits.

- Voltage - The maximum voltage that a capacitor can safely withstand without experiencing breakdown or failure. It is typically expressed in volts (V)

- Capacitance - The measure of a capacitor's ability to store electrical charge, expressed in farads (F). It determines the amount of energy that can be stored in the capacitor

- Case Size - The physical dimensions of an MLCC, typically expressed in codes or millimeters, indicating its length, width, and height

| Keyword | Definition |

|---|---|

| MLCC (Multilayer Ceramic Capacitor) | A type of capacitor that consists of multiple layers of ceramic material, alternating with conductive layers, used for energy storage and filtering in electronic circuits. |

| Capacitance | The measure of a capacitor's ability to store electrical charge, expressed in farads (F). It determines the amount of energy that can be stored in the capacitor |

| Voltage Rating | The maximum voltage that a capacitor can safely withstand without experiencing breakdown or failure. It is typically expressed in volts (V) |

| ESR (Equivalent Series Resistance) | The total resistance of a capacitor, including its internal resistance and parasitic resistances. It affects the capacitor's ability to filter high-frequency noise and maintain stability in a circuit. |

| Dielectric Material | The insulating material used between the conductive layers of a capacitor. In MLCCs, commonly used dielectric materials include ceramic materials like barium titanate and ferroelectric materials |

| SMT (Surface Mount Technology) | A method of electronic component assembly that involves mounting components directly onto the surface of a printed circuit board (PCB) instead of through-hole mounting. |

| Solderability | The ability of a component, such as an MLCC, to form a reliable and durable solder joint when subjected to soldering processes. Good solderability is crucial for proper assembly and functionality of MLCCs on PCBs. |

| RoHS (Restriction of Hazardous Substances) | A directive that restricts the use of certain hazardous materials, such as lead, mercury, and cadmium, in electrical and electronic equipment. Compliance with RoHS is essential for automotive MLCCs due to environmental regulations |

| Case Size | The physical dimensions of an MLCC, typically expressed in codes or millimeters, indicating its length, width, and height |

| Flex Cracking | A phenomenon where MLCCs can develop cracks or fractures due to mechanical stress caused by bending or flexing of the PCB. Flex cracking can lead to electrical failures and should be avoided during PCB assembly and handling. |

| Aging | MLCCs can experience changes in their electrical properties over time due to factors like temperature, humidity, and applied voltage. Aging refers to the gradual alteration of MLCC characteristics, which can impact the performance of electronic circuits. |

| ASPs (Average Selling Prices) | The average price at which MLCCs are sold in the market, expressed in USD million. It reflects the average price per unit |

| Voltage | The electrical potential difference across an MLCC, often categorized into low-range voltage, mid-range voltage, and high-range voltage, indicating different voltage levels |

| MLCC RoHS Compliance | Compliance with the Restriction of Hazardous Substances (RoHS) directive, which restricts the use of certain hazardous substances, such as lead, mercury, cadmium, and others, in the manufacturing of MLCCs, promoting environmental protection and safety |

| Mounting Type | The method used to attach MLCCs to a circuit board, such as surface mount, metal cap, and radial lead, which indicates the different mounting configurations |

| Dielectric Type | The type of dielectric material used in MLCCs, often categorized into Class 1 and Class 2, representing different dielectric characteristics and performance |

| Low-Range Voltage | MLCCs designed for applications that require lower voltage levels, typically in the low voltage range |

| Mid-Range Voltage | MLCCs designed for applications that require moderate voltage levels, typically in the middle range of voltage requirements |

| High-Range Voltage | MLCCs designed for applications that require higher voltage levels, typically in the high voltage range |

| Low-Range Capacitance | MLCCs with lower capacitance values, suitable for applications that require smaller energy storage |

| Mid-Range Capacitance | MLCCs with moderate capacitance values, suitable for applications that require intermediate energy storage |

| High-Range Capacitance | MLCCs with higher capacitance values, suitable for applications that require larger energy storage |

| Surface Mount | MLCCs designed for direct surface mounting onto a printed circuit board (PCB), allowing for efficient space utilization and automated assembly |

| Class 1 Dielectric | MLCCs with Class 1 dielectric material, characterized by a high level of stability, low dissipation factor, and low capacitance change over temperature. They are suitable for applications requiring precise capacitance values and stability |

| Class 2 Dielectric | MLCCs with Class 2 dielectric material, characterized by a high capacitance value, high volumetric efficiency, and moderate stability. They are suitable for applications that require higher capacitance values and are less sensitive to capacitance changes over temperature |

| RF (Radio Frequency) | It refers to the range of electromagnetic frequencies used in wireless communication and other applications, typically from 3 kHz to 300 GHz, enabling the transmission and reception of radio signals for various wireless devices and systems. |

| Metal Cap | A protective metal cover used in certain MLCCs (Multilayer Ceramic Capacitors) to enhance durability and shield against external factors like moisture and mechanical stress |

| Radial Lead | A terminal configuration in specific MLCCs where electrical leads extend radially from the ceramic body, facilitating easy insertion and soldering in through-hole mounting applications. |

| Temperature Stability | The ability of MLCCs to maintain their capacitance values and performance characteristics across a range of temperatures, ensuring reliable operation in varying environmental conditions. |

| Low ESR (Equivalent Series Resistance) | MLCCs with low ESR values have minimal resistance to the flow of AC signals, allowing for efficient energy transfer and reduced power losses in high-frequency applications. |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence has followed the following methodology in all our MLCC reports.

- Step 1: Identify Data Points: In this step, we identified key data points crucial for comprehending the MLCC market. This included historical and current production figures, as well as critical device metrics such as attachment rate, sales, production volume, and average selling price. Additionally, we estimated future production volumes and attachment rates for MLCCs in each device category. Lead times were also determined, aiding in forecasting market dynamics by understanding the time required for production and delivery, thereby enhancing the accuracy of our projections.

- Step 2: Identify Key Variables: In this step, we focused on identifying crucial variables essential for constructing a robust forecasting model for the MLCC market. These variables include lead times, trends in raw material prices used in MLCC manufacturing, automotive sales data, consumer electronics sales figures, and electric vehicle (EV) sales statistics. Through an iterative process, we determined the necessary variables for accurate market forecasting and proceeded to develop the forecasting model based on these identified variables.

- Step 3: Build a Market Model: In this step, we utilized production data and key industry trend variables, such as average pricing, attachment rate, and forecasted production data, to construct a comprehensive market estimation model. By integrating these critical variables, we developed a robust framework for accurately forecasting market trends and dynamics, thereby facilitating informed decision-making within the MLCC market landscape.

- Step 4: Validate and Finalize: In this crucial step, all market numbers and variables derived through an internal mathematical model were validated through an extensive network of primary research experts from all the markets studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step 5: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases, and Subscription Platform

Get More Details On Research Methodology

Download PDF