| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 123.50 Billion |

| Market Size (2030) | USD 157.55 Billion |

| CAGR (2025 - 2030) | 4.99 % |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

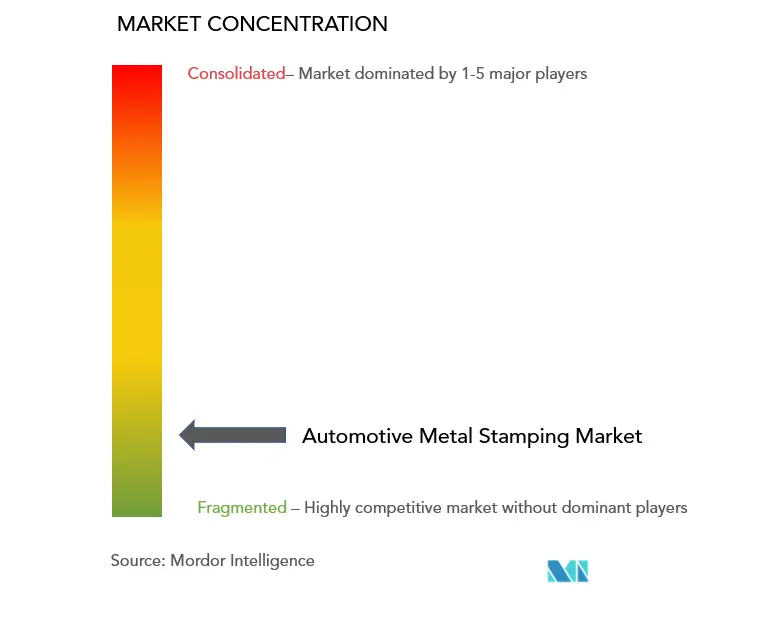

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Automotive Metal Stamping Market Analysis

The Automotive Metal Stamping Market size is estimated at USD 123.50 billion in 2025, and is expected to reach USD 157.55 billion by 2030, at a CAGR of 4.99% during the forecast period (2025-2030).

The automotive metal stamping industry is experiencing a significant transformation driven by the global shift towards sustainable transportation solutions. The increasing adoption of electric vehicles has become a cornerstone of this evolution, with electric vehicles accounting for 9% of total global vehicle sales in recent years. This transition is compelling manufacturers to adapt their production processes and develop innovative automotive metal stamping solutions specifically designed for electric vehicle components, including battery enclosures, motor housings, and structural elements that require precise engineering and advanced manufacturing capabilities.

Technological advancements in automotive stamping processes are revolutionizing the industry landscape, with manufacturers increasingly adopting laser metal stamping and hydraulic metal stamping technologies. These innovations are particularly crucial as the industry focuses on producing lightweight components while maintaining structural integrity. The integration of automation and precision engineering has enabled manufacturers to achieve higher production efficiencies while reducing material waste, leading to more cost-effective manufacturing processes and improved product quality.

The commercial vehicle sector is emerging as a significant growth driver for the automotive metal stamping market, particularly in Europe where over 75% of inland cargo transport, approximately 1,750 billion metric ton-kilometers, travels by road. This substantial reliance on road transportation has created a sustained demand for commercial vehicle components, prompting manufacturers to develop more durable and efficient stamped parts. The industry is witnessing a parallel trend towards the electrification of commercial fleets, exemplified by initiatives such as the London Metropolitan Police and Fire Service's plan to achieve a zero-emission fleet by 2030.

The market is characterized by increasing strategic partnerships between original equipment manufacturers (OEMs) and automotive metal stamping companies, fostering innovation and technological advancement. China's dominant position in global automotive production, accounting for over 30% of worldwide vehicle production, has established the region as a crucial hub for metal stamping operations. This has led to significant investments in manufacturing capabilities and the establishment of new production facilities, particularly focusing on advanced stamping technologies for next-generation vehicles and automotive metal components.

Automotive Metal Stamping Market Trends

Stringent EPA Regulations and CAFE Standards

The automotive regulatory framework, particularly in Europe and North America, continues to play a pivotal role in shaping the trends in the automotive metal stamping market. The European Commission's ambitious climate neutrality goals, which aim for at least a 55% net reduction in greenhouse gas emissions by 2030 compared to 1990 levels, have pushed manufacturers to adopt innovative metal forming technologies in the automotive sector for producing lighter and more fuel-efficient vehicles. These regulations have created a challenging yet evolving environment for automotive manufacturers, compelling them to invest in advanced metal stamping processes that can produce components meeting strict weight and performance requirements.

The automotive industry's response to these regulations has led to increased adoption of sophisticated stamping techniques in the automotive industry, particularly in the production of lightweight body panels and structural components. The focus has shifted towards utilizing advanced high-strength steels and aluminum alloys through precision stamping processes, enabling manufacturers to achieve the desired balance between structural integrity and weight reduction. This trend is further supported by recent technological advancements, such as Fischer Group's implementation of the cutting-edge TruLaser 8000 Coil Edition blanking system in February 2023, which can process up to 25 tons of coiled sheet metal while ensuring enhanced material utilization and resource efficiency.

Understand The Key Trends Shaping This Market

Download PDF

Increasing Adoption of Electric Vehicles

The rapid transition towards electric vehicles has emerged as a significant driver for the automotive metal stamping market, with projections indicating that by 2040, approximately 54% of new car sales and 33% of the global car fleet will be electric in Europe. This shift has created unprecedented demand for specialized metal stamping solutions, particularly in the production of battery enclosures, motor housings, and lightweight structural components essential for electric vehicle manufacturing. The industry has witnessed significant investments in new stamping technologies specifically designed to meet the unique requirements of electric vehicle components, as evidenced by Gestamp's strategic expansion with its fourth hot stamping production line in India, announced in January 2023.

The evolution of electric vehicle architecture has necessitated innovations in sheet metal stamping for automotive applications to accommodate the integration of battery systems and electric powertrains while maintaining optimal vehicle performance. Metal stamping manufacturers are increasingly focusing on developing solutions that can produce complex geometries and lightweight components without compromising structural integrity. This trend is particularly evident in the growing demand for aluminum extrusions and high-pressure aluminum stamping applications, which are crucial for manufacturing battery housings, motor housings, and body structural panels. The industry's commitment to supporting electric vehicle production is further demonstrated through strategic partnerships and investments in advanced stamping technologies that can deliver the precision and quality required for next-generation electric vehicles.

Segment Analysis: By Technology

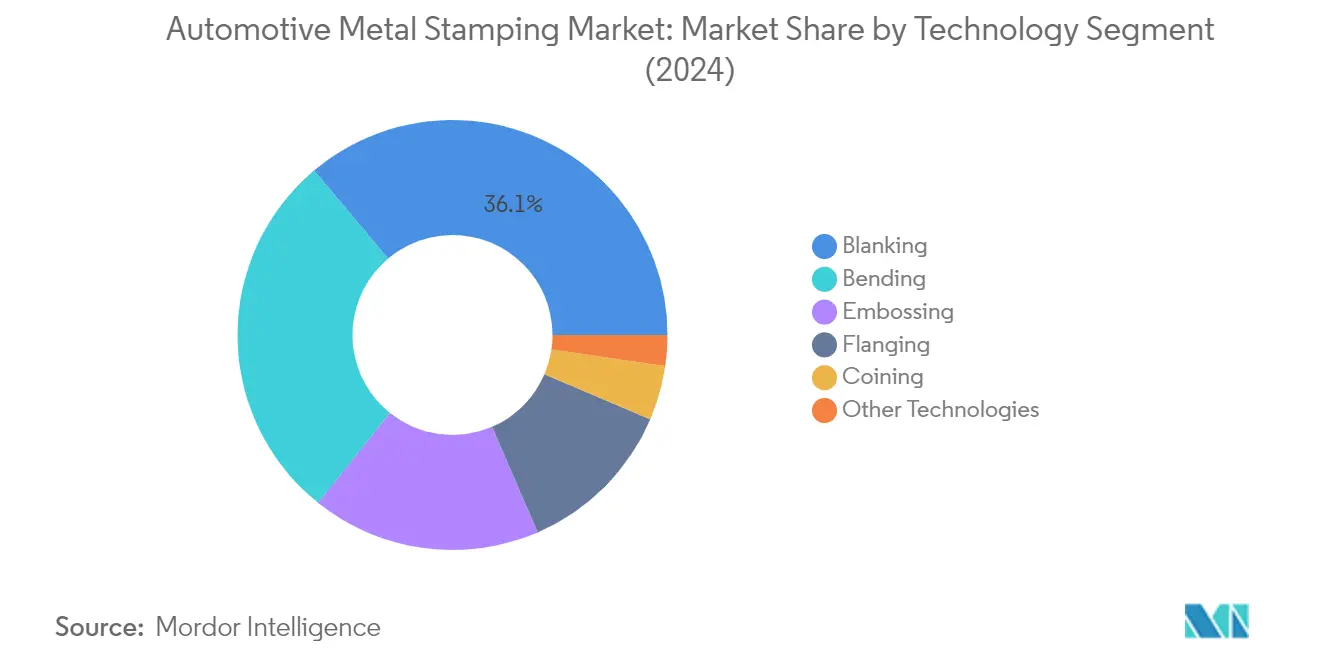

Blanking Segment in Automotive Metal Stamping Market

The blanking segment continues to dominate the automotive stamping market, holding approximately 36% market share in 2024. This significant market position is primarily driven by the increased demand for efficient vehicles requiring innovative and unique outer body structures with aerodynamic efficiency. Blanking metal stamping technology enables manufacturers to fabricate metal into smaller and more manageable pieces that can be tightly packaged in and around vehicles. Major automotive manufacturers are increasingly investing in blanking capabilities to enhance their in-house metal pressing capabilities and improve production efficiency. The technology's ability to produce precise components while maintaining material integrity has made it particularly valuable in the production of vehicle body panels and structural components.

Flanging Segment in Automotive Metal Stamping Market

The flanging segment is emerging as the fastest-growing technology in the automotive metal forming market, projected to grow at approximately 6% during 2024-2029. This growth is primarily attributed to the increasing demand for components that need to withstand high mechanical loads while displaying low friction properties in automotive applications. The technology is particularly crucial in manufacturing rugged environment components like powertrain applications, engine pistons, and driveshaft components. The rapid expansion of the electric vehicle sector has further boosted the demand for flanging technology, as it is essential in producing efficient and high load-withstanding driveshafts and motors for electric vehicles. The technology's ability to ensure structural integrity while maintaining optimal performance characteristics has made it increasingly valuable in modern automotive manufacturing.

Remaining Segments in Automotive Metal Stamping Technology

The automotive metal components market encompasses several other significant technologies including bending, embossing, coining, and other specialized processes. Bending technology plays a crucial role in modifying metal structures into curved surfaces for external body panels, while embossing is essential for producing raised or sunken designs in sheet metal used for various automotive applications. Coining technology, known for high-pressure stamping, is particularly valuable in manufacturing components that require permanent bends and high structural integrity. These technologies collectively contribute to the diverse requirements of modern vehicle manufacturing, from aesthetic elements to crucial structural components, each serving specific purposes in the automotive production process.

Segment Analysis: By Process

Roll Forming Segment in Automotive Metal Stamping Market

Roll forming dominates the automotive stamping market, commanding approximately 44% market share in 2024, driven by its versatility in producing complex metal designs without compromising structural integrity. This process has become increasingly crucial in the automotive industry as manufacturers face the challenge of fitting components into tight spaces within vehicles, particularly in electric vehicles where battery placement demands innovative solutions. The segment's prominence is further reinforced by its ability to accommodate heavy-weight batteries firmly into constricted spaces while maintaining the structural integrity of the components. Major automotive manufacturers are increasingly adopting roll forming techniques for manufacturing critical components like metal brackets, aluminum components for electromagnetic shielding, and high-precision bipolar plates used in hydrogen fuel stacks.

Hot Stamping Segment in Automotive Metal Stamping Market

The hot stamping segment is experiencing remarkable growth in the automotive metal forming market, projected to grow at approximately 10% during 2024-2029. This substantial growth is primarily attributed to the increasing demand for high-quality finished components in luxury vehicles and high-performance sports vehicles. The segment's expansion is further driven by the automotive industry's shift towards premium quality components with superior surface finishes, particularly in electric vehicles and luxury car segments. Major automotive manufacturers are increasingly investing in hot stamping facilities to meet the growing demand for premium-quality components, with several companies establishing dedicated hot stamping plants to cater to the high-end automotive market's specific requirements.

Remaining Segments in Process Segmentation

The automotive metal stamping market's remaining segments include automotive sheet metal forming, metal fabrication, and other processes, each serving distinct purposes in the automotive manufacturing ecosystem. Automotive sheet metal forming plays a crucial role in producing body panels and powertrain components, particularly in rigorous working environments where harsh vibrations and temperatures are constant factors. Automotive metal fabrication represents a conventional yet essential technique in manufacturing desired body panels, while other processes encompass specialized techniques like metal extrusion, primarily used for aluminum products. These segments collectively contribute to the market's diversity, offering manufacturers various options to meet specific component requirements across different vehicle types and applications.

Segment Analysis: By Vehicle Type

Passenger Cars Segment in Automotive Metal Stamping Market

The passenger cars segment continues to dominate the global automotive metal stamping market, holding approximately 62% market share in 2024. This dominance is primarily attributed to the increasing production and sales of passenger cars in several emerging economies, including India, Thailand, Indonesia, Egypt, and other Middle East & African countries. China maintains the largest share for passenger cars, followed by the United States, Japan, Germany, India, and South Korea, driven by improving road infrastructure and rising disposable incomes of the middle-class population. The global shift towards electric vehicles in the passenger car segment has created additional opportunities for metal stamping applications, particularly in manufacturing lightweight components and battery enclosures. The segment's growth is further supported by the increasing adoption of automation technologies in manufacturing processes and the rising demand for premium and luxury vehicles that require high-quality stamped components.

Commercial Vehicles Segment in Automotive Metal Stamping Market

The commercial vehicles segment is projected to be the fastest-growing segment in the automotive metal stamping market, with an expected growth rate of approximately 5% during 2024-2029. This accelerated growth is driven by the increasing demand for pickup trucks, buses, vans, and other light commercial vehicles, particularly in the logistics and transportation sectors. The segment's growth is further propelled by the rising adoption of electric commercial vehicles, with many government organizations worldwide upgrading to all-electric fleets. The expansion of e-commerce and the subsequent need for delivery vehicles has created additional demand for metal stamped components in the commercial vehicle sector. The segment is also benefiting from technological advancements in metal stamping processes, which enable the production of lighter yet stronger components, helping manufacturers meet stringent emission regulations while maintaining vehicle durability and performance.

Automotive Metal Stamping Market Geography Segment Analysis

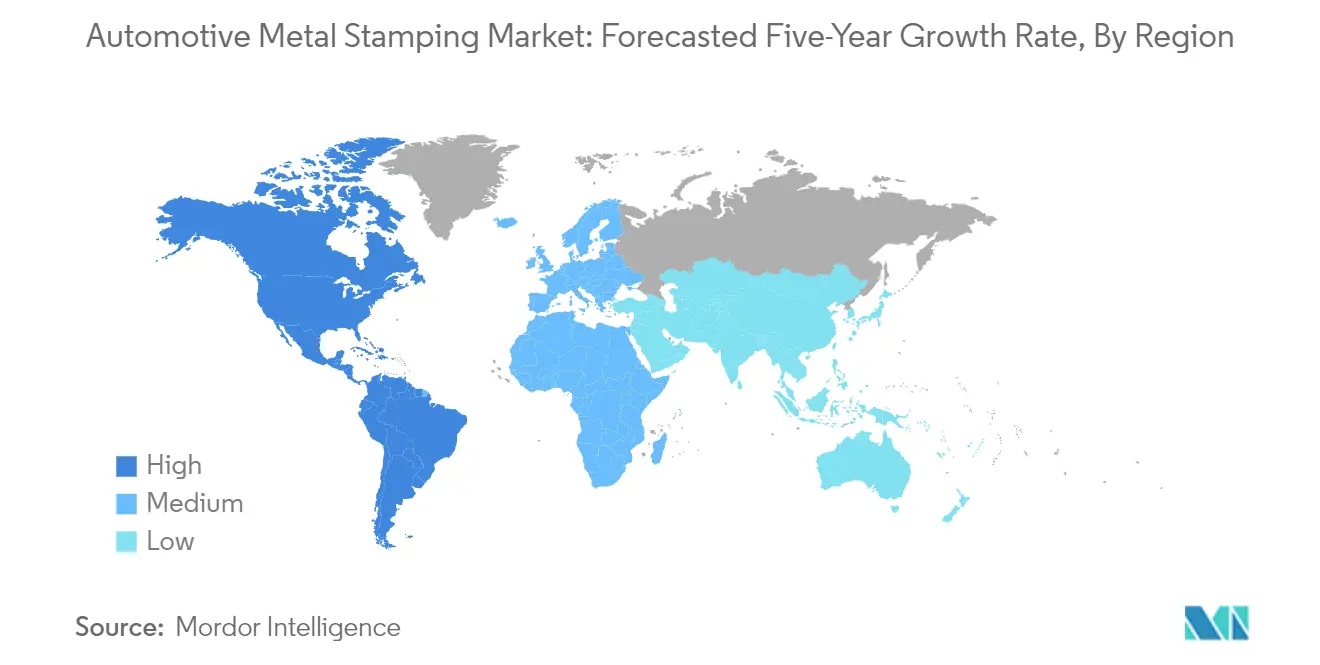

Automotive Metal Stamping Market in North America

North America represents a significant market for automotive metal stamping, driven by the presence of major automotive manufacturers and a robust supply chain network. The United States dominates the regional landscape, followed by Canada and other North American countries. The region's market is characterized by advanced manufacturing capabilities, stringent quality standards, and an increasing focus on lightweight materials for improved fuel efficiency. The presence of established automotive OEMs and their continued investment in manufacturing facilities has created a strong demand for automotive metal stamping solutions across the region.

Automotive Metal Stamping Market in the United States

The United States leads the North American market with approximately 84% market share in 2024, establishing itself as the regional powerhouse in automotive metal stamping. The country's automotive sector remains the largest manufacturing sector, with production plants of major vehicle manufacturers like Ford, Chrysler, and General Motors strategically located throughout the region. The market is supported by robust infrastructure, technological advancements in manufacturing processes, and continuous investments in research and development. The presence of numerous metal stamping companies and their strategic partnerships with automotive OEMs has created a comprehensive ecosystem that caters to both domestic and international markets.

Automotive Metal Stamping Market in Canada

Canada emerges as the fastest-growing market in North America, with a projected growth rate of approximately 6% during 2024-2029. The country's automotive metal stamping sector is characterized by over 100 stamping establishments, primarily concentrated in Ontario and strategically present in British Columbia, Alberta, and Quebec. The growth is driven by increasing technological advancement and development in the Canadian automotive industry, coupled with supportive government initiatives. The country's focus on electric vehicle production and lightweight materials has created new opportunities for metal stamping manufacturers, particularly in developing innovative solutions for next-generation vehicles.

Automotive Metal Stamping Market in Europe

Europe maintains a strong position in the global automotive metal stamping market, with Germany, the United Kingdom, France, and Russia serving as key markets. The region's automotive industry is characterized by its excellence in manufacturing, high-quality standards, and continuous innovation in metal stamping technologies. The market is driven by the increasing adoption of electric vehicles, stringent emission regulations, and the growing focus on lightweight vehicle components. The presence of major automotive manufacturers and their extensive supplier networks has created a robust ecosystem for metal stamping operations across the region.

Automotive Metal Stamping Market in Germany

Germany maintains its position as the largest market in Europe, commanding approximately 19% of the regional market share in 2024. The country's automotive industry represents one of the most innovative and competitive sectors globally, with a strong focus on research and development. Germany's leadership in car production, coupled with the presence of major automotive OEMs such as Audi, BMW, Ford-Werke GmbH, Mercedes-Benz, Opel, Porsche, and Volkswagen, has created sustained demand for high-quality automotive metal fabrication components. The country's emphasis on precision engineering and advanced manufacturing processes has established it as a benchmark for automotive metal stamping operations.

Automotive Metal Stamping Market in Germany

Germany also leads the European market in terms of growth, with a projected growth rate of approximately 5% during 2024-2029. The country's strong focus on electric vehicle production and sustainable manufacturing practices is driving innovation in metal stamping technologies. The automotive sector's commitment to lightweight construction and advanced materials processing has created new opportunities for metal stamping manufacturers. German automotive companies continue to invest in research and development, focusing on innovative stamping solutions for electric vehicles and advanced mobility concepts.

Automotive Metal Stamping Market in Asia-Pacific

The Asia-Pacific region represents the largest market for automotive metal stamping globally, with China, Japan, India, and South Korea as key contributing countries. The region's dominance is attributed to its large automotive manufacturing base, cost-effective production capabilities, and growing domestic demand for vehicles. The market is characterized by increasing investments in manufacturing facilities, the adoption of advanced stamping technologies, and a growing focus on electric vehicle production. The presence of both domestic and international automotive manufacturers has created a diverse and competitive landscape for metal stamping operations.

Automotive Metal Stamping Market in China

China maintains its position as the dominant force in the Asia-Pacific region's automotive metal stamping market. The country's automotive industry has remained the world's largest since 2009, with extensive manufacturing capabilities and a comprehensive supply chain network. The market is characterized by significant investments in automation technologies, cost-effective manufacturing operations, and a growing focus on electric vehicle production. The presence of numerous global automotive manufacturers and their joint ventures with domestic companies has created a robust ecosystem for metal stamping operations.

Automotive Metal Stamping Market in India

India emerges as the fastest-growing market in the Asia-Pacific region. The country's automotive sector is experiencing rapid growth, supported by increasing domestic demand and government initiatives to promote local manufacturing. The growing presence of global automobile original equipment manufacturers (OEMs) has significantly increased the localization of components in the country. The market is characterized by increasing collaborations and partnerships between OEMs and stamped component suppliers to enhance product development and production rates.

Automotive Metal Stamping Market in South America

The South American automotive metal stamping market is characterized by varying levels of industrial development across different countries, with Brazil and Argentina serving as key markets. Brazil emerges as both the largest and fastest-growing market in the region, supported by its robust automotive manufacturing sector and strategic partnerships with global OEMs. The region's market is influenced by economic conditions, government policies supporting local manufacturing, and increasing investments in automotive production facilities. The focus on vehicle modernization and the adoption of new technologies is driving the demand for advanced metal stamping solutions across South America.

Automotive Metal Stamping Market in the Middle East and Africa

The Middle East and Africa region presents a growing market for automotive metal stamping, with the United Arab Emirates and Saudi Arabia as key contributors. Saudi Arabia represents the largest market in the region, while the UAE shows the fastest growth potential. The market is driven by increasing investments in automotive manufacturing capabilities, growing demand for vehicles, and government initiatives to diversify economies beyond oil dependency. The region's focus on developing local manufacturing capabilities and increasing adoption of electric vehicles is creating new opportunities for metal stamping manufacturers.

Get Analysis on Important Geographic Markets

Download PDF

Automotive Metal Stamping Industry Overview

Top Companies in Automotive Metal Stamping Market

The automotive metal stamping companies market features established players like Gestamp, Magna International, Martinrea International, and Shiloh Industries, who are leading innovation and market development. Companies are increasingly focusing on developing lightweight technologies and precision stamping capabilities to meet evolving automotive industry demands. Strategic investments in expanding manufacturing facilities and upgrading press capabilities demonstrate the industry's commitment to operational excellence. Market leaders are strengthening their positions through technological advancements in areas like progressive die stamping, deep draw stamping, and hot forming processes. The competitive landscape is characterized by continuous improvement in production efficiency, quality certifications, and the development of specialized solutions for electric vehicle components. Companies are also expanding their geographical footprint and forming strategic partnerships with automotive OEMs to secure long-term growth opportunities.

Fragmented Market with Strong Regional Players

The automotive metal stamping market exhibits a fragmented structure with a mix of global conglomerates and specialized regional manufacturers. Major players control a significant portion of the market through their extensive manufacturing networks, advanced technological capabilities, and established relationships with automotive OEMs. The market features numerous small and medium-sized players who serve specific regional markets or specialized component segments. These smaller players often compete through specialized expertise, flexible manufacturing capabilities, and close customer relationships in their respective regions. The industry's structure encourages healthy competition while maintaining barriers to entry through capital requirements and technological expertise.

Merger and acquisition activities in the sector are driven by the need to expand geographical presence, enhance technological capabilities, and achieve economies of scale. Large players are actively acquiring smaller, specialized manufacturers to complement their existing capabilities and enter new market segments. The industry also witnesses strategic partnerships and joint ventures aimed at sharing technological expertise and accessing new markets. Companies are increasingly focusing on vertical integration strategies to maintain control over the supply chain and ensure consistent quality standards.

Innovation and Efficiency Drive Market Success

Success in the automotive metal stamping industry increasingly depends on technological innovation, operational efficiency, and the ability to meet evolving customer requirements. Companies must invest in advanced manufacturing technologies, automation, and quality control systems to maintain competitiveness. The ability to offer comprehensive solutions, from design and engineering to final production, is becoming crucial for market success. Players need to develop expertise in lightweight materials and precision manufacturing techniques to address the growing demand for fuel-efficient vehicles and electric vehicle components. Building strong relationships with automotive OEMs through consistent quality, reliable delivery, and competitive pricing remains essential for long-term success.

Market contenders can gain ground by focusing on specialized market segments, developing innovative manufacturing processes, and maintaining operational flexibility. The increasing concentration of automotive OEMs creates both opportunities and challenges, requiring suppliers to demonstrate exceptional value propositions and technological capabilities. While substitution risk remains low due to the essential nature of automotive stamping in automotive manufacturing, companies must stay ahead of technological advances and changing industry requirements. Regulatory pressures for lightweight vehicles and reduced emissions continue to shape product development and manufacturing strategies, creating opportunities for innovative solutions and specialized expertise.

Automotive Metal Stamping Market Leaders

-

Magna International Inc.

-

Shiloh Industries Inc.

-

Alcoa Corporation

-

Manor Tool & Manufacturing Company

-

Wisconsin Metal Parts Inc.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Automotive Metal Stamping Market News

- In January 2023, Gestamp, a Spain-based company specializing in the design, development, and manufacture of highly engineered metal components for the automotive industry, announced its fourth hot stamping line in India.

- In February 2023, Hyundai Motor Corporation announced an investment of USD 300 million to build a new metal stamping plant in Savannah, Georgia, and to become the fifth Hyundai Motor Group supplier to be located in the region.

- In October 2022, ThyssenKrupp Steel showcased the AS Pro-coated MBW steels for automotive construction in series production at the EuroBLECH. This marks the introduction of the next generation of hot stamping technology.

Automotive Metal Stamping Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

-

4.1 Market Drivers

- 4.1.1 Increasing Automobile Production is Anticipated to Boosts the Market

-

4.2 Market Restraints

- 4.2.1 Fluctuating Raw Material Prices May Hinder the Market Growth

-

4.3 Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION (Market Size in Value USD)

-

5.1 Technology

- 5.1.1 Blanking

- 5.1.2 Embossing

- 5.1.3 Coining

- 5.1.4 Flanging

- 5.1.5 Bending

- 5.1.6 Other Technologies

-

5.2 Process

- 5.2.1 Roll Forming

- 5.2.2 Hot Stamping

- 5.2.3 Sheet Metal Forming

- 5.2.4 Metal Fabrication

- 5.2.5 Other Processes

-

5.3 Vehicle Type

- 5.3.1 Passenger Cars

- 5.3.2 Commercial Vehicles

-

5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 India

- 5.4.3.2 China

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 Rest of the World

- 5.4.4.1 South America

- 5.4.4.2 Middle-East and Africa

6. COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

-

6.2 Company Profiles*

- 6.2.1 Clow Stamping Company

- 6.2.2 D&H Industries

- 6.2.3 Magna International Inc.

- 6.2.4 PDQ Tool & Stamping Co.

- 6.2.5 Alcoa Inc.

- 6.2.6 Shiloh Industries Inc.

- 6.2.7 Manor Tool & Manufacturing Company

- 6.2.8 Lindy Manufacturing

- 6.2.9 American Industrial Company

- 6.2.10 Tempco Manufacturing

- 6.2.11 Wisconsin Metal Parts Inc.

- 6.2.12 Goshen Stamping Co. Inc.

- 6.2.13 Interplex Industries Inc.

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Automotive Metal Stamping Industry Segmentation

Automotive metal stamping is the manufacturing process of converting flat metal sheets into specific shapes. This process uses a stamping press and a number of metal forming techniques like blanking, embossing, coining, flanging, bending, and others, to transform metal sheets into the desired shapes.

The Automotive Metal Stamping market is segmented by Technology, Process, Vehicle Type, and Geography. By Technology, the market is segmented into Blanking, Embossing, Coining, Flanging, Bending, and Other Technologies. By Process, the market is segmented into Roll Forming, Hot Stamping, Sheet Metal Forming, Metal Fabrication, and Other Processes. By Vehicle Type, the market is segmented into Passenger Cars and Commercial Vehicles. By Geography, the market is segmented into North America, Europe, Asia-Pacific, and Rest of the World. The report offers the market size in value (USD) and forecasts for all the above segments.

| Technology | Blanking | ||

| Embossing | |||

| Coining | |||

| Flanging | |||

| Bending | |||

| Other Technologies | |||

| Process | Roll Forming | ||

| Hot Stamping | |||

| Sheet Metal Forming | |||

| Metal Fabrication | |||

| Other Processes | |||

| Vehicle Type | Passenger Cars | ||

| Commercial Vehicles | |||

| Geography | North America | United States | |

| Canada | |||

| Rest of North America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | India | ||

| China | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Rest of the World | South America | ||

| Middle-East and Africa | |||

Need A Different Region or Segment?

Customize Now

Automotive Metal Stamping Market Research FAQs

How big is the Automotive Metal Stamping Market?

The Automotive Metal Stamping Market size is expected to reach USD 123.50 billion in 2025 and grow at a CAGR of 4.99% to reach USD 157.55 billion by 2030.

What is the current Automotive Metal Stamping Market size?

In 2025, the Automotive Metal Stamping Market size is expected to reach USD 123.50 billion.

Who are the key players in Automotive Metal Stamping Market?

Magna International Inc., Shiloh Industries Inc., Alcoa Corporation, Manor Tool & Manufacturing Company and Wisconsin Metal Parts Inc. are the major companies operating in the Automotive Metal Stamping Market.

Which is the fastest growing region in Automotive Metal Stamping Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Automotive Metal Stamping Market?

In 2025, the Asia-Pacific accounts for the largest market share in Automotive Metal Stamping Market.

What years does this Automotive Metal Stamping Market cover, and what was the market size in 2024?

In 2024, the Automotive Metal Stamping Market size was estimated at USD 117.34 billion. The report covers the Automotive Metal Stamping Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Automotive Metal Stamping Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Automotive Metal Stamping Market Research

Mordor Intelligence provides a comprehensive analysis of the automotive metal stamping market, drawing on our extensive experience in industrial research. Our latest report examines the evolving landscape of automotive stamping processes. This includes automotive sheet metal applications and automotive metal fabrication techniques. The analysis covers key aspects of automotive parts stamping and auto metal stamping operations. It offers detailed insights into automotive metal components manufacturing and supply chain dynamics. Our research methodology combines primary data from leading automotive metal stamping companies with advanced analytics to deliver actionable intelligence.

The report, available as an easy-to-download PDF, offers stakeholders detailed insights into automotive metal forming processes and emerging automotive metal stamping market trends. Our analysis covers the entire spectrum of automotive sheet metal forming technologies and their applications across global markets. The comprehensive coverage includes a detailed examination of metal stamping automotive industry developments, automotive metal forming market dynamics, and technological innovations. Stakeholders gain access to strategic insights that drive informed decision-making in the rapidly evolving automotive metal stamping industry, supported by robust data analysis and expert consultations.