| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| CAGR | 28.20 % |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players*Disclaimer: Major Players sorted in no particular order |

Automotive LiDAR Market Analysis

The Automotive LiDAR Market is expected to register a CAGR of 28.2% during the forecast period.

The automotive LiDAR industry is experiencing rapid technological evolution, driven by the increasing focus on vehicle safety and autonomous driving capabilities. According to the World Health Organization, auto accidents are responsible for 1.3 million deaths annually, highlighting the critical need for advanced safety systems in vehicles. Leading manufacturers are responding to this challenge by developing more sophisticated automotive LiDAR solutions, with companies like Hesai Group establishing strong relationships with automotive OEMs and robotics companies worldwide, covering over 90 cities in 40 countries. This widespread adoption demonstrates the industry's commitment to enhancing vehicle safety through advanced automotive sensing technologies.

The market is witnessing significant technological advancements, particularly in sensor development and integration capabilities. In 2023, several breakthrough innovations have emerged, such as Valeo's introduction of over-the-air software updates for their third-generation Scala 3 LiDAR, scheduled for production in 2024. Companies like ams-OSRAM AG are making substantial investments, with a recent commitment of EUR 300 million over the next five years for research and development in innovative applications, including LiDAR for autonomous vehicles. These developments are reshaping the industry's landscape and enabling more efficient and cost-effective LiDAR solutions.

Production capabilities and industry partnerships have shown remarkable progress, with major players achieving significant milestones in manufacturing scale. RoboSense delivered over 20,000 units of automotive LiDAR in October 2023, setting a new record for monthly LiDAR shipments in the automotive sector. The industry is also witnessing strategic collaborations, exemplified by the partnership between dSPACE and RoboSense to accelerate the development and testing of LiDAR functionality in ADAS and autonomous driving applications. These collaborations are crucial in advancing the technology's commercial viability and market adoption.

The integration of LiDAR technology in vehicles is becoming increasingly sophisticated, with manufacturers implementing multi-sensor approaches for enhanced perception capabilities. Recent developments include IM Motors' launch of their LS6 model in October 2023, featuring ultra-long-range high-precision LiDARs integrated with high-computing-power chips. Similarly, Aito's introduction of the M5 Intelligent Driving Edition in June 2023, equipped with advanced LiDAR systems and Huawei's latest intelligent cockpit technology, demonstrates the industry's move towards more comprehensive autonomous driving solutions. These implementations showcase the evolution of LiDAR from a standalone sensor to an integral part of sophisticated vehicle intelligence systems, contributing to the growing automotive sensor market.

Automotive LiDAR Market Trends

Increasing Vehicle Safety and Government Regulation to Promote LIDAR Demand

The critical need for enhanced vehicle safety systems continues to drive the adoption of LiDAR technology, particularly given the sobering statistics from the World Health Organization that indicate auto accidents are responsible for 1.3 million deaths annually worldwide. This significant safety concern is further emphasized by the National Highway Traffic Safety Administration's findings that approximately 94% of these accidents are caused by human error, with the remainder attributed to environmental and mechanical failures. In response to these challenges, automotive manufacturers are increasingly integrating ADAS LiDAR safety systems, as demonstrated by Nissan's 2023 implementation of intersection collision avoidance capabilities in their ADAS technology suite.

The regulatory landscape has evolved significantly to promote the adoption of advanced safety technologies. The National Highway Traffic Safety Administration (NHTSA) has taken a proactive stance by implementing a Standing General Order that requires manufacturers and operators of automated driving systems and SAE Level 2 advanced driver assistance systems to report crashes to the agency. This regulatory framework is complemented by the NHTSA's support of the Safe System Approach, a data-driven, holistic, and equitable method to roadway safety that fully integrates the needs of all users. Companies are responding to these requirements by developing comprehensive safety solutions that incorporate vehicle LiDAR technology, enabling features such as pedestrian and bicycle avoidance, Lane Keep Assistance (LKA), Automatic Emergency Braking (AEB), Adaptive Cruise Control (ACC), and Traffic Jam Assist (TJA).

Understand The Key Trends Shaping This Market

Download PDF

Demand for Autonomous Vehicles to Fuel LIDAR Market

The autonomous vehicle sector has demonstrated remarkable technological advancement, with autonomous vehicle LiDAR technology emerging as a crucial component for achieving higher levels of autonomy. A notable milestone in this progression was demonstrated through Vueron Technology's achievement of a 414-kilometer fully automated, LiDAR-only drive from Seoul to Busan, maintaining speeds up to 100 km/hr without any steering intervention from the safety driver. This practical demonstration of LiDAR's capabilities has been complemented by significant cost reductions in the technology, exemplified by Luminar's breakthrough in offering LiDAR-based solutions for under USD 1,000, making the technology more accessible for widespread implementation.

Recent industry developments in 2023 have further accelerated the adoption of LiDAR in autonomous vehicles. Notable examples include IM Motors' launch of their LS6 intelligent coupe SUV, equipped with ultra-long-range high-precision LiDARs and an Orin X high-computing-power chip, representing the cutting edge of intelligent battery electric SUVs. Additionally, Aito's deployment of their M5 Intelligent Driving Edition, featuring advanced LiDAR systems and the Harmony Intelligent Cockpit 3.0, demonstrates the increasing integration of ADAS LiDAR technology in commercial vehicles. These developments are supported by strategic partnerships, such as KDDI's collaboration with transport company T2 to develop autonomous trunk transportation services, highlighting the expanding applications of autonomous driving sensor technology beyond personal vehicles into commercial transportation solutions.

Segment Analysis: By Application

ADAS Segment in Automotive LiDAR Market

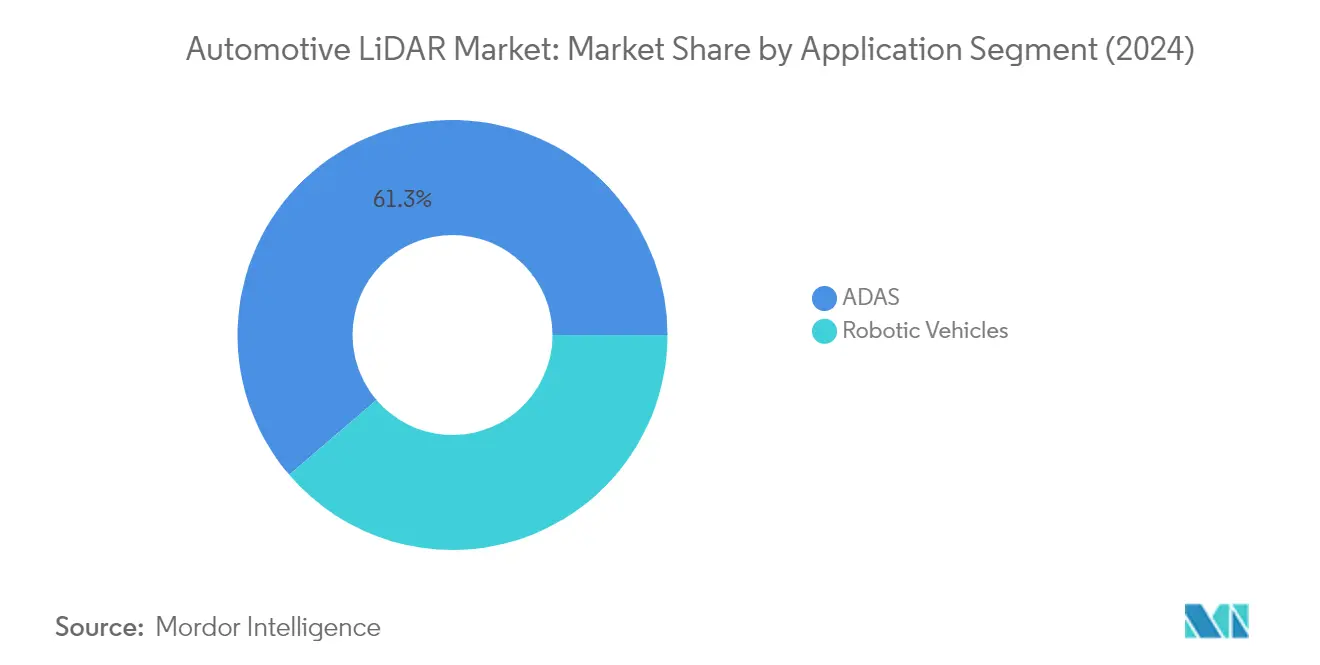

The Advanced Driver Assistance Systems (ADAS) segment dominates the automotive LiDAR market, commanding approximately 61% market share in 2024, driven by the increasing integration of autonomous features in modern vehicles. This segment's prominence is attributed to the rising consumer demand for advanced safety features and the automotive industry's push toward higher levels of autonomy. Major automakers are increasingly incorporating ADAS LiDAR functionalities like lane departure warning, adaptive cruise control, and collision avoidance systems, which rely heavily on LiDAR technology. The segment is experiencing rapid growth with a projected growth rate of nearly 39% from 2024 to 2029, fueled by stringent safety regulations and technological advancements in sensor capabilities. The growth is further supported by the increasing adoption of Level 2+ and Level 3 autonomous features in premium and mid-range vehicles, with manufacturers like Mercedes-Benz, BMW, and other leading automotive companies expanding their ADAS-equipped vehicle portfolios.

Robotic Vehicles Segment in Automotive LiDAR Market

The Robotic Vehicles segment represents a significant portion of the automotive LiDAR market, focusing on commercial applications such as autonomous shuttles, robot taxis, and cargo vehicles. This segment's growth is driven by the increasing automation in logistics, warehousing facilities, and distribution centers. The deployment of robotic vehicles in various industrial applications has created a substantial demand for advanced LiDAR sensors that can efficiently detect objects and prevent collisions. The segment's development is supported by various private companies and governments worldwide investing in robotics technology integration in the automotive sector. The application of LiDAR in robotic vehicles is particularly crucial as these vehicles operate without manual intervention, requiring highly sophisticated autonomous driving sensor capabilities for safe and efficient mobility.

Automotive LiDAR Market Geography Segment Analysis

Automotive LiDAR Market in North America

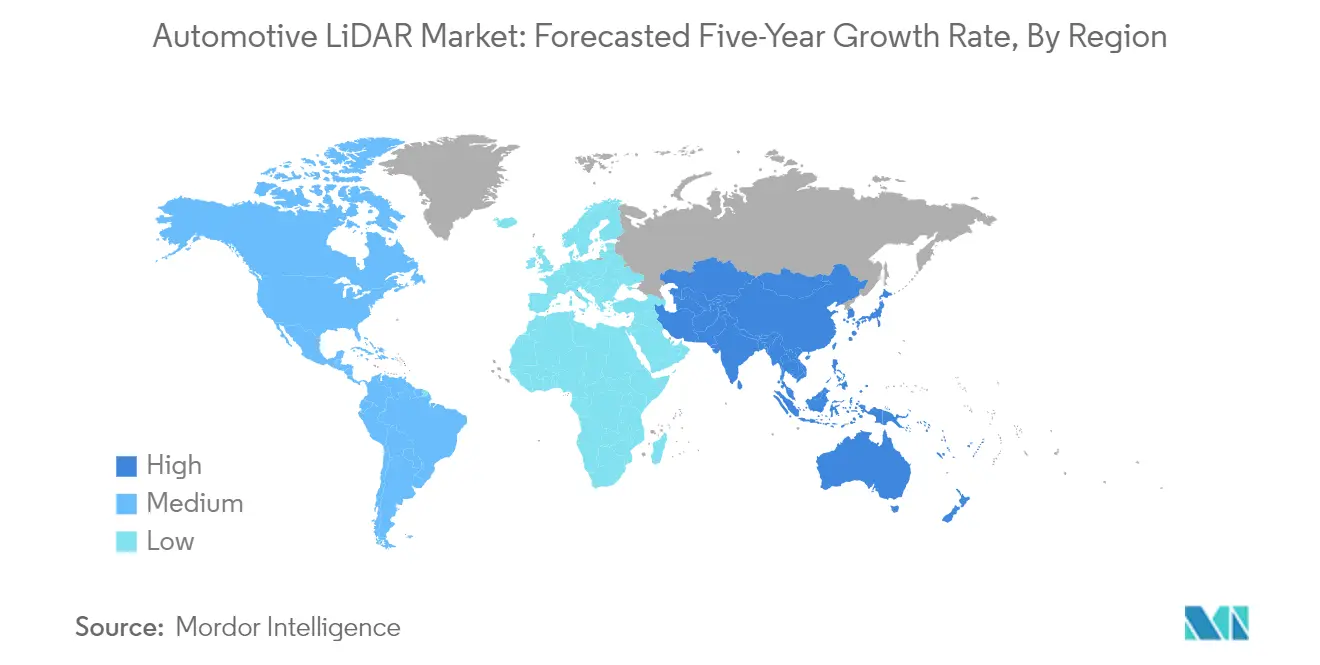

North America has established itself as a pioneering region in automotive LiDAR technology adoption, commanding approximately 38% of the global automotive LiDAR market share in 2024. The region's dominance is primarily driven by its early adoption of autonomous vehicle technology and a robust regulatory framework. The United States, Canada, and Mexico form the core markets, with the United States leading in technological innovation and implementation. The presence of major automotive manufacturers and technology companies has created a robust ecosystem for automotive LiDAR development and integration. The region's advanced infrastructure and consumer readiness for autonomous vehicles have accelerated market growth. Additionally, strict regulatory oversight by bodies like the National Highway Traffic Safety Administration (NHTSA) has created a structured environment for autonomous vehicle testing and deployment. The region's focus on vehicle safety and the increasing integration of advanced driver assistance systems (ADAS) in commercial vehicles has further strengthened market growth. Moreover, the strong presence of research and development facilities and continuous technological innovations has positioned North America as a global leader in automotive LiDAR technology.

Automotive LiDAR Market in Europe

The European automotive LiDAR market has demonstrated remarkable growth, with an impressive growth rate of approximately 71% during the period 2019-2024. The region's market is characterized by strong technological infrastructure and innovative automotive manufacturing capabilities, particularly in countries like Germany, France, and the United Kingdom. The European market's growth is supported by stringent vehicle safety regulations and increasing consumer demand for advanced safety features. The presence of premium automotive manufacturers has driven the adoption of car LiDAR technology in high-end vehicles. The region's commitment to reducing road accidents through advanced safety systems has created a favorable environment for vehicle LiDAR technology adoption. Furthermore, the expanding e-commerce sector and subsequent need for autonomous delivery vehicles have created new opportunities for LiDAR implementation. The European Union's comprehensive regulatory framework for autonomous vehicles has provided clear guidelines for manufacturers and technology providers. The region's focus on sustainable and smart mobility solutions has also contributed to the increased adoption of LiDAR-equipped vehicles.

Automotive LiDAR Market in Asia-Pacific

The Asia-Pacific region represents the most dynamic market for automotive LiDAR technology, with a projected growth rate of approximately 35% during the period 2024-2029. This region, encompassing major automotive markets like China, Japan, South Korea, and India, has emerged as a crucial hub for automotive sensing technology development and implementation. The market is driven by rapid urbanization, increasing vehicle safety awareness, and growing adoption of autonomous vehicle technology. Chinese automakers, in particular, have been aggressive in implementing car LiDAR technology in their vehicles, setting new benchmarks for the industry. The region's robust manufacturing capabilities and cost-competitive environment have attracted significant investments from global LiDAR manufacturers. The presence of major automotive manufacturing facilities and the growing middle-class population has created a strong demand for vehicles equipped with advanced safety features. Furthermore, government initiatives promoting autonomous vehicle development and smart city projects have created additional opportunities for LiDAR technology deployment. The region's focus on technological innovation and the presence of multiple technology startups have fostered a competitive environment for LiDAR development.

Automotive LiDAR Market in Rest of the World

The Rest of the World region, comprising markets in the Middle East, Africa, and South America, represents an emerging opportunity for automotive LiDAR technology. Countries like the United Arab Emirates and Saudi Arabia are leading the adoption of autonomous vehicle technology in the Middle East, driven by their smart city initiatives and technological advancement goals. Brazil stands out in South America as a key market, with its robust automotive sector and increasing focus on vehicle safety technologies. The region's growing emphasis on road safety and the modernization of transportation infrastructure has created new opportunities for vehicle LiDAR technology adoption. Government initiatives to reduce road accidents and improve transportation efficiency have accelerated the implementation of advanced driver assistance systems. The presence of global automotive manufacturers and their increasing focus on these markets has facilitated the introduction of LiDAR-equipped vehicles. Furthermore, the region's expanding logistics and transportation sector has created additional demand for autonomous vehicles equipped with LiDAR technology. The increasing investment in smart transportation infrastructure and the growing awareness of vehicle safety features continue to drive market growth in these regions.

Get Analysis on Important Geographic Markets

Download PDF

Automotive LiDAR Industry Overview

Top Companies in Automotive LiDAR Market

The automotive LiDAR market is characterized by intense innovation and strategic developments from key players, including Hesai Group, Innovusion, Valeo, Waymo LLC, and RoboSense. These automotive LiDAR companies focus on developing advanced LiDAR technologies with improved performance capabilities while simultaneously reducing costs through manufacturing optimization. Strategic partnerships with automotive OEMs and technology companies have become increasingly common as firms seek to strengthen their market positions. Product development efforts are primarily centered around creating more compact, energy-efficient, and reliable LiDAR systems suitable for mass-market adoption. Companies are also expanding their geographical presence through distribution partnerships and establishing regional manufacturing facilities to better serve local markets. The industry has witnessed significant investments in research and development, particularly in areas such as solid-state LiDAR technology and advanced perception software integration.

Dynamic Market with Strong Growth Potential

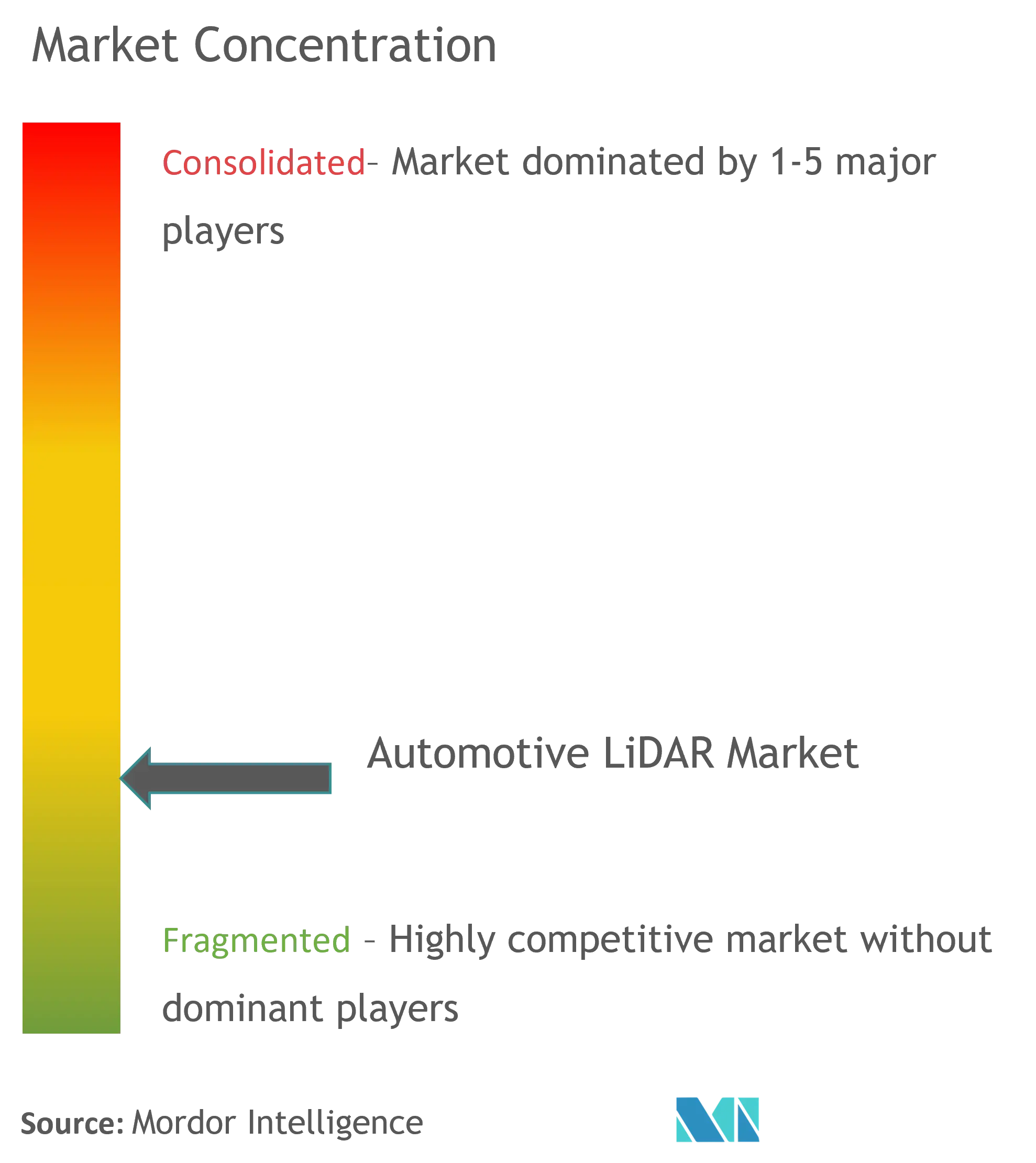

The automotive LiDAR market structure exhibits a mix of established technology conglomerates and specialized LiDAR manufacturers competing for market share. Global players like Bosch and Valeo leverage their extensive automotive industry experience and established relationships with OEMs, while specialized firms like Hesai Group and Innovusion focus exclusively on LiDAR technology development. The market demonstrates moderate consolidation, with larger players actively pursuing acquisitions of smaller, innovative companies to enhance their technological capabilities and expand their product portfolios. Regional players, particularly in Asia-Pacific, are emerging as significant competitors by capitalizing on local manufacturing advantages and government support for autonomous vehicle development.

The industry is witnessing increased collaboration between traditional automotive suppliers and technology companies, creating a complex ecosystem of partnerships and joint ventures. Market dynamics are influenced by the growing demand for advanced driver assistance systems (ADAS) and autonomous driving capabilities, driving both competition and cooperation among players. Companies are increasingly focusing on vertical integration strategies to control key components of the value chain and ensure product quality while reducing costs. The competitive landscape is further shaped by the entry of new players bringing innovative approaches to LiDAR technology, although barriers to entry remain high due to significant capital requirements and technical expertise needed.

Innovation and Adaptability Drive Market Success

Success in the automotive LiDAR market increasingly depends on companies' ability to balance technological innovation with cost-effectiveness while maintaining strong relationships with automotive manufacturers. Incumbent players must focus on continuous product improvement, manufacturing efficiency, and strategic partnerships to maintain their market positions. Companies need to develop comprehensive solutions that integrate hardware and software capabilities while ensuring compatibility with various vehicle platforms. The ability to scale production while maintaining quality standards and meeting stringent automotive requirements is becoming increasingly critical for market success. Establishing strong intellectual property portfolios and developing differentiated technologies are essential strategies for both established players and new entrants.

Market participants must carefully navigate the evolving regulatory landscape surrounding autonomous vehicles and safety standards while addressing concerns about cybersecurity and reliability. Companies need to demonstrate clear value propositions to automotive manufacturers while managing the risk of alternative technologies potentially replacing LiDAR in certain applications. Success factors include the ability to adapt to changing customer requirements, maintain competitive pricing strategies, and develop robust supply chain relationships. The concentration of buying power among major automotive manufacturers necessitates strong customer relationship management and the ability to provide customized solutions. Future market leaders will likely be those who can successfully combine technological excellence with operational efficiency while maintaining strong financial positions to support continued innovation and market expansion.

Automotive LiDAR Market Leaders

-

Ouster Inc.

-

Robert Bosch GmbH

-

Waymo LLC

-

Robosense

-

Valeo

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Automotive LiDAR Market News

- October 2020 - Waymo announced that it is launching fully driverless vehicles to the public, announced by the company. It is starting a driverless ride-hailing service for riders in the Phoenix metro area. It will enable passengers to download its app and hail a ride without a driver.

- March 2020 - Velodyne Lidar Inc announced a multi-year sales agreement with NAVYA, a leading company in autonomous driving systems. NAVYA plans to pursue the worldwide expansion of its shuttle with Velodyne's state-of-the-art sensors for precise real-time localization and object detection.

Automotive LiDAR Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. MARKET INSIGHTS

- 3.1 Market Overview

-

3.2 Industry Attractiveness - Porter's Five Forces Analysis

- 3.2.1 Threat of New Entrants

- 3.2.2 Bargaining Power of Buyers

- 3.2.3 Bargaining Power of Suppliers

- 3.2.4 Threat of Substitutes

- 3.2.5 Intensity of Competitive Rivalry

-

3.3 Market Drivers

- 3.3.1 Technological Superiority of LiDAR

- 3.3.2 Increasing Vehicle Safety Regulations and Growing Adoption of Adas Technology By OEM's

-

3.4 Market Challenges

- 3.4.1 High Cost of LiDAR Raises Overall Vehicle Cost

- 3.5 LiDAR Ecosystem (Photodetectors, IC, LiDAR Systems, Laser sources and Optical Components)

- 3.6 Integration of LiDAR in ADAS Vehicles (Advantages and Pain Points at Different Areas in the Vehicle)

- 3.7 Automotive LiDAR Technology Roadmap (2018 vs 2020 vs 2025)

- 3.8 Change in the Average Cost of LiDAR Technology in Automotive (Laser Ranging Sensor, High Resolution Spinning LiDAR mapping, Spinning & Solid State LiDAR for Positioning and Detection, and LiDAR for Mapping)

4. MARKET SEGMENTATION

-

4.1 By Application

- 4.1.1 Robotic Vehicles

- 4.1.2 ADAS

- 4.1.2.1 ADAS Level 2+ and 2++

- 4.1.2.2 ADAS Level 3 and Level 4

- 4.1.2.3 ADAS Level 5

-

4.2 By Geography

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia-Pacific

- 4.2.4 Rest of World

5. COMPETITIVE INTELLIGENCE

- 5.1 Vendor Ranking Analysis

-

5.2 Company Profile

- 5.2.1 Ouster Inc.

- 5.2.2 Robert Bosch GmbH

- 5.2.3 Valeo

- 5.2.4 Insight LiDAR

- 5.2.5 Velodyne LiDAR Inc.

- 5.2.6 Leddar Tech

- 5.2.7 Waymo LLC

- 5.2.8 RoboSense

6. INVESTMENT ANALYSIS

7. FUTURE OPPORTUNITIES OF LIDAR MARKET

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Automotive LiDAR Industry Segmentation

LIDAR - sometimes called time of flight (ToF), laser scanners or laser radar - is a sensing method that detects objects and maps their distances. The technology works by illuminating a target with an optical pulse and measuring the characteristics of the reflected return signal. The width of the optical pulse can range from a few nanoseconds to several microseconds. The study analyses the application of LiDAR in automotive industry. It provides a in-depth analysis of the application along with the extent of development and adoption in various geographies.

| By Application | Robotic Vehicles | ||

| ADAS | ADAS Level 2+ and 2++ | ||

| ADAS Level 3 and Level 4 | |||

| ADAS Level 5 | |||

| By Geography | North America | ||

| Europe | |||

| Asia-Pacific | |||

| Rest of World | |||

Need A Different Region or Segment?

Customize Now

Automotive LiDAR Market Research FAQs

What is the current Automotive LiDAR Market size?

The Automotive LiDAR Market is projected to register a CAGR of 28.2% during the forecast period (2025-2030)

Who are the key players in Automotive LiDAR Market?

Ouster Inc., Robert Bosch GmbH, Waymo LLC, Robosense and Valeo are the major companies operating in the Automotive LiDAR Market.

Which is the fastest growing region in Automotive LiDAR Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Automotive LiDAR Market?

In 2025, the North America accounts for the largest market share in Automotive LiDAR Market.

What years does this Automotive LiDAR Market cover?

The report covers the Automotive LiDAR Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Automotive LiDAR Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Automotive LiDAR Market Research

Mordor Intelligence offers a comprehensive analysis of the automotive LiDAR industry. We leverage our extensive expertise in automotive sensing and automotive scanning technologies. Our research thoroughly examines vehicle LiDAR applications, including systems for autonomous vehicles and ADAS LiDAR implementations. The report provides detailed insights into automotive imaging solutions, car LiDAR technologies, and emerging flash LiDAR developments. Available as an easy-to-download report PDF, our analysis covers crucial developments in automotive optical sensor technology and automotive 3D sensing applications.

This detailed market analysis benefits stakeholders across the automotive LiDAR market ecosystem, from manufacturers to end-users. The report examines key automotive LiDAR companies and their innovative contributions to autonomous driving sensor development. Our comprehensive coverage of the automotive sensor market includes a detailed analysis of market dynamics, technological advancements, and growth opportunities. The report provides actionable insights into the size of the automotive LiDAR market, enabling stakeholders to make informed decisions based on robust data and expert analysis of current and future market trends.