Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 22.35 Billion |

| Market Size (2030) | USD 29.21 Billion |

| Growth Rate (2025 - 2030) | 5.50% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Automotive Glass Market Analysis by Mordor Intelligence

The automotive glass market size stands at USD 22.35 billion in 2025 and is projected to reach USD 29.21 billion by 2030, reflecting a steady 5.5% CAGR during the forecast period (2025-2030). Rising vehicle production, stricter safety mandates, and the shift toward electric mobility are sustaining momentum even as raw-material prices and logistics costs fluctuate. Growing demand for panoramic roofs, lightweight laminated windshields, and electrochromic glazing is encouraging manufacturers to scale specialized lines and deepen partnerships with OEMs. The emphasis on larger glass surfaces in SUVs, coupled with regulatory pressure to cut CO₂ emissions, is accelerating the adoption of coated and multi-functional products. Together, these forces position the automotive glass market for resilient, technology-led growth through the decade.

Key Report Takeways

- By glass type, regular glass led with 82.70% of the automotive glass market share in 2024, while smart glass is forecast to expand at a 12.8% CAGR to 2030.

- By application, windshields captured 44.60% of the automotive glass market size in 2024; sunroofs are advancing at a 10.2% CAGR through 2030.

- By vehicle type, passenger cars dominated with 72.30% of the automotive glass market revenue share in 2024; light commercial vehicles are expected to post the fastest 6.9% CAGR between 2025-2030.

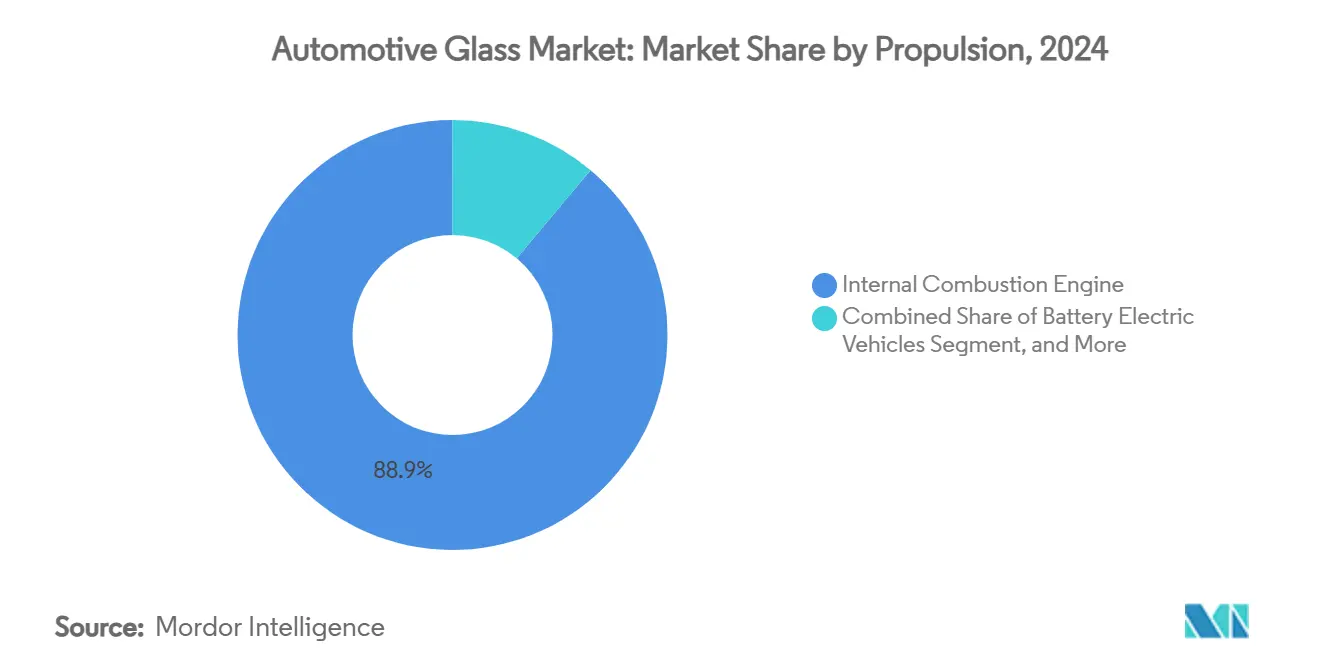

- By propulsion, Internal combustion engine vehicles retained 88.90% of the automotive glass market share in 2024, but BEVs are projected to climb at a 17.4% CAGR to 2030.

- By sales channel, OEMs held 78.50% of the automotive glass market revenue in 2024, while the aftermarket is growing at a 5.6% CAGR.

- By region, Asia-Pacific accounted for 49.20% of the automotive glass market revenue in 2024; the Middle East and Africa is set to rise at a 7.1% CAGR from 2025-2030.

Global Automotive Glass Market Trends and Insights

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Deadline |

|---|---|---|---|

| Shift Toward Panoramic Glazing In EV Platforms | +1.7% | North America, Europe, China | Medium term (2-4 years) |

| OEM Demand For Lightweight Laminated Glass To Meet CO₂ Targets | +1.5% | Global, emphasis on Europe | Long term (≥ 4 years) |

| Rapid Sunroof Penetration In SUVs | +1.2% | North America, Europe, China | Short term (≤ 2 years) |

| Regulation-Led Mandatory Safety Glazing For Side Windows | +0.8% | Europe, North America, Japan | Medium term (2-4 years) |

| Growing Retrofit Of HUD-Compatible Windshields By Premium OEMs | +0.5% | Europe, North America, Japan | Medium term (2-4 years) |

| Integration Of Embedded Sensors For ADAS Functionality | +0.4% | Global, focus on North America & Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shift Toward Panoramic Glazing In EV Platforms

Electric-vehicle makers are installing larger roof panes to enhance cabin ambience and brand identity. Tesla’s Cybertruck and Mercedes-Benz’s Vision V concept integrate electrochromic roofs that modulate tint levels, cutting cabin temperatures by up to 18°F and lowering HVAC loads. Glass area per vehicle is forecast to surge, prompting suppliers to invest in wide-format bending, low-E coatings, and infrared-absorbing interlayers. This premium specification is expected to permeate mid-priced EVs as production costs fall, supporting sustained growth in the automotive glass market.

OEM Demand For Lightweight Laminated Glass To Meet CO₂ Targets

European regulations set a 100 g/km fleet-average CO₂ goal for 2030, pushing automakers to shave every kilogram. EPA studies of the 2017 Ford GT show laminated glazing contributed materially to a 30% mass drop. Thin-gauge laminates using ionoplast interlayers now trim weight by up to 30% without compromising impact performance. AGC and Saint-Gobain are commercializing 1.6-mm windshield constructions that pair weight savings with acoustic damping, reinforcing long-term prospects for the automotive glass market.

Rapid Sunroof Penetration In SUVs

SUV share in global passenger-car output keeps rising, and nearly every new model offers a panoramic roof option. The European Vehicle Glazing Innovation Summit 2025 reported that roof modules spanning 70-90% of the vehicle’s length have become mainstream in mid-size crossovers [1]“Vehicle Glazing Innovation Summit 2025 Agenda,” ECV International, ecvinternational.com. Suppliers are optimizing roller-blind geometry, UV filtering, and drainage systems to ensure durability. The trend generates incremental square-meter demand, lifting the automotive glass market size over the forecast horizon.

Regulation-Led Mandatory Safety Glazing For Side Windows

The U.S. FMVSS 205 and UN R127 rules encourage a switch from tempered to laminated sidelites to reduce ejection risk in rollovers [2]National Highway Traffic Safety Administration, “FMVSS No. 205—Glazing Materials,” United Nations Economic Commission for Europe, “UN Regulation No. 127,”. Europe and Japan are tightening similar norms. Laminated side glazing adds noise-reduction benefits that resonate with EV buyers who notice tire roar more acutely. Regulatory certainty gives glassmakers confidence to scale new lamination lines, solidifying volume growth in the automotive glass market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Deadline |

|---|---|---|---|

| Supply-Chain Crunch Of Specialty Interlayers (PVB, Ionoplast) | −1.0% | Global, severe in Europe | Short term (≤ 2 years) |

| Margin Erosion From Chinese Float-Glass Overcapacity Flooding EU Market | -0.7% | Europe, spillover to North America | Medium term (2-4 years) |

| High Warranty Costs Linked To Acoustic Laminated Backlights In SUVs | -0.4% | North America, Europe | Short term (≤ 2 years) |

| Slow Replacement Cycles In Mature Aftermarket Channels | -0.3% | North America, Europe, Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Supply-Chain Crunch Of Specialty Interlayers (PVB, Ionoplast)

Kuraray’s PVB capacity expansions have not kept pace with rising demand for acoustic and HUD-grade films, extending lead times and forcing allocation programs. European laminators report spot shortages, compelling them to prioritize OEM production over aftermarket orders. Experimental bio-based interlayers deliver promising mechanical gains of 53.1% but remain years from scale. Short-term supply stress may temper automotive glass market growth until new plants start up.

Margin Erosion From Chinese Float-Glass Overcapacity Flooding EU Market

State-supported producers in China continue exporting surplus float glass at low prices, undercutting European mills by up to 20% [3]“Industrial Overcapacity in China Report,” MERICS, merics.org. Oceania Glass has sought anti-dumping actions, signaling broader trade tensions. European manufacturers are redirecting capital toward coated and smart glazing niches where technological barriers protect margins. However, headline pricing pressure still subtracts 0.7 percentage points from forecast automotive glass market CAGR.

Segment Analysis

By Glass Type: Smart Glass Disrupts Traditional Dominance

Regular glass commanded 82.70% of the automotive glass market share in 2024, thanks to cost efficiency and entrenched production assets. Laminated variants are gaining against tempered formats because they keep shards intact on impact, satisfying global safety norms. The shift tightens the supply of specialty interlayers, yet it positions laminators for higher value capture as OEMs demand thinner, lighter constructions. Smart glass, though only a minority today, is projected to post a 12.8% CAGR, carving out niches in luxury vehicles and high-end EVs.

Electrochromic roofs dominate early adoption; suspended particle devices (SPD) deliver faster switching and durability, as shown in Mercedes-Benz’s Vision V prototype. Polymer-dispersed liquid crystal (PDLC) windows target privacy partitions, while thermochromic films remain pre-commercial. As economies of scale improve, smart glass will expand beyond flagships, bolstering the automotive glass market.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Application: Sunroofs Accelerate Beyond Core Segments

Windshields held 44.60% of the automotive glass market size in 2024, underpinned by mandatory fitment and rising ADAS sensor content. Complexity drives up unit value, reinforcing supplier-OEM co-development cycles. Sunroofs, however, are the fastest-growing application at 10.2% CAGR as SUVs standardize large openings for panoramic vistas.

Backlites see modest traction from acoustic laminates, though warranty issues temper speed. Sidelites transition to laminated construction to meet ejection-prevention laws, especially in Europe and Japan. Rear-view mirrors and quarter windows integrate electrochromic anti-glare coatings, adding feature content without large area demand. Collectively, the application mix underpins steady expansion in the automotive glass market.

By Vehicle Type: SUVs Drive Premium Glass Adoption

Passenger cars represented 72.30% of the automotive glass market revenue in 2024, with crossover-style SUVs intensifying their presence. Larger roof apertures and acoustic glazing grant glassmakers higher dollar content per unit. Hatchbacks and sedans remain high-volume but low-innovation segments, while luxury coupes showcase cutting-edge smart glass in limited runs.

Light commercial vehicles, projected to grow 6.9% CAGR, adopt passenger-car comfort features for delivery drivers, including acoustic windshields and solar-absorbing sidelites. Heavy truck demand stays steady, emphasizing durability and serviceable designs. This vehicle mix diversity supports healthy breadth in the automotive glass market.

By Propulsion: Electric Vehicles Redefine Glass Requirements

ICE models still accounted for 88.90% of the automotive glass market in 2024, yet their incremental growth lags electrified alternatives. BEVs will expand 17.4% annually, spurring needs for lightweight laminated glass and low-E coatings that curb HVAC draw and extend range. HUD-ready windshields also assist battery-efficiency-driven cockpit redesigns.

Hybrids balance both worlds, demanding moderate heat-management performance. FCEVs remain experimental but inform long-range glass R&D roadmaps. Electrification thus injects fresh momentum into the automotive glass market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Sales Channel: OEMs Lead While Aftermarket Evolves

OEM contracts delivered 78.50% of the automotive glass market revenue in 2024, as model launches multiplied and glazing complexity rose. Long-term agreements favor vertically integrated producers that can co-engineer laminated, coated, and sensor-embedded products. The aftermarket, pacing at 5.6% CAGR, contends with ADAS recalibration hurdles; still, an aging fleet and aggressive roll-ups by firms like Auto Glass Brands point to resilient demand.

Digital claims management and mobile repair services are differentiators. Collaboration between OEMs and independent fitters on calibration standards may unlock further growth, keeping the automotive glass market dynamic across channels.

Geography Analysis

Asia-Pacific dominated the automotive glass market, with 49.20% of the revenue in 2024, anchored by China’s vast output and rapid domestic uptake. Government incentives have kept plants near capacity, while India’s production climb adds a fresh demand axis. Conferences in Shanghai spotlight intelligent glazing, LiDAR transparency, and AR-HUD integration, showcasing continual innovation. Japan and South Korea supply advanced laminated and coated products for premium OEMs, preserving high-margin niches as part of the broader automotive glass market.

Producers combat margin squeeze from Chinese imports by pivoting into smart glass and sustainability programs. AGC and Saint-Gobain’s joint Volta furnace evidences a strategic move to slash CO₂ intensity. Meanwhile, North America remains influential due to the demand for SUVs. The United States features vibrant aftermarket activity; brands such as Auto Glass Now scale national footprints to capture replacement revenue.

The Middle East and Africa are expected to be the fastest climbers at 7.1% CAGR through 2030. Saudi Arabia’s silica-rich deposits attract float-glass investments intended to localize supply. Subsidies aligned with broader industrial-diversification agendas incentivize auto-component production, broadening the region’s stake in the automotive glass market. South America’s outlook is tied chiefly to Brazilian assembly volumes, while Africa’s growth centers on South Africa’s relatively mature sector. Proximity production strategies help global suppliers balance freight costs and just-in-time expectations across these varied geographies.

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

The Automotive Glass Market is dominated by several key players such as AGC Inc., Saint-Gobain, Nippon Sheet Glass, Fuyao Glass, and Xinyi Glass. Each operates multi-regional float, lamination, and coating facilities, allowing synchronized launches with major OEM programs. Saint-Gobain’s 2024 record operating margin showed the payoff from a focus on specialty products and decarbonization.

M&A activity is reshaping regional positions. PGW Auto Glass’s acquisition of PH Vitres d’Autos widened its distribution scale in North America. At the same time, Chinese low-cost exports intensify competition in commodity float segments and spur defensive innovation among Western firms. Partnerships with niche smart-glass developers such as Research Frontiers and Gauzy illustrate how incumbents secure IP access for electrochromic and SPD technologies, enlarging the automotive glass market’s frontier.

Aftermarket consolidation is quickening. Auto Glass Brands plans more than 40 locations by 2026, chasing scale in calibration-heavy replacements. Digital platforms streamline claims, and mobile units reduce downtime for fleet customers. Simultaneously, R&D into bio-based interlayers targets performance boosts and lower environmental impact. Combined, these dynamics keep the competitive landscape fluid and innovation-centric.

Automotive Glass Industry Leaders

-

AGC Inc. (Asahi Glass)

-

Saint-Gobain S.A.

-

Nippon Sheet Glass Co. Ltd.

-

Xinyi Glass Holdings Ltd.

-

Fuyao Glass Industry Group Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- May 2025: Saint-Gobain launched an innovative triple-layer acoustic windshield that reduces cabin noise by an impressive 40% compared to standard laminates, significantly enhancing driving comfort. This advanced technology has received strong support from several European original equipment manufacturers (OEMs), who plan to incorporate it into their upcoming vehicle models.

- April 2025: Gauzy introduced its advanced SPD-SmartGlass technology in the striking Mercedes-Benz Vision V. This development highlights a key shift toward incorporating advanced materials in the luxury automotive market. The presentation not only demonstrates Gauzy's innovative capabilities but also reflects a growing trend among premium automakers to adopt smart glass solutions, enhancing both aesthetics and functionality in modern vehicles.

- March 2025: Auto Glass Brands LLC unveiled ambitious plans to expand its footprint across the United States, aiming to establish more than 40 retail outlets by the year 2026. This strategic move not only demonstrates the company's commitment to growth but also solidifies its role as a key player in the ongoing consolidation within the aftermarket industry. As it broadens its presence, Auto Glass Brands seeks to enhance accessibility and service quality for customers nationwide.

Global Automotive Glass Market Report Scope

In order to safeguard the driver and to provide smooth driving, different types of glasses are being used in automobiles. The automotive glass market report covers the latest trends and COVID-19 impact followed by technological developments in the market.

The scope of the report covers the segmentation based on type, application type, vehicle type, and geography. By type, the market is segmented as regular glass and smart glass. By application type, the market is segmented as windshield, rear view mirrors, sunroof, and other application types. By vehicle type, the market is segmented into passenger vehicles and commercial vehicles. By geography, the market is segmented into North America, Europe, Asia-Pacific, and the Rest of the world. For each segment market sizing and forecast have been done on basis of value (USD billion).

By Glass Type

| Regular Glass | Laminated Glass |

| Tempered Glass | |

| Smart Glass | Electrochromic |

| Suspended Particle Device (SPD) | |

| Polymer Dispersed Liquid Crystal (PDLC) | |

| Thermochromic |

By Application

| Windshield |

| Backlite (Rear Window) |

| Sidelite (Side Windows) |

| Sunroof |

| Rear-view & Side-view Mirrors |

| Other Glazing (Quarter & Vent) |

By Vehicle Type

| Passenger Cars | Hatchback |

| Sedan | |

| SUV & Crossover | |

| Luxury & Sports | |

| Light Commercial Vehicles | |

| Medium and Heavy Commercial Vehicles |

By Propulsion

| Internal Combustion Engine (ICE) |

| Battery Electric Vehicle (BEV) |

| Hybrid Electric Vehicle (HEV/PHEV) |

| Fuel Cell Electric Vehicles (FCEV) |

By Sales Channel

| OEM |

| Aftermarket |

By Geography

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle East and Africa |

| By Glass Type | Regular Glass | Laminated Glass |

| Tempered Glass | ||

| Smart Glass | Electrochromic | |

| Suspended Particle Device (SPD) | ||

| Polymer Dispersed Liquid Crystal (PDLC) | ||

| Thermochromic | ||

| By Application | Windshield | |

| Backlite (Rear Window) | ||

| Sidelite (Side Windows) | ||

| Sunroof | ||

| Rear-view & Side-view Mirrors | ||

| Other Glazing (Quarter & Vent) | ||

| By Vehicle Type | Passenger Cars | Hatchback |

| Sedan | ||

| SUV & Crossover | ||

| Luxury & Sports | ||

| Light Commercial Vehicles | ||

| Medium and Heavy Commercial Vehicles | ||

| By Propulsion | Internal Combustion Engine (ICE) | |

| Battery Electric Vehicle (BEV) | ||

| Hybrid Electric Vehicle (HEV/PHEV) | ||

| Fuel Cell Electric Vehicles (FCEV) | ||

| By Sales Channel | OEM | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How big is the automotive glass market today?

The automotive glass market size is USD 22.35 billion in 2025 and is forecast to reach USD 29.21 billion by 2030.

Which glass type is growing the fastest?

Smart glass is projected to expand at a 12.8% CAGR between 2025-2030, far outpacing regular glass.

What segment holds the largest automotive glass market share?

Windshields lead with 44.60% share of market revenue in 2024 thanks to mandated fitment and rising ADAS integration.

Why are EVs influencing glass design?

BEVs prioritize lightweight, thermally efficient glazing to maximize driving range, pushing demand for thin laminates and low-E coatings.

Page last updated on: