Automotive Cylinder Liner Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 7.25 Billion |

| Market Size (2030) | USD 9.31 Billion |

| Growth Rate (2025 - 2030) | 5.11% CAGR |

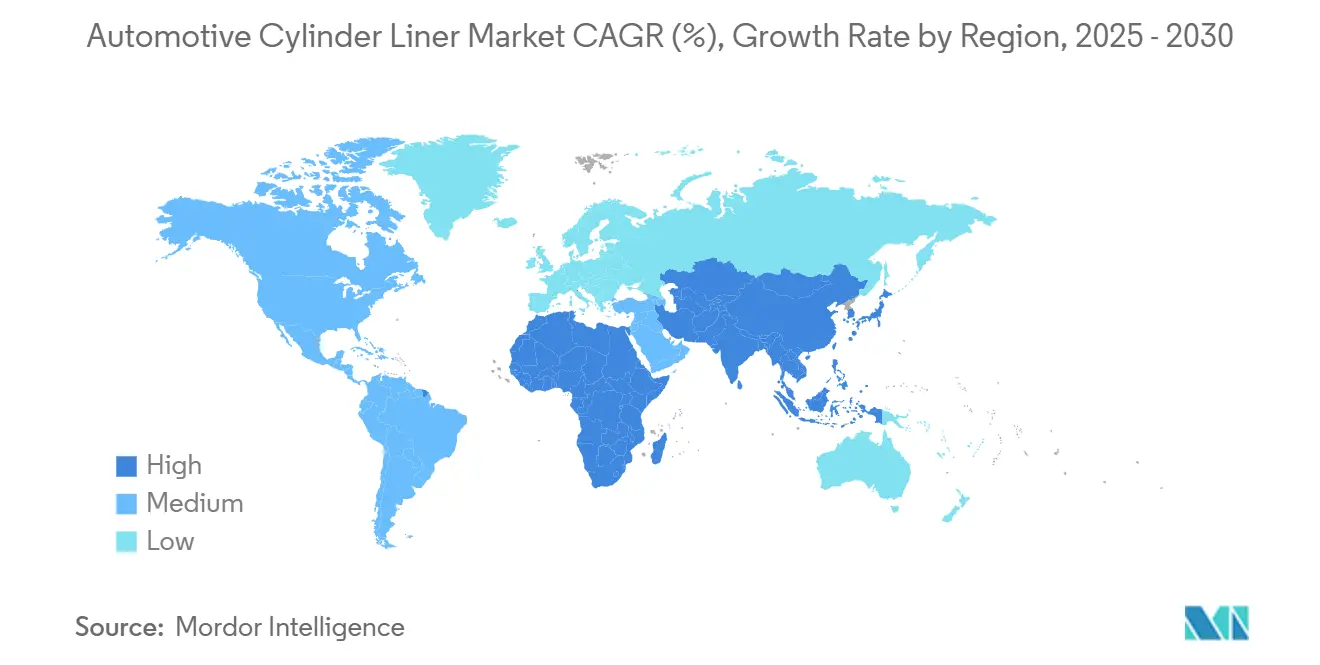

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Automotive Cylinder Liner Market Analysis by Mordor Intelligence

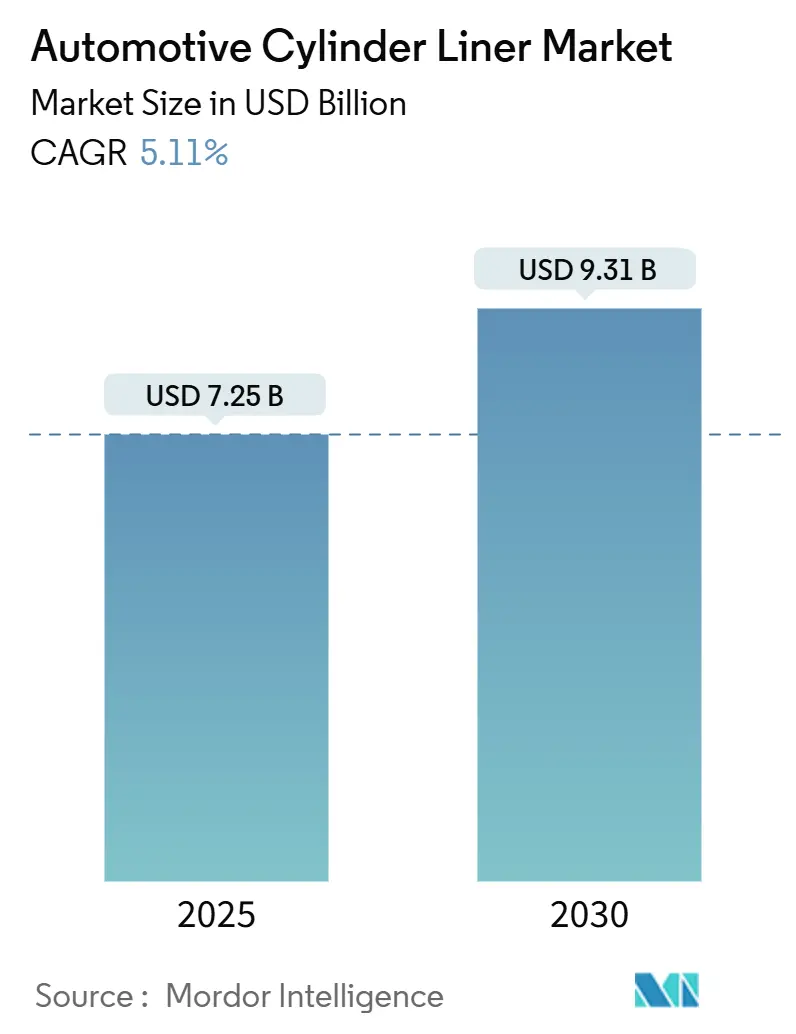

The automotive cylinder liner market size is valued at USD 7.25 billion in 2025 and is projected to reach USD 9.31 billion by 2030, growing at a 5.11% CAGR. Current growth is driven by heavy-duty commercial vehicle demand, tighter global emission regulations, and the ongoing preference for cast iron liners, which are expected to maintain a significant share of the automotive cylinder liner market in 2024. Composite liners, led by aluminum-silicon alloys, are the fastest-growing segment, reflecting the industry’s move toward lighter engines with improved heat transfer.

Key Report Takeaways

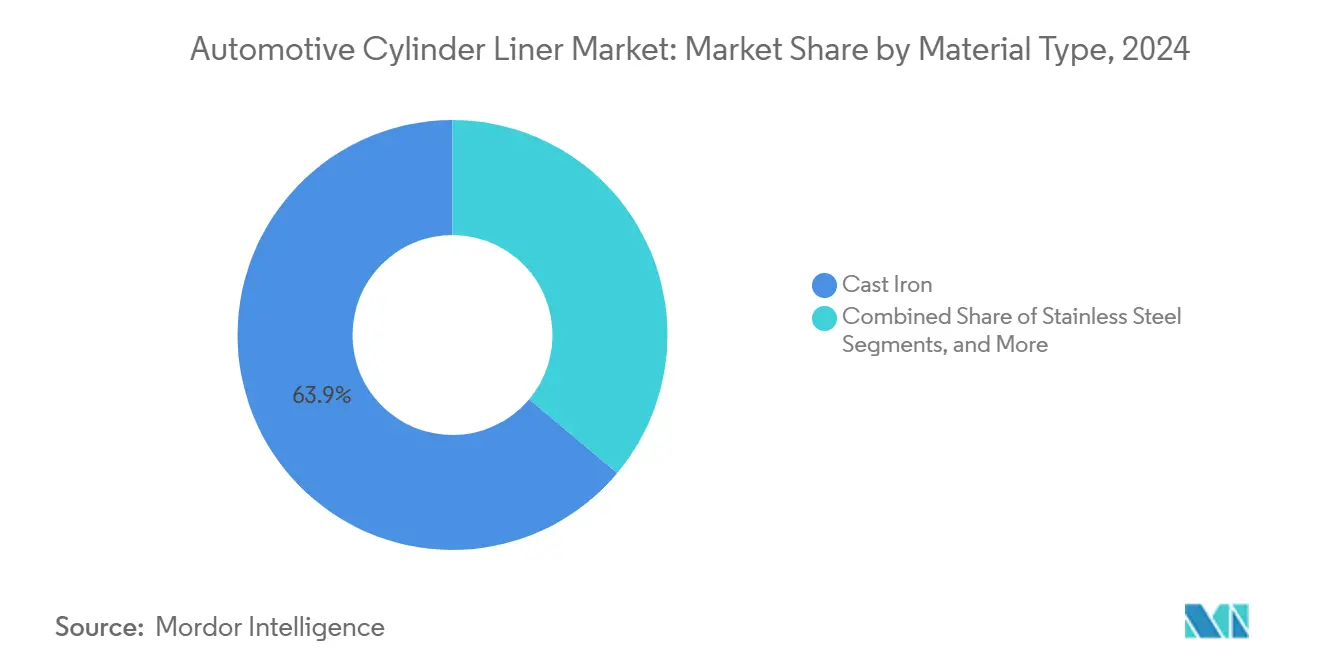

- By material type, cast iron dominated with 63.87% of the automotive cylinder liner market size in 2024, while composite liners posted the highest 9.96% CAGR through 2030.

- By manufacturing process, sand casting led with 52.74% share of the automotive cylinder liner market in 2024; hydroforming is projected to expand at an 8.75% CAGR through 2030.

- By cylinder configuration, inline engines captured 70.82% of the automotive cylinder liner market share in 2024, while V-shaped engines are forecast to see a 6.51% CAGR growth through 2030.

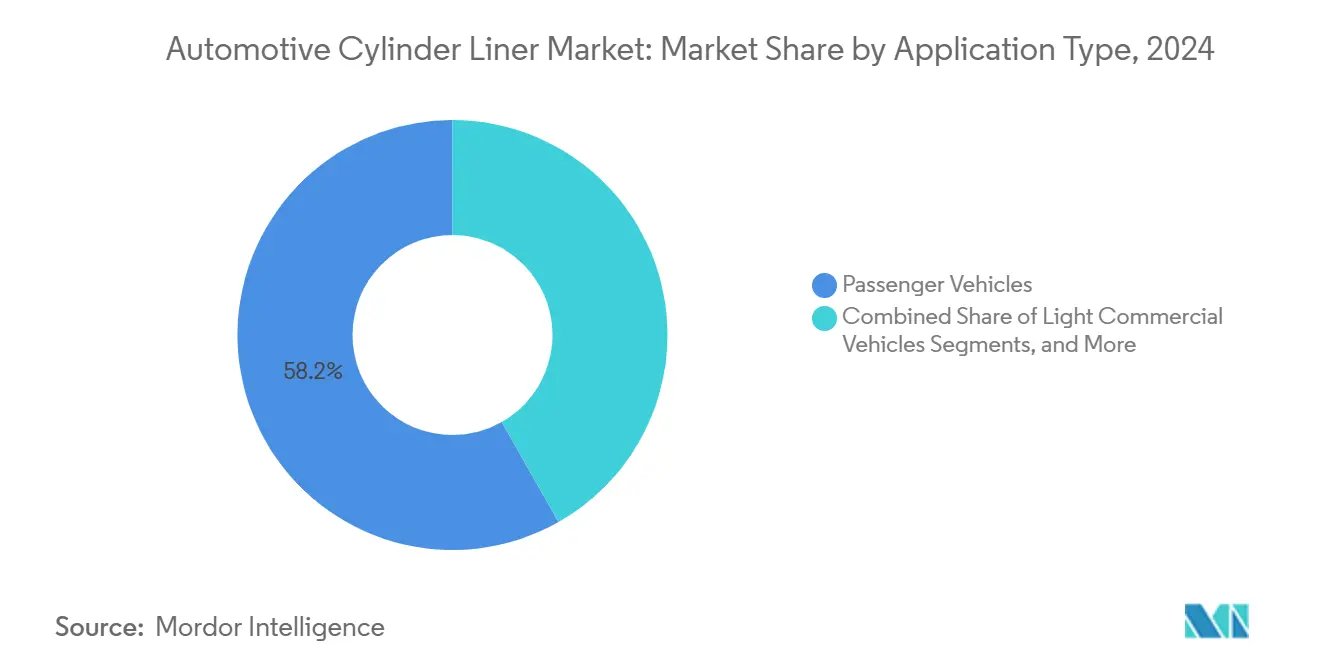

- By application type, passenger vehicles accounted for a 58.23% share of the automotive cylinder liner market in 2024. In contrast, medium- and heavy-duty vehicles are poised to register the fastest growth rate of 7.64% from 2024 to 2030.

- By surface treatment, honed liners held a 46.15% share of the automotive cylinder liner market in 2024, while nitrided liners advanced at an 8.18% CAGR driven by durability demand during the forecast period.

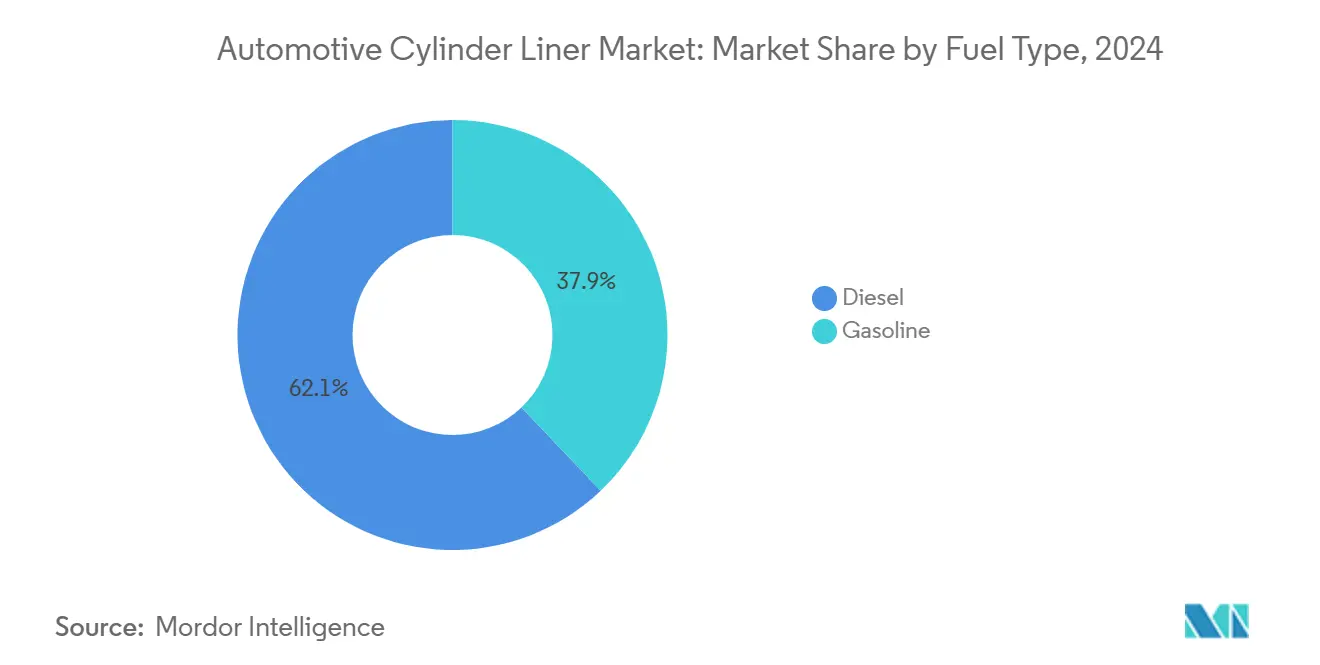

- By fuel type, diesel engines accounted for 62.14% of the automotive cylinder liner market size in 2024; gasoline applications are poised to grow at a 6.85% CAGR through 2030.

- By contact type, wet liners represented a 68.29% revenue share in 2024, as dry liners are expected to advance at a 5.47% CAGR driven by passenger-car lightweighting strategies through 2030.

- By geography, the Asia-Pacific region accounted for 41.76% of the automotive cylinder liner market share in 2024, while the Middle East and Africa are projected to witness an 8.39% share through 2030.

Global Automotive Cylinder Liner Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Electrification-Resistant Demand from Heavy-Duty ICE Engines | +1.8% | Global, with concentration in North America, Europe, and Asia-Pacific | Long term (≥ 4 years) |

| Tightening Emission Norms Boosting Lightweight Composite Liners | +1.2% | Global, led by Europe and North America regulatory frameworks | Medium term (2-4 years) |

| Rapid Expansion of Remanufacturing and Aftermarket Engine Rebuilds | +0.9% | Asia-Pacific core, with spillover to Middle East and Africa and Latin America | Medium term (2-4 years) |

| Growth of Tier-3 Regional Foundries in South and Southeast Asia | +0.7% | South Asia and Southeast Asia, with export potential to Middle East and Africa | Long term (≥ 4 years) |

| Mainstream OEM Shift Toward Modular Engine Platforms | +0.6% | Global, with early adoption in Europe and North America | Medium term (2-4 years) |

| Fleet Life-Extension Programs in Emerging Markets | +0.5% | Emerging markets in Asia-Pacific, Middle East and Africa, and Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Electrification-Resistant Demand from Heavy-Duty ICE Engines

Heavy-duty trucks, construction machinery, and off-highway equipment face payload and range barriers that limit full battery electrification in the coming decade. These fleets continue to specify durable cylinder liners that withstand higher compression ratios, extended duty cycles, and frequent rebuilds. End-user focus on lifetime operating cost keeps investment directed toward robust cast iron and upgraded composite liners that meet output and endurance targets under stricter nitrogen oxide and particulate caps. Sustained infrastructure expansion and international freight volumes reinforce demand stability despite wider passenger-car electrification.

Tightening Emission Norms Boosting Lightweight Composite Liners

Euro 7[1]"Euro 7: Deal on new EU rules to reduce road transport emissions," European Parliament, europarl.europa.eu in Europe and Tier 4 Final limits in the United States progressively reduce allowable tailpipe pollutants, compelling OEMs to integrate liners with superior heat transfer and lower mass. Composite solutions combining aluminum alloys or ceramic layers help engines run cooler and meet transient emissions by cutting friction and stabilizing combustion temperatures. Plasma spray and diamond-like carbon coatings further decrease wear and oil consumption, supporting regulatory compliance while extending service intervals.

Rapid Expansion of Remanufacturing and Aftermarket Engine Rebuilds

Cost-sensitive operators increasingly opt to rebuild engines rather than replace vehicles, driving liner replacement volumes in areas with maturing truck fleets. In India, the broader automotive aftermarket is forecasted to demonstrate a high growth rate through 2030, with cylinder liners accounting for a sizable share of rotating parts demand. Engine-rebuild centers invest in advanced honing, automated inspection, and digital measurement to return liners to OEM tolerances, thereby assuring consistent performance and reducing downtime.

Growth of Tier-3 Regional Foundries in South and Southeast Asia

Vietnam, Thailand, and Bangladesh offer competitive labor, state incentives, and proximity to iron ore, drawing investments into small and midsize foundries. New entrants serve localized production runs for regional OEMs and leverage shorter lead times and lower logistics costs. Technology transfer from multinational producers, combined with certification programs such as IATF 16949, enhances process capability, enabling these foundries to deliver liners that meet global metallurgical and dimensional accuracy standards.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Long-Term EV Adoption in Passenger Cars | -1.4% | Global, with accelerated impact in Europe, China, and California | Long term (≥ 4 years) |

| Volatile Ferrous Metal Prices Eroding Supplier Margins | -0.8% | Global, with particular impact on cost-sensitive emerging markets | Short term (≤ 2 years) |

| Capital Intensity of Composite Liner Production Lines | -0.6% | Global, with higher barriers in emerging markets | Medium term (2-4 years) |

| OEM In-House Liner Manufacturing Trend | -0.4% | North America and Europe, with selective adoption in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Long-Term EV Adoption in Passenger Cars

Battery EV penetration in passenger models is expected to climb sharply through policy mandates like the California Advanced Clean Cars II rule. Shrinking internal-combustion engine allocations in volume passenger platforms gradually compress liner demand, particularly in compact and midsize vehicles. Premium sports cars and performance applications still rely on high-revving ICE variants, though volumes remain niche relative to total OEM production.

Volatile Ferrous Metal Prices Eroding Supplier Margins

Iron ore and steel billet prices swung over 30% during 2024, creating unpredictable cost bases for cast iron liner manufacturers. Material expenses account for roughly two-thirds of liner production cost, so unstable pricing erodes profitability when surcharges lag raw-material spikes. Smaller regional producers without hedging programs or captive mines face the greatest exposure, prompting accelerated process efficiencies, energy conservation programs, and selective forward-buy contracts to cushion volatility.

Segment Analysis

By Material Type: Cast Iron Durability Meets Composite Innovation

Cast iron held 63.87% of the automotive cylinder liner market size in 2024 due to its proven strength under high cylinder pressures and its cost-effective supply chain. Despite weight penalties, heavy-duty trucks and marine engines often favor cast iron for its thermal stability under continuous loads. Composite liners, while only a fraction of 2024 unit shipments, grow at a 9.96% CAGR to 2030. The shift is driven by aluminum-silicon alloys that reduce engine mass and enhance heat conduction, thereby addressing stricter tailpipe regulations.

Manufacturers now deploy simulation tools that streamline alloy design, allowing composite liners to exhibit near-cast iron wear resistance at lower density. As tool wear falls and reject rates drop, volume economics improve, creating a tipping point for broader adoption beyond high-performance vehicles. Over the outlook, dual-material strategies emerge, combining cast iron for durability-critical cylinders and composites for lighter modules, enabling OEMs to adjust to divergent regional emission timelines without redesigning entire block architectures.

Note: Segment shares of all individual segments available upon report purchase

By Manufacturing Process: Sand Casting Tradition Versus Hydroforming Precision

Sand casting held 52.74% of the automotive cylinder liner market size in 2024, favored for its ability to produce complex shapes with inexpensive tooling. Lines employing automated molding and core setting now reach cycle times that rival machining for mid-volume runs, making sand casting a cornerstone of replacement and remanufacturing demand. Hydroforming, although still small in share, demonstrates the fastest 8.75% CAGR through 2030, as it fabricates thin-wall liners with uniform grain flows and tighter dimensional repeatability.

Hydroformed liners enable weight reductions without compromising wall strength, aligning closely with the uptake of composite materials. OEM modular engine programs further encourage hydroforming because standard bore diameters across multiple displacements facilitate the use of shared tooling, thereby cutting capital expenditure. As precision increases, downstream honing steps become shorter, improving throughput and freeing up plant capacity. Makers that integrate hydroforming alongside legacy sand lines gain portfolio flexibility that adapts to market shifts between cost-driven commercial vehicles and regulation-driven passenger platforms.

By Cylinder Configuration: Inline Dominance Challenged by V-Shaped Performance

Inline blocks delivered 70.82% of the automotive cylinder liner market size in 2024, reflecting their efficiency in packaging smaller engine bays and the prevalence of four- and six-cylinder passenger models. The configuration also simplifies coolant jacket routing, keeping liner manufacturing straightforward and cost-competitive. V-shaped engines, although representing a narrower base, expand at a 6.51% CAGR due to premium SUV and commercial applications that require high torque in compact footprints.

V engines require more intricate liner geometry to manage uneven heat gradients, prompting suppliers to adopt coated cast iron or hybrid wall constructions. Premium automakers pair these liners with spray-boring or localized nitriding to reduce oil consumption under high specific outputs. Rebuilders also identify recurring V-engine wear clusters, driving proprietary oversized liner programs that restore bore concentricity and extend service life in heavy-haul applications.

By Application Type: Passenger Volume Meets Commercial Growth

Passenger vehicles accounted for 58.23% of the automotive cylinder liner market size in 2024, primarily driven by routine engine overhauls in the Asia-Pacific and Latin America regions, where vehicle lifetimes often exceed 15 years. Yet, medium- and heavy-duty vehicles are expected to achieve a 7.64% CAGR through 2030, reflecting global freight expansion and increased mining activity. The automotive cylinder liner market share tied to vocational trucks and off-road equipment benefits from longer duty cycles and stricter uptime requirements, prompting fleets to select liners with advanced coatings resistant to high-sulfur fuels.

Leading liner producers collaborate with filtration and coolant treatment specialists to offer integrated warranty packages that enhance asset reliability for fleet operators. Passenger-car electrification curtails long-term new-build liner volumes; yet, higher power density turbo petrol engines still rely on friction-optimized bores, where honed and nitrided finishes maintain significance.

Note: Segment shares of all individual segments available upon report purchase

By Surface Treatment: Honed Standards Meet Nitride Advancement

Honed liners accounted for 46.15% of the automotive cylinder liner market size in 2024, with plateau-honing delivering ideal oil retention for break-in and sustained lubrication. The treatment remains the backbone for both OEM first-fit and independent overhauls owing to its repeatability across materials. Nitrided liners log an 8.18% CAGR by forming complex epsilon iron nitride layers that withstand abrasive soot in EGR-equipped diesels.

Plasma nitriding techniques run at lower temperatures than gas nitriding, preventing liner distortion and preserving dimensional integrity. Hybrid processes combine micro-texturing with nitriding, enabling superior ring sealing that reduces blow-by and oil consumption under transient loads. Investments in multi-station nitriders ensure growing capacity to meet rising demand from turbocharged heavy-duty engines that must comply with real-world driving emission tests.

By Fuel Type: Diesel Leadership Faces Gasoline Efficiency

Diesel engines held 62.14% of the automotive cylinder liner market share in 2024, as the freight, agriculture, and marine sectors rely on their torque and fuel economy. Stricter diesel particulate and NOx limits require liners with high thermal conductivity and low distortion. Tier 4 and Euro VII obligations compress the acceptable liner wear to maintain emissions within the design life, driving the adoption of composite or coated cast iron.

Gasoline liners expand at a 6.85% CAGR through 2030 as small-displacement turbo engines gain traction. Here, direct injection creates a fuel wash that can dilute oil, necessitating bore finishes with micro-dimple textures that retain oil while expelling soot. OEMs enhance liners with diamond-like carbon coatings that reduce boundary friction, supporting fleet-average CO₂ targets without costly redesigns.

By Contact Type: Wet Liner Tradition Versus Dry Liner Engineering

Wet liners held 68.29% of the automotive cylinder liner market share in 2024, prized for their direct coolant contact, which rapidly removes heat in large displacement diesels and stationary engines. Their design allows field replacement without block machining, reducing downtime in commercial fleets. Dry liners, though lighter, historically struggled with heat rejection. Process improvements and higher-grade gray irons now raise thermal conductivity, enabling a 5.47% CAGR through 2030, as automakers pursue smaller, lighter blocks for hybrid vehicles.

Dry liners also simplify assembly lines by eliminating individual liner seals, reducing leak paths, and shortening block machining cycles. In parallel, additive manufacturing of block-in-liner structures emerges, where closely controlled bore alloys integrate cast-in-place dry liners to achieve optimal stiffness-to-weight ratios, particularly in performance sports cars.

Geography Analysis

The Asia-Pacific region dominated the automotive cylinder liner market, accounting for a 41.76% share in 2024. China leads in passenger and heavy-duty production volumes, supported by a full-range domestic supply chain, while India’s truck manufacturing rebounds and government incentives boost regional liner demand. North America claims steady revenue through heavy-duty truck output and a mature remanufacturing ecosystem that services aging vehicle populations. Environmental Protection Agency regulations are accelerating the adoption of composite liners in new engines to lower greenhouse gas emissions. At the same time, the off-road segments in mining and agriculture continue to maintain high volumes of cast iron.

Europe focuses on advanced liner technologies vital for Euro 7 compliance. Suppliers invest in plasma spray and thin-wall aluminum liners that reduce engine mass and improve catalyst warm-up times. Stringent sustainability directives also propel a circular economy approach, where spent liners are reclaimed, remelted, and recast, thereby cutting virgin iron demand and lowering CO₂ emissions. Despite passenger-car EV momentum, steady production of light commercial vans and niche performance vehicles preserves liner requirements across the forecast.

The Middle East and Africa are expected to exhibit the fastest growth rate of 8.39% through 2030. Fleet modernization across Gulf Cooperation Council states, coupled with the development of large-scale logistics hubs and mining projects, drives demand for heavy-duty diesel. South Africa’s engine parts manufacturing cluster services both domestic truck assembly and regional aftermarket sales. New investment zones in Egypt and Morocco are encouraging the localized machining of imported rough cast liners, thereby boosting employment and minimizing shipping costs.

Competitive Landscape

The market shows moderate concentration. Global leaders such as Mahle, Federal-Mogul (Tenneco), Nippon Piston Ring, and Rheinmetall possess significant technology portfolios that encompass composite metallurgy, DLC coatings, and fully automated honing lines. Their vertically integrated models secure raw material supply, ensure traceability, and meet IATF 16949 and ISO 14001 certifications. Regional manufacturers compete through cost leadership and quick turnaround across replacement channels.

Strategic investments target lightweight lining solutions and flexible manufacturing. MAHLE’s investment in composite liner lines in Germany and China enhances capacity for Euro 7 platforms. Additionally, MAN Truck & Bus has awarded MAHLE a pivotal contract to provide cutting-edge components, including cylinder liners, for its hydrogen-powered hTGX truck[2]Abhijeet Singh, "MAHLE Secures Contract For Hydrogen Engine Components In MAN hTGX Truck," MOBILITY OUTLOOK, mobilityoutlook.com . Nippon Piston Ring’s joint venture in India increases access to fast-growing South Asian rebuild volumes[3]"Establishment of NPR AUTO PARTS MANUFACTURING INDIA PRIVATE LIMITED, NPR-RIKEN Corporation, npr-riken.co.jp. Mid-tier suppliers are embracing automation, coupling robotic handling with in-process gauging to enhance output consistency and qualify for global sourcing bids.

Patent activity centers on thermal barrier spray coatings and ceramic matrix layers that prolong ring life under low-viscosity lubricants. Cross-licensing sometimes emerges, allowing smaller firms to adopt proven coatings while compensating innovators via royalties. The aftermarket also witnesses rising branded liner kits that bundle rings, gaskets, and fasteners, simplifying procurement for independent workshops. Overall, competition blends high-value technology differentiation with regional cost competitiveness.

Automotive Cylinder Liner Industry Leaders

-

Mahle GmbH

-

Tenneco Inc.

-

TPR Co. Ltd.

-

ZYNP International Corporation

-

Nippon Piston Ring Co. Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Ruifeng Power Group Company Limited, listed on the Hong Kong Stock Exchange, has experienced a notable increase in cylinder block sales. The company attributes this boost to increased demand in its primary markets and improvements in operational efficiency.

- May 2024: ZYNP Corporation, based in China, secured a USD 100 million contract with General Motors for the supply of cylinder liners. This agreement highlights the growing demand for high-performance engine components in the global automotive market. Industry experts note an increasing trend: manufacturers are channeling investments into advanced materials and coatings, aiming to align with increasingly stringent efficiency and emission benchmarks.

Global Automotive Cylinder Liner Market Report Scope

A cylinder liner is a part of the engine assembly that is fitted to the engine block to form the cylinder. Additionally, the liner plays a crucial role in providing smoothness to the reciprocating surface during engine operation.

The automotive cylinder liner market is segmented by material type, fuel type, contact, vehicle type, engine capacity, and geography. By material type, the market is segmented into cast iron, stainless steel, aluminum, and titanium. By fuel type, the market is segmented into gasoline and diesel. By contact, the market is segmented into wet cylinder liners and dry cylinder liners. By vehicle type, the market is segmented into passenger cars, light commercial vehicles, and medium and heavy-duty commercial vehicles. By geography, the market is segmented into North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa.

The report provides market sizes and forecasts in terms of value (USD) for all the aforementioned segments.

| Cast Iron |

| Stainless Steel |

| Composite Materials |

| Sand Casting |

| CNC Machining |

| Hydroforming |

| Inline |

| V-Shaped |

| Passenger Vehicles |

| Light Commercial Vehicles |

| Medium and Heavy-Duty Vehicles |

| Bus and Coach |

| Uncoated |

| Nitrided |

| Honed |

| Gasoline |

| Diesel |

| Wet Cylinder Liner |

| Dry Cylinder Liner |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Turkey | |

| Rest of Middle East and Africa |

| By Material Type | Cast Iron | |

| Stainless Steel | ||

| Composite Materials | ||

| By Manufacturing Process | Sand Casting | |

| CNC Machining | ||

| Hydroforming | ||

| By Cylinder Configuration | Inline | |

| V-Shaped | ||

| By Application Type | Passenger Vehicles | |

| Light Commercial Vehicles | ||

| Medium and Heavy-Duty Vehicles | ||

| Bus and Coach | ||

| By Surface Treatment | Uncoated | |

| Nitrided | ||

| Honed | ||

| By Fuel Type | Gasoline | |

| Diesel | ||

| By Contact Type | Wet Cylinder Liner | |

| Dry Cylinder Liner | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the automotive cylinder liner market by 2030?

The market is forecast to reach USD 9.31 billion by 2030, growing at a 5.11% CAGR through 2030.

Which material type dominates volume?

Cast iron remains the leading material, retaining 63.87% of 2024 revenue due to proven durability and established manufacturing networks.

Which region shows the highest growth rate through 2030?

The Middle East and Africa post the fastest 8.39% CAGR, supported by fleet modernization and infrastructure programs.

How fast are composite liners growing?

Composite liners register a 9.96% CAGR, the highest among material types, driven by lightweighting and emission compliance needs.

What manufacturing process records the quickest expansion?

Hydroforming advances at an 8.75% CAGR because it delivers precise thin-wall liners that suit modular engine architectures.

Why are nitrided liners gaining traction?

Nitrided surfaces improve hardness and wear resistance, supporting prolonged service intervals in turbocharged and heavy-duty engines.

Page last updated on: