| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 29.57 Billion |

| Market Size (2030) | USD 37.74 Billion |

| CAGR (2025 - 2030) | 5.00 % |

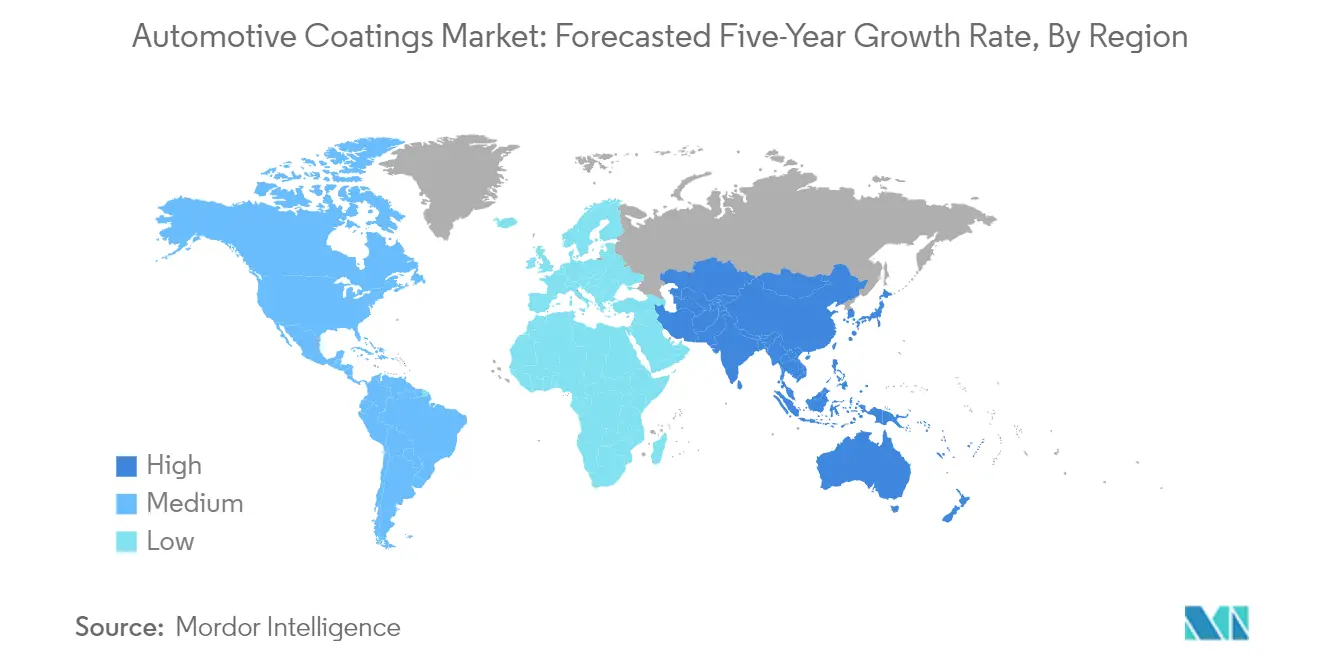

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia Pacific |

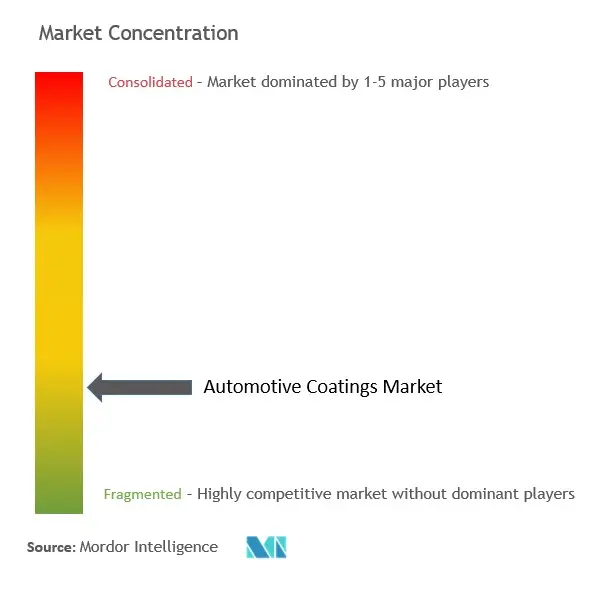

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Automotive Coatings Market Analysis

The Automotive Coatings Market size is estimated at USD 29.57 billion in 2025, and is expected to reach USD 37.74 billion by 2030, at a CAGR of greater than 5% during the forecast period (2025-2030).

The automotive coatings industry continues to evolve amid significant transformations in the global automotive sector. According to industry data, global vehicle production reached 85.4 million units in 2022, marking a substantial growth of 5.7% compared to the previous year, indicating a robust recovery in manufacturing activities. This growth has been accompanied by increasing demands for sustainable coating solutions, with manufacturers focusing on developing eco-friendly products that comply with stringent environmental regulations while maintaining high-performance standards. The industry is witnessing a shift toward water-based and powder coatings, reflecting the broader automotive sector's commitment to reducing environmental impact and meeting regulatory requirements.

The rapid transition toward electric vehicles (EVs) is fundamentally reshaping coating requirements and application processes. In 2023, global electric vehicle sales reached 14.8 million units, representing a significant increase of 15.8% compared to 2022. This shift has spurred innovation in automotive paint technologies, particularly for battery components and lightweight materials commonly used in EVs. Manufacturers are developing specialized car paint that provides enhanced protection against electromagnetic interference, thermal management, and corrosion resistance specifically designed for electric vehicle components.

Technological advancements in auto paint materials and application processes are driving significant improvements in efficiency and performance. The industry is experiencing increased adoption of automated application systems and smart coating technologies that offer functionalities beyond conventional primers, such as self-healing properties and anti-scratch features. These innovations are particularly evident in the refinish segment, where advanced vehicle paint systems are being developed to accommodate the growing complexity of vehicle surfaces and materials while ensuring optimal adhesion and durability.

Regional production dynamics continue to shape the automotive coatings market landscape, with significant investments in manufacturing capabilities across key markets. For instance, in Malaysia, vehicle production reached approximately 774,000 units in 2023, marking a notable increase of 10.26% compared to the previous year. This regional growth is complemented by the establishment of new manufacturing facilities and the expansion of existing ones, particularly in emerging markets. Coating manufacturers are responding by localizing production and developing market-specific solutions that address varying climatic conditions and regulatory requirements while maintaining global quality standards. The automotive paint industry is thus poised for continued growth as it adapts to these dynamic changes.

Automotive Coatings Market Trends

Growing Automotive Production

The global automotive industry has witnessed substantial growth in production volumes, with total vehicle production reaching 85.4 million units in 2022, registering a growth rate of around 6% compared to approximately 80.21 million vehicles in 2021. This growth trajectory has continued into 2023, with automotive manufacturers ramping up production to meet increasing consumer demand. The automotive coatings industry directly benefits from this expansion, as each vehicle requires multiple coating layers, including e-coat, primer, basecoat, and clearcoat, for protection against environmental factors such as changing temperatures, acid rain, dust, and water, while also enhancing aesthetic appeal through automotive finish solutions.

The automotive manufacturing sector has shown remarkable resilience, with production facilities operating at increased capacities. For instance, according to the European Automobile Manufacturers Association, in the first three quarters of 2023 (January 2023 – September 2023), the total production of cars in the region increased by almost 14% compared to the same period in 2022. This growth in production volumes has been supported by improving supply chain conditions and the resolution of semiconductor shortages that previously constrained production. The increasing production volumes directly correlate to higher demand for automotive paint protection, as these coatings are essential for both interior and exterior parts of vehicles, including metallic parts and plastic vehicle components.

Understand The Key Trends Shaping This Market

Download PDF

Increasing Investments and Government Policies for Automotive OEM

Significant investments in automotive manufacturing facilities and supporting government policies have created a strong foundation for market growth. In January 2024, Honda Motor announced plans to construct an electric vehicle plant in Canada with an investment of approximately USD 14 billion. Similarly, in February 2024, Volkswagen Mexico announced an investment of around USD 1 billion for an electromobility hub in its Puebla plant. These investments demonstrate the industry's commitment to expanding production capabilities and transitioning towards electric vehicle manufacturing, which requires specialized car coating solutions.

The automotive sector has received substantial government support through various initiatives and policies. For instance, in the United States, as part of President Biden's Investing in America agenda, the Department of Energy (DOE) announced a comprehensive package of USD 15 billion for the automotive industry in 2023. This includes USD 2 billion in grants and up to USD 10 billion in loans specifically for supporting automotive manufacturing conversion projects. Additionally, in September 2023, Lucid Group opened its first car manufacturing facility in Saudi Arabia, marking a significant milestone in the country's automotive manufacturing capabilities. These investments and supportive government policies are creating new opportunities for automotive paint companies, as new production facilities require complete auto coating solutions for their manufacturing processes.

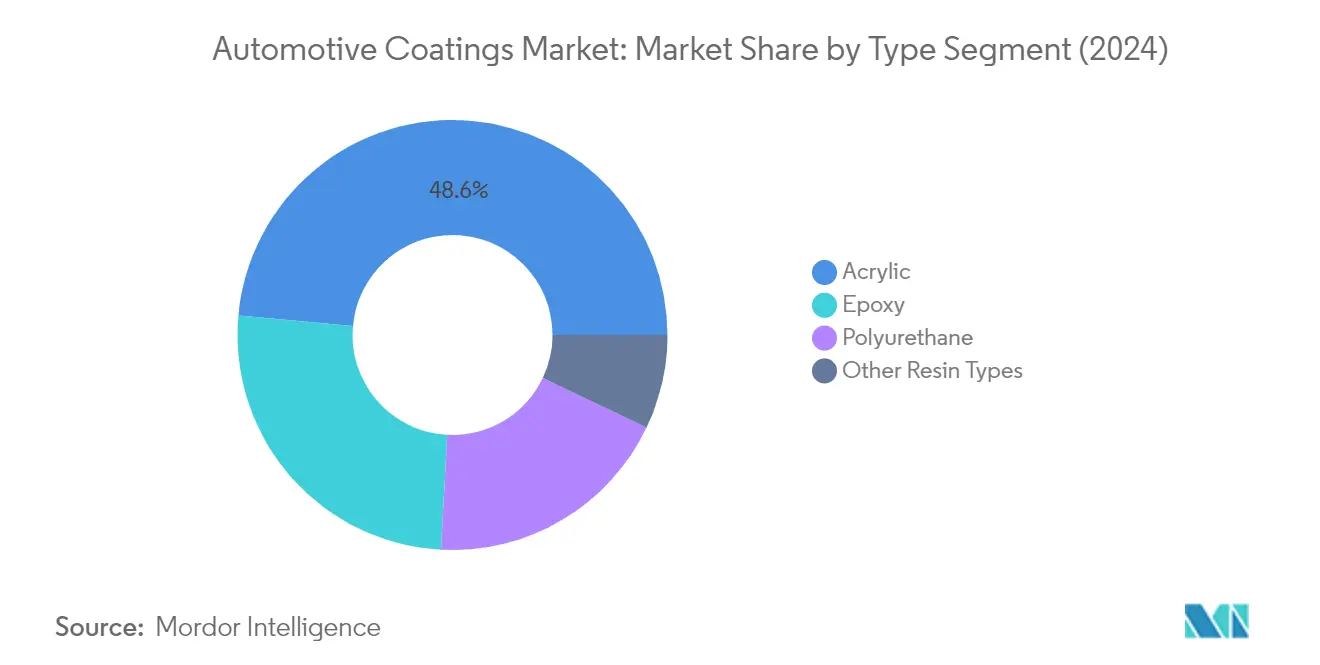

Segment Analysis: By Type

Acrylic Segment in Automotive Coatings Market

The acrylic segment dominates the global automotive coatings market, holding approximately 49% of the market share in 2024. Acrylic coatings are widely preferred due to their excellent color and gloss retention capabilities, along with superior durability and good adhesion properties across various substrates. Water-based acrylic coatings are experiencing particularly high demand due to growing environmental concerns and regulations around VOC emissions. These coatings offer strong resistance against chipping and fading while providing a glossy finish at a competitive price point. The segment's dominance is further strengthened by the increasing adoption of water-based acrylic coatings in automotive manufacturing, particularly in regions with strict environmental regulations.

Polyurethane Segment in Automotive Coatings Market

The polyurethane segment is projected to witness the fastest growth in the automotive coatings market, with an expected growth rate of approximately 5% during the forecast period 2024-2029. This growth is primarily driven by polyurethane coatings' superior performance characteristics, including excellent UV resistance, weather resistance, and chemical resistance properties. These coatings are particularly valued for their ability to provide high-quality finishes with exceptional durability and scratch resistance in both wet and dry conditions. The segment's growth is further supported by increasing demand for premium automotive finishes and the expanding electric vehicle market, where polyurethane coatings are preferred for their superior protection and aesthetic properties.

Remaining Segments in Automotive Coatings Market by Type

The epoxy and other resin types segments continue to play crucial roles in the automotive coatings market. Epoxy coatings are particularly valued for their excellent corrosion resistance and strong adhesion properties, making them ideal for primer applications and protective coatings in automotive manufacturing. The other resin types segment, which includes fluoropolymer, polyester, and polyaspartic coatings, offers specialized solutions for specific automotive applications. These segments cater to diverse requirements in the automotive industry, from providing enhanced protection for specific components to meeting specialized performance requirements in various automotive applications.

Segment Analysis: Technology

Solvent-borne Segment in Automotive Coatings Market

The solvent-borne coatings segment dominates the automotive coatings market, accounting for approximately 71% of the total market share in 2024. This significant market position is attributed to solvent-borne coatings' high viscosity, low cost, and superior performance characteristics. These coatings are widely preferred in the automotive industry due to their excellent durability and resistance to harsh conditions. The segment is also expected to maintain its leading position with the highest growth rate of around 5% during 2024-2029. Solvent-borne coatings are typically available as one-component or two-component resin-based systems for both OEM and refinish applications, offering various properties including anti-squeak features, chemical resistance, good leveling extension, high mechanical resistance, high sagging limit, and superior scratch resistance. These coatings can be applied to numerous substrates including polycarbonate, carbon fiber, galvanized aluminum, polyamide, and steel, making them versatile for various automotive applications.

Water-borne Segment in Automotive Coatings Market

The water-borne coatings segment represents a significant portion of the automotive coatings market, driven by increasing environmental regulations and growing demand for eco-friendly coating solutions. These coatings are gaining acceptance in the automotive industry owing to their environmental friendliness, durability, and performance efficiency. Water-borne coatings typically have higher coverage than solvent-based coatings due to their higher solids content, allowing them to cover vehicles more efficiently and reduce application time. The introduction of alkyd latex resin technology has enabled coating manufacturers to combine the performance advantages of alkyd-based paint chemistries with solvent-free water-borne coatings. Additionally, water-borne coatings do not require thinners, additives, or hardeners, making them more cost-effective and environmentally sustainable.

Remaining Segments in Technology

The automotive powder coating segment, while smaller in market share, plays a crucial role in specific automotive applications. Powder coatings offer unique advantages such as zero or near-zero levels of volatile organic compounds, making them environmentally friendly. These coatings are particularly effective for high-heat-resistant parts such as engine blocks, intake manifolds, window trims, door frames, and handles. The powder coating technology has evolved to become an alternative for auto-body coating as automotive manufacturers seek to reduce both their carbon footprint and costs without compromising on technical quality or performance. Recent technological advancements have enabled powder coating systems to reduce the number of process steps and achieve significant reductions in energy consumption.

Segment Analysis: Layers

Clear Coat Segment in Automotive Coatings Market

Clear coat dominates the automotive coatings layers market, holding approximately 35% market share in 2024. As the top layer of the automotive paint system, automotive clear coat plays a crucial role in providing effective protection against harmful outside influences while helping the car maintain its shine. The segment's prominence is driven by its ability to offer high scratch resistance in both wet and dry conditions, along with superior chemical resistance against environmental factors like bird droppings and oil. Clear coats have evolved to include innovative features like matte finishes, which have become increasingly popular for their ability to give a unique silky and smooth finish while highlighting the vehicle's shape. The segment has also seen significant advancement in structured clear coats, which offer texture effects on cars, allowing designers to highlight specific areas according to their preferences. Additionally, the increasing focus on high solids clear coats, which reduce the emission of volatile organic compounds (VOCs) during the painting process, has further strengthened this segment's market position.

E-coat Segment in Automotive Coatings Market

The E-coat segment is projected to witness the highest growth rate of approximately 5% during the forecast period 2024-2029. This growth is primarily attributed to its superior efficiency in coating film formation using electricity, achieving 95% or more paint utilization compared to traditional spray coating methods. E-coat technology has become increasingly vital in the automotive industry due to its ability to protect surfaces, edges, and cavities of car bodies from corrosion while providing an excellent base for subsequent paint layers. The segment's growth is further driven by its eco-friendly characteristics and the development of lead-free cathodic epoxy electrocoat products. The technology's ability to paint and coat complex parts while ensuring high uniformity of coating has made it particularly attractive to vehicle manufacturers. Additionally, the adoption of electrocoating technology has been boosted by the increasing utilization of fast coating methods in factories, contributing to improved manufacturing speed and efficiency. The segment also benefits from ongoing innovations in e-coat materials that produce significantly less solid waste and have substantially lower environmental impact compared to other coating processes.

Remaining Segments in Layers

The automotive primer and automotive basecoat segments continue to play vital roles in the automotive coatings market, each serving distinct purposes in the coating process. Primers provide the critical bond to the electrodeposition coating and ensure adhesion between the primer and base coat or topcoat, while also protecting the electrodeposition layer from UV degradation and providing stone chip resistance. The base coat segment is crucial for imparting color and aesthetic appeal to vehicles, offering various options including solid, metallic, or pearlescent finishes. Recent innovations in these segments include the development of thin-film primers based on water-borne technology, designed for extraordinary performance at low film thickness, and the introduction of advanced basecoat systems that achieve an unprecedented balance of properties for automotive coating systems, providing stunning visual appearance and long-term durability.

Segment Analysis: Application

OEM Segment in Automotive Coatings Market

The Original Equipment Manufacturer (OEM) segment dominates the global automotive coatings market, accounting for approximately 71% of the total market share in 2024. This segment's prominence is primarily driven by the growing automotive production across major manufacturing hubs worldwide. The segment has also witnessed significant growth due to increasing investments in electric vehicle manufacturing facilities and supportive government policies for automotive OEM operations. Major automotive manufacturers are expanding their production capabilities, particularly in emerging markets, while simultaneously adopting advanced coating technologies to meet evolving environmental regulations and consumer preferences. The rise in electric vehicle production has created new opportunities for automotive OEM coating, as these vehicles require specialized coating solutions for battery components and lightweight materials. Furthermore, the segment is experiencing robust growth with a projected growth rate of around 5% from 2024 to 2029, driven by technological advancements in coating materials and increasing demand for sustainable coating solutions.

Refinish Segment in Automotive Coatings Market

The automotive refinish coating segment represents a significant portion of the automotive coatings market, serving the aftermarket and repair sectors. This segment plays a crucial role in maintaining and restoring vehicles' appearance and protection after accidents or wear and tear. The segment's growth is supported by the increasing number of vehicle collisions and the rising demand for used cars across various regions. In countries like Italy and India, the segment has seen substantial growth due to increasing road accidents and subsequent repair requirements. The refinish segment is also evolving with the introduction of water-based and low-VOC coating solutions to meet stringent environmental regulations. Additionally, the segment is benefiting from the growing premium car market and increasing consumer preference for maintaining vehicle aesthetics. The automotive refinish coating manufacturers are focusing on developing innovative products that offer better durability, faster drying times, and enhanced color matching capabilities to meet the evolving needs of body shops and repair centers.

Automotive Coatings Market Geography Segment Analysis

Automotive Coatings Market in Asia-Pacific

The Asia-Pacific region represents the largest and most dynamic automotive coatings market globally, driven by robust automotive manufacturing activities across multiple countries. The region encompasses major automotive manufacturing hubs, including China, India, Japan, and South Korea, along with emerging markets in Southeast Asia such as Indonesia, Malaysia, and Thailand. The automotive coatings industry in this region benefits from increasing vehicle production, growing investments in manufacturing facilities, and supportive government policies promoting domestic automotive production. The presence of both established and emerging automotive manufacturers, coupled with rising domestic demand for vehicles, continues to drive the growth of the automotive coatings market in the region.

Automotive Coatings Market in China

China dominates the Asia-Pacific automotive coatings market as the region's largest automotive producer and consumer. With approximately 58% share of the regional market in 2024, China's automotive coatings sector benefits from the country's massive automotive manufacturing infrastructure and continuous investments in production capacity. The country has experienced significant growth in electric vehicle production, currently ranking as the second-largest electric vehicle manufacturer globally. In 2023, China's automotive production increased by 4.7% during the first three quarters compared to the same period in 2022. The strong market position is further reinforced by the presence of numerous domestic and international coating manufacturers, extensive distribution networks, and ongoing technological advancements in car paint solutions.

Automotive Coatings Market in India

India emerges as the fastest-growing market in the Asia-Pacific region, with a projected growth rate of approximately 6% from 2024 to 2029. The country's automotive coatings market is experiencing rapid expansion driven by increasing vehicle production and rising investments in manufacturing facilities. The government's initiatives, such as "Make in India" and the Production Linked Incentive (PLI) Scheme for the automotive sector, are catalyzing growth in the automotive manufacturing industry. Major automotive manufacturers are expanding their production capacities in India, with companies like Tata Motors starting production at new facilities. The country's focus on electric vehicle manufacturing and the government's target of 30% electric vehicle adoption by 2030 are creating additional opportunities for automotive coatings companies.

Automotive Coatings Market in North America

The North American automotive coatings market is characterized by advanced manufacturing capabilities, stringent quality standards, and high adoption of innovative coating technologies. The region, comprising the United States, Canada, and Mexico, benefits from the presence of major automotive manufacturers and coating suppliers. The market is driven by increasing investments in electric vehicle manufacturing, technological advancements in vehicle coating solutions, and growing demand for environmentally friendly coating options. The region's strong focus on research and development, coupled with the presence of established automotive manufacturing infrastructure, continues to support market growth.

Automotive Coatings Market in United States

The United States leads the North American automotive coatings market, commanding approximately 70% of the regional market share in 2024. As the second-largest automotive market globally after China, the country maintains a robust automotive manufacturing sector with numerous assembly plants and R&D facilities. The automotive industry in the United States has shown significant recovery, with vehicle production reaching 10 million units in 2022. The market benefits from substantial investments in electric vehicle manufacturing, with various automotive companies announcing expansion plans and new manufacturing facilities across different states.

Automotive Coatings Market in Canada

Canada represents a significant growth opportunity in the North American region, with a projected growth rate of approximately 3% from 2024 to 2029. The country's automotive coatings market is supported by its strong automotive manufacturing base, particularly in regions like Quebec and Ontario. Recent developments in the electric vehicle sector, including major investments by automotive manufacturers in EV production facilities, are driving market growth. The government's ambitious targets for zero-emission vehicles and supportive policies are creating new opportunities for automotive paint manufacturers, particularly in the electric vehicle segment.

Automotive Coatings Market in Europe

The European automotive coatings market is characterized by its strong focus on technological innovation, environmental sustainability, and high-quality standards. The region encompasses major automotive manufacturing countries, including Germany, France, the United Kingdom, Italy, Spain, and Russia. The market is driven by stringent environmental regulations, increasing adoption of electric vehicles, and continuous innovations in car paint technologies. The European automotive industry's transition towards electric vehicle production and sustainable manufacturing practices is creating new opportunities for coating manufacturers across the region.

Automotive Coatings Market in Germany

Germany stands as the largest market for automotive coatings in Europe, with its strong automotive manufacturing heritage and technological leadership. The country hosts major car-making brands, including Volkswagen, Mercedes-Benz, Audi, BMW, and Porsche, supporting a robust automotive coatings market. The German automotive industry's commitment to research and development, coupled with its leadership in electric vehicle production, continues to drive innovation in coating technologies. The country's focus on sustainable manufacturing practices and advanced coating solutions reinforces its position as a key market for automotive coatings in Europe.

Automotive Coatings Market in Spain

Spain emerges as a significant growth market in the European region, driven by its expanding automotive manufacturing sector. As the second-largest automaker in Europe, Spain continues to attract investments in automotive manufacturing, particularly in the electric vehicle segment. The country's automotive industry has shown remarkable recovery from supply chain disruptions, with production facilities increasing their output. The government's support for the automotive sector, coupled with investments in electric vehicle manufacturing, is creating new opportunities for coating manufacturers in the Spanish market.

Automotive Coatings Market in South America

The South American automotive coatings market, primarily driven by Brazil and Argentina, demonstrates significant potential for growth despite economic challenges in the region. Brazil leads the market as the largest automotive producer in South America, with a robust automotive manufacturing infrastructure and increasing investments in electric vehicle production. Argentina follows as the second-largest market, benefiting from its established automotive industry and government initiatives to promote automotive manufacturing. The region's automotive coatings market is characterized by increasing domestic production capabilities and growing investments in manufacturing facilities.

Automotive Coatings Market in Middle East and Africa

The Middle East and Africa automotive coatings market presents emerging opportunities driven by increasing investments in automotive manufacturing capabilities. The region, encompassing Saudi Arabia, South Africa, and Egypt, is witnessing growing interest from global automotive manufacturers establishing production facilities. South Africa leads the regional market with its established automotive manufacturing sector, while Saudi Arabia shows the fastest growth potential due to its ambitious plans to develop its automotive industry. The region's focus on developing local manufacturing capabilities and increasing investments in electric vehicle production is expected to drive the demand for automotive coatings.

Get Analysis on Important Geographic Markets

Download PDF

Automotive Coatings Industry Overview

Top Companies in Automotive Coatings Market

The global automotive coatings market is led by established players like Axalta Coating Systems, PPG Industries, Kansai Nerolac, Nippon Paint, and AkzoNobel, who are driving innovation through sustainable coating technologies and advanced application methods. Companies are increasingly focusing on developing water-borne and low-VOC coating solutions to meet stringent environmental regulations while maintaining high-performance standards. Strategic partnerships with automotive OEMs and the expansion of production facilities, particularly in emerging markets, demonstrate the industry's commitment to operational excellence. Market leaders are investing heavily in research and development to create innovative products like scratch-resistant ceramic clearcoats and self-healing coating technologies. The competitive landscape is characterized by continuous product launches, strategic acquisitions to enhance technological capabilities, and the expansion of distribution networks to strengthen market presence across different regions.

Fragmented Market with Strong Regional Players

The automotive coatings market exhibits a fragmented structure with the top five players accounting for less than half of the global market share, while numerous regional and local players serve specific geographic markets or specialized coating applications. Global conglomerates like BASF and Sherwin-Williams leverage their extensive research capabilities and broad product portfolios to maintain competitive positions, while specialized coating manufacturers focus on niche segments and custom solutions. The market has witnessed significant consolidation through strategic acquisitions, particularly in emerging markets, as companies seek to expand their geographic footprint and technological capabilities.

The industry is characterized by a mix of multinational corporations with integrated operations across the value chain and specialized coating manufacturers focusing on specific market segments. Recent years have seen increased merger and acquisition activity, with companies like Nippon Paint actively acquiring regional players to strengthen their market position and expand their product offerings. The market also features strategic alliances between coating manufacturers and raw material suppliers to ensure stable supply chains and develop innovative solutions, while partnerships with automotive manufacturers help in creating customized coating solutions for specific applications.

Innovation and Sustainability Drive Future Growth

Success in the automotive paint industry increasingly depends on companies' ability to develop sustainable coating solutions while maintaining high-performance standards and cost-effectiveness. Market leaders are investing in advanced technologies like smart coatings and nano-coatings, while also focusing on reducing environmental impact through water-based formulations and eco-friendly raw materials. The growing electric vehicle segment presents new opportunities for coating manufacturers to develop specialized solutions addressing unique requirements such as electromagnetic shielding and thermal management. Companies are also strengthening their digital capabilities to improve customer service and streamline operations.

For new entrants and smaller players, success lies in identifying and serving niche markets or specific regional demands while building strong relationships with local automotive manufacturers. The industry's high entry barriers, including significant capital requirements and stringent quality standards, make strategic partnerships crucial for market expansion. Regulatory compliance, particularly regarding VOC emissions and environmental protection, continues to shape product development and manufacturing processes. Companies must also consider the increasing consolidation in the automotive industry, which affects coating supplier relationships and necessitates strong technical capabilities to meet evolving requirements for durability, aesthetics, and sustainability.

Automotive Coatings Market Leaders

-

Akzo Nobel N.V.

-

Axalta Coating Systems Ltd

-

Kansai Nerolac Paints Limited

-

Nippon Paint Holdings Co. Ltd

-

PPG Industries Inc.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Automotive Coatings Market News

- February 2024: BASF Coatings signed a partnership agreement with INEOS Automotive for its Global Body and Paint Program. The partners will work together on a strategic partnership that sets them apart from the rest of the industry and allows them to go above and beyond the industry standard when it comes to vehicle body repairs and paint refinishes. The partnership will include sustainable refinish services, expertise, and digital color-matching solutions and training.

- July 2023: The Sherwin-Williams Company and the Mercedes-AMG PETRONAS Formula One Team announced a new partnership. Sherwin-Williams is the Official Team Partner of the Mercedes-AMG PETRONAS Formula One Team. Sherwin-Williams became the approved supplier of automotive paint and coatings for the team’s F1 cars.

- March 2023: Eastman Chemical acquired Ai-Red Technology (Dalian) Co. Ltd, a manufacturer and supplier of paint protection and window film for automotive and architectural markets in Asia-Pacific.

Automotive Coatings Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

-

4.1 Market Drivers

- 4.1.1 Growing Automotive Production

- 4.1.2 Increasing Investments and Government Policies for Automotive OEM

- 4.1.3 Other Drivers

-

4.2 Market Restraints

- 4.2.1 Stringent VOC Regulations

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

-

4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5. MARKET SEGMENTATION (Market Size in Value)

-

5.1 By Type

- 5.1.1 Polyurethane

- 5.1.2 Epoxy

- 5.1.3 Acrylic

- 5.1.4 Other Resin Types

-

5.2 By Technology

- 5.2.1 Solvent-Borne

- 5.2.2 Water-Borne

- 5.2.3 Powder

-

5.3 By Layers

- 5.3.1 E-Coat

- 5.3.2 Primer

- 5.3.3 Base Coat

- 5.3.4 Clear Coat

-

5.4 By Application

- 5.4.1 OEM

- 5.4.2 Refinish

-

5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Australia and New Zealand

- 5.5.1.6 Indonesia

- 5.5.1.7 Malaysia

- 5.5.1.8 Thailand

- 5.5.1.9 Rest of ASEAN

- 5.5.1.10 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 France

- 5.5.3.3 United Kingdom

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Egypt

- 5.5.5.4 Rest of Middle East and Africa

6. COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) Analysis

- 6.3 Strategies Adopted by Leading Players

-

6.4 Company Profiles

- 6.4.1 Akzo Nobel NV

- 6.4.2 Axalta Coating Systems Ltd

- 6.4.3 BASF SE

- 6.4.4 Beckers Group

- 6.4.5 Cabot Corporation

- 6.4.6 Eastman Chemical Company

- 6.4.7 HMG Paints Limited

- 6.4.8 Jotun

- 6.4.9 Kansai Nerolac Paints Limited

- 6.4.10 KCC Corporation

- 6.4.11 Nippon Paint Holdings Co. Ltd

- 6.4.12 Parker Hannifin Corp.

- 6.4.13 PPG Industries Inc.

- 6.4.14 RPM International Inc.

- 6.4.15 Shanghai Kinlita Chemical Co. Ltd

- 6.4.16 The Sherwin-Williams Company

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Opportunity in the Electric Vehicle Market

- 7.2 Other Opportunities

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Automotive Coatings Industry Segmentation

The automotive coatings market covers the products used during the manufacture or repair of automobiles, such as passenger cars and light commercial vehicles (LCVs), etc., to protect and decorate the metal bodywork.

The automotive coatings market is segmented by resin type, technology, layer, application, and geography. By resin type, the market is segmented into polyurethane, epoxy, acrylic, and other resin types. By technology, the market is segmented into solvent-borne, water-borne, and powder. By layer, the market is segmented into e-coat, primer, base coat, and clear coat. By application, the market is segmented into OEM and refinish. The report also covers the market size and forecasts for the automotive coatings market in 22 countries across major regions. For each segment, the market sizing and forecasts are provided based on value (USD).

| By Type | Polyurethane | ||

| Epoxy | |||

| Acrylic | |||

| Other Resin Types | |||

| By Technology | Solvent-Borne | ||

| Water-Borne | |||

| Powder | |||

| By Layers | E-Coat | ||

| Primer | |||

| Base Coat | |||

| Clear Coat | |||

| By Application | OEM | ||

| Refinish | |||

| By Geography | Asia-Pacific | China | |

| India | |||

| Japan | |||

| South Korea | |||

| Australia and New Zealand | |||

| Indonesia | |||

| Malaysia | |||

| Thailand | |||

| Rest of ASEAN | |||

| Rest of Asia-Pacific | |||

| North America | United States | ||

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| France | |||

| United Kingdom | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Saudi Arabia | ||

| South Africa | |||

| Egypt | |||

| Rest of Middle East and Africa | |||

Need A Different Region or Segment?

Customize Now

Automotive Coatings Market Research FAQs

How big is the Automotive Coatings Market?

The Automotive Coatings Market size is expected to reach USD 29.57 billion in 2025 and grow at a CAGR of greater than 5% to reach USD 37.74 billion by 2030.

What is the current Automotive Coatings Market size?

In 2025, the Automotive Coatings Market size is expected to reach USD 29.57 billion.

Who are the key players in Automotive Coatings Market?

Akzo Nobel N.V., Axalta Coating Systems Ltd, Kansai Nerolac Paints Limited, Nippon Paint Holdings Co. Ltd and PPG Industries Inc. are the major companies operating in the Automotive Coatings Market.

Which is the fastest growing region in Automotive Coatings Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Automotive Coatings Market?

In 2025, the Asia Pacific accounts for the largest market share in Automotive Coatings Market.

What years does this Automotive Coatings Market cover, and what was the market size in 2024?

In 2024, the Automotive Coatings Market size was estimated at USD 28.09 billion. The report covers the Automotive Coatings Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Automotive Coatings Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Automotive Coatings Market Research

Mordor Intelligence provides a comprehensive analysis of the automotive coatings industry. We leverage decades of expertise in automotive paint and coating research. Our extensive report covers the complete spectrum of car paint technologies. This includes automotive primer, automotive basecoat, and automotive clearcoat applications. The analysis encompasses both automotive OEM coating and automotive refinish coating segments. It offers detailed insights into automotive paint companies and their innovative solutions for vehicle coating applications.

Stakeholders across the automotive coatings industry benefit from our detailed examination of car coating trends and automotive paint regulations. We also explore emerging technologies like automotive powder coating. The report, available as an easy-to-download PDF, includes a comprehensive analysis of automotive paint protection solutions. This includes automotive paint protection film and advanced automotive finish technologies. Our research covers everything from traditional auto paint applications to cutting-edge transportation coating developments. It offers valuable insights for manufacturers, suppliers, and industry professionals involved in vehicle paint systems and solutions.