Automotive Chip Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

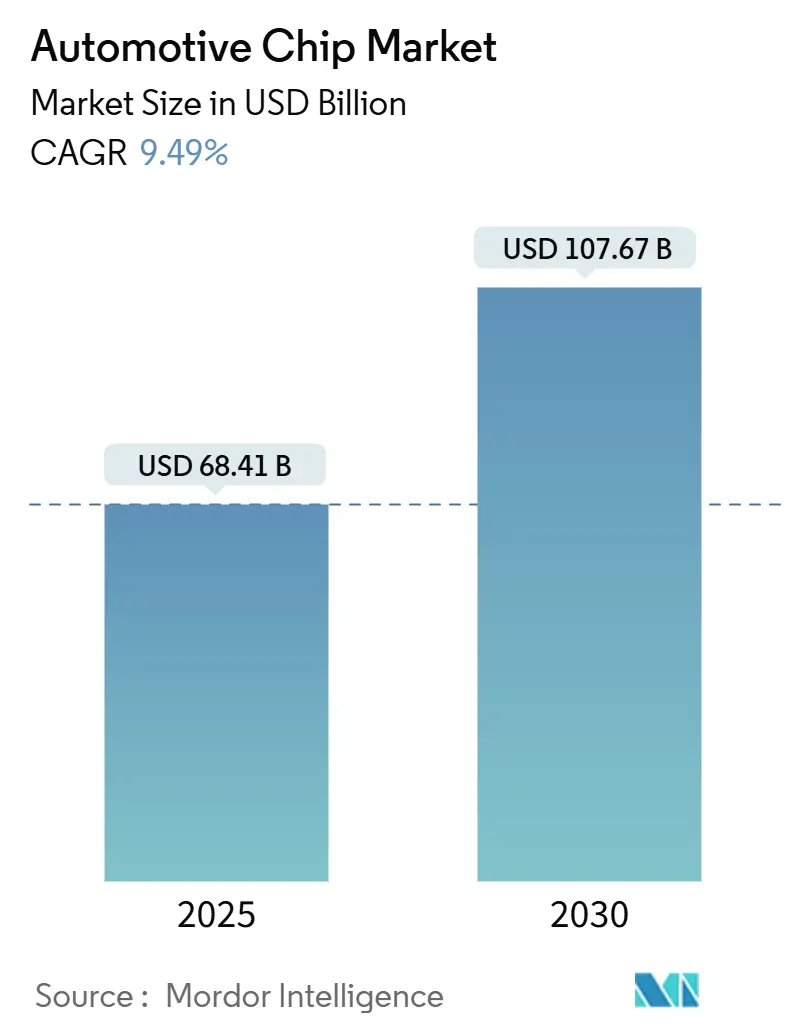

| Market Size (2025) | USD 68.41 Billion |

| Market Size (2030) | USD 107.67 Billion |

| Growth Rate (2025 - 2030) | 9.49% CAGR |

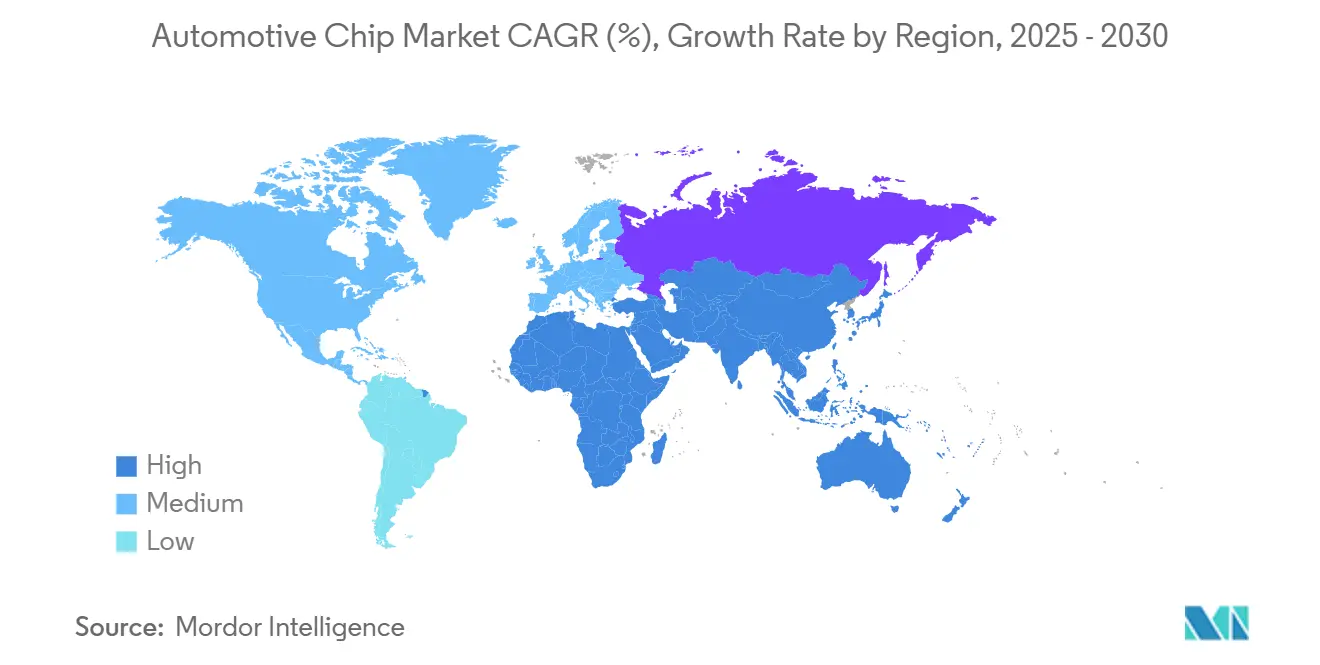

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Chip Market Analysis by Mordor Intelligence

The automotive chip market size stood at USD 68.41 billion in 2025 and is forecast to reach USD 107.67 billion by 2030, registering a 9.49% CAGR. This expansion mirrored the vehicle’s transformation into a software-defined computer on wheels as semiconductor value per car rose toward USD 1,000. Automakers replaced scores of distributed electronic control units with a handful of zonal controllers tied to centralized computers, creating sustained demand for high-performance processors, wide-bandgap power devices, and high-speed networking chips. Electric‐vehicle programs amplified the trend because battery electric models carried two to three times more semiconductor content than their internal-combustion counterparts. At the same time, the shift toward advanced fabrication nodes for Level 3+ autonomous driving and stricter cybersecurity regulations raised silicon requirements and lengthened design win cycles.[1]Texas Instruments, “Smart Power Distribution for Zonal Architectures,” ti.com

Key Report Takeaways

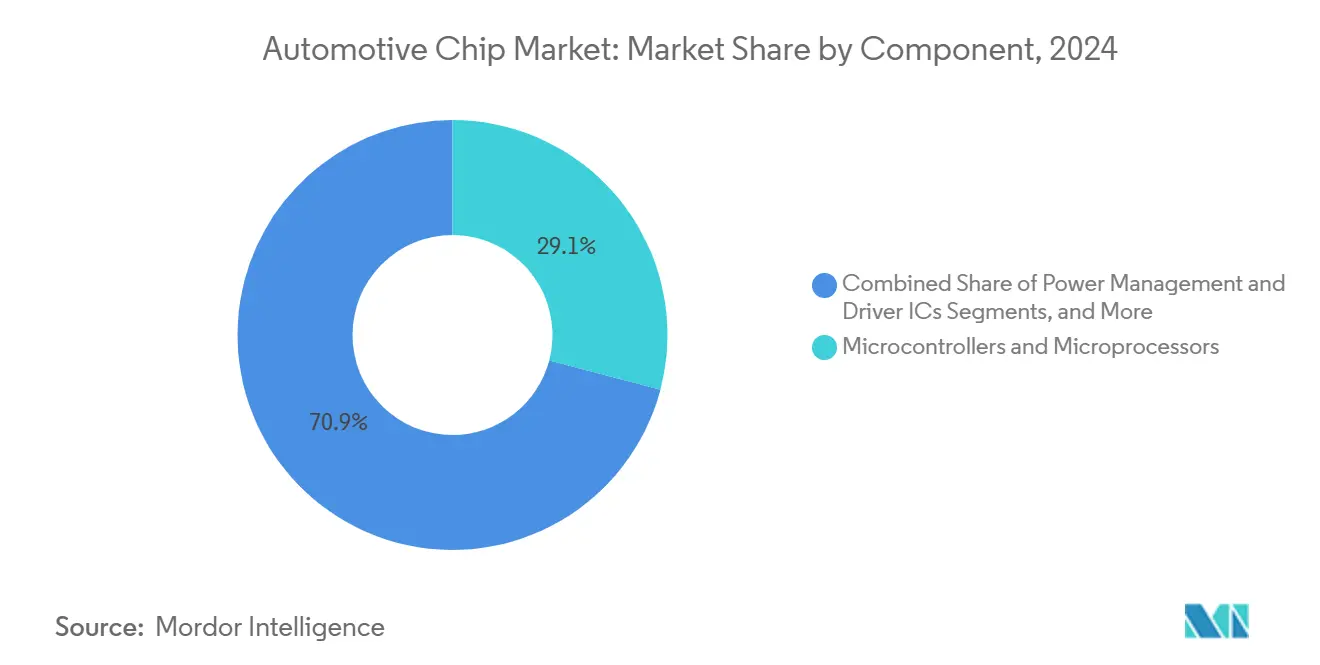

- By component, Microcontrollers and Microprocessors led with 29.1% revenue share in 2024; Sensors are projected to expand at a 13.2% CAGR to 2030.

- By fabrication node, the 23-45 nm category held 42.4% of the automotive chip market share in 2024, while ≤10 nm nodes are expected to grow at 19.4% CAGR through 2030.

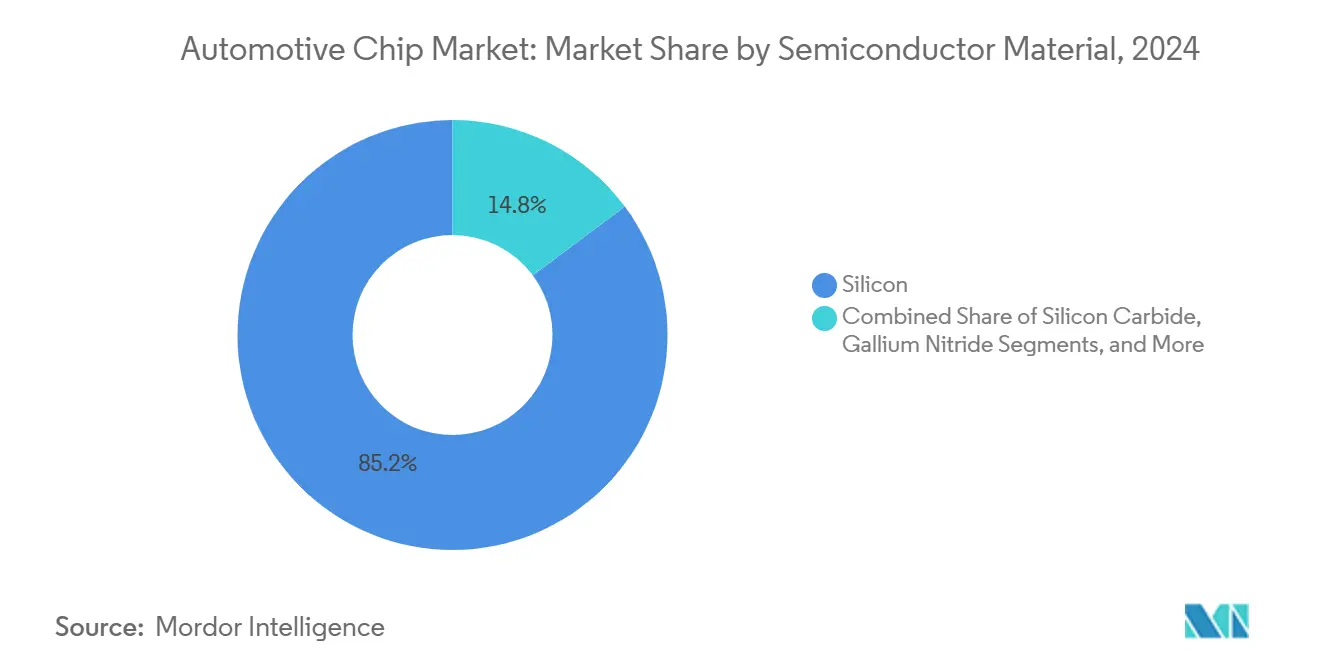

- By semiconductor material, Silicon accounted for 85.2% of sales in 2024; Silicon Carbide is forecast to rise at a 31.5% CAGR during 2025-2030.

- By propulsion type, ICE vehicles commanded 57.1% of the automotive chip market size in 2024; BEVs are set to advance at 15.5% CAGR to 2030.

- By vehicle class, Passenger Cars captured 71.3% share in 2024, whereas Heavy Commercial Vehicles should register an 11.2% CAGR to 2030.

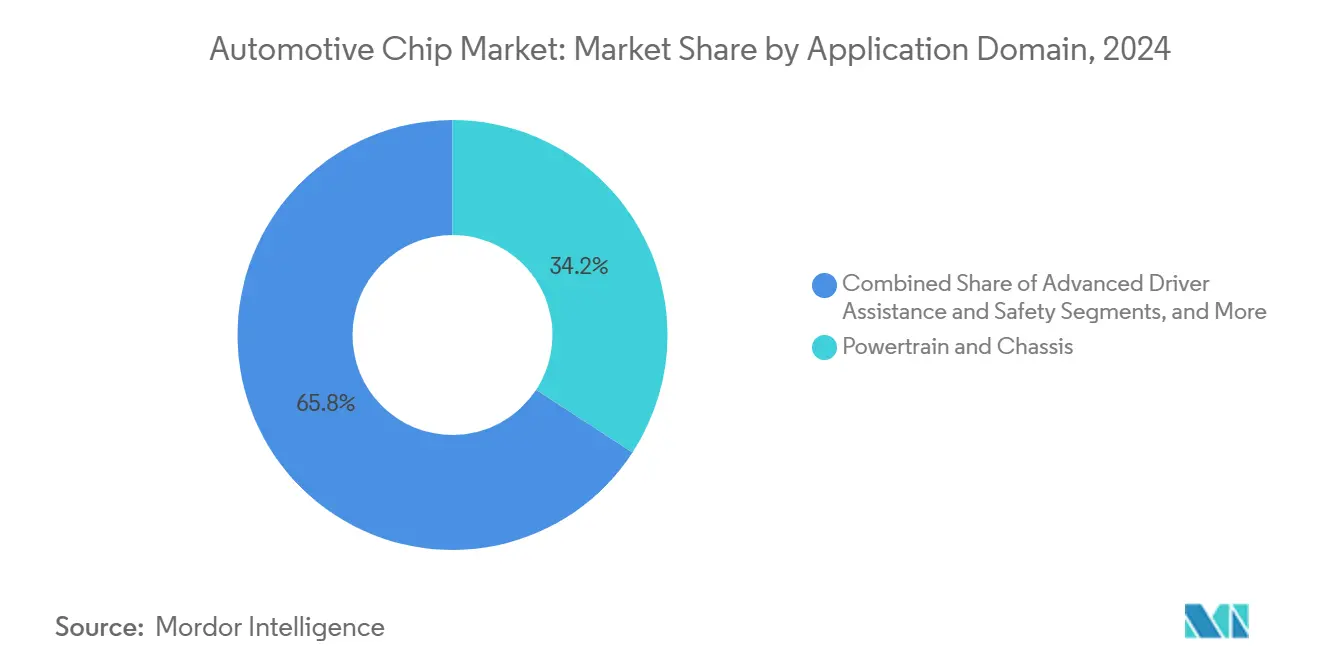

- By application domain, Powertrain and Chassis comprised 34.2% of sales in 2024; Battery Management Systems are predicted to post a 17.4% CAGR through 2030.

- By geography, Asia-Pacific dominated with a 46.2% share in 2024; the Middle East and Africa region is poised for a 13.8% CAGR between 2025 and 2030.

Global Automotive Chip Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating Transition to Software-Defined and Zonal E-Architectures Led by Europe | +2.3% | Europe, North America, with spillover to Asia-Pacific | Medium term (2-4 years) |

| Rapid Adoption of SiC and GaN Power Devices in High-Voltage EV Platforms (China-centric) | +1.8% | China, followed by Europe and North America | Medium term (2-4 years) |

| OEM Push for 4-nm/5-nm Automotive SoCs to Enable L3+ ADAS Features | +1.5% | Global, with early adoption in North America and Europe | Long term (≥ 4 years) |

| Government-Mandated Cyber-Security/OTA Standards (WP.29, UNECE R155/R156) Raising Silicon Content | +1.2% | Europe, North America, Japan, South Korea | Short term (≤ 2 years) |

| Battery Cost Parity Accelerating BEV Penetration in South America | +0.9% | South America, with Brazil and Argentina leading | Medium term (2-4 years) |

| Chiplet-Based Modular Designs Shortening Time-to-Market for Tier-1s | +0.7% | Global, with North America and Europe leading adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating Transition to Software-Defined and Zonal E-Architectures

European brands adopted zonal layouts that cut up to 20% of harness weight and replaced 70-100 ECUs with 5-10 zone controllers linked to a central computer. Mercedes-Benz confirmed the fleet-wide rollout of its MB.OS backbone by 2026. Texas Instruments introduced smart power-distribution chips that combined local intelligence with solid-state fusing for each zone, improving fault isolation and power efficiency. The re-architecture demanded gigabit Ethernet and PCIe links, pushing automotive Ethernet toward a 25% CAGR. As zonal designs matured, over-the-air updates became standard, locking in higher flash, DRAM, and network-processor content per vehicle.

Rapid Adoption of SiC and GaN Power Devices in High-Voltage EV Platforms

Silicon Carbide inverters held 28% of the BEV market in 2023 and are on track to top 50% by 2035. Chinese makers led deployment; NIO’s ET7 sedan used a 180 kW SiC module that cut conduction losses by 50% against silicon IGBT designs. Wolfspeed expanded 200 mm SiC wafer capacity to meet rising traction-inverter demand. Gallium Nitride followed a parallel path in onboard chargers and DC-DC converters, with Navitas devices shrinking charger volume by 50% and tripling power density. Widening use of wide-bandgap materials improved driving range, enabled faster charging, and accelerated the automotive chip market’s shift toward power semiconductors with higher average selling prices.

OEM Push for 4 nm/5 nm Automotive SoCs to Enable L3+ ADAS Features

Automakers migrated compute-heavy ADAS workloads to ≤10 nm nodes. TSMC released N4AE and N3AE platforms tailored for 15-year automotive lifecycles. NXP taped out 5 nm vehicle CPUs whose first production lots shipped in 2025. Ambarella’s CV3 domain controller delivered 500 TOPS of AI throughput on an advanced node while meeting AEC-Q100 Grade 2 requirements. Performance gains of 15x versus 16 nm predecessors supported real-time sensor fusion for Level 3+ autonomy, cementing the business case for advanced lithography in the automotive chip market.

Government-Mandated Cyber-Security and OTA Standards

UNECE R155 and R156 became mandatory for all new vehicle types in July 2024, compelling automakers to embed hardware security modules and trusted-execution environments in every central processor. The compliance cost added USD 45-60 of silicon per vehicle and pushed security chip shipments up 30% year over year. Keysight’s SA8710A automated security-testing platform shortened validation cycles, while NXP shipped firewalled CAN-FD transceivers with built-in encryption keys. Cybersecurity’s new status as a type-approval prerequisite permanently raised baseline semiconductor content.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic 28-45 nm Foundry Capacity Bottlenecks Despite New Fab Announcements | -1.2% | Global, with a severe impact in Asia-Pacific | Medium term (2-4 years) |

| Functional-Safety (ISO 26262/ASIL-D) Certification Costs Burdening Mid-Tier Suppliers | -0.8% | Global, with higher impact in Europe and North America | Short term (≤ 2 years) |

| Limited Thermal Management Headroom in 3-D Packaging for In-Cabin Domains | -0.6% | Global | Long term (≥ 4 years) |

| Export-Control Restrictions on EDA/IP for Chinese OEMs | -0.5% | China, with spillover effects in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Chronic 28-45 nm Foundry Capacity Bottlenecks

Microcontrollers, power-management ICs, and analog front ends relied on mature 28-45 nm processes that delivered proven reliability at lower mask costs. These nodes represented 42.4% of 2024 automotive wafer starts, yet lead times stretched to 26 weeks as industrial and IoT buyers competed for the same capacity. SEMI reported 18 new fabs breaking ground in 2025, but most targeted ≤7 nm technologies, leaving the supply gap at mature geometries unresolved. OEMs responded with buffer inventories and dual sourcing, but the imbalance continued to clip near-term growth.

Export-Control Restrictions on EDA/IP for Chinese OEMs

U.S. export rules limited Chinese automakers’ access to advanced EDA suites and IP blocks. BYD accelerated domestic chip development, yet verification flows lagged industry best practice, slowing time-to-market. The restrictions spurred China’s USD 150 billion self-sufficiency program, but the parallel ecosystem raised integration risks and threatened cross-border compatibility. Tier-1 suppliers diversified design centers to circumvent licensing hurdles, adding cost and complexity to programs targeting Chinese production.

Segment Analysis

By Component: Microcontrollers Anchor the Zonal Era

Microcontrollers and Microprocessors generated 29.1% of 2024 revenue and formed the backbone of every major vehicle domain. Premium cars carried up to 100 MCUs, while mass-market models averaged 30-50. As zonal architectures condensed functions, designers specified higher-performance 32-bit MCUs with functional-safety hardware, concentrating value even as unit counts fell. Sensors grew at a 13.2% CAGR due to the spread of radar, vision, and LiDAR suites. Continental’s integration of Ambarella AI SoCs boosted image-processing efficiency and reduced camera module footprint.[2]Ambarella, “Continental Is Latest Ambarella AI System-on-Chip Customer,” insideautonomousvehicles.com Power-management ICs, discrete power devices, and memory followed as supporting cast, each benefiting from electrification and richer infotainment payloads.

Rising silicon complexity doubled embedded flash density inside MCUs, pushing suppliers toward split-gate and MRAM solutions. Discrete power transistors shifted to 750 V SiC MOSFETs, enabling traction inverters with 98% efficiency. Network IC demand rose with gigabit Ethernet backbones and CAN-XL gateways that bridged zonal domains. The automotive chip market continued to favor component suppliers able to bundle software libraries and safety toolchains, shortening OEM development cycles.

By Fabrication Node: Mature Geometry Resilience Meets Advanced Node Surge

The 23-45 nm class owned 42.4% of 2024 revenue thanks to decades of field reliability and cost advantages for mixed-signal integration. Microcontrollers for body and comfort domains remained on 40 nm FLASH. Yet the market’s fastest growth stemmed from ≤10 nm wafers, which climbed at a 19.4% CAGR as automakers deployed multi-sensor ADAS stacks requiring hundreds of TOPS. TSMC’s N4AE line qualified in 2024 and opened volume in 2025, bringing automotive yields to parity with consumer products. The 11-22 nm tier served digital instrument clusters and service gateways, balancing cost and scalability.

Production at nodes finer than 10 nm required back-side power delivery and advanced-packaging reliability at 175 °C junction temperatures. Foundries invested in automotive-grade cleanroom flows, but capacity remained modest relative to smartphone demand. Consequently, design wins centered on high-margin flagship models first, then cascaded to volume segments as wafer supply improved.

By Semiconductor Material: Silicon Rules While SiC Transforms Power

Conventional silicon captured 85.2% of sales in 2024 owing to its mature ecosystem and broad applicability. However, Silicon Carbide climbed at a 31.5% CAGR as automakers specified 800 V drivetrains that demanded wide-bandgap efficiency. Infineon’s CoolSiC modules delivered 5-10% range gains for several Chinese EVs. Gallium Nitride followed in fast chargers, trimming board space and shrinking thermal systems. Silicon Germanium and Gallium Arsenide filled RF and radar niches, while emerging diamond substrates remained in R&D. By 2035, SiC is forecast to hold half of automotive power-device revenue, permanently altering the supply base and raising ASPs across the automotive chip market.

By Propulsion Type: Electrification Shifts Value Toward Power Devices

ICE platforms still generated 57.1% of 2024 semiconductor spend, but BEVs advanced at a 15.5% CAGR. BEV designs averaged USD 1,200 of silicon versus USD 600 for ICE, driven by traction inverters, battery management, and thermal-propulsion integration. Hybrids bridged the gap, combining dual 400 V and 12 V power nets with regenerative-braking controllers. Fuel-cell buses piloted in Asia and Europe adopted SiC DC-DC converters and isolation monitors to manage 600 V stacks. As battery parity spread to South America, regional OEMs accelerated fully electric lineups, further tilting the automotive chip market toward power and control silicon.

By Vehicle Class: Passenger Cars Dominate but Heavy Trucks Accelerate

Passenger cars produced 71.3% of 2024 sales owing to high build volumes and rapid feature adoption. Yet heavy commercial vehicles posted the best outlook at 11.2% CAGR as fleets pursued electrification, platooning, and over-the-air diagnostics. Electric buses integrated 350 kW SiC inverters and domain controllers with ISO 26262 ASIL-D certification. Light commercial vans adopted wireless BMS systems that trimmed harness weight for last-mile delivery. Rising regulatory pressure on freight emissions in Europe and North America guaranteed a steady pipeline of semiconductor upgrades throughout the segment’s long service life.

By Application Domain: Powertrain and Chassis Lead, BMS Rises Fastest

Powertrain and Chassis functions claimed 34.2% of 2024 revenue, spanning engine control, traction inverter gating, suspension actuation, and brake-by-wire. Electrification elevated inverter ASPs and introduced SiC gate drivers with Kelvin-source layouts for fast switching. Battery Management Systems grew at a 17.4% CAGR through 2030. Tesla’s predictive BMS used cell-level impedance tracking, while General Motors applied wireless sensing to its Ultium pack, lowering wiring mass and improving assembly yield. ADAS and Safety held second place, with radar, camera, and LiDAR fusing into domain controllers. Body electronics added zonal power switches and ambient lighting drivers, whereas infotainment expanded DRAM footprints to support streaming media and gaming.

By End-Market: Factory-Fit Dominance

OEM installations represented more than 90% of the value, as core vehicle functions could not be retrofitted easily. Over-the-air feature unlocks pushed hardware standardization even further, letting automakers sell software options without additional modules. Aftermarket demand concentrated on fleet telematics and infotainment, areas where modularity and cost drove independent upgrades. As software-defined platforms matured, suppliers generated additional lifetime revenue through feature subscriptions rather than replacement hardware, reshaping traditional accessory channels.

Geography Analysis

Asia-Pacific secured a 46.2% share in 2024, propelled by China’s leadership in electric-vehicle output and aggressive semiconductor self-reliance spending above USD 150 billion. BYD, NIO, and XPENG integrated in-house power devices, while Taiwanese foundries produced the most advanced automotive wafers under 10 nm. Japan preserved its strength in power electronics, and South Korea leveraged Samsung’s memory and application-processor ecosystems. India’s domestic production ramped quickly, lifting semiconductor value per locally built car at 14% annually.

Europe ranked second by revenue, driven by premium OEMs that pioneered zonal architectures and Level 3 autonomy. The European Chips Act earmarked EUR 43 billion (USD 48.6 billion) for local fabs to double the region’s global share to 20% by 2030.[3]Polish Investment and Trade Agency, “Achievements and Prospects of the Semiconductor Manufacturing Industry in Poland 2024,” paih.gov.pl Germany led demand, with CARIAD locking long-term wafer agreements. France advanced GaN epitaxy, and Intel invested USD 4.6 billion in Polish test facilities. Stringent cyber and emission rules pushed per-vehicle silicon spend above global averages.

North America combined world-class chip design with accelerating EV programs. The USD 52 billion CHIPS Act improved access to local capacity for automotive-grade nodes. General Motors and Ford scaled Ultium and Model e platforms, embedding silicon-rich battery packs and domain computers. Tesla maintained a vertically integrated stack that inspired other OEMs to pursue custom silicon. Canada and Mexico supplied robust assembly footprints, attracting chip module makers.

The Middle East and Africa, although the smallest today, enjoyed the fastest forecast CAGR at 13.8%. Morocco’s export-oriented auto plants adopted ADAS and connectivity features, and South Africa incentivized local electronics sourcing. GCC states funded R&D centers for power devices suited to extreme climates. South America benefited from battery cost parity; Brazil and Argentina rolled out BEV incentives, lifting semiconductor content despite economic headwinds.

Competitive Landscape

Five suppliers—Infineon, NXP, STMicroelectronics, Texas Instruments, and Renesas—held the majority of the 2024 revenue. Scale, stringent AEC-Q qualification records, and software ecosystems created high barriers to entry. Infineon acquired Marvell’s Automotive Ethernet unit for USD 2.5 billion in April 2025 to secure a foothold in zonal backbones. NXP followed with the USD 625 million purchase of TTTech Auto, adding deterministic middleware to its CoreRide portfolio.

Competition intensified around wide-bandgap power and AI accelerators. Wolfspeed scaled 200 mm SiC wafers, onsemi expanded trench SiC lines, and newcomers such as Navitas targeted GaN chargers. In compute, Ambarella, Mobileye, and Qualcomm vied to supply 500 TOPS domain controllers. Automakers increased vertical integration: Tesla designed Dojo inference chips, and BYD introduced traction-inverter control ICs. These moves pressured Tier-1s to offer full-stack solutions that blended hardware, firmware, and security certification.

Supplier strategies shifted toward multi-die packaging and reference platforms that cut system cost and time-to-market. Texas Instruments sampled chiplet-based zone controllers, while STMicroelectronics partnered with GlobalFoundries on radar SoCs with embedded phase-array antennas.[4]GlobalFoundries, “indie Semiconductor and GlobalFoundries Announce Strategic Collaboration to Accelerate Automotive Radar Adoption,” gf.com As the market gravitated to centralized compute, players able to deliver scalable silicon and software roadmaps secured design wins that extended through the decade.

Automotive Chip Industry Leaders

Infineon Technologies AG

NXP Semiconductors N.V.

Renesas Electronics Corp.

STMicroelectronics N.V.

Texas Instruments Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: TSMC advanced customers from N7A/N5A to N3A nodes for ADAS computing.

- April 2025: LG and Ambarella launched an in-cabin safety platform using the CV25 SoC.

- April 2025: Infineon Technologies acquired Marvell Technology’s Automotive Ethernet business for USD 2.5 billion, adding USD 225-250 million revenue at 60% gross margin.

- March 2025: GlobalFoundries and Indie Semiconductor formed a radar-focused development pact.

Global Automotive Chip Market Report Scope

Automotive chips are specialized integrated circuits tailored for vehicles. These chips are integral to modern automobiles, managing engine control, safety features, and infotainment systems. They oversee critical functions, including fuel injection, anti-lock braking (ABS), airbag deployment, navigation, and entertainment. With technological advancements, these chips have evolved, now supporting features like autonomous driving, enhanced connectivity, and advanced safety measures. The study tracks the revenue generated from selling several components utilized for several applications in automotive manufacturing. It also tracks the growing market trends and macroeconomic factors impacting the market.

The automotive chip market is segmented by component (microprocessor and microcontroller, integrated circuits, discrete power devices, sensors, memory devices, other components), vehicle type (passenger vehicles and commercial vehicles), application (powertrain and chassis, safety and security, body electronics, telematics and infotainment Systems, others), and geography (North America, Europe, Asia Pacific, Latin America, Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Microcontrollers and Microprocessors |

| Power Management and Driver ICs |

| Discrete Power Devices (IGBT, MOSFET, SiC, GaN) |

| Sensors (Image, LiDAR, Radar, MEMS) |

| Memory (DRAM, NAND, NOR) |

| Connectivity and Network ICs (Ethernet, CAN-FD, LIN, FlexRay) |

| Others (Clock, Analog Front-Ends, Interface) |

| ≤ 10 nm |

| 11 – 22 nm |

| 23 – 45 nm |

| > 45 nm |

| Silicon (Si) |

| Silicon Carbide (SiC) |

| Gallium Nitride (GaN) |

| Others (SiGe, GaAs, SOS) |

| Internal Combustion Engine (ICE) Vehicles |

| Hybrid and Plug-in Hybrid Electric Vehicles (HEV/PHEV) |

| Battery Electric Vehicles (BEV) |

| Fuel-Cell Electric Vehicles (FCEV) |

| Passenger Cars |

| Light Commercial Vehicles (LCV) |

| Heavy Commercial Vehicles (HCV and Buses) |

| Powertrain and Chassis |

| Advanced Driver Assistance and Safety |

| Body, Comfort and Convenience |

| Telematics, Infotainment and Connectivity |

| Battery Management Systems (BMS) |

| OEM-Installed (Factory-Fit) |

| Aftermarket Retro-Fit |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Component | Microcontrollers and Microprocessors | ||

| Power Management and Driver ICs | |||

| Discrete Power Devices (IGBT, MOSFET, SiC, GaN) | |||

| Sensors (Image, LiDAR, Radar, MEMS) | |||

| Memory (DRAM, NAND, NOR) | |||

| Connectivity and Network ICs (Ethernet, CAN-FD, LIN, FlexRay) | |||

| Others (Clock, Analog Front-Ends, Interface) | |||

| By Fabrication Node | ≤ 10 nm | ||

| 11 – 22 nm | |||

| 23 – 45 nm | |||

| > 45 nm | |||

| By Semiconductor Material | Silicon (Si) | ||

| Silicon Carbide (SiC) | |||

| Gallium Nitride (GaN) | |||

| Others (SiGe, GaAs, SOS) | |||

| By Propulsion Type | Internal Combustion Engine (ICE) Vehicles | ||

| Hybrid and Plug-in Hybrid Electric Vehicles (HEV/PHEV) | |||

| Battery Electric Vehicles (BEV) | |||

| Fuel-Cell Electric Vehicles (FCEV) | |||

| By Vehicle Class | Passenger Cars | ||

| Light Commercial Vehicles (LCV) | |||

| Heavy Commercial Vehicles (HCV and Buses) | |||

| By Application Domain | Powertrain and Chassis | ||

| Advanced Driver Assistance and Safety | |||

| Body, Comfort and Convenience | |||

| Telematics, Infotainment and Connectivity | |||

| Battery Management Systems (BMS) | |||

| By End-Market | OEM-Installed (Factory-Fit) | ||

| Aftermarket Retro-Fit | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| France | |||

| United Kingdom | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the automotive chip market?

The market totaled USD 68.41 billion in 2025 and is projected to grow to USD 107.67 billion by 2030.

Which component segment holds the largest revenue share?

Microcontrollers and Microprocessors led with 29.1% revenue share in 2024.

Why are Silicon Carbide devices gaining traction?

SiC inverters improve electric-vehicle range by 5-10% and are forecast to rise at a 31.5% CAGR through 2030.

Which region will grow fastest between 2025 and 2030?

The Middle East and Africa region is expected to post the highest CAGR at 13.8%.

How are zonal architectures influencing semiconductor demand?

They replace tens of ECUs with a handful of zone controllers and a central computer, boosting demand for high-performance processors and gigabit networking chips.

What is driving the move to ≤10 nm automotive SoCs?

Level 3+ autonomous features require hundreds of TOPS of processing, achievable only on advanced nodes that cut power by 30% and raise performance by 15x.