Automotive Carbon Fiber Composites Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

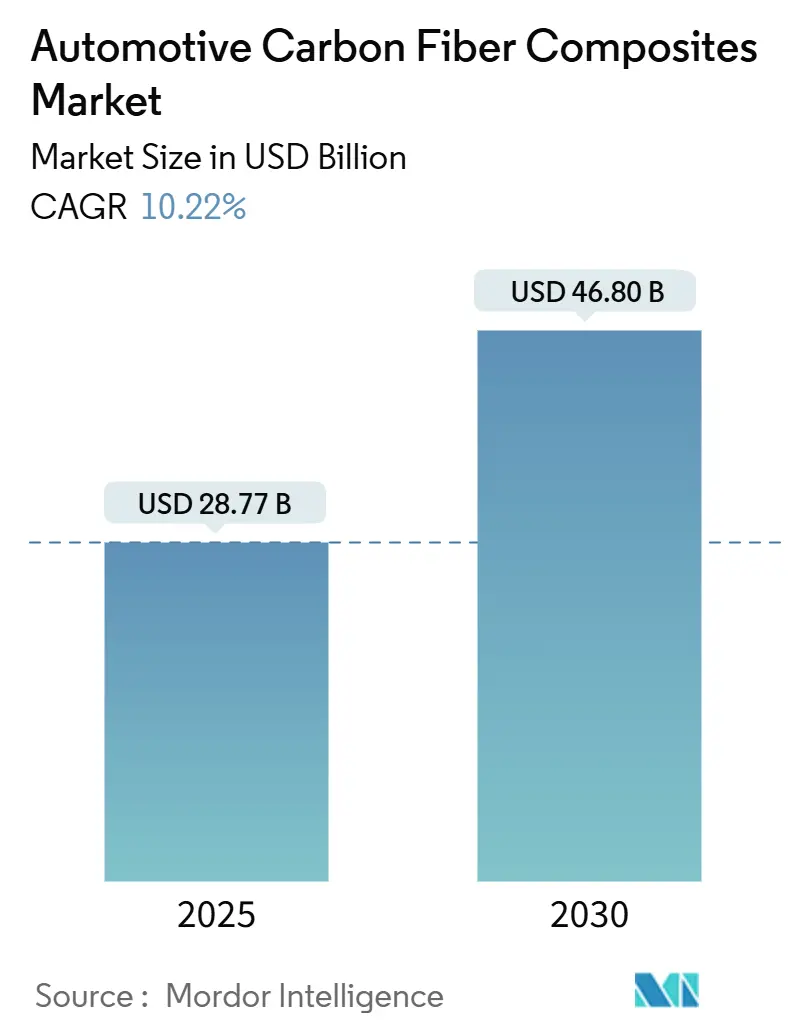

| Market Size (2025) | USD 28.77 Billion |

| Market Size (2030) | USD 46.80 Billion |

| Growth Rate (2025 - 2030) | 10.22% CAGR |

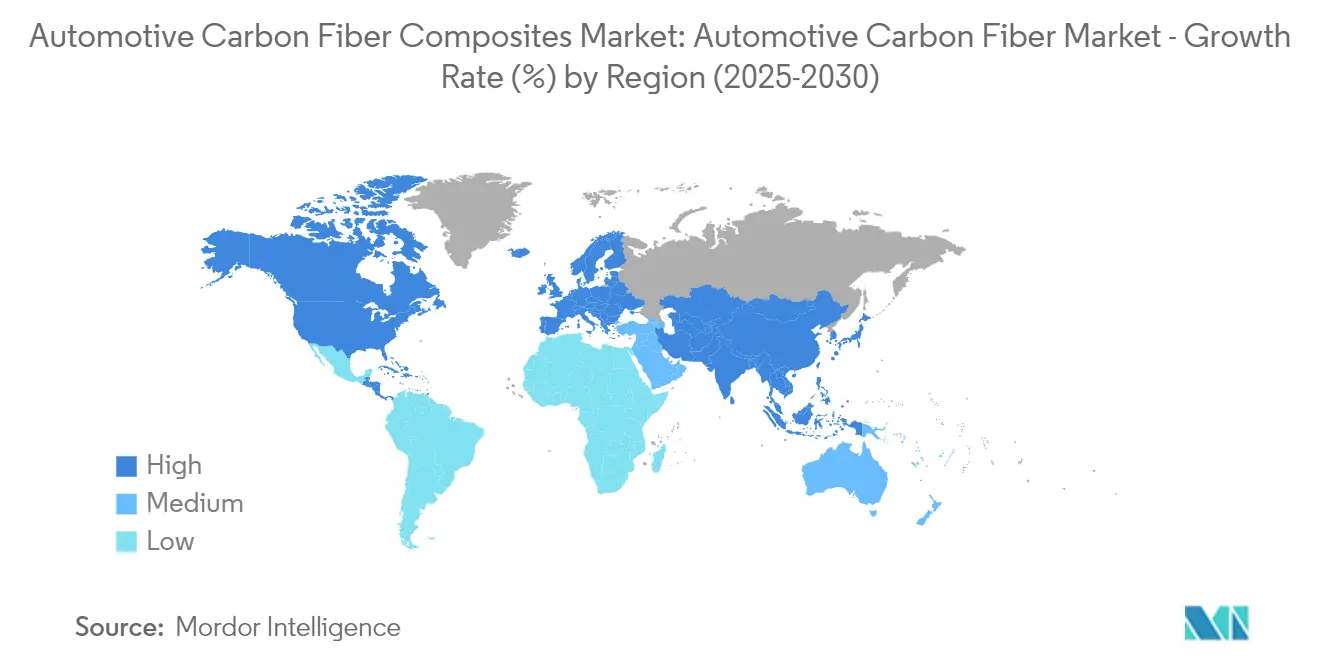

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

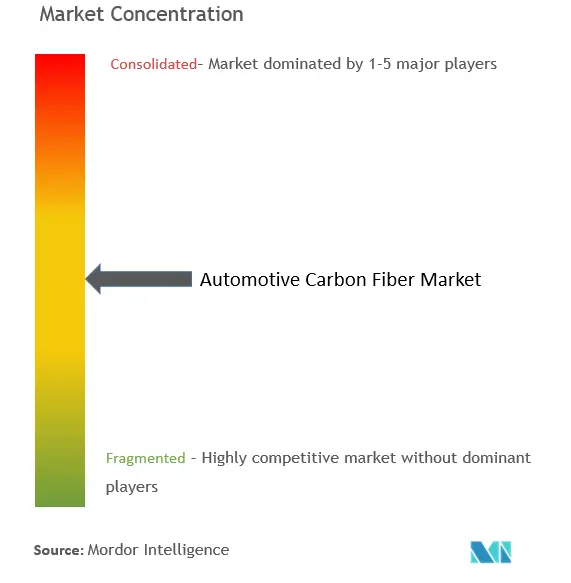

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Carbon Fiber Composites Market Analysis by Mordor Intelligence

The Automotive Carbon Fiber Composites Market size is estimated at USD 28.77 billion in 2025, and is expected to reach USD 46.80 billion by 2030, at a CAGR of 10.22% during the forecast period (2025-2030).

Carbon fiber composites are revolutionizing the automotive industry, offering benefits like lightweight construction, better fuel efficiency, superior performance, and design flexibility. These advantages have made carbon fiber a favored choice among automotive manufacturers aiming to produce high-performance, lightweight vehicles.

As the automotive industry increasingly demands lightweight materials and prioritizes fuel economy, carbon fiber's popularity surges. With tightening emission regulations and escalating fuel prices, carbon fiber emerges as a superior alternative to traditional metals, significantly reducing vehicle weight. This not only boosts fuel efficiency and engine performance but also boasts a physical strength nearly double that of conventional metals.

Leading carbon fiber suppliers are aligning with the aspirations of vehicle OEMs, system suppliers, and end-users to produce lighter, cleaner, safer, and more cost-effective vehicles. Major automakers, including BMW, Audi, GM, and Honda, are forging partnerships with carbon fiber producers for mass production, channeling investments into processes that promise cost-effective carbon fiber manufacturing. For instance,

- In April 2024, Hyundai Motor Group inked a strategic cooperation deal with Toray Industries, Inc., a frontrunner in carbon fiber and composite technology. This collaboration aims to harness advanced materials, particularly carbon fiber, to bolster the performance and safety of future mobility solutions.

Yet, the intricate manufacturing processes of carbon fiber drive up costs, hindering widespread adoption. Additionally, the lack of a robust recycling infrastructure for carbon fiber raises environmental concerns due to potential waste accumulation. Such challenges could stifle market growth, especially since integrating carbon fiber into budget vehicles could significantly inflate their prices.

With the global surge in electric vehicle demand, carbon fiber's role in extending EV range becomes pivotal, suggesting a robust market growth trajectory in the coming years.

Global Automotive Carbon Fiber Composites Market Trends and Insights

Passenger Cars Dominate the Automotive Carbon Fiber Market

- Passenger cars are experiencing significant growth globally, driven by increasing urbanization, evolving consumer preferences for affordable personal transportation, and the rising adoption of electric vehicles. To meet government fuel efficiency standards, automakers are prioritizing the use of lightweight materials like carbon fiber to reduce fuel consumption.

- Advanced materials such as carbon fiber are critical for improving the fuel efficiency of modern vehicles while maintaining safety and performance. Lightweight materials are essential for optimizing vehicle efficiency, as less energy is required to accelerate lighter objects. For instance, reducing a vehicle's weight by 10% can result in a 6-8% improvement in fuel economy.

- As exhaust emissions raise environmental concerns, the demand for high-performance electric vehicles has surged. This momentum is bolstered by stringent regulations on emissions and fuel economy, alongside government initiatives like subsidies and incentives promoting the shift to electrification. For instance,

- The UK government has announced its intention to reduce CO2 emissions by 68% by 2030 as part of its climate change strategy and has set a ban on gasoline and diesel cars starting in 2030.

- Carbon fiber's importance in electric vehicles lies in its ability to enhance driving range. Given that electric vehicles rely heavily on battery life, reducing vehicle weight with carbon fiber decreases energy consumption, enabling longer travel distances on a single charge. These benefits are expected to drive the demand for carbon fiber composites in electric vehicle design.

- Furthermore, numerous automakers are channeling efforts into crafting lightweight electric vehicles, harnessing advanced materials like carbon fiber for peak performance. For instance,

- In September 2024, Lotus unveiled its ultra-luxury electric hyper-SUV variant, the Eletre Carbon, in North America. This model features an extensive carbon fiber design both inside and out, marking the debut of Lotus's new performance SUV lineage.

- Given these dynamics, the demand for Automotive Carbon Fiber Composites Market in passenger cars is set to witness significant growth in the coming years.

Asia-Pacific Anticipated to Lead the Automotive Carbon Fiber Market

- The Asia-Pacific region is experiencing significant growth in the automotive carbon fiber market, driven by its strong automotive industry, rapid industrial expansion, and the increasing adoption of lightweight materials to enhance fuel efficiency and reduce emissions, particularly with the growing popularity of electric vehicles.

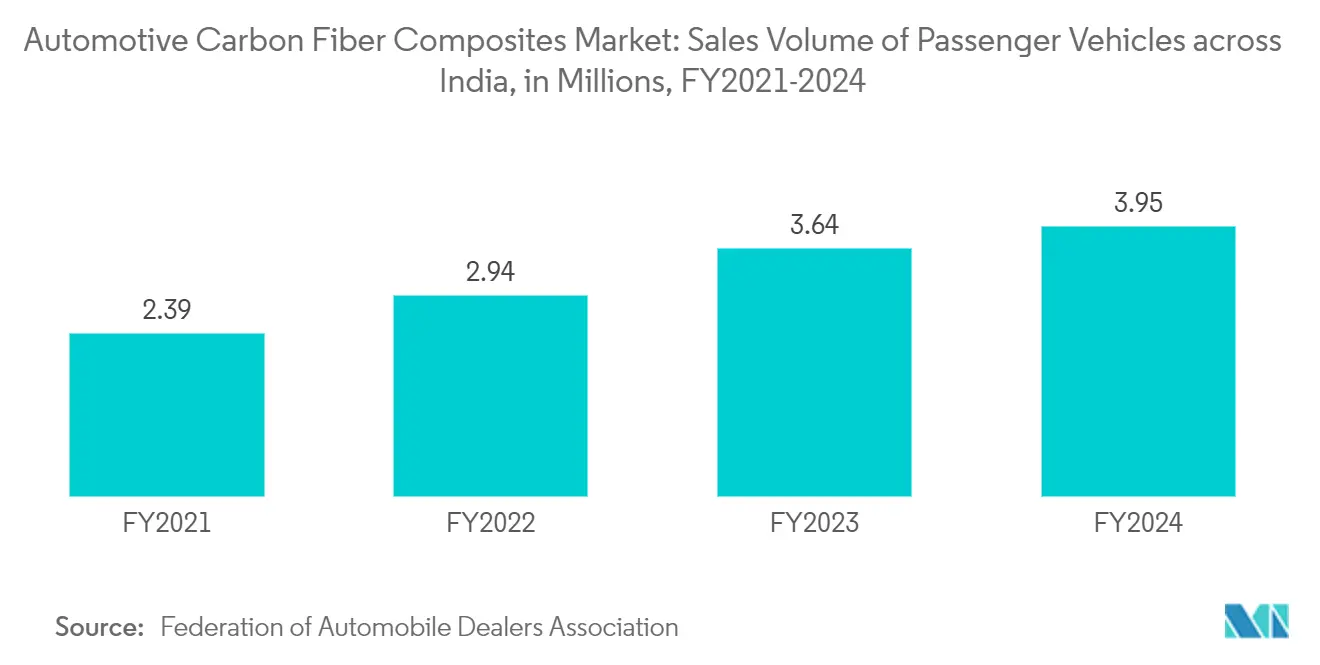

- According to the China Association of Automobile Manufacturers (CAAM), in 2024, China set new records by producing 31.28 million and selling 31.44 million vehicles, marking year-on-year increases of 3.7% and 4.5%, and surpassing the 30 million unit threshold for the second consecutive year.

- Stringent government regulations on vehicle emissions are catalyzing a shift towards eco-friendly vehicles in the region. Given that vehicle weight significantly influences fuel consumption, automakers are increasingly turning to lightweight materials like carbon fiber to enhance fuel efficiency. For instance,

- China's Ministry of Ecology and Environment (MEE) has proposed a policy aiming for electric vehicles (EVs) to constitute 50% of all vehicle sales by 2030 in "key polluting regions," underscoring a targeted effort to curb emissions in areas grappling with severe air pollution.

- Additionally, nations like Japan and South Korea are carving out a competitive edge in carbon fiber production and processing. Furthermore, heightened R&D initiatives by chemical firms to craft advanced composite materials for automotive uses are poised to bolster the carbon fiber market. For instance,

- In April 2024, UBE Corporation, a Japan-based chemicals firm, unveiled a new composite product aimed at curbing greenhouse gas emissions. By integrating recycled carbon fiber with various nylons and enhancing functionalities, UBE's innovation targets automotive and sports markets, emphasizing energy conservation through weight reduction.

- Given the mounting emphasis on sustainable mobility, rigorous emissions regulations, and the surging demand for lightweight materials in the automotive sector, the Asia-Pacific region is set to lead the Automotive Carbon Fiber Composites Market in the coming years.

Competitive Landscape

Several key players, including Hexcel Corporation, Mitsubishi Chemical Group, Teijin Limited, Toray Industries Inc., and SGL Carbon SE, dominate the Automotive Carbon Fiber Composites Market, which is moderately consolidated. Demand remains robust, driven by aggressive expansion and growth strategies from leading carbon fiber manufacturers. For instance,

In March 2024, Mitsubishi Chemical Group unveiled its BiOpreg #400 series, a carbon fiber prepreg material crafted from plant-derived resin. This innovative fiber targets mobility applications, specifically for both interior and exterior automotive materials, as well as broader industrial uses.

Automotive Carbon Fiber Composites Industry Leaders

Toray Industries Inc.

Hexcel Corporation

SGL Carbon SE

Teijin Limited

Mitsubishi Chemical Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: McLaren has unveiled a groundbreaking carbon fiber manufacturing technique, dubbed Automated Rapid Tape (ART) carbon, by repurposing a method from the aerospace sector for its supercars. This innovative approach automates the application of dry composite tape, ensuring precise fiber placement and enhancing the strength-to-weight ratio. The McLaren W1 will be the inaugural model to showcase this technology, with intentions to integrate it into upcoming supercar models.

- March 2025: Mercedes has revealed that their 2025 model, the W16, will pioneer the use of sustainable carbon fiber composites in Formula 1. Given that carbon fiber composites constitute about 75% of the materials in their race cars, bolstering both performance and safety, these advancements present a prime opportunity to curtail the car's carbon footprint.

Global Automotive Carbon Fiber Composites Market Report Scope

In the automotive industry, "carbon fiber" refers to a composite material composed of strong, lightweight carbon fibers that are woven together and reinforced with a resin or polymer. This material is utilized in various vehicle components to reduce weight while preserving structural integrity.

The Automotive Carbon Fiber Composites Market is segmented by application, vehicle type, propulsion, and geography. By application, the market is segmented into structural assembly, powertrain components, interiors, and exteriors. By vehicle type, the market is segmented into passenger cars and commercial vehicles. By propulsion, the market is segmented into internal combustion engines, battery electric vehicles, hybrid electric vehicles, plug-in hybrid electric vehicles, and fuel cell electric vehicles. By geography, the market is segmented into North America, Europe, Asia-Pacific, and Rest of the World. For each segment, the market sizing and forecast have been done based on the value (USD).

| Structural Assembly |

| Powertrain Components |

| Interiors |

| Exteriors |

| Passenger Car |

| Commercial Vehicle |

| Internal Combustion Engine |

| Battery Electric Vehicles |

| Hybrid Electric Vehicles |

| Plug-in Hybrid Electric Vehicles |

| Fuel Cell Electric Vehicles |

| North America | United States |

| Canada | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Rest of the World | South America |

| Middle East and Africa |

| By Application | Structural Assembly | |

| Powertrain Components | ||

| Interiors | ||

| Exteriors | ||

| By Vehicle Type | Passenger Car | |

| Commercial Vehicle | ||

| By Propulsion | Internal Combustion Engine | |

| Battery Electric Vehicles | ||

| Hybrid Electric Vehicles | ||

| Plug-in Hybrid Electric Vehicles | ||

| Fuel Cell Electric Vehicles | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Rest of the World | South America | |

| Middle East and Africa | ||

Key Questions Answered in the Report

How big is the Automotive Carbon Fiber Composites Market?

The Automotive Carbon Fiber Composites Market size is expected to reach USD 28.77 billion in 2025 and grow at a CAGR of 10.22% to reach USD 46.80 billion by 2030.

What is the current Automotive Carbon Fiber Composites Market size?

In 2025, the Automotive Carbon Fiber Composites Market size is expected to reach USD 28.77 billion.

Who are the key players in Automotive Carbon Fiber Composites Market?

Toray Industries Inc., Hexcel Corporation, SGL Carbon SE, Teijin Limited and Mitsubishi Chemical Corporation are the major companies operating in the Automotive Carbon Fiber Composites Market.

Which is the fastest growing region in Automotive Carbon Fiber Composites Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Automotive Carbon Fiber Composites Market?

In 2025, the Asia Pacific accounts for the largest market share in Automotive Carbon Fiber Composites Market.

What years does this Automotive Carbon Fiber Composites Market cover, and what was the market size in 2024?

In 2024, the Automotive Carbon Fiber Composites Market size was estimated at USD 25.83 billion. The report covers the Automotive Carbon Fiber Composites Market historical market size for years: 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Automotive Carbon Fiber Composites Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.