| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 17.93 Billion |

| Market Size (2030) | USD 21.29 Billion |

| CAGR (2025 - 2030) | 3.50 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order |

Automotive Brake Pad Market Analysis

The Automotive Brake Pad Market size is estimated at USD 17.93 billion in 2025, and is expected to reach USD 21.29 billion by 2030, at a CAGR of 3.5% during the forecast period (2025-2030).

The automotive brake pad industry is undergoing significant transformation driven by stringent environmental regulations and technological innovations. Brake pad manufacturers are increasingly focusing on developing copper-free brake pad formulations to comply with environmental legislation, particularly in response to the European Commission's Euro 7 standards that will be implemented from July 2025. These regulations specifically target particulate matter emissions from brake pads, setting a limit of 7 mg/km for passenger cars. This regulatory push has accelerated research and development in eco-friendly materials, with companies like Hella Pagid committing to exclusively offer copper-free brake options by 2025.

The industry is witnessing substantial investments in manufacturing capabilities and technological advancement. In June 2023, ITT Inc. announced a USD 55 million expansion of its friction production facility in Italy, focusing on research and development capabilities for high-performance brake pads. This investment is expected to increase the covered area of their Termoli plant by 75% and includes the addition of rapid prototyping and automated production modules. Similarly, SGL Carbon and Brembo's joint venture announced plans to invest approximately EUR 150 million by 2027 to expand production capacities by over 70% at their facilities in Meitingen and Stezzano.

The electric vehicle revolution is reshaping brake pad requirements and design considerations. In Germany alone, electric car sales witnessed a significant surge in 2022, capturing a 17.7% share of the new car market. This shift has prompted manufacturers to develop specialized brake pad solutions that address the unique challenges of electric vehicles, including regenerative braking systems and reduced noise requirements. Continental's introduction of the Green Caliper brake system in late 2022 exemplifies this trend, featuring reduced weight and lower residual brake torque specifically designed to enhance electric vehicle range.

The commercial vehicle segment is experiencing notable technological transitions, particularly in heavy-duty applications. During the first half of 2023, diesel vehicles dominated new truck registrations with a 95.6% market share, while battery-electric trucks witnessed an extraordinary growth of 351.5%, accumulating 2,384 units. This evolution has led to innovations in brake pad materials and designs, with manufacturers developing specialized solutions for different vehicle categories. For instance, Carlisle Brake & Friction's introduction of the EL121 Disc Brake Pads in September 2023 specifically targets mine haul truck applications, offering double the service life for front-axle brake pads while maintaining optimal performance in autonomous operations.

The automotive brake components aftermarket is also experiencing growth as consumers seek high-quality replacement parts. This trend is supported by the increasing number of vehicles on the road and the demand for reliable brake pad manufacturers to supply the necessary components. A leading brake pad company, for example, has expanded its offerings to include a wider range of products to meet this growing demand.

Automotive Brake Pad Market Trends

Vehicle Sales to Fuel Automotive Brake Pad Demand

The automotive brake pad market continues to be primarily driven by robust global vehicle sales across both passenger and commercial segments. In 2022, worldwide passenger car sales reached 57.49 million units, showcasing a 1.9% year-over-year growth from 56.44 million units in 2021, while commercial vehicle sales maintained strong momentum with 24.14 million units. This sustained growth in vehicle sales directly correlates to increased demand for brake pad sales, as every new vehicle requires this essential safety component. The expansion of commercial vehicle fleets, particularly in the logistics and delivery sectors, has further amplified the need for durable and reliable vehicle brake pad systems that can withstand frequent usage and heavy loads.

The rising adoption of electric vehicles (EVs) and the subsequent need for specialized braking systems has created additional demand streams for brake pad manufacturers. This trend is evidenced by recent industry developments, such as Continental's introduction of the innovative Green Caliper brake design in November 2022, specifically engineered for electric vehicles with features like reduced weight and lower residual brake torque. The automotive industry's shift towards electric mobility has prompted manufacturers to develop brake pads with enhanced heat dissipation capabilities and improved durability, leading to increased investment in research and development for advanced braking solutions that can meet the unique requirements of electric vehicles while maintaining optimal performance standards.

Understand The Key Trends Shaping This Market

Download PDF

Increased Demand for Vehicle Safety to Fuel Brake Pad Market

Growing emphasis on vehicle safety, backed by stringent regulations and increased consumer awareness, continues to be a fundamental driver for the automotive brake pad market. This is exemplified by the National Highway Traffic Safety Administration's (NHTSA) July 2023 proposal for a new Federal Motor Vehicle Safety Standard, which would mandate automatic emergency braking systems including pedestrian AEB on light vehicles. The significance of these safety measures is underscored by NHTSA projections indicating that this proposed rule could save at least 360 lives annually and reduce injuries by at least 24,000 cases. Furthermore, studies by the Insurance Institute for Highway Safety (IIHS) have demonstrated that vehicles equipped with AEB systems experienced a 43% reduction in crashes, with injuries in these types of incidents declining by 64%.

The industry's response to these safety demands is evident in the continuous technological advancement and innovation in brake pad materials and designs. In August 2023, Totachi Industrial Co. Ltd. expanded its manufacturing capabilities to include specialized brake pads designed for diverse passenger car brands, focusing on OEM-quality standards and exceptional performance. Similarly, in March 2023, Brakes India introduced ZAP brake pads featuring advanced friction technology specifically tailored for electric vehicles, emphasizing improved corrosion protection and quieter braking performance. These developments reflect the industry's commitment to enhancing vehicle safety through improved brake pad technology, driven by both regulatory requirements and consumer expectations for higher safety standards. The automotive brake friction materials market is thus poised for significant growth as manufacturers innovate to meet these evolving demands.

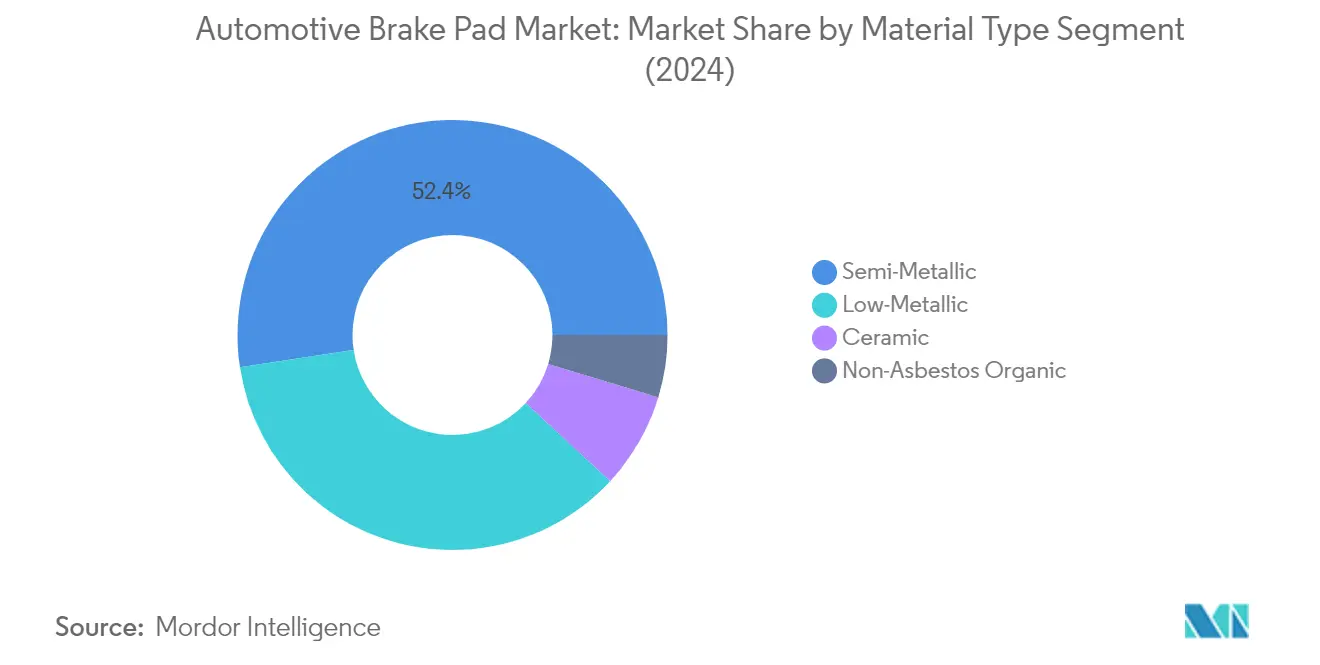

Segment Analysis: By Material Type

Semi-Metallic Segment in Automotive Brake Pad Market

The semi-metallic segment continues to dominate the automotive brake pad market, commanding approximately 52% of the total market share in 2024. This significant market position is attributed to the segment's comprehensive composition, which includes between 30% and 70% metal content, incorporating materials such as copper, iron, steel, and other composite alloys combined with graphite lubricant and additional fillers. These brake pads have established themselves as the preferred choice for both daily commuting vehicles and high-performance applications due to their exceptional durability, superior heat dissipation capabilities, and remarkable braking efficiency. The segment's strong market presence is further reinforced by its versatility in handling various driving conditions and its proven reliability in both wet and dry environments, making it particularly suitable for vehicles that require consistent performance across diverse operating conditions.

Non-Asbestos Organic Segment in Automotive Brake Pad Market

The non-asbestos organic (NAO) segment is emerging as the fastest-growing segment in the automotive brake pad market, projected to grow at approximately 4% during the forecast period 2024-2029. This growth is primarily driven by increasing environmental consciousness and the segment's eco-friendly characteristics. These brake pads, composed of fibers and materials like rubber, carbon compounds, glass, or fiberglass bound together by resin, are gaining popularity particularly in daily commuter vehicles. The segment's growth is further propelled by its advantages in minimizing dust production, generating moderate friction without excessive heat generation, and providing quieter operation compared to other variants. The increasing preference for low-speed vehicles (LSVs) and light-urban vehicles (LUVs) for shorter commutes worldwide is expected to continue driving the demand for NAO brake pads.

Remaining Segments in Material Type

The low-metallic and ceramic segments complete the automotive brake pad market's material type categorization, each serving distinct market needs. Low-metallic brake pads, incorporating 10-30% metal components, primarily copper or steel, offer an optimal balance between performance and cost, making them particularly suitable for moderate to high-performance vehicles. Meanwhile, the ceramic segment, though smaller in market share, has carved out a significant niche in the premium vehicle segment, offering superior noise reduction, minimal brake dust, and consistent performance across a wide range of temperatures. Both segments continue to evolve with technological advancements, particularly in addressing the specific requirements of electric vehicles and high-performance applications.

Segment Analysis: By Position Type

Front Segment in Automotive Brake Pad Market

The front brake pad segment maintains its dominant position in the automotive brake pad market, commanding approximately 53% market share in 2024. Front brakes play a crucial role in a vehicle's braking system, handling up to 75% of the braking load and generating significant heat, often exceeding 500°F during intense braking. With rising concerns for safety and the increasing adoption of electric vehicles (EVs) and autonomous vehicles (AVs), automakers are compelled to continuously employ advanced parts and components in their vehicle models. The implementation of a front disc braking system holds great importance as it provides superior braking control. The constant wear and tear of the frontal brake pads due to excessive pressure exerted while braking leads to surging demand for aftermarket replacement of these parts. Furthermore, increasing used vehicle sales across various countries assist the rising demand for the front brake pad market.

Rear Segment in Automotive Brake Pad Market

The rear brake pad segment is projected to experience the fastest growth rate of approximately 3.4% during the forecast period 2024-2029. Rear brakes usually endure less than 40% of the braking force, leading to reduced heat production compared to the front brakes. However, it is crucial to prioritize a top-notch rear brake system as it plays a significant role in maintaining vehicle stability and preventing rear rise during braking. Due to their limited involvement in handling braking force, the replacement interval for rear brake pads is longer when compared to front brake pads. Consequently, the cost of replacing rear brake pads is slightly more economical than their front counterparts. Due to growing safety concerns, manufacturers now recommend replacing all sets of rear brake pads simultaneously to enhance the braking performance of the vehicle.

Segment Analysis: By Sales Channel

Aftermarket Segment in Automotive Brake Pad Market

The aftermarket segment dominates the automotive brake pad market, commanding approximately 67% of the total market share in 2024. This significant market presence is primarily driven by the constant wear and tear of brake pads, especially in commercial vehicles that carry heavy loads for longer distances and in passenger cars, contributing to the substantial demand for aftermarket brake pad products for replacement or upgradation purposes. The segment's dominance is further reinforced by the increasing average age of vehicles on roads across various emerging countries, coupled with consumers' rising preference for utilizing higher-quality automotive brake pads compared to lower-priced and lower-quality imported products. Major manufacturers are actively expanding their aftermarket presence through strategic partnerships and collaborations worldwide to enhance their business performance and meet the growing demand for replacement brake pads.

OEM Segment in Automotive Brake Pad Market

The Original Equipment Manufacturer (OEM) segment is projected to experience the highest growth rate of approximately 4% during the forecast period 2024-2029. This growth trajectory is primarily driven by the increasing need of automotive manufacturers to utilize brake pads that can sustain high temperatures along with availing high-quality and high-performance friction materials. The segment's growth is further supported by substantial investments being made by different manufacturers in the development of disc brakes appropriate for the commercial vehicles sector. Additionally, the rising demand for advanced and eco-friendly brake pad products, coupled with stringent safety regulations and the growing electric vehicle market, is expected to fuel the OEM segment's expansion. Manufacturers are increasingly focusing on developing innovative materials and technologies to meet the specific requirements of electric and autonomous vehicles, further accelerating the segment's growth momentum.

Segment Analysis: By Vehicle Type

Passenger Car Segment in Automotive Brake Pad Market

The passenger car segment continues to dominate the automotive brake pad market, commanding approximately 68% of the market share in 2024. This segment's prominence is driven by the increasing adoption of electric vehicles across emerging economies and the rising demand for advanced automotive brake pad products with enhanced durability and superior heat dissipation capabilities. The segment is also experiencing the fastest growth trajectory, projected to grow at around 3% during 2024-2029, primarily due to stringent government safety regulations related to vehicle components and the phasing out of low-quality imported products. The growth is further supported by various brake pad manufacturers strategizing to expand their brake pad coverage to cater to all passenger cars, with companies like TOTACHI INDUSTRIAL CO., LTD. initiating new manufacturing facilities for passenger car brake pads. Additionally, the increasing focus on electric vehicle safety systems and the integration of advanced braking technologies in modern passenger vehicles are contributing significantly to the segment's market leadership.

Commercial Vehicle Segment in Automotive Brake Pad Market

The commercial vehicle segment represents a vital component of the automotive brake pad market, characterized by unique requirements for enhanced durability and longer-lasting performance due to the vehicles' heavy-duty applications and longer travel distances. The segment has witnessed significant developments in brake pad technology, particularly in addressing the specific needs of heavy-duty trucks, buses, and delivery vehicles. Manufacturers are increasingly focusing on developing specialized brake pad solutions that can withstand higher temperatures and provide superior braking performance under heavy loads. The segment has also seen notable innovations in materials and design, with companies introducing copper-free brake pads and advanced friction materials specifically engineered for commercial applications. The rise of e-commerce and delivery services has further intensified the demand for reliable braking systems in commercial vehicles, while the increasing adoption of electric commercial vehicles has sparked new developments in brake pad technology to accommodate their unique requirements.

Automotive Brake Pad Market Geography Segment Analysis

Automotive Brake Pad Market in North America

North America represents a significant market for automotive brake pad suppliers, characterized by advanced manufacturing capabilities and stringent safety regulations. The region's market is primarily driven by the presence of major automotive manufacturers, a robust aftermarket sector, and an increasing focus on vehicle safety features. The United States dominates the regional landscape, followed by Canada, with both countries showing strong adoption of premium brake pad technologies. The market is particularly influenced by the growing demand for high-performance vehicles and the increasing adoption of electric vehicles, which require specialized braking solutions.

Automotive Brake Pad Market in the United States

The United States stands as the dominant force in North America's automotive brake pad market, holding approximately 90% of the regional market share. The country's market is characterized by a strong presence of major brake pad manufacturers and a well-established distribution network. The automotive industry in the US continues to evolve with an increasing emphasis on electric vehicles and advanced braking technologies. The market is further strengthened by stringent safety regulations and standards set by regulatory bodies, driving the demand for high-quality brake pads. The presence of major automotive manufacturers and their continuous focus on research and development activities contributes significantly to market growth.

Automotive Brake Pad Market in Canada

Canada emerges as the fastest-growing market in North America, with a projected growth rate of approximately 3% during 2024-2029. The country's market is driven by increasing vehicle sales and a growing focus on vehicle safety features. Canada's automotive sector is experiencing significant transformation with the rise of electric vehicles and the implementation of stringent safety regulations. The market is characterized by strong aftermarket activities and increasing consumer awareness about vehicle maintenance and safety. The country's focus on environmental regulations and sustainable automotive solutions is also influencing the development and adoption of advanced brake pad technologies.

Automotive Brake Pad Market in Europe

Europe represents a mature market for automotive brake pad suppliers, characterized by advanced technological adoption and stringent safety standards. The region's market is driven by the presence of leading automotive manufacturers and a strong focus on innovation in braking technologies. Germany, Italy, France, the United Kingdom, and Spain are the key markets, each contributing significantly to the regional landscape. The European market is particularly influenced by the growing emphasis on environmental regulations and the increasing adoption of electric vehicles, which is driving innovations in brake pad technology.

Automotive Brake Pad Market in Germany

Germany maintains its position as the largest market for automotive brake pads in Europe, commanding approximately 15% of the regional market share. The country's market is driven by its robust automotive manufacturing sector and the presence of leading brake pad manufacturers. Germany's strong focus on technological innovation and research and development in the automotive sector continues to drive market growth. The country's automotive industry is particularly notable for its emphasis on high-performance vehicles and premium brake solutions, supported by a strong network of manufacturers and suppliers.

Automotive Brake Pad Market in Italy

Italy emerges as the fastest-growing market in Europe, with a projected growth rate of approximately 3% during 2024-2029. The country's market is characterized by a strong presence of automotive component manufacturers and a growing focus on premium vehicle segments. Italy's automotive sector is experiencing significant transformation with an increasing emphasis on electric vehicles and advanced braking technologies. The market benefits from the country's strong tradition in automotive manufacturing and continuous innovation in brake pad technologies, particularly in the high-performance segment.

Automotive Brake Pad Market in Asia Pacific

The Asia Pacific region represents a dynamic and rapidly evolving market for automotive brake pad suppliers, driven by increasing vehicle production and rising safety awareness. The region encompasses key markets including China, Japan, India, and South Korea, each contributing uniquely to the market landscape. The market is characterized by a mix of local manufacturers and international players, creating a competitive environment that drives innovation and market growth. The region's rapid industrialization and increasing vehicle ownership rates continue to fuel market expansion.

Automotive Brake Pad Market in China

China stands as the largest market for automotive brake pads in the Asia Pacific region, driven by its massive automotive manufacturing capabilities and large consumer base. The country's market benefits from strong government support for automotive manufacturing and increasing safety regulations. China's automotive sector continues to evolve with significant investments in electric vehicle technology and advanced braking systems. The market is characterized by a mix of domestic and international manufacturers, creating a competitive environment that drives innovation and quality improvements.

Automotive Brake Pad Market in India

India emerges as the fastest-growing market in the Asia Pacific region, driven by rapid urbanization and increasing vehicle ownership. The country's automotive sector is experiencing significant transformation with a growing emphasis on safety features and quality components. India's market is characterized by a strong presence of both domestic and international manufacturers, creating a competitive environment that drives innovation. The country's focus on developing its automotive manufacturing capabilities and increasing safety awareness continues to drive market growth.

Automotive Brake Pad Market in Rest of the World

The Rest of the World region, encompassing South America and the Middle East & Africa, represents an emerging market for automotive brake pads with significant growth potential. These regions are characterized by increasing vehicle ownership rates and growing awareness about vehicle safety. The Middle East & Africa region leads in market size, while South America shows promising growth potential. The market in these regions is driven by increasing industrialization, rising disposable incomes, and growing automotive manufacturing activities. The presence of both international and regional manufacturers creates a competitive environment that drives market growth and innovation in brake pad technologies.

Get Analysis on Important Geographic Markets

Download PDF

Automotive Brake Pad Industry Overview

Top Companies in Automotive Brake Pad Market

The automotive brake pad market is characterized by intense innovation and strategic developments among key players, including ZF Friedrichshafen AG, Robert Bosch GmbH, Tenneco Inc., Brembo SpA, Continental AG, and other prominent manufacturers. Companies are heavily investing in research and development to create advanced friction materials and environmentally friendly brake pad solutions, particularly focusing on reducing noise, vibration, and harshness while improving overall braking efficiency. The industry witnesses continuous product launches incorporating innovative technologies like copper-free formulations and enhanced coating techniques. Operational excellence is being achieved through strategic partnerships with OEMs and the expansion of manufacturing facilities across different regions. Market leaders are strengthening their aftermarket presence through extensive distribution networks and strategic collaborations, while simultaneously focusing on developing specialized solutions for emerging vehicle segments, particularly electric and hybrid vehicles.

Fragmented Market with Strong Regional Players

The automotive brake pad market exhibits a moderately fragmented structure with a mix of global conglomerates and specialized regional manufacturers. Global players leverage their extensive research capabilities, established brand reputation, and strong relationships with automotive manufacturers to maintain their market positions. These companies typically operate through multiple business segments, offering comprehensive brake system solutions alongside other automotive components. Regional players, particularly in emerging markets, compete effectively by offering cost-competitive products and maintaining strong local distribution networks.

The industry is witnessing strategic consolidation through mergers and acquisitions, particularly as larger companies seek to expand their technological capabilities and geographic presence. Companies are increasingly focusing on vertical integration to better control their supply chains and maintain quality standards. The aftermarket segment remains particularly attractive for both established players and new entrants, leading to increased competition and market dynamism. Manufacturing companies are establishing new ventures and partnerships to diversify their product offerings and strengthen their market presence in untapped regions.

Innovation and Sustainability Drive Future Success

Success in the automotive brake pad market increasingly depends on companies' ability to develop innovative, sustainable products while maintaining cost competitiveness. Manufacturers must invest in advanced manufacturing technologies and sustainable materials to meet evolving environmental regulations and customer preferences. The ability to offer customized solutions for different vehicle segments, particularly in the growing electric vehicle market, will be crucial for maintaining market share. Companies need to strengthen their aftermarket presence through robust distribution networks and digital platforms while maintaining strong relationships with OEM customers.

Market contenders can gain ground by focusing on specific market niches, developing specialized products for particular vehicle segments or regional markets. The increasing focus on vehicle safety and performance creates opportunities for companies offering premium products with advanced features. Success will also depend on the ability to navigate regulatory changes, particularly regarding environmental standards and safety requirements. Companies must maintain operational flexibility to address varying customer demands across different regions while managing raw material costs and supply chain efficiencies. Building strong relationships with both OEMs and aftermarket distributors will remain crucial for sustainable growth in the market.

Automotive Brake Pad Market Leaders

-

Brembo S.p.A.

-

Tenneco Inc.

-

ITT Inc.

-

Nisshinbo Holdings Inc.,

-

Akebono Brake Industry Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Automotive Brake Pad Market News

- January 2024: Winhere Co. Ltd held a groundbreaking ceremony for its new modern factory in WHA Industrial Estate Rayong. The facility will manufacture brake discs and pads for both domestic and international markets, boosting Thailand's position as a key automotive parts supplier. The factory is expected to be completed by early 2025.

- October 2023: Brembo and SGL Carbon announced two new facilities for their Brembo SGL Carbon Ceramic Brakes. The halls, covering 8,500 square meters, are scheduled for completion by October 2024, and production is set to begin in January 2025. This expansion will create about 80 new jobs, strengthening the automotive industry.

Automotive Brake Pad Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

-

4.1 Market Drivers

- 4.1.1 Advancements in Brake Pad Materials and Technologies

-

4.2 Market Restraints

- 4.2.1 Brake Malfunctions and Product Recalls

-

4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION (Market Size in Value (USD))

-

5.1 By Material Type

- 5.1.1 Semi-metallic

- 5.1.2 Non-asbestos Organic

- 5.1.3 Low-metallic

- 5.1.4 Ceramic

-

5.2 By Position Type

- 5.2.1 Front

- 5.2.2 Rear

-

5.3 By Sales Channel Type

- 5.3.1 Original Equipment Manufacturers (OEMs)

- 5.3.2 Aftermarket

-

5.4 By Vehicle Type

- 5.4.1 Passenger Cars

- 5.4.2 Commercial Vehicles

-

5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 India

- 5.5.3.2 China

- 5.5.3.3 South Korea

- 5.5.3.4 Japan

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 Rest of the world

- 5.5.4.1 South America

- 5.5.4.2 Middle East and Africa

6. COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

-

6.2 Company Profiles*

- 6.2.1 Brembo SpA

- 6.2.2 ITT Inc.

- 6.2.3 Robert Bosch GmBH

- 6.2.4 Tenneco Inc.

- 6.2.5 Akebono Brake Industry Co. Ltd

- 6.2.6 ZF Friedrichshafen AG

- 6.2.7 Continental AG

- 6.2.8 Federal-Mogul Holdings LLC

- 6.2.9 BorgWarner Inc.

- 6.2.10 Nisshinbo Holdings Inc.

- 6.2.11 Garrett Motion Inc.

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

8. Key Supplier Information**

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Automotive Brake Pad Industry Segmentation

Brake pads are a key part of the brake system. These are the components that contact and apply pressure and friction to a vehicle's brake rotors. Brake pads are composed of steel backing plates with friction material bound to the surface that faces the disc brake rotors.

The automotive brake pad market has been segmented based on material type, position type, sales channel, vehicle type, and geography. By material type, the market is segmented into semi-metallic, non-asbestos organic, low-metallic, and ceramic. By position type, the market is segmented into front and rear. By sales channel, the market is segmented into original equipment manufacturers (OEMs) and aftermarket. By vehicle type, the market is segmented into passenger cars and commercial vehicles. By geography, the market is segmented into North America, Europe, Asia-Pacific, and the Rest of the world. For each segment, the market sizing and forecast have been done based on the value (USD).

| By Material Type | Semi-metallic | ||

| Non-asbestos Organic | |||

| Low-metallic | |||

| Ceramic | |||

| By Position Type | Front | ||

| Rear | |||

| By Sales Channel Type | Original Equipment Manufacturers (OEMs) | ||

| Aftermarket | |||

| By Vehicle Type | Passenger Cars | ||

| Commercial Vehicles | |||

| By Geography | North America | United States | |

| Canada | |||

| Rest of North America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | India | ||

| China | |||

| South Korea | |||

| Japan | |||

| Rest of Asia-Pacific | |||

| Rest of the world | South America | ||

| Middle East and Africa | |||

Need A Different Region or Segment?

Customize Now

Automotive Brake Pad Market Research FAQs

How big is the Automotive Brake Pad Market?

The Automotive Brake Pad Market size is expected to reach USD 17.93 billion in 2025 and grow at a CAGR of 3.5% to reach USD 21.29 billion by 2030.

What is the current Automotive Brake Pad Market size?

In 2025, the Automotive Brake Pad Market size is expected to reach USD 17.93 billion.

Who are the key players in Automotive Brake Pad Market?

Brembo S.p.A., Tenneco Inc., ITT Inc., Nisshinbo Holdings Inc., and Akebono Brake Industry Co., Ltd. are the major companies operating in the Automotive Brake Pad Market.

Which is the fastest growing region in Automotive Brake Pad Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Automotive Brake Pad Market?

In 2025, the Asia Pacific accounts for the largest market share in Automotive Brake Pad Market.

What years does this Automotive Brake Pad Market cover, and what was the market size in 2024?

In 2024, the Automotive Brake Pad Market size was estimated at USD 17.30 billion. The report covers the Automotive Brake Pad Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Automotive Brake Pad Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Automotive Brake Pad Market Research

Mordor Intelligence delivers a comprehensive analysis of the automotive brake pad market. We leverage decades of expertise in automotive brake manufacturing research. Our extensive coverage includes brake pad manufacturers and brake pad suppliers. We also focus on crucial aspects of automotive brake friction materials. The report provides detailed insights into automotive brake components. This includes automotive brake wear sensors, automotive disc brake systems, and automotive brake linings, with particular attention to both OEM and aftermarket segments.

Stakeholders across the industry, from brake pad companies to component suppliers, benefit from our actionable intelligence. This information is available in an easy-to-download report PDF format. The analysis covers various segments, including two-wheeler brake pads, automotive carbon brake rotors, and industrial motor brakes. Our research includes comprehensive brake pad size specifications and brake pad size charts to support manufacturing decisions. The report also examines emerging trends in automotive brake wear indicators and automotive friction brake systems. These insights are valuable for strategic planning and market entry decisions.