| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 102.41 Billion |

| Market Size (2030) | USD 120.58 Billion |

| CAGR (2025 - 2030) | 3.32 % |

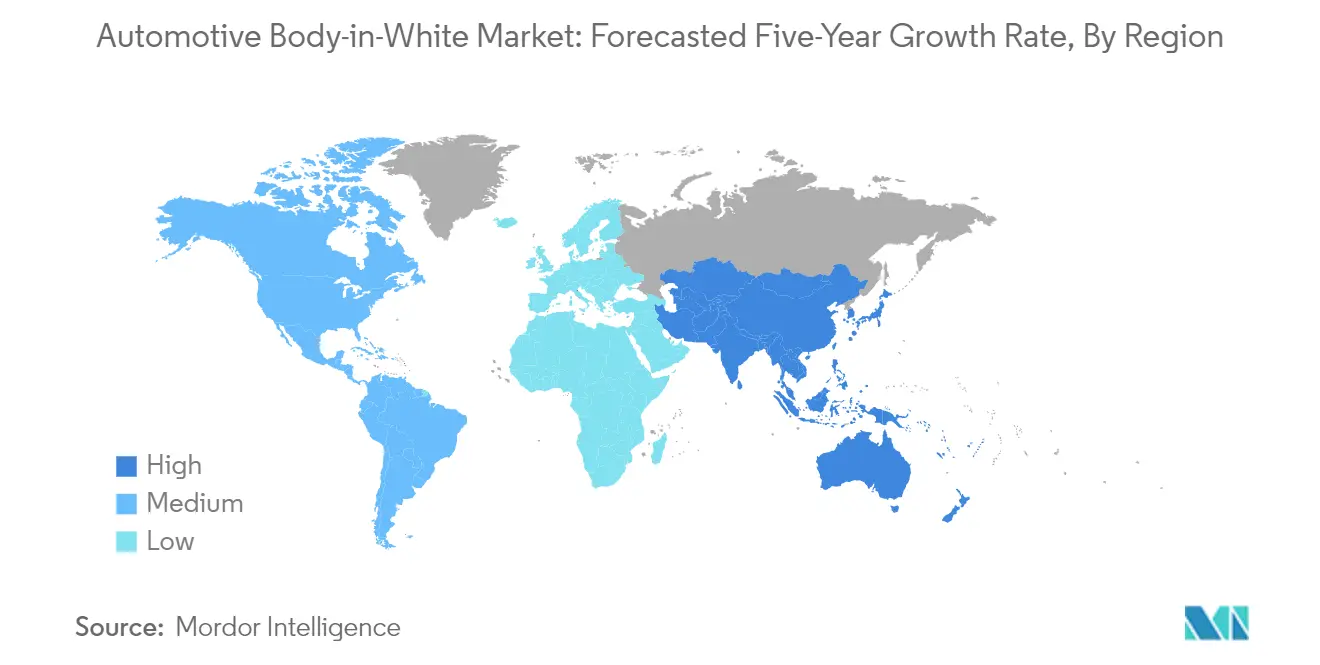

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

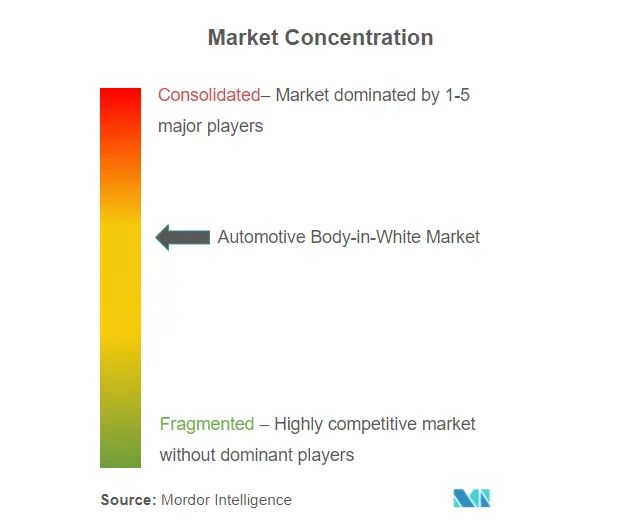

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order |

Automotive Body-in-White Market Analysis

The Automotive Body-in-White Market size is estimated at USD 102.41 billion in 2025, and is expected to reach USD 120.58 billion by 2030, at a CAGR of 3.32% during the forecast period (2025-2030).

The automotive body-in-white industry is undergoing a significant transformation driven by the increasing focus on vehicle weight reduction and environmental sustainability. Manufacturers are increasingly adopting lightweight materials and advanced design techniques, with studies indicating that approximately 75% of average vehicle weight reduction now comes from exterior and structural parts. This shift towards lightweight construction is particularly evident in recent developments, such as the implementation of advanced high-strength steel materials that can provide up to 20% weight savings in key energy absorption parts. The integration of aluminum, high-strength steel, and composite materials is becoming increasingly prevalent as manufacturers strive to balance structural integrity with weight optimization requirements.

Manufacturing technology in the body-in-white sector continues to evolve with the introduction of advanced joining and assembly techniques. A notable development in this direction was demonstrated in April 2023, when Comau unveiled an intelligent welding solution for Hycan Automotive Technology, achieving a remarkable 60 JPH cycle efficiency across multiple vehicle platforms. This advancement in welding technology represents a significant step forward in manufacturing flexibility and efficiency, allowing seamless transitions between different vehicle models while maintaining high precision standards. The development of solid-state laser sources has particularly revolutionized welding solutions for body-in-white assembly, offering improved electrical efficiency and enhanced tool flexibility.

Research and development initiatives are driving innovation across the industry, with manufacturers investing heavily in new materials and production methodologies. In June 2023, NDR Auto Component Limited announced significant R&D efforts focused on developing advanced metal components for passenger vehicle seat frames and body-in-white components, highlighting the industry's commitment to innovation. These developments are particularly focused on creating multi-functional components that can meet the demanding requirements of modern vehicle designs while maintaining structural integrity and safety standards. The industry is witnessing a surge in the development of hybrid materials and smart manufacturing solutions that combine different materials for optimal performance.

Quality control and inspection processes are experiencing a technological revolution with the implementation of automated systems and advanced measurement technologies. Traditional inspection methods are being replaced by sophisticated laser radar systems and scanners, enabling manufacturers to achieve higher precision and efficiency in quality control processes. This transformation in quality assurance methodology is particularly evident in the body-in-white process, where precise measurements of holes, slots, studs, and welding lines are crucial for maintaining product quality and consistency. The industry is moving towards contactless inspection systems that offer greater accuracy and efficiency, representing a significant advancement in manufacturing quality control processes.

Automotive Body-in-White Market Trends

Increase in Demand for Lightweight Materials

The automotive industry is witnessing a significant shift toward lightweight materials in body-in-white applications, driven primarily by stringent fuel economy standards and emission regulations across the globe. This trend is evidenced by major automotive manufacturers increasingly adopting innovative materials such as aluminum, magnesium alloy, and fiber-reinforced plastics (FRP) for vehicle body structures. The industry's focus on weight reduction is further demonstrated by recent developments, such as Lamborghini's introduction of the LB744 in March 2023, featuring their lightest 12-cylinder engine to date, weighing just 218 kilograms—17 kilograms lighter than its predecessor. Similarly, Porsche's launch of the limited edition 911 S/T in August 2023 showcases the industry's commitment to lightweight design principles for enhanced driving performance.

The push for lightweight materials is also fostering innovative collaborations between automotive manufacturers and material suppliers. A notable example is the September 2022 partnership between Atlis Motor Vehicles and ArcelorMittal, focusing on implementing S-in motion lightweight steel solutions for electric pickup trucks. This collaboration demonstrates how manufacturers are leveraging advanced materials to address multiple objectives—reducing vehicle weight, improving fuel efficiency, and enhancing structural integrity. The industry's commitment to lightweight materials is further driven by customer demands for improved styling, aesthetic appearance, and reduced noise, vibration, and harshness (NVH) aspects, while maintaining optimal comfort levels. These materials enable manufacturers to achieve nearly 30% weight reduction in high-strength steel-intensive body-in-white parts and approximately 40% weight reduction in aluminum-intensive vehicle bodies.

Understand The Key Trends Shaping This Market

Download PDF

High Demand for Commercial Vehicles

The commercial vehicle sector is experiencing robust growth, primarily driven by the expansion of e-commerce, logistics, and construction activities across global markets. This surge in demand is particularly evident in the light commercial vehicle segment, where manufacturers are introducing new models with enhanced performance and efficiency features. The market's vitality is demonstrated by the strong performance in the United States, where light trucks dominated vehicle sales in 2022, accounting for approximately 10.9 million units out of the total 13.75 million light vehicles sold, highlighting the growing preference for commercial and utility vehicles among consumers.

The increasing focus on environmental sustainability is also reshaping the commercial vehicle segment, with manufacturers investing heavily in developing lightweight and fuel-efficient commercial vehicles. This trend is supported by the rising adoption of advanced material joining techniques and innovative manufacturing processes specifically designed for commercial vehicle production. The sector's growth is further bolstered by the strong and sustained freight demand across the world, prompting fleet operators to accelerate their renewal and expansion activities. Additionally, the pickup truck segment has shown significant growth, especially in major markets, as these vehicles increasingly serve dual purposes—as both commercial workhorses and personal transportation, leading manufacturers to invest in new technologies and materials for their automotive body-in-white components.

Segment Analysis: Vehicle Type

Commercial Vehicles Segment in Automotive Body-in-White Market

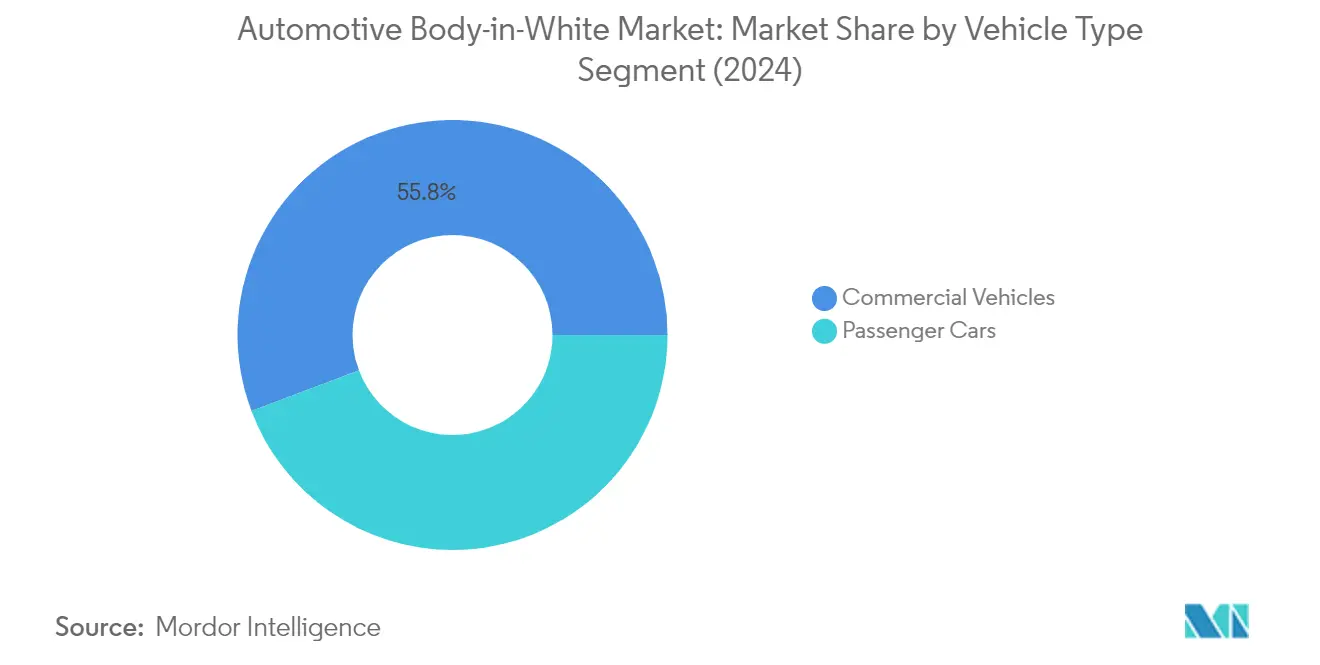

Commercial vehicles dominate the automotive body-in-white market, holding approximately 56% market share in 2024, while also demonstrating the strongest growth trajectory. The segment's prominence is primarily driven by the increasing worldwide demand for light commercial vehicles, medium and heavy commercial vehicles, particularly due to the growth of e-commerce and logistics sectors. The robust utilization rates and profitability across operators are boosting fleet renewals and expansions at an accelerated pace. The demand for pickup trucks has shown particular strength, especially in North America and Europe, attributed to growing preferences for multi-purpose utility and enhanced comfort features among buyers. The surge in construction activities across developing nations worldwide has further amplified the demand for commercial vehicles, consequently driving the body-in-white market in this segment.

Passenger Cars Segment in Automotive Body-in-White Market

The passenger cars segment maintains a significant presence in the automotive body-in-white market, driven by continuous technological advancements and evolving consumer preferences. The segment's growth is supported by increasing production and sales of passenger cars in several emerging economies, including India, Thailand, Indonesia, Egypt, and other Middle Eastern and African countries. The improving road infrastructure and rising disposable incomes of the middle-income class group are particularly influential in driving the passenger car market in developing countries. China continues to hold the largest share for passenger cars, followed by the United States, Japan, Germany, India, and South Korea. The segment's evolution is further characterized by the increasing focus on lightweight materials and advanced manufacturing processes to meet stringent emission standards and safety requirements.

Segment Analysis: Propulsion Type

IC Engine Segment in Automotive Body-in-White Market

The Internal Combustion (IC) Engine segment continues to dominate the global body-in-white market, commanding approximately 91% market share in 2024. This substantial market position is primarily driven by the extensive global manufacturing infrastructure and established supply chains supporting IC engine vehicle production. The segment's dominance is particularly evident in developing regions where the transition to electric vehicles is still in early stages. Major automotive manufacturers continue to optimize their IC engine vehicle body-in-white components through innovative lightweight materials and advanced manufacturing processes to meet stringent fuel efficiency and emission standards. The segment benefits from ongoing technological advancements in high-strength steel applications and aluminum integration, which help reduce vehicle weight while maintaining structural integrity. Additionally, the widespread availability of raw materials and cost-effective production methods for IC engine vehicle bodies continues to support this segment's market leadership.

Electric Vehicle Segment in Automotive Body-in-White Market

The Electric Vehicle (EV) segment is experiencing remarkable growth in the car body-in-white market, with a projected growth rate of approximately 25% during 2024-2029. This exceptional growth is driven by increasing global focus on sustainable transportation and stringent environmental regulations across major automotive markets. The segment's expansion is supported by significant investments in dedicated EV production facilities and innovative manufacturing technologies specifically designed for electric vehicle architectures. Automotive manufacturers are increasingly adopting specialized body-in-white parts that accommodate battery packs and unique structural requirements of EVs, while maintaining optimal weight distribution and safety standards. The segment is witnessing rapid technological advancements in materials and joining techniques specifically tailored for EV body structures, including new aluminum alloys and composite materials that offer enhanced strength-to-weight ratios. Furthermore, the growing consumer acceptance of EVs and supportive government policies worldwide are creating a robust foundation for sustained growth in this segment.

Segment Analysis: Material Type

Steel Segment in Automotive Body-in-White Market

Steel continues to dominate the automotive structural sheet market, commanding approximately 77% of the total market share in 2024. This substantial market position is primarily attributed to steel's cost-effectiveness and the ongoing development of new high-strength grades that combine material strength with superior formability characteristics. The automotive industry's preference for steel stems from its versatility in structural and framing applications, particularly in developing advanced high-strength steel variants that offer enhanced strength-to-weight ratios. Major automotive manufacturers are increasingly adopting ultra-high-strength steel grades for critical structural components, as these materials provide optimal performance while meeting stringent safety requirements. The steel segment's dominance is further reinforced by the material's excellent crash performance, corrosion resistance, and the established manufacturing infrastructure across global automotive production hubs.

Aluminum Segment in Automotive Body-in-White Market

The aluminum segment is experiencing remarkable growth in the automotive body-in-white market, projected to expand at approximately 7% during the forecast period 2024-2029. This accelerated growth is driven by the increasing demand for lightweight materials in vehicle manufacturing, particularly in electric vehicle production where weight reduction is crucial for extending range capabilities. Aluminum's superior strength-to-weight ratio, excellent formability, and corrosion resistance properties make it an increasingly attractive option for automotive manufacturers looking to reduce vehicle weight without compromising structural integrity. The segment's growth is further supported by technological advancements in aluminum forming processes, improved joining techniques, and the material's high recyclability potential, which aligns with the automotive industry's sustainability goals. Manufacturers are increasingly investing in aluminum-intensive body structures, particularly for premium vehicles and electric vehicle platforms, where the material's benefits can justify its higher cost compared to traditional steel.

Remaining Segments in Material Type

The composites and other material types segments play crucial roles in the automotive body-in-white market, offering unique advantages for specific applications. Composites, including carbon fiber and glass fiber materials, are gaining traction in premium vehicle segments where their exceptional strength-to-weight ratio and design flexibility provide significant advantages. These materials are particularly valuable in creating complex shapes and integrated structures that would be difficult to achieve with traditional materials. The other materials segment, which includes various innovative materials and hybrid solutions, continues to evolve with technological advancements. These materials often find applications in specialized components where specific performance characteristics such as enhanced thermal properties, acoustic dampening, or unique structural requirements are needed. Both segments contribute to the overall advancement of automotive lightweight construction techniques and provide manufacturers with expanded options for optimizing vehicle design and performance.

Segment Analysis: Material Joining Technique

Welding Segment in Automotive Body-in-White Market

Welding continues to dominate the automotive body-in-white market, commanding approximately 45% of the total market share in 2024. This significant market position is attributed to welding's versatility and effectiveness in joining thicker metals and larger automotive components like doors, hoods, roofs, and chassis. The technology's prominence is further strengthened by the emergence of advanced robotic welding systems that offer enhanced precision, superior quality welds, and improved productivity while reducing the need for rework. Major automotive manufacturers are increasingly adopting automated welding solutions that incorporate artificial intelligence and machine learning capabilities to optimize welding parameters and ensure consistent quality across their production lines. The segment's strong performance is also supported by welding's cost-effectiveness compared to other joining techniques, particularly for high-volume production scenarios in automotive manufacturing.

Laser Brazing Segment in Automotive Body-in-White Market

The laser brazing segment is emerging as a rapidly growing segment in the automotive body-in-white market, expected to grow at approximately 3.5% during the forecast period 2024-2029. This growth is primarily driven by the increasing demand for superior aesthetic finishes and the technique's ability to join dissimilar materials without compromising the zinc coating, which is crucial for corrosion resistance. Laser brazing is particularly favored for visible joints such as roof joints, tailgates, and C-columns, where maintaining surface smoothness is paramount. The technology's ability to operate at lower temperatures compared to traditional welding, thereby preventing material distortion and maintaining the integrity of protective coatings, has made it increasingly popular among premium automotive manufacturers. The segment is also benefiting from ongoing technological advancements in laser systems and automation capabilities, which are improving the precision and efficiency of the brazing process.

Remaining Segments in Material Joining Technique

The automotive body-in-white market's remaining joining techniques include clinching, bonding, and other specialized methods, each serving specific applications in vehicle manufacturing. Clinching has gained traction as a mechanical fastening alternative, particularly suitable for joining lightweight materials and components where thermal joining methods might be unsuitable. Bonding techniques have become increasingly important with the growing use of advanced materials and composites in automotive manufacturing, offering advantages in weight reduction and structural integrity. Other specialized joining techniques continue to evolve, incorporating innovative technologies such as flow-hole screwing, module mechanical joining, and self-piercing riveting, providing manufacturers with additional options for specific applications and material combinations in vehicle assembly.

Automotive Body-in-White Market Geography Segment Analysis

Automotive Body-in-White Market in North America

North America represents a significant market for automotive body-in-white components, driven by the presence of major automotive manufacturers and a robust automotive production ecosystem. The region encompasses key markets, including the United States and Canada, with each country contributing uniquely to the market's dynamics. The United States leads the regional market with its extensive automotive manufacturing infrastructure and technological advancements in production processes, while Canada maintains a strong position with its focus on lightweight materials and electric vehicle production.

Automotive Body-in-White Market in the United States

The United States dominates the North American body-in-white market, accounting for approximately 82% of the regional market share in 2024. The country's market is characterized by the presence of major manufacturers like Ford, Dodge, General Motors, Lincoln, Chrysler, and Tesla. The US automotive industry has been witnessing a surge in the sales of SUVs and crossover utility vehicles, which has directly impacted the demand for body-in-white components. The country's focus on electric vehicle production and advanced manufacturing technologies has further strengthened its position in the market. The presence of numerous manufacturing facilities and continuous investment in research and development has helped maintain the United States' leadership position in the region.

Automotive Body-in-White Market in Canada

Canada emerges as the fastest-growing market in North America, with a projected growth rate of approximately 3% during 2024-2029. The country's automotive sector plays a crucial role in its economy, with significant contributions to the GDP. Canada has positioned itself as a key player in commercial vehicle production and electric vehicle manufacturing. The government's ambitious targets for electric vehicle adoption and significant investments in manufacturing infrastructure have created favorable conditions for market growth. The country's focus on sustainable transportation and commitment to reducing emissions has led to increased adoption of lightweight materials and innovative manufacturing processes in the automotive body-in-white segment.

Automotive Body-in-White Market in Europe

The European automotive body-in-white market is characterized by its advanced manufacturing capabilities and strong focus on innovation. The region comprises key markets, including Germany, the United Kingdom, France, and Spain, each contributing significantly to the overall market landscape. The presence of premium automotive manufacturers and stringent emission regulations has driven the adoption of advanced materials and manufacturing processes in the body-in-white segment. The region's push towards electric vehicle production has also influenced the development of innovative body-in-white solutions.

Automotive Body-in-White Market in Germany

Germany maintains its position as the largest market in Europe, commanding approximately 38% of the regional market share in 2024. The country's automotive industry is renowned for its excellence and innovation, particularly in the premium vehicle segment. Germany's leadership position is supported by the presence of major automotive manufacturers like Mercedes, Audi, and BMW, who continue to invest heavily in research and development. The country's focus on high-quality manufacturing processes and advanced automation technologies has established it as a benchmark for body-in-white production in Europe.

Automotive Body-in-White Market in the United Kingdom

The United Kingdom demonstrates the highest growth potential in Europe, with a projected growth rate of approximately 3% during 2024-2029. The country's automotive sector is undergoing significant transformation, particularly in the adoption of electric vehicle technologies. The UK's strong focus on research and development, coupled with government support for sustainable transportation solutions, has created favorable conditions for market growth. The presence of both traditional automotive manufacturers and new electric vehicle producers has contributed to the dynamic nature of the automotive body-in-white market.

Automotive Body-in-White Market in Asia-Pacific

The Asia-Pacific region represents a crucial market for automotive body-in-white components, encompassing major automotive manufacturing hubs such as China, Japan, India, and South Korea. The region's market is characterized by rapid industrialization, increasing automotive production capabilities, and growing demand for vehicles. Each country in the region brings unique strengths to the market, from China's massive production capacity to Japan's technological expertise, India's growing automotive sector, and South Korea's focus on innovation.

Automotive Body-in-White Market in China

China stands as the dominant force in the Asia-Pacific region's body-in-white market. The country's massive automotive manufacturing infrastructure, coupled with its position as the world's largest automobile market, has established it as a key player in the industry. China's market is characterized by the presence of both domestic and international automotive manufacturers, with a strong focus on electric vehicle production. The country's continuous investment in manufacturing capabilities and adoption of advanced technologies has further strengthened its position in the regional market.

Automotive Body-in-White Market in India

India emerges as the fastest-growing market in the Asia-Pacific region. The country's automotive sector is experiencing rapid growth, driven by increasing domestic demand and growing manufacturing capabilities. India's focus on becoming a global automotive manufacturing hub, coupled with government initiatives supporting the automotive industry, has created favorable conditions for market growth. The country's emphasis on cost-effective manufacturing solutions and growing adoption of advanced technologies in automotive production has positioned it as a key market for future growth.

Automotive Body-in-White Market in Rest of the World

The Rest of the World market, encompassing South America and the Middle East & Africa regions, presents diverse opportunities in the automotive body-in-white sector. South America, particularly Brazil, serves as a significant automotive manufacturing hub, while the Middle East & Africa region is experiencing growing automotive sector investments. South America emerges as the larger market in this region, driven by Brazil's established automotive manufacturing infrastructure. The region's market is characterized by increasing investments in manufacturing capabilities, growing domestic demand, and the presence of both regional and international automotive manufacturers. The Middle East & Africa region shows promising growth potential, supported by increasing automotive investments and growing domestic market demand.

Get Analysis on Important Geographic Markets

Download PDF

Automotive Body-in-White Industry Overview

Top Companies in Automotive Body-in-White Market

The automotive body-in-white market is led by established players including Magna International, Norsk Hydro ASA, Gestamp Automocion SA, Aisin Seiki Co., Thyssenkrupp AG, and Benteler International. These companies are heavily investing in research and development to create innovative lightweight materials and efficient manufacturing techniques for body-in-white components. The industry is witnessing a significant shift towards automation and robotics in production processes, with major players incorporating advanced technologies like digital twin and Industry 4.0 solutions. Companies are expanding their global footprint through strategic partnerships and facility expansions, particularly in emerging markets. There is also an increasing focus on developing solutions for electric vehicles, with manufacturers adapting their body-in-white engineering designs to accommodate battery systems and meet new structural requirements. The competitive landscape is characterized by continuous innovation in materials, particularly in aluminum and high-strength steel applications, along with investments in quality inspection systems and contactless measurement technologies.

Consolidated Market with Strong Regional Players

The automotive body-in-white market structure is characterized by a mix of global conglomerates and specialized manufacturers, with the top players holding significant market share through their established relationships with major automotive OEMs. The market demonstrates a high degree of consolidation, particularly in mature markets like North America and Europe, where large integrated suppliers dominate the landscape through their comprehensive product portfolios and advanced manufacturing capabilities. These established players leverage their extensive research and development capabilities, global manufacturing footprint, and long-standing relationships with automotive manufacturers to maintain their competitive positions. The market also features regional specialists who have carved out strong positions in specific geographic markets or technological niches.

The industry has witnessed significant merger and acquisition activity, driven by the need to acquire new technologies, expand geographic presence, and achieve economies of scale. Companies are increasingly pursuing strategic partnerships and joint ventures to combine complementary capabilities and address the evolving needs of the automotive industry, particularly in emerging technologies like electric vehicles. The market is also seeing vertical integration efforts, with some players expanding their capabilities across the value chain, from raw material processing to final assembly, to better control quality and costs while improving operational efficiency.

Innovation and Adaptability Drive Market Success

Success in the automotive body-in-white market increasingly depends on companies' ability to innovate in lightweight materials, develop efficient manufacturing processes, and adapt to changing automotive industry requirements, particularly the shift towards electric vehicles. Incumbent players must focus on strengthening their technological capabilities through continued investment in research and development, while also maintaining cost competitiveness through operational excellence and automation. Companies need to develop flexible manufacturing systems that can accommodate multiple vehicle platforms and propulsion types, while also investing in sustainability initiatives to meet increasingly stringent environmental regulations and customer demands for greener solutions.

For new entrants and smaller players, success lies in identifying and focusing on specific market niches or geographic regions where they can build competitive advantages. This includes developing specialized expertise in emerging technologies, forming strategic partnerships with established players, such as Kirchhoff Automotive, or focusing on specific customer segments or regional markets. The market's high barriers to entry, including substantial capital requirements and stringent quality standards, make it crucial for contenders to differentiate themselves through innovation or specialized capabilities. Companies must also carefully manage their relationships with automotive OEMs, who hold significant bargaining power and increasingly demand global supply capabilities along with local presence in key markets.

Automotive Body-in-White Market Leaders

-

Magna International Inc.

-

Norsk Hydro ASA

-

Gestamp Automocion SA

-

Aisin seiki co ltd

-

Thyssenkrupp AG

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Automotive Body-in-White Market News

- July 2023: Hyundai Motor Company unveiled the IONIQ 5 N - N brand's first high-performance, all-electric vehicle, the IONIQ 5 N. The IONIQ 5 N combines the electrified-global modular platform (E-GMP) of the basic model with N's motorsport-bred innovations. The corner rascal capabilities of the IONIQ 5 N begin with improvements to the body-in-white (BIW) construction, including 42 more welding sites and 2.1 meters of additional adhesives.

- June 2023: Kirchhoff Automotive GmbH claimed that it received a large number of fresh orders for Mexican manufacture. It plans to extend its presence in Querétaro. The Querétaro II facility will begin operations in 2025. It will include an e-coating line capable of thick-film coating as well as preparations for a moderate pickling procedure. The estimated plant area is 15,000 square meters. It is installing resistance spot welding and arc welding equipment at the Puebla facility. It will manufacture body-in-white components as well as cross-car beams for new client applications.

- March 2023: Steyr Automotive announced the successful conclusion of the Volkswagen Group's 4-day process audit. It has now achieved Tier 1 status. Auditors from MAN Truck & Bus and Volkswagen specifically assessed the body-in-white and plastic components painting in accordance with VW requirements. Steyr Automotive is now mentioned as a prospective VW Group supplier.

- July 2022: Sika AG participated in the 'Joining in Car Body Engineering' conference in Germany. It introduced SikaPower, a one-component, epoxy-based bulk hybrid adhesive that cures under the temperature impact of electro-coat ovens. It also focused on the various aspects of sustainability in the life cycle of new body-in-white adhesives, ranging from the development of new formulations with sustainable/bio-based raw materials to new 'low bake' adhesives that enable an energy/CO2 reduced process by allowing a lower e-coat oven temperature, to a more sustainable use-phase by light-weighting through aluminum and mixed material bonding, to the topic of material separation during body recycling at end-of-life.

- August 2022: Chery Holding Group Co., Ltd. (Chery) exhibited the AtlantiX - EXEED M38T mass-production concept automobile to the public in Qingdao, Shandong, under the EXEED brand. Simultaneously, the first body-in-white EXEED M38T rolled off the production line at the Qingdao factory. The M38T was designed using the new M3X Architecture 2.0 and the advanced electronic and electrical architecture EEA4.0. The body-in-white contour of M38T suggests that it adheres to AtlantiX's design language.

Automotive Body-in-White Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

-

4.1 Market Drivers

- 4.1.1 Growing Demand for Lightweight Vehicles to Drive the Automotive Body-in-White Market

-

4.2 Market Restraints

- 4.2.1 High Cost of Materials to Manufacture BIW Structures is Expected to Limit Market Growth.

-

4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION (Market Value in USD)

-

5.1 Vehicle Type

- 5.1.1 Passenger Vehicles

- 5.1.2 Commercial Vehicles

-

5.2 Propulsion Type

- 5.2.1 IC Engines

- 5.2.2 Electric Vehicles

-

5.3 Material Type

- 5.3.1 Aluminum

- 5.3.2 Steel

- 5.3.3 Composites

- 5.3.4 Other Material Types

-

5.4 Material Joining Technique

- 5.4.1 Welding

- 5.4.2 Clinching

- 5.4.3 Laser Brazing

- 5.4.4 Bonding

- 5.4.5 Other Material Joining Techniques

-

5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Spain

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 India

- 5.5.3.2 China

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 Rest of the World

- 5.5.4.1 South America

- 5.5.4.2 Middle-East and Africa

6. COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

-

6.2 Company Profiles *

- 6.2.1 Magna International Inc.

- 6.2.2 Norsk Hydro ASA

- 6.2.3 Gestamp Automocion SA

- 6.2.4 Aisin Seiki Co. Limited

- 6.2.5 Thyssenkrupp AG

- 6.2.6 ABB Corporation

- 6.2.7 TECOSIM Group

- 6.2.8 Tata Steel Limited

- 6.2.9 Dura Automotive Systems

- 6.2.10 Tower International

- 6.2.11 CIE Automotive

- 6.2.12 Benteler International

- 6.2.13 Kuka AG

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Automotive Body-in-White Industry Segmentation

Automotive body-in-white refers to the phase in automotive manufacturing in which the sheet metal body components of an automobile have been welded together. In other words, the automotive body-in-white is the frame structure of the automobile before painting and assembly of the engine, chassis, glass, seat, doors, hood, and other such sub-assemblies.

The automotive body-in-white market is segmented by vehicle type (passenger vehicles and commercial vehicles), propulsion type (IC engine and electric vehicles), material type (aluminum, steel, composites, and other material types), material joining technique (welding, clinching, laser brazing, bonding, and other material joining techniques), and geography (North America, Europe, Asia-Pacific, and Rest of the World).

The report offers market size and forecast for the Automotive Body-in-White market in value (USD) for all the above segments.

| Vehicle Type | Passenger Vehicles | ||

| Commercial Vehicles | |||

| Propulsion Type | IC Engines | ||

| Electric Vehicles | |||

| Material Type | Aluminum | ||

| Steel | |||

| Composites | |||

| Other Material Types | |||

| Material Joining Technique | Welding | ||

| Clinching | |||

| Laser Brazing | |||

| Bonding | |||

| Other Material Joining Techniques | |||

| Geography | North America | United States | |

| Canada | |||

| Rest of North America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | India | ||

| China | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Rest of the World | South America | ||

| Middle-East and Africa | |||

Need A Different Region or Segment?

Customize Now

Automotive Body-in-White Market Research FAQs

How big is the Automotive Body-in-White Market?

The Automotive Body-in-White Market size is expected to reach USD 102.41 billion in 2025 and grow at a CAGR of 3.32% to reach USD 120.58 billion by 2030.

What is the current Automotive Body-in-White Market size?

In 2025, the Automotive Body-in-White Market size is expected to reach USD 102.41 billion.

Who are the key players in Automotive Body-in-White Market?

Magna International Inc., Norsk Hydro ASA, Gestamp Automocion SA, Aisin seiki co ltd and Thyssenkrupp AG are the major companies operating in the Automotive Body-in-White Market.

Which is the fastest growing region in Automotive Body-in-White Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Automotive Body-in-White Market?

In 2025, the Asia-Pacific accounts for the largest market share in Automotive Body-in-White Market.

What years does this Automotive Body-in-White Market cover, and what was the market size in 2024?

In 2024, the Automotive Body-in-White Market size was estimated at USD 99.01 billion. The report covers the Automotive Body-in-White Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Automotive Body-in-White Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Automotive Body-in-White Market Research

Mordor Intelligence brings extensive expertise in analyzing the automotive body-in-white market. We offer comprehensive insights into this crucial automotive manufacturing segment. Our research thoroughly examines body in white components and processes. This includes body in white welding techniques and automotive structural sheet applications. The report covers essential aspects of body in white engineering and automotive body in white production systems. We pay particular attention to emerging automotive structural sheet market trends and technological innovations in automotive cross car beam design.

Stakeholders gain valuable insights through our detailed analysis of body in white process developments and automotive body comfort system innovations. The report, available as an easy-to-download PDF, provides in-depth coverage of automotive body exterior components and automotive longitudinal beam technologies. Our research encompasses vehicle body in white manufacturing techniques and automotive BIW advancements. It also includes a comprehensive evaluation of body in white production methodologies. The analysis includes detailed assessments of leading companies like Kirchhoff Automotive and their contributions to automotive body-in-white development.