Market Trends of Automotive Bearings Industry

This section covers the major market trends shaping the Automotive Bearings Market according to our research experts:

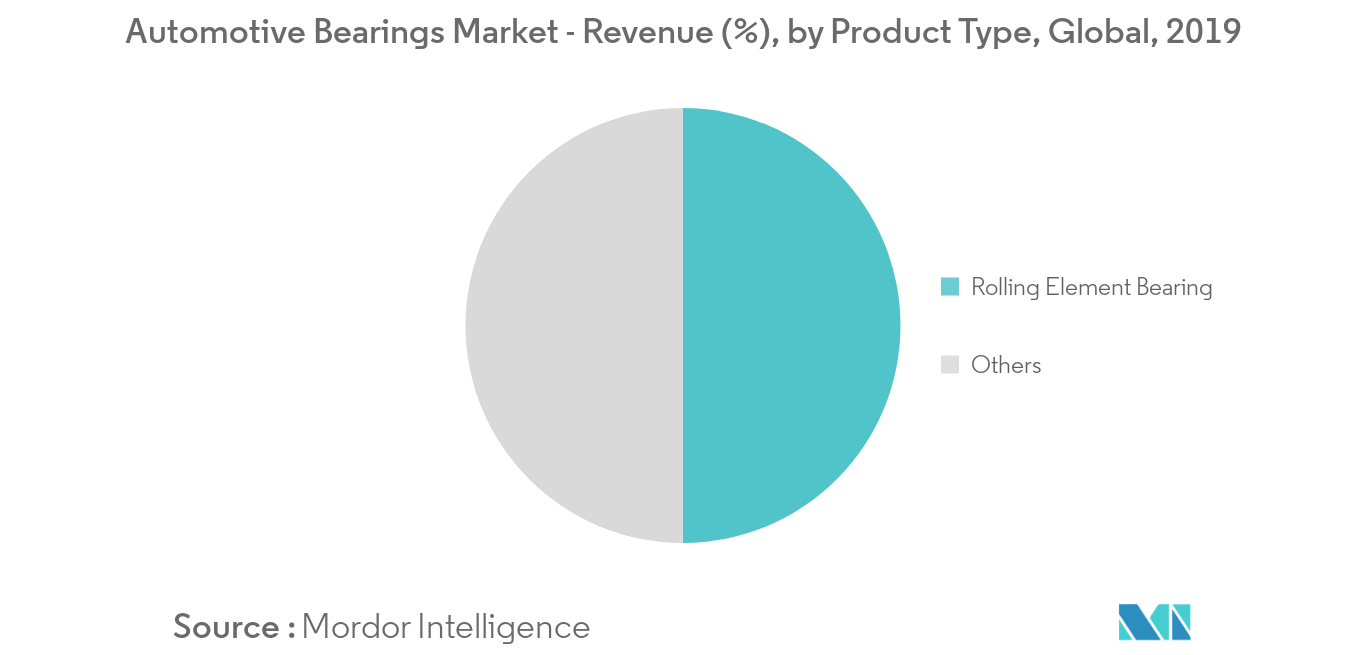

Rolling Element Bearings Dominated the Market and are Expected to Grow at a Fast Pace

The global automotive rolling element bearings segment is expected to project a CAGR of 5.39%, during the forecast period.

Tapered roller, needle roller, spherical roller, and cylindrical/straight roller are the major types of automotive rolling element bearings. These bearings have been widely deployed in vehicle systems, predominantly in the engine, transmission, and wheels (excluding needle rollers for wheel bearings).

During 2017-2018, major bearing manufacturers, like SKF, NSK, Schaeffler, and JTEKT, announced their investment plans regarding expansion of their rolling element bearings production facilities, to meet the growing demand in the automotive industry. The above-mentioned manufacturers have expanded their rolling element bearing production facilities, majorly in the Asia-Pacific region, and especially in countries, like Japan, India, South Korea, Vietnam, Malaysia, and China. Tapered and needle roller bearings are identified as the major production plans of the aforementioned players.

Owing to the growing competition in the automotive rolling bearings segment, bearing manufacturers have focused on improving their rolling element bearing products. Thus, in 2018, the automotive industry has seen numerous developments of new rolling element bearings. For instance, in April 2018, Schaeffler developed a new transmission bearing with low friction, known as an angular roller unit (ARU). In March 2018, NSK developed a 2.5-generation high-performance taper-roller hub unit bearing with a hub shaft for vehicles, like pickup trucks, large SUVs, and commercial vehicles.

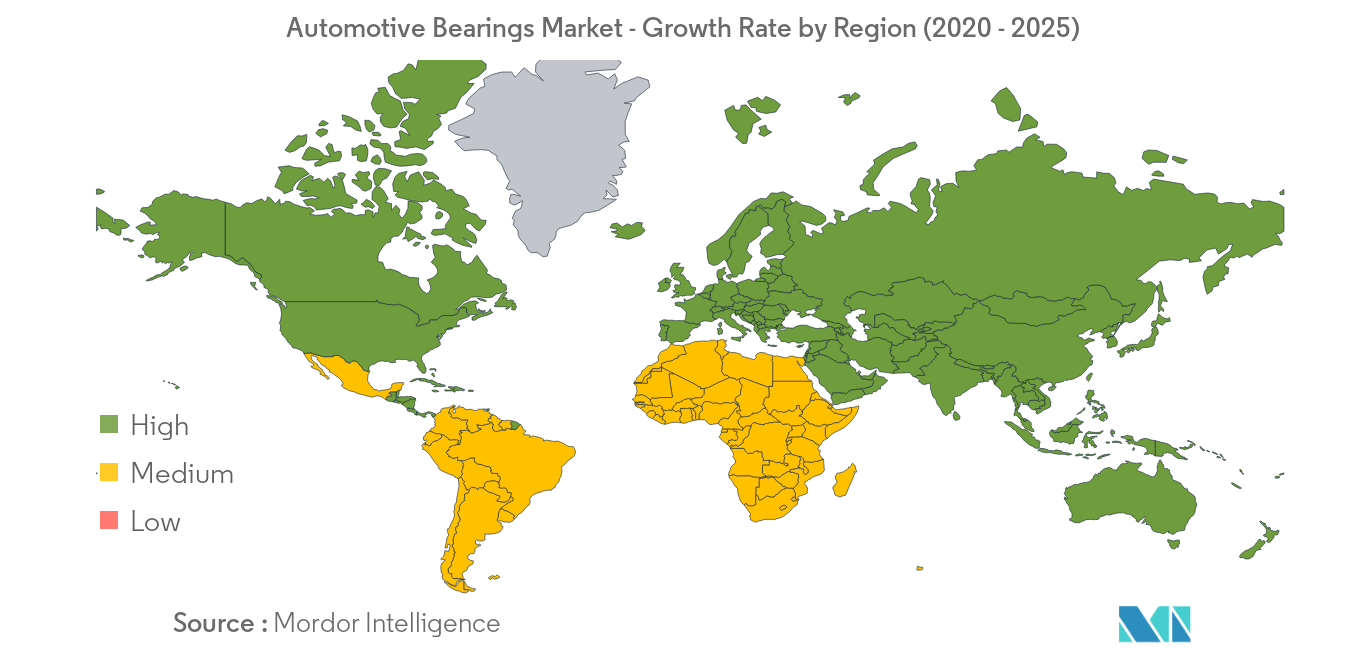

Asia-Pacific Dominated the Global Market

In the automotive bearings market, Asia-Pacific dominated the market and is expected to witness the highest growth rate during the forecast period.

In the Asia-Pacific region, China dominated the market, followed by Japan and India. The Chinese economy is growing, and the disposable income of middle-class consumers is also increasing. This, in turn, reflects positively on the growing demand for vehicles. Over the past five years, owing to the low production costs in the country, the demand for vehicle production has gone up drastically. Additionally, in 2017, 24,961,948 units of passenger vehicles were sold in China, compared to 24,376,902 units in 2016. The increased sales of the vehicles in the country are expected to give rise to the brake system market, creating demand for production.

However, in 2018, the country witnessed a decline in vehicle sales by 3%, owing to trade tensions and shaky consumer confidence, which hindered the growth of the market. Furthermore, industry experts predict a further decline in vehicle sales in 2019. To overcome the same, the government has unveiled numerous measures to increase sales of cars, which is expected to drive the growth of the market.

In India, in 2018, vehicle sales declined, owing to an uneven monsoon, poor festive demand, and high fuel and insurance costs. However, owing to the government’s Make in India initiative, automotive component manufacturers are investing in the country, by either investing or launching a new product, or through mergers and acquisitions. For instance, ABC Bearing Limited is merging with Timken India Limited. This merger will help both the companies to achieve a larger product portfolio, access new domestic and export markets, and increase market share and economies of scale.