Automotive Battery Rental Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

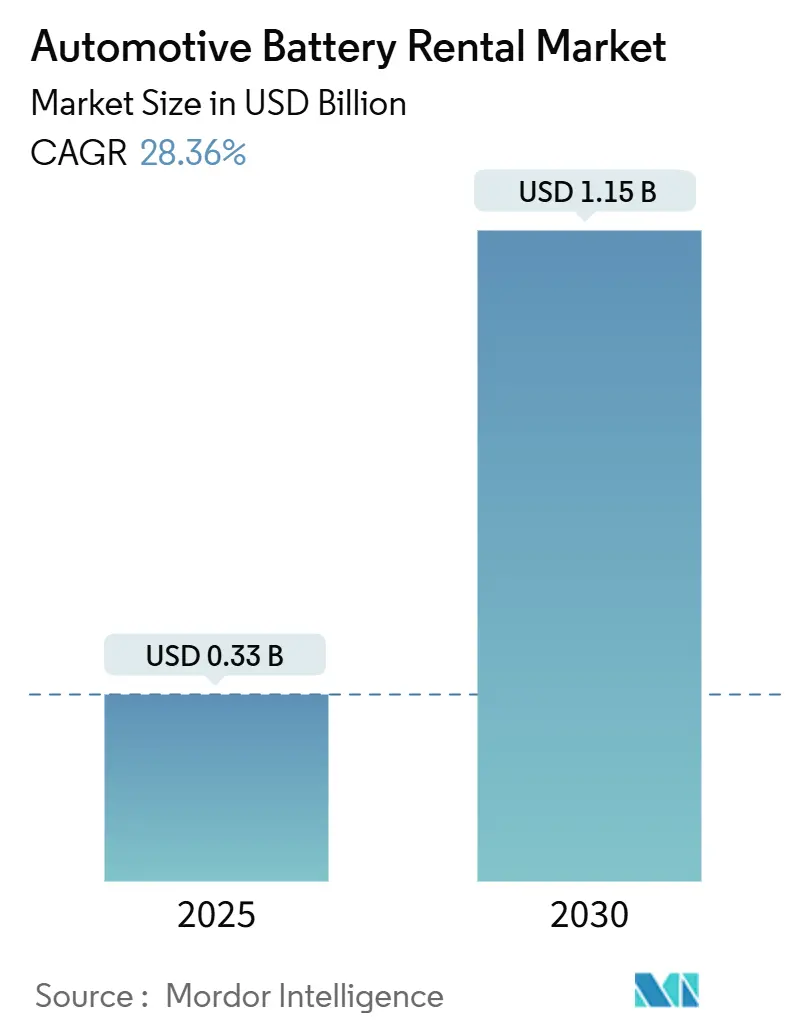

| Market Size (2025) | USD 0.33 Billion |

| Market Size (2030) | USD 1.15 Billion |

| Growth Rate (2025 - 2030) | 28.36% CAGR |

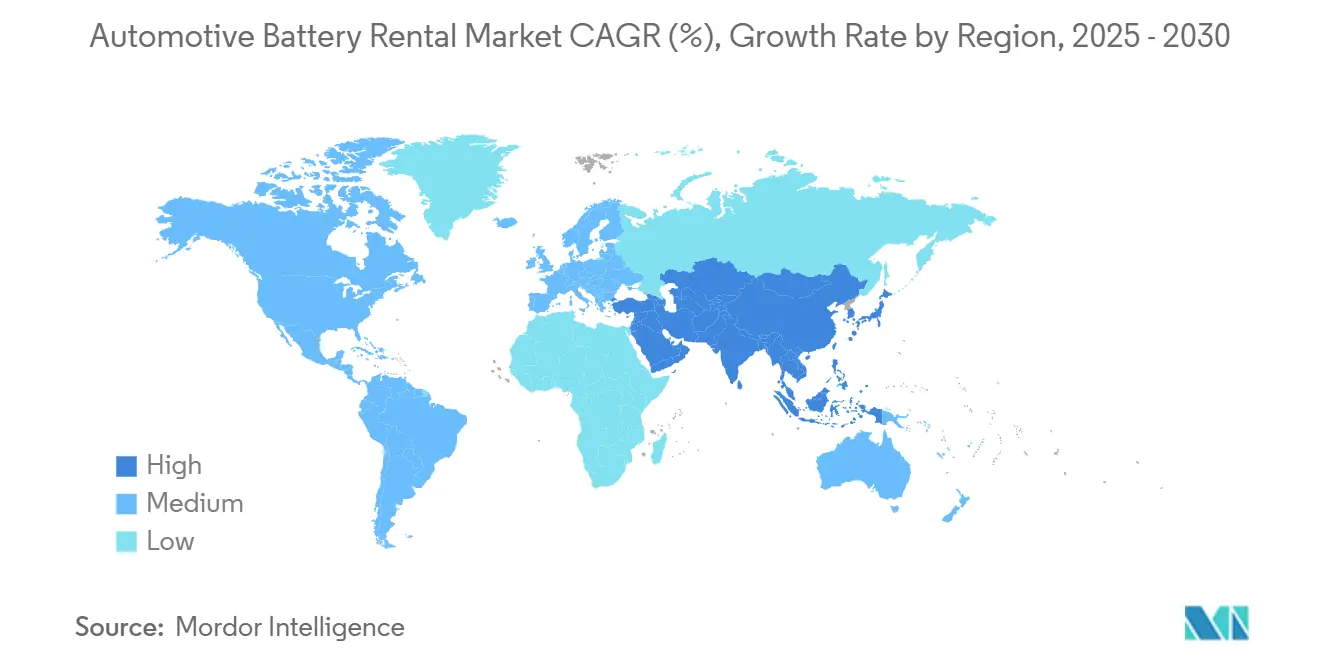

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Automotive Battery Rental Market Analysis by Mordor Intelligence

The automotive battery rental market size is valued at USD 0.33 billion in 2025 and is forecast to reach USD 1.15 billion by 2030, expanding at a 28.36% CAGR during the period. Battery-as-a-service (BaaS) models lower the upfront cost of electric vehicles, de-risk battery obsolescence for users, and enable service providers to monetize battery life far beyond a single vehicle. Four structural forces sustain momentum: falling battery pack prices, swap-station density that cuts range anxiety, regulations that reward circular-economy compliance, and connected-fleet software that drives predictive maintenance. Competitive dynamics favor vertically integrated platforms that combine battery manufacturing, leasing, and digital fleet optimization. Asia Pacific commands early leadership because governments in China and India pair industrial policy with air-quality targets, while fleet operators worldwide deploy battery subscriptions to lock in predictable total cost of ownership.

Key Report Takeaways

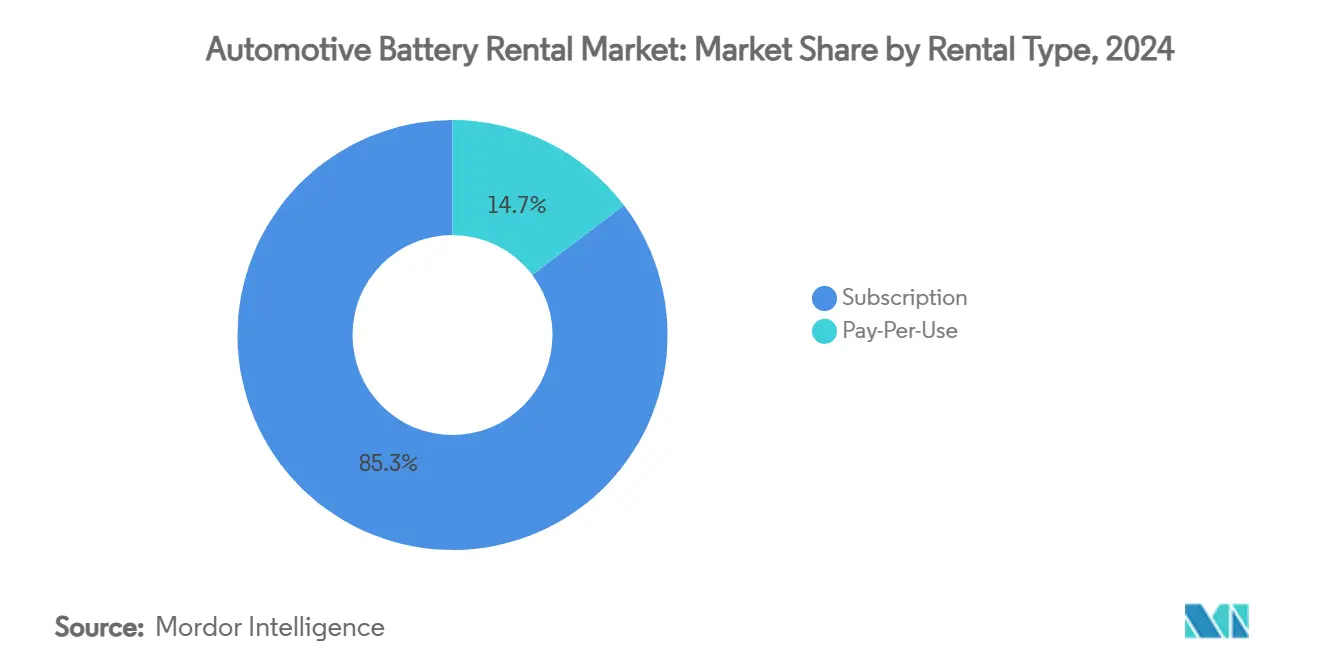

- By rental type, subscription plans accounted for 85.34% of revenue in 2024; pay-per-use contracts post the highest projected CAGR at 34.41% through 2030.

- By battery type, lithium-ion held 96.25% of the automotive battery rental market share in 2024, whereas solid-state units are set to grow at an 88.95% CAGR to 2030.

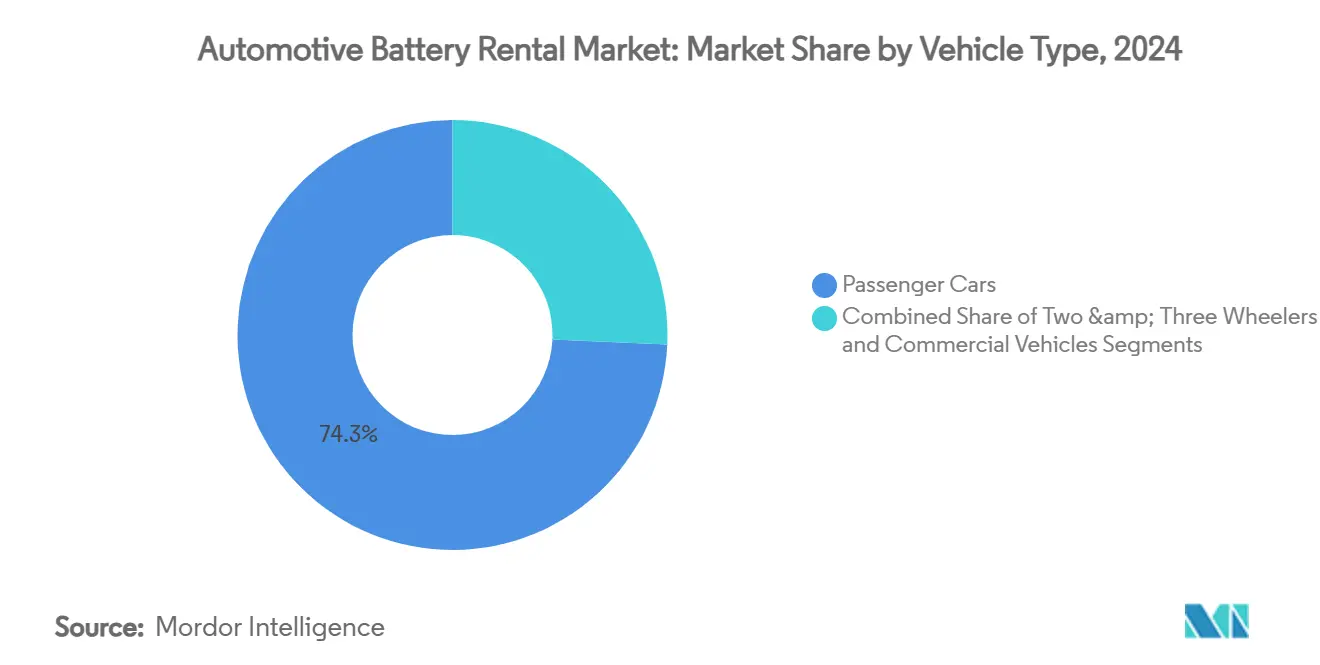

- By vehicle type, passenger cars produced 74.25% revenue in 2024; commercial vehicles will accelerate at a 34.13% CAGR between 2025-2030.

- By end user, fleet operators controlled 84.12% of demand in 2024; the private-consumer segment is tracking a 32.87% CAGR to 2030.

- By geography, Asia Pacific generated 65.25% revenue in 2024 and is forecast to expand at a 31.45% CAGR through 2030.

Global Automotive Battery Rental Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Global EV Sales and Model Variety | +6.2% | Global, APAC leading | Medium term (2-4 years) |

| Declining Battery Cost Curve | +5.1% | Global, production centered in APAC | Long term (≥ 4 years) |

| Government Incentives for Battery Leasing & Swapping | +4.8% | APAC core, Europe & North America widening | Short term (≤ 2 years) |

| Rapid Rollout of Swap-Station Networks | +3.9% | APAC dominance, selective Europe | Medium term (2-4 years) |

| Circular-Economy Rules | +3.4% | Europe first, global later | Long term (≥ 4 years) |

| Fleet-Telematics Integration | +2.7% | North America & Europe front-running | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Global EV Sales and Model Variety

Electric-vehicle registrations exceeded 14 million in 2024, and the International Energy Agency projects annual sales of 30 million by 2030, more than tripling the addressable base for battery rental services [1]International Energy Agency, “Global EV Outlook 2024,” iea.org. Every new model launch creates additional form-factor commonality, letting rental operators spread the same pack across multiple platforms, enhance utilization, and reduce cost per cycle. OEMs now promote BaaS as a differentiator in crowded passenger-car line-ups, while commercial-van makers bundle rental plans to remove battery risk for logistics clients. The trend is strongest where model diversity coincides with city congestion charges, prompting last-mile fleets to replace internal-combustion units. Interoperability standards remain a prerequisite for scale but are advancing through voluntary cross-industry alliances and European Union mandates.

Declining Battery Cost Curve Boosts Rental Economics

Average lithium-ion pack prices fell from USD 156/kWh in 2022 to USD 119/kWh in 2024, according to the International Energy Agency, shaving almost 25% off acquisition costs for rental fleets. Lower costs let operators price subscriptions 30-40% below outright battery purchase while protecting margins through second-life energy-storage resale. Solid-state prototypes that Toyota and CATL plan to commercialize by 2028 promise further cost-per-cycle reductions and extended warranty windows, reinforcing the service proposition. Rapid cost deflation, however, forces rental firms to shorten depreciation schedules to avoid inventory write-downs.

Government Incentives for Battery Leasing & Swapping

Policy support is most visible in the Asia Pacific. China reimburses up to 30% of swap-station capex under the “dual-carbon” framework, and India’s Ministry of Power issued January 2025 guidelines that target 26,000 swap kiosks by March 2026. The European Union’s Regulation 2023/1542 introduces a digital battery passport by 2027, making centralized battery ownership attractive for compliance [2]European Parliament, “Regulation (EU) 2023/1542 on Batteries and Waste Batteries,” eur-lex.europa.eu. US state fleets receive tax credits when opting for certified battery-leasing schemes. Together, these programs address the chicken-and-egg dilemma of early infrastructure funding, derisking capital deployment, and accelerating demand.

Rapid Rollout of Swap-Station Networks by OEMs & Start-ups

CATL and Sinopec announced a program to deploy 10,000 swap stations across mainland China, leveraging existing fuel-station real estate for accelerated coverage. NIO’s fourth-generation station processes 480 swaps a day and accommodates multi-brand packs, illustrating technical maturity and throughput gains [3]NIO Inc., “NIO Fourth-Generation Battery Swap Station Launch,” nio.com. Modular-pod innovators such as Ample secured corporate capital from Mitsubishi to export micro-station concepts to Europe and the United States. Higher network density dilutes range anxiety and normalizes battery rental in urban commute patterns. Yet, capital intensity keeps entry barriers high for small players without downstream energy partners.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of Cross-OEM Battery Standards | -4.2% | Global, higher for multi-brand fleets | Medium term (2-4 years) |

| Capex-Intensive Swap-Station Deployment | -3.8% | Global, steeper in developed markets | Short term (≤ 2 years) |

| Ultra-fast-Charging Competition | -3.1% | Developed regions with dense chargers | Medium term (2-4 years) |

| Residual-Value Uncertainty for Leased Batteries | -2.9% | North America & Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Lack of Cross-OEM Battery Standards

ANSI’s 2024 gap analysis identified 37 interoperability deficiencies across EV systems, 14 of which relate directly to battery geometry, communication, and safety. This fragmentation pushes rental companies to stock multiple pack formats, inflating working capital and shrinking asset-turnover ratios. Fleet buyers also fear lock-in, delaying volume commitments until a universal connector emerges. China’s standard-size modules show how harmonization multiplies swap-station throughput, but global consensus remains elusive.

Capex-Intensive Swap-Station Deployment

A fully automated high-capacity swap hub can require USD 3.5 million in equipment, civil works, and grid upgrades when built in tier-one urban centers, according to CATL supplier tenders. Smaller 6-battery kiosks still cost more than USD 150,000, stretching payback periods to 5-7 years under present utilization. Such front-loaded expenditure favors power-sector incumbents and petroleum retailers with existing land banks, slowing greenfield rollouts in markets where zoning or grid permits are onerous. Government co-funding lowers the hurdle, yet capital scarcity keeps several regional start-ups in pilot mode.

Segment Analysis

By Rental Type: Subscriptions Anchor Scale but Pay-Per-Use Gains Traction

Subscriptions delivered 85.34% of 2024 revenue as fleet operators locked in multi-year contracts that stabilized cash flow for service providers. Under these tiers, pricing typically bundles battery access, predictive maintenance, and end-of-life recycling, insulating users from residual-value risk. The automotive battery rental market size for subscription plans is forecast to reach USD 0.97 billion by 2030 at a 26.2% CAGR. Emerging pay-per-use schemes—enabled by IoT metering and app-based billing—record a 34.41% surge, riding on episodic users such as ride-hail drivers or municipal fleets that require flexibility during seasonal peaks.

Growing acceptance of pay-per-use stems from transparent unit economics: operators charge per kWh exchanged or per swap event, mirroring fuel-card logic familiar to fleet managers. CATL’s Choco-Swap pilot advertises a CNY 599 monthly tier for high-kilometer taxis alongside a CNY 0.20/kWh ad-hoc tariff, blending subscription stability with variable demand capture. Hybrid pricing variants are likely to dominate as providers introduce loyalty discounts that encourage predictable demand while keeping entry barriers low for new users.

By Battery Type: Solid-State Poised to Disrupt Incumbent Lithium-Ion

Lithium-ion packs controlled 96.25% of 2024 revenue, owing to well-established supply chains and a dramatic 20% price drop between 2023-2024. The automotive battery rental market share of lithium-ion technology remains secure over the near term, yet the automotive battery rental market size attributable to solid-state units could exceed USD 0.12 billion by 2030, given an 88.95% CAGR. Toyota targets mass-production readiness by 2028, while BYD and CATL have public roadmaps for earlier limited deployment.

Solid-state gains derive from 2-3× energy density and intrinsic thermal stability, permitting pack miniaturization without compromising range. Gogoro and ProLogium unveiled a swappable solid-state scooter battery prototype that achieves 220 Wh/kg, 45% higher than today’s cobalt-rich lithium-ion cells. The rental model mitigates early-adopter risk, allowing providers to monetize premium energy density even if cell prices remain above USD 200/kWh in initial batches, whereas vehicle OEMs would face affordability constraints.

By Vehicle Type: Commercial Fleets Drive the Next Wave of Growth

Passenger cars contributed 74.25% of the 2024 turnover, reflecting China’s early adoption of consumer-oriented BaaS. Nevertheless, commercial vans, trucks, and buses are accelerating at a 34.13% CAGR toward 2030. High utilization amplifies the cost advantage of swap-based downtimes under 110 seconds, outperforming 400 kW liquid-cooled charging that still sidelines vehicles for 25 minutes. For logistics carriers clocking 200-300 km per shift, this productivity delta outweighs the subscription premium.

Two- and three-wheelers capture wallets in South and Southeast Asia, where battery cost equals up to 40% of vehicle retail price. Government-issued interoperability rules in India’s 2025 policy framework oblige OEMs to adopt standardized pack housings, catalyzing fast-cycle rentals for food-delivery gig workers.

Note: Segment shares of all individual segments available upon report purchase

By End User: Fleet Dominance Sustained, Private Uptake Builds

Fleet operators managed 84.12% of 2024 demand because they unlock volume discounts, professional maintenance protocols, and data-rich telematics that maximize battery utilization. Cost accountants precisely quantify the 8-10% fuel-and-maintenance savings attainable when swapping replaces hybrid fast charging cycles. Honda-Mitsubishi’s ALTNA delivers BaaS bundled into the N-VAN e: launch, reflecting how OEMs themselves seek annuity revenues instead of one-off sales.

Private consumers, although currently niche, post the fastest trajectory at 32.87% CAGR. Hyundai’s Casper EV lease in Korea removes the battery from the sticker price, lowering entry cost by more than 25% while retaining the same monthly outlay as petrol micro-cars once the subscription is included. Growth depends on dense swap-station coverage and transparent lifetime pricing so that owners see a payback within 4 years versus outright purchase.

Geography Analysis

Asia Pacific generated 65.25% of global revenue in 2024 and should preserve a commanding lead through 2030 with a 31.45% CAGR. China’s industrial policy wraps subsidies, land grants, and grid-fee rebates into a cohesive package that accelerates CATL-Sinopec’s 10,000-station blueprint. India’s Ministry of Power aims to scale kiosk density tenfold within eighteen months, leveraging Make-in-India battery production to lower cost curves. Southeast-Asian ride-hail fleets increasingly bundle subscription plans for e-bikes that require less than one square meter of swap-station footprint, allowing operators to penetrate congested urban districts where charging bays are scarce.

Europe ranks second by value thanks to stringent circular-economy mandates that make professional battery stewardship a compliance necessity. The automotive battery rental market size for the region is forecast to reach USD 0.24 billion by 2030 with a 27.4% CAGR. Early institutional demand comes from leasing giants integrating BaaS into vehicle-as-a-service bundles. Stellantis signed frame agreements for 500,000 vehicles with Ayvens that include swap-compatible battery leasing, a strategic hedge against depreciation risk, and an avenue to capture post-sale service margins. Municipal bus fleets in France and Germany also pilot fixed-route swap depots to avoid midday charging that would otherwise disrupt timetables.

North America lags in infrastructure density but yields high-margin projects in last-mile and drayage ports where downtime penalises asset turns. Ample’s collaboration with Mitsubishi Corporation established modular swap pods outside San Francisco, cutting refuel time for electric delivery vans to five minutes. Regulatory alignment remains piecemeal; however, California’s incentive package for zero-emission drayage could spark wider adoption. The Middle East and Africa sit in exploratory stages yet show keen interest from oil-and-gas incumbents seeking to repurpose forecourts for fast-cycle battery exchange to future-proof downstream assets.

Competitive Landscape

Competition is moderate, with regional clusters consolidating around platform economics rather than traditional manufacturing volume. CATL, NIO, and Gogoro represent first-mover ecosystems that combine cell production, leasing, and software, raising the capital barrier for late entrants. Their supply-chain control allows them to underwrite uptime guarantees that pure-play station operators cannot match. NIO surpassed 2,300 swap sites in mainland China by May 2025, covering 90% of highway service areas and significantly eroding consumer range anxiety.

Start-ups carve niches by offering cross-OEM compatibility. Ample’s robotic pod swaps an empty pack in less than five minutes and can reconfigure for different vehicle footprints overnight via interchangeable adapter plates. Battery Smart in India focuses on low-capex two-wheeler kiosks, extracting value from extraordinarily high utilization rates in food-delivery fleets, though it must secure continuous cell supply against a backdrop of aggressive domestic demand.

Legacy OEMs increasingly move beyond pilot programs. Stellantis’ Free2move mobility brand formed a pact with Ample to evaluate fast-deployment stations in Madrid, laying the groundwork for European expansion once a favorable regulatory template emerges. Ford and General Motors each filed patents for slide-in battery trays, signaling intent to standardize chassis platforms with swap-readiness for both retail and fleet buyers. Patent thickets could become a strategic lever, yet standards alliances may neutralize proprietary advantages if governments opt for open architectures to accelerate climate goals.

Automotive Battery Rental Industry Leaders

-

Ample Inc.

-

NIO Limited

-

Contemporary Amperex Technology Co., Limited (CATL)

-

Gogoro Inc.

-

Sun Mobility Pvt Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Hyundai launched a battery lease for the Casper EV, separating pack cost from vehicle price to undercut combustion rivals.

- September 2024: Vidyut and JSW MG Motor India introduced a passenger-car battery rental program covering MG’s electric portfolio.

- June 2024: Honda and Mitsubishi Corporation established ALTNA Co., Ltd. to deliver integrated battery leasing, monitoring, and recycling for the Honda N-VAN e.

- February 2024: Stellantis and Ayvens finalized a frame deal for up to 500,000 vehicles with embedded battery-leasing options across Europe by 2026.

Global Automotive Battery Rental Market Report Scope

The automotive battery rental service offers users the option to rent a battery over a specific time frame or through a subscription model. This convenient service allows users to access a reliable and fully charged battery as and when needed without the commitment of outright ownership of battery.

The automotive battery rental market is segmented by rental type, battery type, vehicle type, and geography. By rental type, the market is segmented into Subscription and Pay-Per-Use. By battery type, the market is segmented into Lead Acid Battery, Lithium-Ion Battery, and Other Battery Types. By vehicle type, the market is segmented into passenger cars and commercial vehicles. By Geography, the market is segmented into North America, Europe, Asia-Pacific, and Rest of the World. For each segment, the market sizing and forecast have been done based on the value (USD).

| Subscription |

| Pay-Per-Use |

| Lead-Acid |

| Lithium-Ion |

| Solid-State |

| Others |

| Two & Three Wheelers |

| Passenger Cars |

| Commercial Vehicles |

| Fleet Operators |

| Private Consumers |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Rental Type | Subscription | |

| Pay-Per-Use | ||

| By Battery Type | Lead-Acid | |

| Lithium-Ion | ||

| Solid-State | ||

| Others | ||

| By Vehicle Type | Two & Three Wheelers | |

| Passenger Cars | ||

| Commercial Vehicles | ||

| By End User | Fleet Operators | |

| Private Consumers | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the expected growth rate of the automotive battery rental market through 2030?

The market is projected to grow at a 28.36% CAGR, rising from USD 0.33 billion in 2025 to USD 1.15 billion in 2030.

Why does Asia Pacific dominate automotive battery rental adoption?

Government subsidies for swap infrastructure, high urban density, and vertically integrated battery supply chains give Asia Pacific 65.25% global revenue in 2024 and sustain the region’s 31.45% CAGR outlook.

How do subscription and pay-per-use models differ?

Subscriptions bundle battery access, maintenance, and recycling into a flat monthly fee that simplifies budgeting, whereas pay-per-use charges per swap or kilowatt-hour appeal to fleets with variable utilization patterns.

Will solid-state batteries disrupt current rental economics?

Solid-state packs promise 2-3× energy density and improved safety. Their forecast 88.95% CAGR suggests rental providers will adopt them quickly, but lithium-ion remains dominant until mass-production costs fall.

Page last updated on: