Automotive Adhesive Tape Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

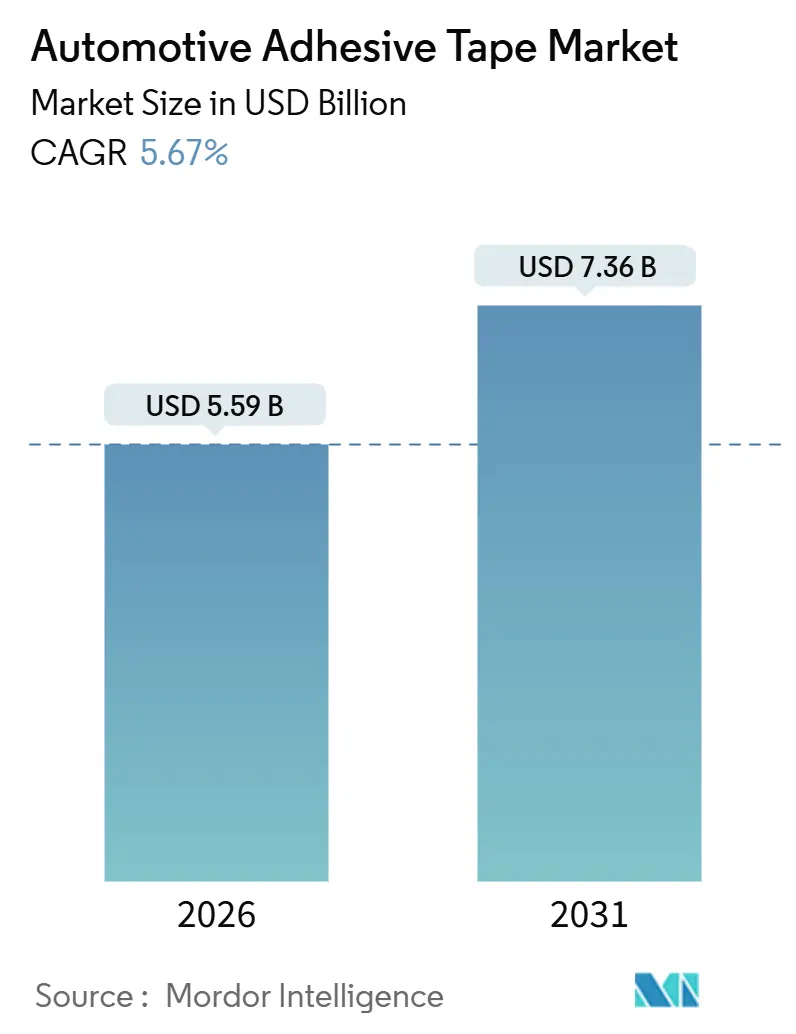

| Market Size (2026) | USD 5.59 Billion |

| Market Size (2031) | USD 7.36 Billion |

| Growth Rate (2026 - 2031) | 5.67% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Adhesive Tape Market Analysis by Mordor Intelligence

The Automotive Adhesive Tape Market size is estimated at USD 5.59 billion in 2026, and is expected to reach USD 7.36 billion by 2031, at a CAGR of 5.67% during the forecast period (2026-2031). Demand pivots toward bonding solutions that integrate electric-vehicle battery packs, advanced driver-assistance sensors, and mixed-material body structures. Electronics applications, which already account for almost half of global revenue, capture the strongest momentum as thermal-management, EMI-shielding, and wire-harness tasks migrate from mechanical fastening to specialty tapes. OEM lightweighting programs reinforce uptake because a single kilogram eliminated from fasteners can extend battery-electric driving range. Geographically, Asia-Pacific anchors more than half of the current volume owing to China’s cell-manufacturing scale and India’s light-vehicle expansion, while Europe and North America concentrate on high-margin specialty grades that satisfy premium OEM specifications. At the chemistry level, acrylic adhesives dominate because they blend UV stability, wide service-temperature bandwidth, and compatibility with steel, aluminum, and composite substrates.

Key Report Takeaways

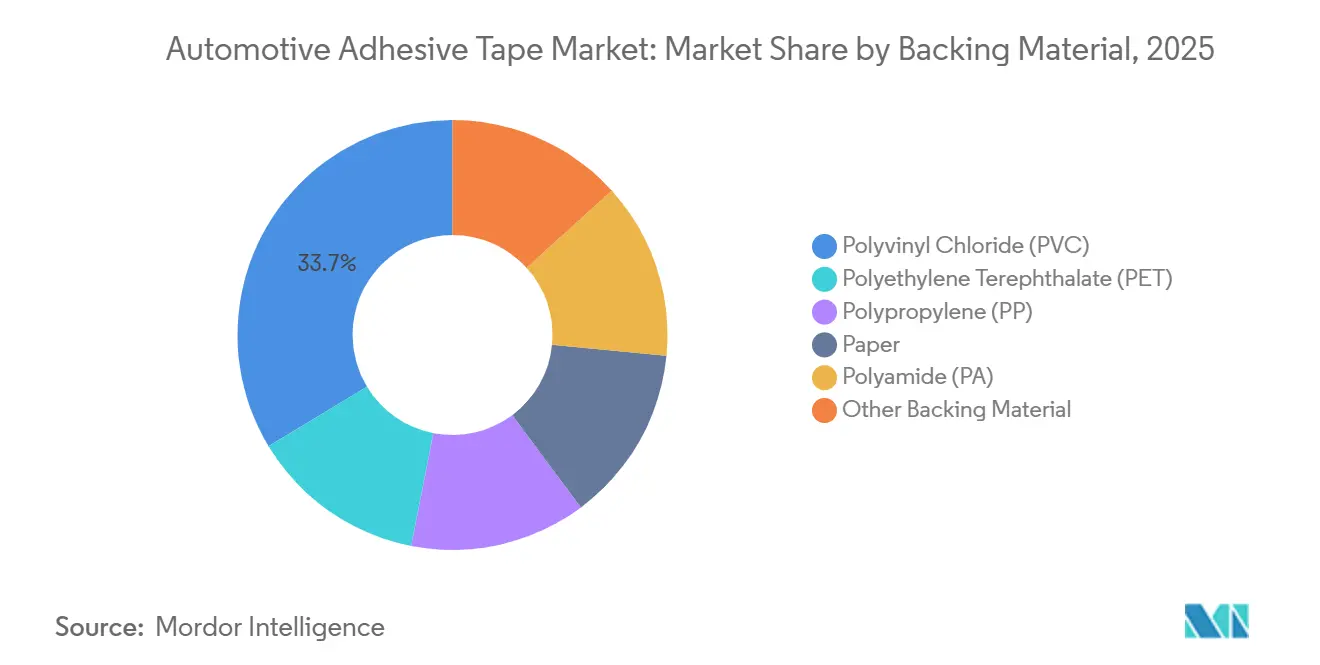

- By backing materials, polyvinyl chloride held 33.65% of 2025 revenue, while polypropylene is forecast to grow at 6.13% through 2031, the fastest among backing materials.

- By adhesive types, acrylic captured 64.10% of 2025 revenue and is expected to expand at a 6.03% CAGR, the leading trajectory within adhesive types.

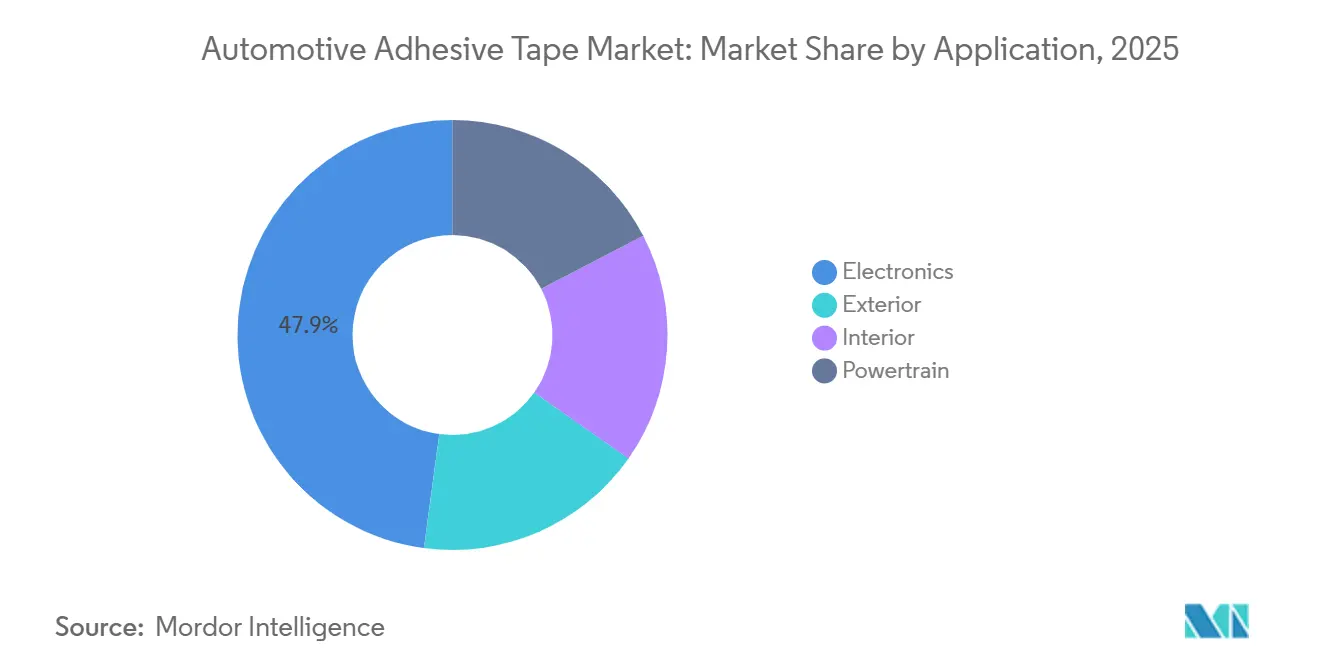

- By applications, electronics accounted for 47.89% of 2025 revenue and showed the highest growth at 6.29% through 2031 among all applications.

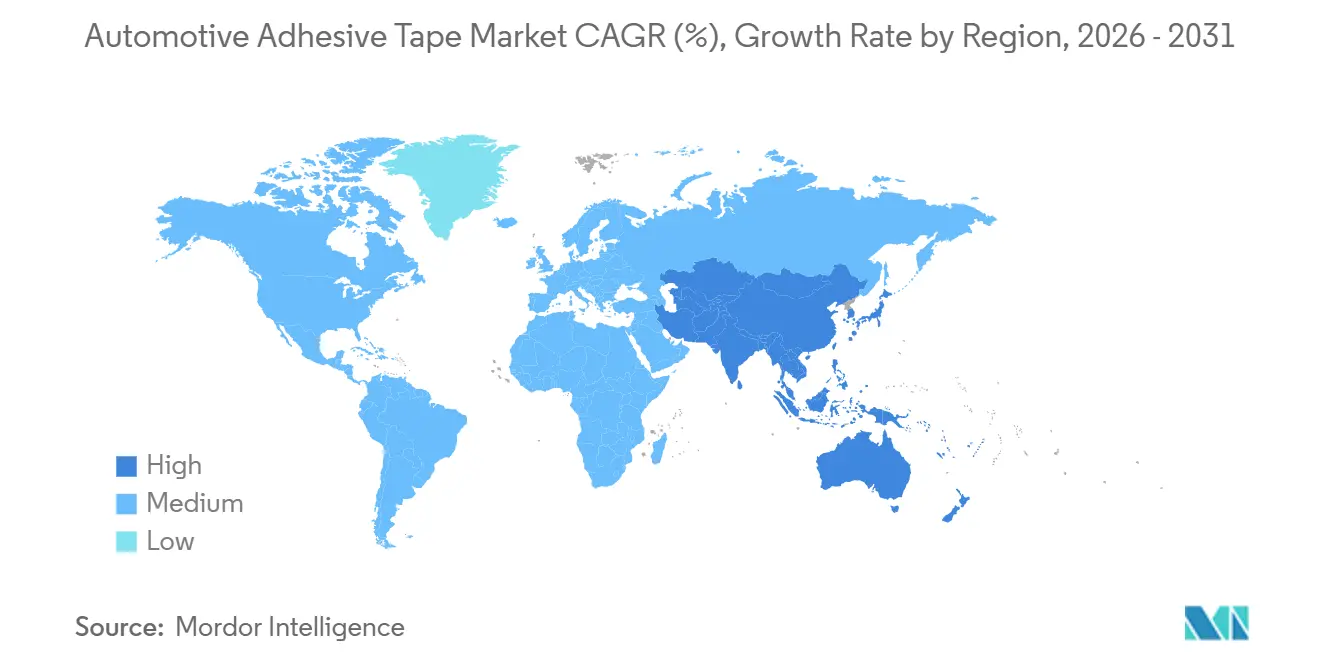

- By geography, Asia-Pacific commanded 53.26% of the 2025 volume and is projected to sustain a 5.90% CAGR, outpacing other regions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Automotive Adhesive Tape Market Trends and Insights

Drivers Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV battery thermal-management tape demand | +1.2% | Global, with concentration in China, South Korea, Germany, United States | Medium term (2-4 years) |

| Lightweighting replacing mechanical fasteners | +0.9% | North America and EU, spill-over to APAC premium segments | Long term (≥ 4 years) |

| ADAS sensor EMI-shielding tape adoption | +0.8% | Global, led by markets with Level 2+ penetration (EU, US, Japan, South Korea) | Short term (≤ 2 years) |

| Composite materials need compatible tapes | +0.7% | Europe and North America luxury OEMs, emerging in China NEV brands | Long term (≥ 4 years) |

| Modular vehicle architectures enable disassembly tapes | +0.5% | EU-led with right-to-repair mandates, early adoption in Scandinavia and Germany | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EV Battery Thermal-Management Tape Demand

As lithium-ion packs increasingly demand continuous heat dissipation to prevent thermal runaway, thermally conductive, flame-retardant tapes have surged beyond their traditional powertrain applications. Tesa's ACXplus line adeptly bonds cooling plates directly to cell modules at a consistent 180 °C, eliminating the need for mechanical clamps[1]tesa SE, “ACXplus Thermal Management Solutions for Battery Applications,” tesa.com. Lohmann's DuploFLEX solutions not only meet the stringent UL 94 V-0 standards but also maintain a thickness variation of less than 5% across one-meter widths, a critical requirement for automated dispensing systems[2]Lohmann GmbH & Co. KG, “DuploFLEX Portfolio for Battery Thermal Interface,” lohmann-tapes.com. Collectively, these advancements are steering the market towards specialty tape formulations, which command prices significantly outpacing traditional interior-trim grades.

Lightweighting Replacing Mechanical Fasteners

In response to Corporate Average Fuel Economy mandates in the U.S. and Euro 7 regulations in Europe, automakers are increasingly replacing rivets and screws with structural adhesive tapes. Ford, for instance, lightened the 2024 F-150 Lightning's body-in-white by using adhesive tape to bond roof panels. This change not only lightened the vehicle but also significantly reduced the bonding cycle time. The use of adhesive tapes on assembly lines boosts throughput by evenly distributing stress, preventing rework due to heat distortion, and reducing tool maintenance costs. In a similar vein, Avery Dennison is capitalizing on consistent acrylic chemistries across both original equipment (OE) and graphic films, effectively distributing research and development costs across diverse revenue streams. Interior suppliers are also hopping on this bandwagon, using double-coated PET tapes to bond decorative trims. This not only conceals visible fasteners but also minimizes squeaks, elevating cabin refinement for luxury brands.

Composite Materials Need Compatible Tapes

Luxury OEMs are increasingly turning to carbon-fiber and glass-fiber composites for applications like doors, roofs, and battery enclosures. However, these materials pose a challenge: they resist wet-out by traditional epoxy tapes. Enter Sika with its SikaForce polyurethane tape. This innovative tape not only cures at ambient temperatures but also achieves strong lap-shear strength on carbon fiber, making it a boon for out-of-autoclave processes. In a testament to the tape's efficiency, BMW’s iX utilizes it in its roof-panel assembly. This choice has led to the elimination of rivets and a significant reduction in the overall build time. Yet, challenges remain. Surface energies dipping below 40 dynes/cm necessitate specially engineered adhesives for low-energy plastics. Failing to do so risks bond delamination during thermal cycling. To further enhance durability, polyamide liners are employed, shielding against galvanic corrosion when composites come into contact with aluminum frames. As the use of composites in premium EVs continues to rise, suppliers demonstrating compatibility are positioning themselves advantageously for next-generation platforms.

ADAS Sensor EMI-Shielding Tape Adoption

In 2025, global light-vehicle production incorporated Level 2+ driver-assistance functions. Each radar or lidar module in these vehicles necessitated shielding tape. 3M’s copper-foil tape, boasting a sheet resistance below 0.05 Ω/m² and capable of withstanding solder-reflow peaks of 150 °C, met the stringent requirements set by Tesla for its Model 3 radar housings. Meanwhile, Nitto Denko, with its nickel-coated polyester solutions, expanded coverage to counter sub-100 kHz magnetic interference, effectively shielding 48-V electrical architectures. Tape-based shielding not only weighs less and occupies reduced volume compared to metal housings, but also allows for greater design flexibility in compact bumper corners. Additionally, the ease of serviceability is a significant advantage; technicians can swiftly replace adhesive gaskets over machined covers, enhancing dealer throughput and reducing warranty costs.

Restraints Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Petrochemical feedstock price volatility | -0.6% | Global, acute in regions dependent on imported crude (Europe, Japan, South Korea) | Short term (≤ 2 years) |

| PFAS regulatory scrutiny on adhesives | -0.4% | North America and EU, potential spill-over to APAC export-oriented producers | Medium term (2-4 years) |

| Poor recyclability of multi-material tapes | -0.3% | EU-focused due to End-of-Life Vehicles Regulation, expanding to Japan and South Korea | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Petrochemical Feedstock Price Volatility

Crude oil fluctuations directly influence the prices of polypropylene and polyethylene terephthalate films, as both resins are products of naphtha cracking. Polypropylene resin prices have surged, leading converters to face margin compression. While automotive contracts typically lock in tape prices for a year, resin suppliers adjust their prices quarterly. This discrepancy heightens the risk for mid-scale converters lacking hedging strategies. Avery Dennison has adopted tolling arrangements, transferring resin procurement responsibilities to OEMs, thereby reducing its risk. However, regional specialists continue to face vulnerabilities. The unpredictable nature of resin costs complicates capacity-planning decisions, causing delays in investments for solvent-free coating lines, which could hasten the adoption of polypropylene.

PFAS Regulatory Scrutiny on Adhesives

In October 2024, the U.S. EPA proposed a CERCLA designation for PFOA and PFOS, imposing strict liabilities on manufacturers and escalating costs for legacy cleanups. Following suit, Europe unveiled in February 2025 a strategy to outlaw most non-essential PFAS applications within a five-year window. While fluorinated adhesives boast superior resistance to oils and solvents, their fluorine-free counterparts exhibit reduced peel strength on low-energy plastics. Reformulating these adhesives not only incurs added research and development costs but might also necessitate redesigning joint geometries to uphold durability. Moreover, compliance transcends mere chemistry; the obligation to report PFAS usage dating back to 2011 introduces significant legal and administrative challenges, particularly burdensome for converters without dedicated regulatory teams.

Segment Analysis

By Backing Material: PVC Still Leads but PP Gains

PVC held 33.65% of 2025 revenue because it balances cost, conformability, and flame retardancy, especially for wire-harness wrapping inside the automotive adhesive tape market. Polypropylene’s lighter basis weight, however, propels a 6.13% growth rate as every gram saved in tape backing supports OEM lightweight targets. Avery Dennison's polypropylene film not only cut material spending but also adhered to interior flammability norms, leading several European programs to pivot from PVC. In 2024, Lohmann introduced a bio-based PP backing, aligning with the rising trend of scope-3 emission audits and aiding suppliers in retaining their approved-vendor status with sustainability-centric OEMs.

Throughput is a key focus in the segment's competitive discussions. A polypropylene tape yields more linear meters per master roll compared to a PVC tape, leading to reduced freight costs per unit area and enhanced line productivity in the automotive adhesive tape sector. While PET holds a consistent position in exhaust-adjacent heat zones, PVC outperforms in under-body areas due to its chlorine content, which curbs combustion without incurring additive costs. Polyamide carves out a niche for ultra-high-temperature joints surpassing 200 °C.

Note: Segment shares of all individual segments available upon report purchase

By Adhesive Type: Acrylic Dominance Continues

Acrylic formulations captured 64.10% of 2025 and are expected to expand at a 6.03% CAGR, thanks to broad substrate compatibility and zero-VOC water-borne processing that simplifies Rule 1151 and EU 2004/42/EC compliance. 3M’s 300LSE series boasts strong peel strength on untreated polypropylene. Notably, it eliminates the need for corona pre-treatment, resulting in time savings in facilities operating on a 60-second takt time. Silicone tapes, maintaining their dominance at temperatures exceeding 180 °C, are pivotal in applications like turbocharger heat shields and inverter dampers. Meanwhile, polyurethane solutions stand out for their ability to absorb impact energy in composite panels, effectively reducing peak stress compared to traditional epoxy bonds.

Nitto Denko, in 2025, unveiled a latent-hardener epoxy tape that achieves a significant portion of its ultimate bond strength within four hours under ambient conditions. This rapid bonding capability diminishes reliance on ovens and paves the way for just-in-time logistics. While these chemical advancements solidify acrylics' leading position, they also carve out opportunities for specialized formulations tailored for high-temperature or structural applications in the automotive adhesive tape sector.

By Application: Electronics Capture Nearly Half of All Value

Electronics applications accounted for 47.89% of 2025 revenue and expanded at a 6.29% CAGR, the highest among all use cases in the automotive adhesive tape market. Battery-electric vehicles, integrating roughly 3 km of wiring—twice that of their combustion counterparts—demand flame-retardant cloth tapes, specifically rated for 150 °C under FMVSS 302. While the phase-out of traditional engines sees a decline in powertrain usage, the need for potting and damping in electric motors somewhat compensates for the reduced demand in gaskets. Interior trims are witnessing growth, as foam tapes increasingly replace clips, effectively minimizing squeak-and-rattle issues. In contrast, exterior attachment tapes are seeing more modest growth, attributed to their already mature market penetration.

The premium pricing of electronics underscores their market leadership. For instance, thermal-management tapes command significantly higher prices compared to standard interior tapes. This price disparity incentivizes suppliers to focus on battery and sensor applications. Furthermore, Saint-Gobain’s silicone foam Norseal, designed to mitigate inverter vibrations between 500 Hz and 2 kHz, underscores the evolving sub-uses in electronics that uphold their premium pricing.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Asia-Pacific contributed 53.26% of global volume in 2025 and is forecast to grow 5.90% annually through 2031. This growth is driven by the sale of new energy vehicles in China and a substantial consumption of thermal tape at CATL’s single Ningde site. Following closely, India is set to grow, thanks to localization incentives. These incentives impose duties on finished tapes but exempt raw materials, prompting converters to invest locally. Meanwhile, Japan and South Korea continue to be at the forefront of innovation. For instance, Nitto Denko’s graphene-enhanced thermal tape, boasting superior performance, commands a premium over conventional grades and has secured spots on premium EV platforms.

North America, with a notable revenue share, owes much of its buoyancy to Mexico’s assembly corridor. In 2024, Avery Dennison bolstered its Tijuana capacity by adding clean-room space, catering to the rising demand for electronics-grade tape. This move underscores the region's pivot towards more intricate value streams. Additionally, U.S. OEMs are leveraging long-term resin contracts to mitigate feedstock volatility, thereby safeguarding margins for converters operating North American coating lines. Europe, while accounting for a significant portion of 2025's revenue, grapples with challenges. Industrial electricity costs in Germany are significantly higher than in China. This disparity squeezes margins on commodity tapes, nudging converters to pivot towards high-specification products tailored for luxury brands.

In 2025, South America and the combined regions of the Middle-East and Africa accounted for a modest share of the total value. Brazil, buoyed by local outputs from Volkswagen and Fiat, registered growth. However, the market remains highly price-sensitive, showing a preference for PVC-backed tapes. The limited production of EVs in the region curtails the uptake of specialty grades, indicating a slower penetration of advanced electronics tapes in the automotive adhesive tape market.

Competitive Landscape

The automotive adhesive tape market is moderately consolidated. Suppliers are proactively adopting fluorine-free chemistries to sidestep impending PFAS bans. Additionally, they're developing recyclable mono-material tapes to align with the proposed EU End-of-Life Vehicle Regulation, which aims for material recovery by 2028.

As automakers streamline their global vendor lists to simplify operations, consolidation pressures in the market are set to heighten. Suppliers that can't manage simultaneous launches across three continents face potential disqualification. In contrast, those that provide joint-development, rapid prototyping, and localized clean-room capabilities are positioned to become preferred suppliers in the automotive adhesive tape arena.

Automotive Adhesive Tape Industry Leaders

3M

tesa Tapes (India) Private Limited

Nitto Denko Corporation

Avery Dennison Corporation

Lohmann Gmbh & Co. Kg

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Avery Dennison introduced pressure-sensitive tapes, labels, and reflective solutions tailored for electric-vehicle charging stations. This will affect the demand for automotive adhesive tape.

- June 2024: Avery Dennison launched a cell-wrapping tape portfolio engineered to mitigate arcing inside electric vehicle (EV) battery packs.

Global Automotive Adhesive Tape Market Report Scope

Automotive adhesive tapes replaced traditional joining methods, such as bolts, screws, or welding. Automakers can manufacture lightweight vehicles with increased fuel economy using adhesive tapes instead of mechanical fasteners.

The automotive adhesive tape market is segmented by backing material, adhesive type, application, and geography. By backing material, the market is segmented into polyethylene terephthalate (PET), polyvinyl chloride (PVC), polypropylene (PP), paper, polyamide, and other backing materials. By adhesive type, the market is segmented into epoxy, acrylic, polyurethane, silicon, and other adhesive types. By application, the market is segmented into exterior, interior, powertrain, and electronics. The report also covers the market size and forecasts for the automotive adhesive tape market for 18 major countries across the major regions. For each segment, the market sizing and forecasts are done on the basis of value (USD).

| Polyethylene Terephthalate (PET) |

| Polyvinyl Chloride (PVC) |

| Polypropylene (PP) |

| Paper |

| Polyamide (PA) |

| Other Backing Material |

| Epoxy |

| Acrylic |

| Polyurethane |

| Silicone |

| Other Adhesive Tape |

| Exterior |

| Interior |

| Powertrain |

| Electronics |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Backing Material | Polyethylene Terephthalate (PET) | |

| Polyvinyl Chloride (PVC) | ||

| Polypropylene (PP) | ||

| Paper | ||

| Polyamide (PA) | ||

| Other Backing Material | ||

| By Adhesive Type | Epoxy | |

| Acrylic | ||

| Polyurethane | ||

| Silicone | ||

| Other Adhesive Tape | ||

| By Application | Exterior | |

| Interior | ||

| Powertrain | ||

| Electronics | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large is the automotive adhesive tape market in 2026?

The automotive adhesive tape market size reached USD 5.59 billion in 2026, reflecting rapid electrification and light weighting demand.

Which backing material is growing fastest?

Polypropylene backing is forecast to expand 6.13% annually through 2031 as OEMs pursue mass reduction.

Why do electronics applications dominate tape demand?

Battery thermal management, wire-harness bundling, and sensor EMI-shielding together account for 47.89% of 2025 revenue and deliver the highest growth at 6.29% CAGR.

What role do acrylic adhesives play?

Acrylic chemistry holds 64.10% of 2025 revenue because it bonds diverse substrates, maintains UV stability, and meets zero-VOC regulations.

Which region leads consumption?

Asia-Pacific captured 53.26% of the 2025 volume, driven by China’s battery-cell manufacturing scale and India’s vehicle production growth.

How are PFAS regulations affecting tape suppliers?

Proposed bans in the United States and Europe are prompting formulators to shift toward fluorine-free chemistries, adding research and development and compliance costs that may compress margins.