| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| CAGR | 6.00 % |

| Fastest Growing Market | North America |

| Largest Market | Europe |

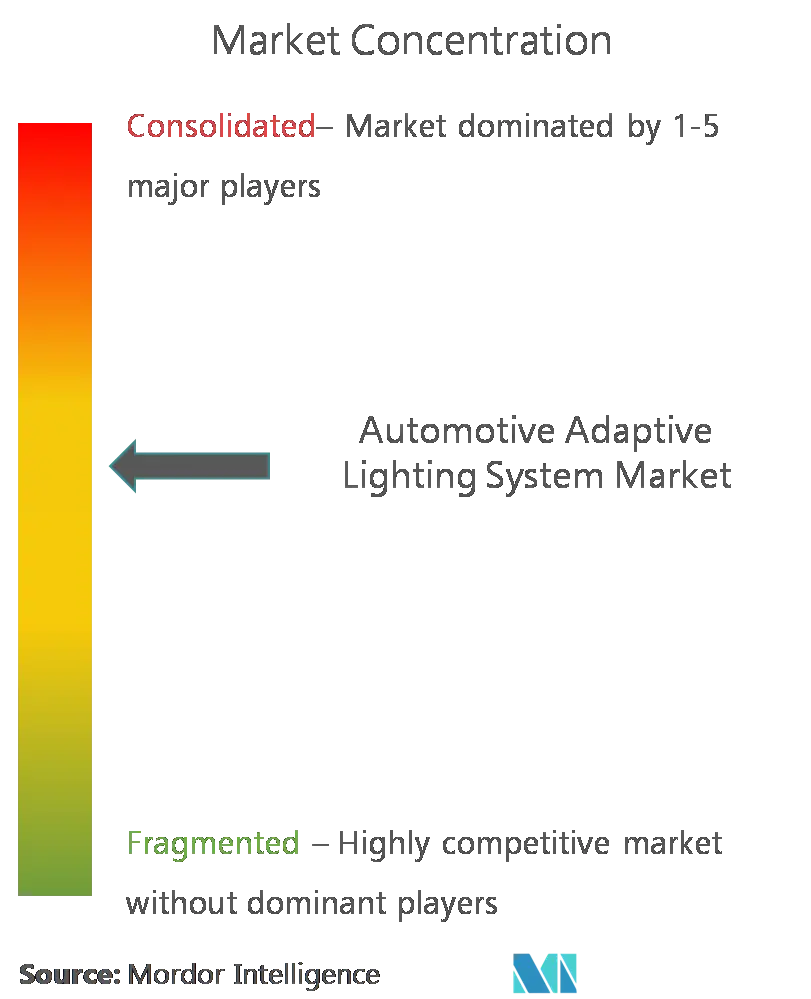

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order |

Automotive Adaptive Lighting System Market Analysis

The Automotive Adaptive Lighting System Market is expected to register a CAGR of greater than 6% during the forecast period.

The automotive lighting industry is undergoing a dramatic transformation driven by the rapid electrification of vehicles and changing consumer preferences. Electric vehicle sales witnessed unprecedented growth, surging by 60% in 2022 to surpass 10 million units globally, with one in seven passenger cars sold being an EV. This shift has catalyzed innovation in lighting technologies, as evidenced by LED headlight penetration exceeding 60% in conventional vehicles and reaching over 90% in electric vehicles during 2022. The integration of advanced lighting systems has become a crucial differentiator for automotive manufacturers, particularly in the premium and luxury segments where technological sophistication drives consumer purchase decisions.

The technological landscape of automotive lighting continues to evolve with breakthrough innovations in adaptive beam technology and smart lighting solutions. According to recent studies by the American Automobile Association, adaptive beam headlights demonstrate 86% better performance in providing consistent illumination compared to traditional systems, particularly in managing glare for oncoming traffic. This advancement has prompted major manufacturers to invest heavily in research and development, focusing on creating more sophisticated and efficient lighting solutions that enhance both safety and aesthetic appeal.

Manufacturing innovations have reached new heights in 2023, with several groundbreaking developments reshaping the automotive lighting industry landscape. In July 2023, Marelli introduced the revolutionary h-Digi microLED module, featuring approximately 40,000 LED pixels per vehicle, enabling fully adaptive and dynamic headlight operation with image projection capabilities. Similarly, the collaboration between Nichia Corporation and Infineon Technologies resulted in the industry's first fully integrated micro-LED light engine for high-definition adaptive driving beam applications, incorporating over 16,000 micro-LEDs on a thumbnail-sized surface area.

The market landscape is experiencing significant shifts as automotive manufacturers increasingly integrate advanced lighting systems into their standard offerings. This trend is exemplified by Buick's 2023 launch of the next-generation LaCrosse, featuring Matrix adaptive headlamps with 222 LED lighting sources and nine intelligent lighting modes. The industry's focus has expanded beyond basic illumination to encompass sophisticated features such as adaptive driving beams, construction and narrow-lane lighting, and intelligent motorway high-beam systems, reflecting the growing convergence of lighting technology with advanced driver assistance systems. The automotive LED lighting market is poised to benefit significantly from these advancements, as manufacturers continue to prioritize innovation in automotive smart lighting solutions.

Automotive Adaptive Lighting System Market Trends

Increasing Concerns About Road Safety and Government Lighting Requirements to Enhance Demand in the Market

The rising number of nighttime accidents and fatalities has become a major concern for transportation agencies worldwide, driving the demand for advanced automotive lighting systems. According to research by the National Safety Council (NSC), the rate of nighttime crashes is three times higher compared to crashes occurring during daylight hours, with particular challenges in avoiding collisions with wildlife, pedestrians, bicyclists, and roadside objects in dim light conditions. A comprehensive study by the American Automobile Association (AAA) demonstrated that smart headlights with adaptive driving beam (ADB) technology are up to 86% more effective at providing consistent illumination when encountering oncoming traffic compared to traditional headlights. The study further projected that ADB headlights could potentially reduce wildlife-related crashes by 18,000 annually, resulting in estimated savings of USD 500 million.

Government regulations and safety requirements are increasingly mandating the implementation of advanced lighting technologies in vehicles. For instance, the United States Department of Transportation's National Highway Traffic Safety Administration (NHTSA) recently approved the usage of adaptive driving beams (ADB), following similar regulations in Asia and Europe. This regulatory shift has prompted automotive manufacturers to enhance their lighting technologies, with companies like General Motors now producing vehicles equipped with ADB technology capable of generating 34 different beam patterns. Additionally, requirements for emergency stop signals (ESS) have been included in recent amendments across various regions, further emphasizing the importance of adaptive lighting systems in improving road safety. These regulatory changes are complemented by initiatives like the European Union's mandate requiring all new cars to be equipped with advanced safety systems, including intelligent speed assistance and emergency stop signals.

Understand The Key Trends Shaping This Market

Download PDF

Growing Adoption of New Technologies

The automotive industry is witnessing rapid technological advancement in lighting systems, particularly with the integration of automotive LED lighting market and advanced driver assistance systems (ADAS). In January 2023, Nichia Corporation and Infineon Technologies AG unveiled a groundbreaking high-definition light engine featuring more than 16,000 micro-LEDs for headlight applications, marking a significant leap in adaptive lighting technology. This innovation enables high-resolution light distribution up to twice as bright on a surface four times larger than previous top-tier systems, demonstrating the industry's commitment to pushing technological boundaries. The integration of these advanced lighting systems with ADAS features has become increasingly prevalent, with manufacturers focusing on developing solutions that combine safety, efficiency, and sophisticated lighting control.

The evolution of electric vehicles (EVs) has further accelerated the adoption of advanced lighting technologies. In 2022, LED headlight penetration exceeded 90% in the new energy vehicle category, significantly higher than the 60% penetration rate in conventional vehicles. This trend is supported by innovations such as Marelli's h-Digi microLED module, launched in July 2023, which enables fully adaptive, dynamic headlight operation and image projection while remaining cost-effective for a wider range of vehicles. The technology utilizes around 40,000 LED pixels per vehicle, allowing for very flexible low-beam and high-beam light distributions that adapt to various driving situations. These technological advancements are complemented by the development of sophisticated control systems, such as Porsche's new high-resolution HD matrix technology, which combines over 16,000 individually controllable micro-LEDs onto a surface area the size of a thumbnail, providing enhanced visibility at distances of up to 600 meters. The growing focus on automotive laser lighting is also contributing to advancements in the automotive lighting market, as manufacturers seek to enhance visibility and safety features in modern vehicles.

Segment Analysis: By Vehicle Type

Premium Vehicles Segment in Automotive Adaptive Lighting System Market

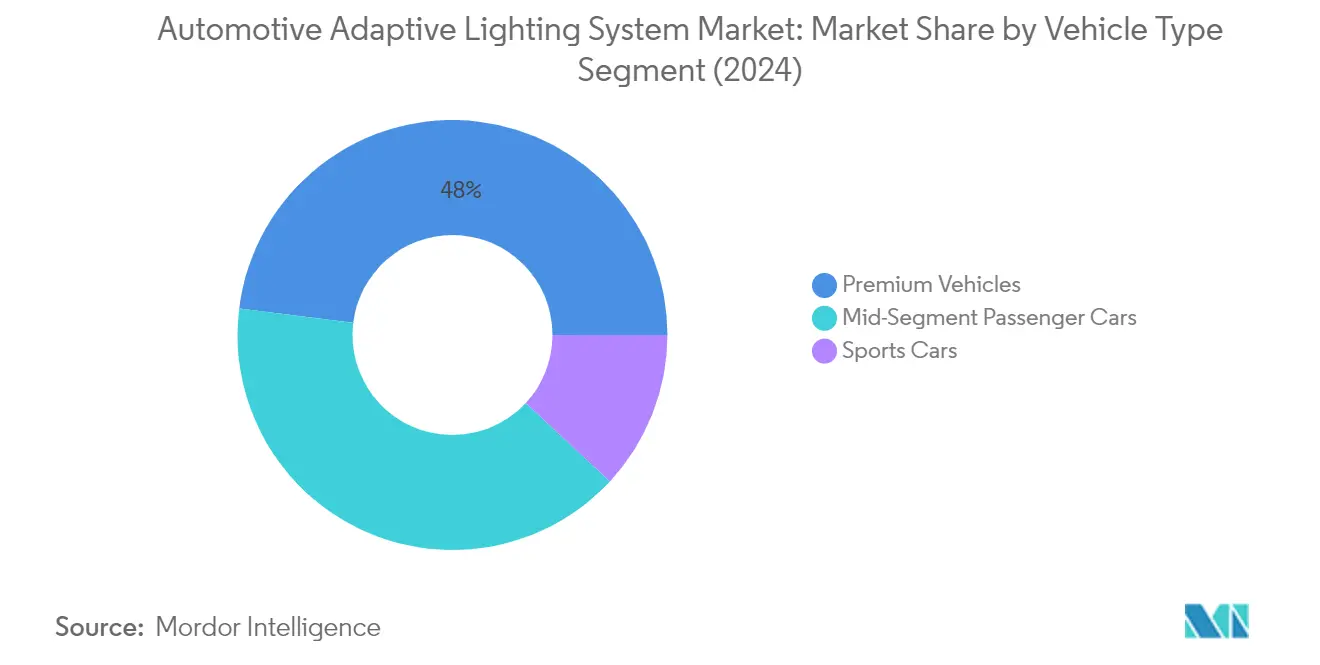

Premium vehicles continue to dominate the automotive lighting system market, commanding approximately 48% market share in 2024. This segment's leadership position is primarily driven by the increasing integration of advanced lighting technologies in luxury and high-end vehicles. Premium vehicle manufacturers are prioritizing innovative lighting solutions as a key differentiator in their offerings, with many models now featuring sophisticated adaptive matrix LED systems and dynamic lighting capabilities. The segment's growth is further supported by rising consumer demand for enhanced safety features and premium driving experiences, particularly in key markets like Europe and North America. Major luxury automakers are continuously introducing new models with advanced adaptive lighting systems, contributing to the segment's market dominance.

Mid-Segment Passenger Cars Segment in Automotive Adaptive Lighting System Market

The mid-segment passenger cars category is experiencing remarkable growth in the automotive lighting system market, with an expected growth rate of approximately 17% during 2024-2029. This accelerated growth is primarily driven by the increasing democratization of advanced safety features in mainstream vehicles. Automotive manufacturers are increasingly incorporating adaptive lighting systems in their mid-range models to enhance safety and improve the overall driving experience. The segment's growth is further fueled by advancing technology and decreasing component costs, making adaptive lighting systems more accessible to a broader consumer base. Additionally, stringent safety regulations and growing consumer awareness about advanced vehicle safety features are contributing to the increased adoption of adaptive lighting systems in mid-segment vehicles.

Remaining Segments in Vehicle Type

The sports cars segment, while smaller in market share, plays a significant role in driving innovation in automotive smart lighting systems. Sports car manufacturers often serve as early adopters of cutting-edge lighting technologies, helping to establish new trends and standards in the industry. These vehicles typically feature high-performance adaptive lighting systems that are specifically designed to enhance visibility during high-speed driving and challenging road conditions. The segment's influence extends beyond its market share, as innovations initially introduced in sports cars often trickle down to other vehicle segments, contributing to the overall advancement of automotive lighting technology.

Segment Analysis: By Type

Front Segment in Automotive Adaptive Lighting System Market

The front segment continues to dominate the automotive headlight system market, commanding approximately 98% market share in 2024. This overwhelming dominance is primarily attributed to the crucial role front adaptive lighting plays in enhancing visibility and safety during nighttime driving conditions. Front adaptive lighting systems are essential as they incorporate advanced features like automatic adjustment of light distribution based on driving conditions, speed, and oncoming traffic. These systems utilize sophisticated sensors and cameras to optimize illumination patterns, particularly useful when navigating curves, intersections, and varying weather conditions. The integration of LED and matrix LED technologies in front adaptive lighting has further strengthened this segment's position, offering superior illumination quality while consuming less energy. Major automotive manufacturers are increasingly incorporating these systems as standard features in their premium and mid-segment vehicles, reflecting the growing importance of front adaptive lighting in modern vehicle safety systems.

Rear Segment in Automotive Adaptive Lighting System Market

The rear segment is emerging as the fastest-growing segment in the automotive lighting market, projected to grow at approximately 24% during 2024-2029. This remarkable growth rate is driven by increasing awareness of rear-end collision prevention and the integration of smart lighting technologies in vehicle safety systems. Automotive manufacturers are investing heavily in developing advanced rear adaptive lighting solutions that can automatically adjust brightness and pattern based on following traffic and weather conditions. The adoption of sophisticated LED technology in rear lighting systems, coupled with the integration of adaptive brake light features that respond to emergency braking situations, is fueling this segment's growth. Furthermore, the increasing focus on vehicle aesthetics and the development of dynamic rear lighting patterns for improved visibility and style are contributing to the segment's rapid expansion in the market.

Segment Analysis: By Component Type

Lamp Assembly Segment in Automotive Adaptive Lighting System Market

The lamp assembly segment continues to dominate the automotive lighting system market, commanding approximately 51% market share in 2024. This segment's leadership position is attributed to its crucial role in the adaptive lighting system, where it is responsible for beam projection and maintaining proper road focus. The increasing adoption of LED technology in lamp assemblies has further strengthened this segment's position, with major luxury car manufacturers advancing their lamp assembly designs to incorporate sophisticated features. For instance, Porsche has developed next-generation light technology with high-resolution HD matrix technology, utilizing over 16,000 individually controllable micro-LEDs on a thumbnail-sized surface area. The segment is also witnessing strong growth momentum, projected to expand at around 16% annually through 2024-2029, driven by continuous technological innovations and increasing demand for advanced lighting solutions in premium and electric vehicles.

Sensor/Camera Segment in Automotive Adaptive Lighting System Market

The sensor/camera segment represents a critical component in automotive headlight system, playing a vital role in detecting oncoming traffic and adjusting headlamp functionality accordingly. These components are typically positioned near the rearview mirror and are essential for enabling features like automatic high-beam control and cornering light adjustment. The segment is experiencing robust growth as automotive manufacturers increasingly integrate advanced driver assistance systems (ADAS) with lighting controls. The technology allows for precise control of light distribution, helping to prevent glare for oncoming vehicles while maintaining optimal road illumination. Recent technological advancements have led to the development of more sophisticated sensor systems that can detect multiple variables including ambient light levels, vehicle speed, steering angle, and the presence of other vehicles, contributing to enhanced adaptive lighting performance.

Remaining Segments in Automotive Adaptive Lighting System Market by Component Type

The controller and other components segments play complementary roles in the automotive adaptive lighting ecosystem. The controller segment encompasses the electronic control units that process sensor inputs and manage the adaptive lighting system's response to various driving conditions. These controllers are becoming increasingly sophisticated, incorporating advanced algorithms for better light distribution control. The other components category includes essential elements such as stepper motors, wiring harnesses, and printed circuit boards (PCBs), which are crucial for the proper functioning of adaptive lighting systems. Both segments are witnessing technological advancements, particularly in terms of energy efficiency and integration capabilities with other vehicle systems, contributing to the overall evolution of automotive adaptive lighting solutions.

Segment Analysis: By Sales Channel

OEM Segment in Automotive Adaptive Lighting System Market

The Original Equipment Manufacturer (OEM) segment continues to dominate the automotive adaptive lighting system market, holding approximately 68% market share in 2024. This dominance is primarily driven by the increasing integration of advanced lighting technologies in new vehicle models directly from manufacturers. Major automotive OEMs are actively collaborating with lighting system suppliers to develop and implement innovative adaptive lighting solutions that enhance both safety and aesthetic appeal. The segment's strength is further reinforced by stringent safety regulations requiring advanced lighting systems in new vehicles, particularly in premium and luxury segments. Additionally, the growing trend of vehicle electrification has prompted OEMs to incorporate energy-efficient adaptive lighting systems as standard features in their electric vehicle offerings. The rise in consumer demand for vehicles equipped with advanced driver assistance systems (ADAS) has also contributed significantly to the OEM segment's market leadership, as adaptive lighting systems are increasingly being integrated into comprehensive ADAS packages.

Aftermarket Segment in Automotive Adaptive Lighting System Market

The aftermarket segment is emerging as the fastest-growing segment in the automotive adaptive lighting system market, projected to grow at approximately 17% during the forecast period 2024-2029. This remarkable growth is being driven by increasing consumer awareness about the benefits of adaptive lighting systems and their desire to upgrade existing vehicles with advanced lighting technologies. The segment is witnessing substantial innovation in retrofit solutions that make adaptive lighting systems more accessible to a broader range of vehicle owners. Market players are developing cost-effective aftermarket solutions that can be easily integrated into existing vehicle systems, making advanced lighting features available to vehicles that didn't originally come equipped with them. The growth is further supported by the rising demand for vehicle customization and enhancement, particularly in regions with a large base of older vehicles. Additionally, the expansion of online retail channels and the increasing availability of DIY installation kits are making aftermarket adaptive lighting systems more accessible to end-users.

Automotive Adaptive Lighting System Market Geography Segment Analysis

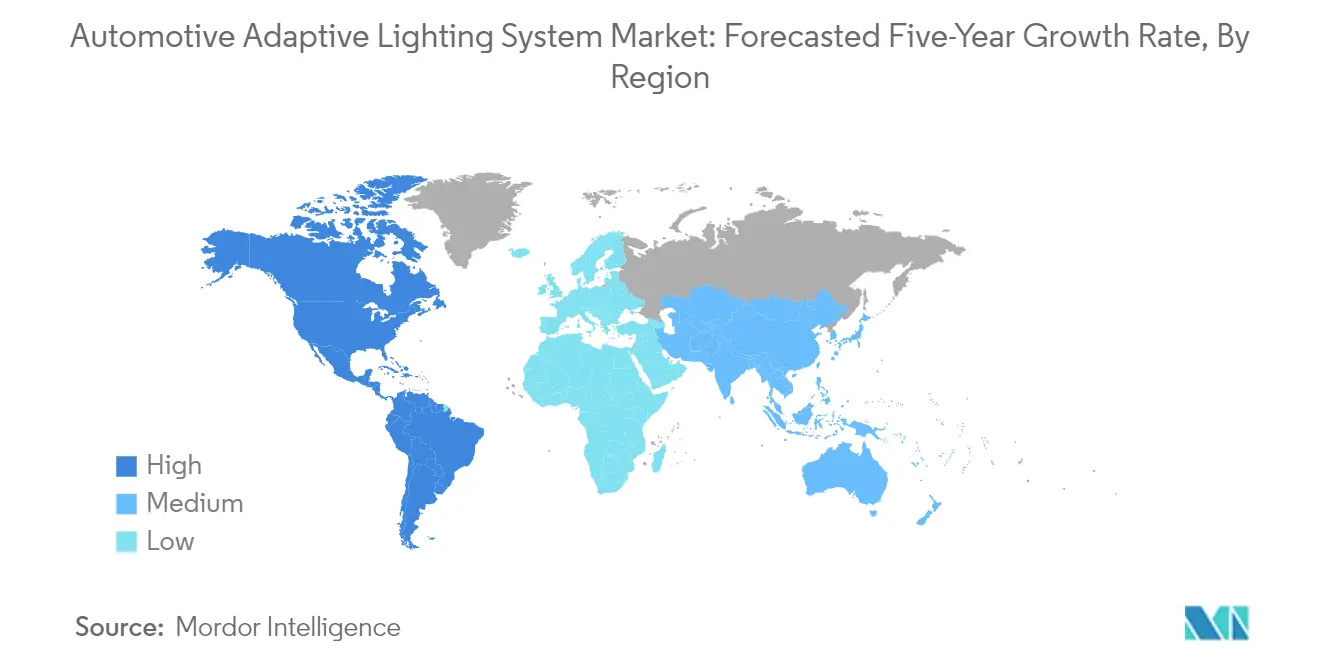

Automotive Adaptive Lighting System Market in North America

North America represents a significant market for automotive lighting systems, driven by stringent safety regulations and high adoption of premium vehicles. The United States and Canada are the key contributors to the regional market growth, with both countries showing strong demand for advanced automotive technologies. The region's market is characterized by the presence of major automotive manufacturers and their focus on incorporating innovative lighting solutions in their vehicle lineup. The increasing consumer awareness about vehicle safety features and the growing preference for luxury vehicles equipped with advanced lighting systems continue to drive market expansion across North America.

Automotive Adaptive Lighting System Market in United States

The United States dominates the North American market, holding approximately 24% share of the global automotive lighting market in 2024. The country's market leadership is attributed to its large automotive manufacturing base and high consumer spending power. The presence of stringent safety regulations by the National Highway Traffic Safety Administration (NHTSA) regarding vehicle lighting systems has been instrumental in driving adoption. American consumers' increasing preference for premium vehicles equipped with advanced safety features, combined with the presence of major automotive manufacturers and their focus on technological innovation, continues to drive market growth in the country.

Automotive Adaptive Lighting System Market in Canada

Canada emerges as the fastest-growing market in North America, with a projected growth rate of approximately 15% during 2024-2029. The country's market is driven by increasing vehicle safety regulations and growing consumer awareness about advanced automotive lighting technologies. Canadian automotive manufacturers are increasingly incorporating adaptive lighting systems in their vehicle models, particularly in premium and luxury segments. The government's focus on road safety and mandatory requirements for automated lighting systems in new vehicles has created a favorable environment for market growth.

Automotive Adaptive Lighting System Market in Europe

Europe represents a mature market for automotive lighting systems, with Germany, the United Kingdom, and France leading the regional adoption. The region's strong automotive manufacturing base, coupled with strict vehicle safety regulations, drives market growth. The presence of premium automotive manufacturers and their focus on incorporating advanced lighting technologies in their vehicles contributes significantly to market expansion. The European Union's emphasis on vehicle safety standards and energy efficiency requirements continues to shape the market landscape across the region.

Automotive Adaptive Lighting System Market in Germany

Germany maintains its position as the largest market in Europe, commanding approximately 21% of the European automotive lighting market share in 2024. The country's leadership is attributed to its strong automotive manufacturing sector, including industry giants like BMW, Mercedes-Benz, and Volkswagen. German automakers' focus on technological innovation and premium vehicle production, combined with high consumer acceptance of advanced automotive technologies, drives market growth. The presence of major lighting system manufacturers and ongoing research and development activities further strengthens Germany's position in the market.

Automotive Adaptive Lighting System Market in France

France demonstrates the highest growth potential in Europe, with a projected growth rate of approximately 15% during 2024-2029. The country's market is characterized by strong technological innovation and increasing adoption of advanced automotive smart lighting systems. French automotive manufacturers are actively incorporating adaptive lighting technologies in their vehicle models, particularly in the premium segment. The government's support for automotive innovation and stringent safety regulations continues to drive market growth in the country.

Automotive Adaptive Lighting System Market in Asia-Pacific

The Asia-Pacific region represents a dynamic market for automotive lighting industry systems, with China, Japan, India, and South Korea as key contributors. The region's rapid automotive industry growth, increasing vehicle production, and rising consumer awareness about advanced safety features drive market expansion. The presence of major automotive manufacturers and their focus on incorporating advanced lighting technologies in their vehicles contributes significantly to market growth.

Automotive Adaptive Lighting System Market in China

China maintains its position as the largest market in Asia-Pacific, driven by its massive automotive manufacturing capacity and growing demand for premium vehicles. The country's automotive industry's rapid technological advancement and increasing focus on vehicle safety features contribute to market growth. The presence of both domestic and international automotive manufacturers, coupled with government support for automotive technology innovation, strengthens China's market position.

Automotive Adaptive Lighting System Market in India

India emerges as the fastest-growing market in Asia-Pacific, driven by increasing vehicle production and rising consumer demand for advanced safety features. The country's automotive sector is witnessing significant technological advancement, with manufacturers increasingly incorporating adaptive lighting systems in their vehicle models. Government initiatives promoting vehicle safety and the growing presence of premium vehicle manufacturers contribute to market growth.

Automotive Adaptive Lighting System Market in Rest of the World

The Rest of the World region, comprising South America and the Middle East & Africa, represents an emerging market for automotive LED lighting industry systems. These regions are witnessing increasing adoption of advanced automotive technologies, driven by growing vehicle safety awareness and rising disposable incomes. South America, particularly Brazil, represents the largest market in this region, while the Middle East & Africa show the fastest growth potential. The presence of international automotive manufacturers and their focus on expanding their market presence contributes to regional market growth. Government initiatives promoting vehicle safety and increasing investments in automotive manufacturing capabilities further drive market expansion in these regions.

Get Analysis on Important Geographic Markets

Download PDF

Automotive Adaptive Lighting System Industry Overview

Top Companies in Automotive Adaptive Lighting System Market

The automotive lighting industry is characterized by the presence of established players like HELLA KGaA Hueck & Co., Valeo Group, Magneti Marelli SpA, Koito Manufacturing, and OSRAM Licht AG leading the innovation landscape. Companies are heavily investing in research and development to develop advanced lighting technologies, particularly focusing on LED and laser-based solutions for enhanced safety and performance. The industry witnesses continuous product launches incorporating smart features like automatic beam adjustment, pedestrian detection, and weather-adaptive functionalities. Strategic partnerships between lighting manufacturers and automotive OEMs have become increasingly common to develop customized solutions and ensure a steady market presence. Manufacturing facilities are being expanded, particularly in Asia-Pacific regions, to meet the growing demand and reduce operational costs while maintaining quality standards. Companies are also focusing on sustainable manufacturing practices and green development initiatives to align with global environmental regulations and consumer preferences.

Consolidated Market with Strong Regional Players

The automotive lighting market demonstrates a relatively consolidated structure with global conglomerates dominating the landscape, while regional specialists maintain strong positions in their respective markets. Major players leverage their extensive research capabilities, established distribution networks, and long-standing relationships with automotive manufacturers to maintain their market positions. The industry has witnessed significant merger and acquisition activities, particularly involving technology companies and traditional lighting manufacturers, aimed at combining expertise in electronics, software, and optical systems. These strategic consolidations have helped companies expand their product portfolios and geographical presence while accelerating technological advancement in adaptive lighting solutions.

The market is characterized by high entry barriers due to substantial capital requirements, technical expertise needs, and stringent quality standards. Companies with established manufacturing facilities and strong supplier relationships hold significant advantages in terms of cost management and production efficiency. Regional players, particularly in emerging markets, are gaining prominence through joint ventures and technology licensing agreements with global leaders, enabling them to serve local automotive manufacturers while gradually expanding their international presence. The industry's competitive dynamics are further shaped by the increasing integration of lighting systems with other vehicle safety and autonomous driving technologies.

Innovation and Integration Drive Market Success

Success in the automotive lighting industry increasingly depends on companies' ability to innovate while maintaining cost competitiveness and manufacturing efficiency. Incumbent players must focus on developing proprietary technologies, strengthening their intellectual property portfolios, and expanding their presence in emerging markets through strategic partnerships and localized production facilities. Companies need to invest in next-generation lighting technologies while maintaining strong relationships with automotive manufacturers and staying ahead of evolving safety regulations. The ability to integrate automotive lighting electronics with other vehicle technologies, particularly advanced driver assistance systems and autonomous driving capabilities, has become crucial for maintaining market relevance.

For new entrants and challenger brands, success lies in identifying specific market niches or technological gaps that can be addressed through innovative solutions. Companies must develop strong value propositions that differentiate them from established players, whether through cost advantages, superior technology, or specialized applications. Building relationships with tier-1 automotive suppliers and establishing credibility through quality certifications and compliance with international standards is essential. The increasing focus on electric vehicles and autonomous driving technologies presents opportunities for companies to develop specialized adaptive lighting solutions tailored to these emerging segments. Additionally, companies must carefully navigate regulatory requirements across different regions while maintaining flexibility to adapt to changing market demands and technological standards.

Automotive Adaptive Lighting System Market Leaders

-

Osram Licht AG

-

Valeo

-

Stanley Electric Co. Ltd.

-

HELLA KGaAHueck& Co.

-

Koninklijke Philips N.V.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Automotive Adaptive Lighting System Market News

- In February 2022, Opel and the Technical University of Darmstadt have announced a strategic partnership to jointly conduct research into new lighting technologies. The funded research will also seek to develop a self-adapting headlamp and tail-lamp system that adapts to its surroundings - providing optimal conditions based on the environment and traffic around the vehicle alongside other influencing factors.

- In July 2021, Hero Motorcorp introduced Hero Glamour Xtec, equipped with various advance features such as, LED headlights, Bluetooth connectivity, navigation, XPulse-derived digital instrument console as well as an integrated USB charger.

- In May 2021, Ford announced the launch of its new technologically advance headlight, which can use GPS to intelligently illuminate the road. It enhances the safety level and improves the night-time driving experience.

- In April 2021, Samsung launched its new automotive LED module optimized for intelligent headlight systems, PixCell LED, in order to enhance the road safety at night and during poor weather conditions.

Automotive Adaptive Lighting System Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

- 4.1 Market Drivers

- 4.2 Market Restraints

-

4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION

-

5.1 By Vehicle Type

- 5.1.1 Mid-Segment Passenger Cars

- 5.1.2 Sports Cars

- 5.1.3 Premium Vehicles

-

5.2 By Type

- 5.2.1 Front

- 5.2.2 Rear

-

5.3 By Component Type

- 5.3.1 Controller

- 5.3.2 Sensors/ Camera

- 5.3.3 Lamp Assembly

- 5.3.4 Others

-

5.4 By Sales Channel Type

- 5.4.1 OEM

- 5.4.2 Aftermarket

-

5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 India

- 5.5.3.2 China

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 Rest of the World

- 5.5.4.1 South America

- 5.5.4.2 Middle-East and Africa

6. COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

-

6.2 Company Profiles

- 6.2.1 HELLA KGaA Hueck & Co.

- 6.2.2 Hyundai Mobis

- 6.2.3 Valeo Group

- 6.2.4 Magneti Marelli SpA

- 6.2.5 Koito Manufacturing Co. Ltd

- 6.2.6 Koninklijke Philips N.V.

- 6.2.7 Texas Instruments

- 6.2.8 Stanley Electric Co. Ltd

- 6.2.9 OsRam Licht AG

- 6.2.10 ZKW Group

- 6.2.11 General Electric Company

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Automotive Adaptive Lighting System Industry Segmentation

The Automotive Adaptive Lighting System Market is segmented by Vehicle Type, Application Type, Component Type, Sales Channel, and Geography. By Vehicle Type, the market is segmented into Mid-Segment Passenger Cars, Sports Cars, and Premium Vehicles.

By Application Type, the market is segmented into Front, Rear. By Component type, the market is segmented into Controller, Sensors/ Camera, Lamp Assembly, and Others, and by Sales Channel Type, the market is segmented into OEM and Aftermarket. By Geography, the market is segmented into North America, Europe, Asia-Pacific, and the Rest of the World. For each segment, market sizing and forecast have been done on the basis of value (USD billion).

| By Vehicle Type | Mid-Segment Passenger Cars | ||

| Sports Cars | |||

| Premium Vehicles | |||

| By Type | Front | ||

| Rear | |||

| By Component Type | Controller | ||

| Sensors/ Camera | |||

| Lamp Assembly | |||

| Others | |||

| By Sales Channel Type | OEM | ||

| Aftermarket | |||

| By Geography | North America | United States | |

| Canada | |||

| Rest of North America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Rest of Europe | |||

| Asia-Pacific | India | ||

| China | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Rest of the World | South America | ||

| Middle-East and Africa | |||

Need A Different Region or Segment?

Customize Now

Automotive Adaptive Lighting System Market Research FAQs

What is the current Automotive Adaptive Lighting System Market size?

The Automotive Adaptive Lighting System Market is projected to register a CAGR of greater than 6% during the forecast period (2025-2030)

Who are the key players in Automotive Adaptive Lighting System Market?

Osram Licht AG, Valeo, Stanley Electric Co. Ltd., HELLA KGaAHueck& Co. and Koninklijke Philips N.V. are the major companies operating in the Automotive Adaptive Lighting System Market.

Which is the fastest growing region in Automotive Adaptive Lighting System Market?

North America is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Automotive Adaptive Lighting System Market?

In 2025, the Europe accounts for the largest market share in Automotive Adaptive Lighting System Market.

What years does this Automotive Adaptive Lighting System Market cover?

The report covers the Automotive Adaptive Lighting System Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Automotive Adaptive Lighting System Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Automotive Adaptive Lighting System Market Research

Mordor Intelligence provides a comprehensive analysis of the automotive adaptive lighting system market. With decades of expertise in the automotive lighting industry, we offer extensive coverage of the evolving landscape of automotive intelligent lighting system technologies. This includes a detailed examination of automotive LED lighting developments and emerging automotive laser lighting innovations. The report offers an in-depth analysis of automotive lighting control module implementations and advancements in the automotive headlight system. It is available as a report PDF for easy download.

Stakeholders in the automotive lighting electronics sector will benefit from our detailed examination of automotive smart lighting market trends and automotive LED lighting industry dynamics. The analysis covers crucial developments in automotive adaptive front lighting system technologies and explores the expanding automotive LED lighting market size. Our research provides actionable insights into automotive smart lighting innovations and automotive lighting advancements. This enables industry participants to make informed decisions and optimize their market positioning and strategic planning initiatives.