| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 5.34 Billion |

| Market Size (2030) | USD 6.52 Billion |

| CAGR (2025 - 2030) | 4.09 % |

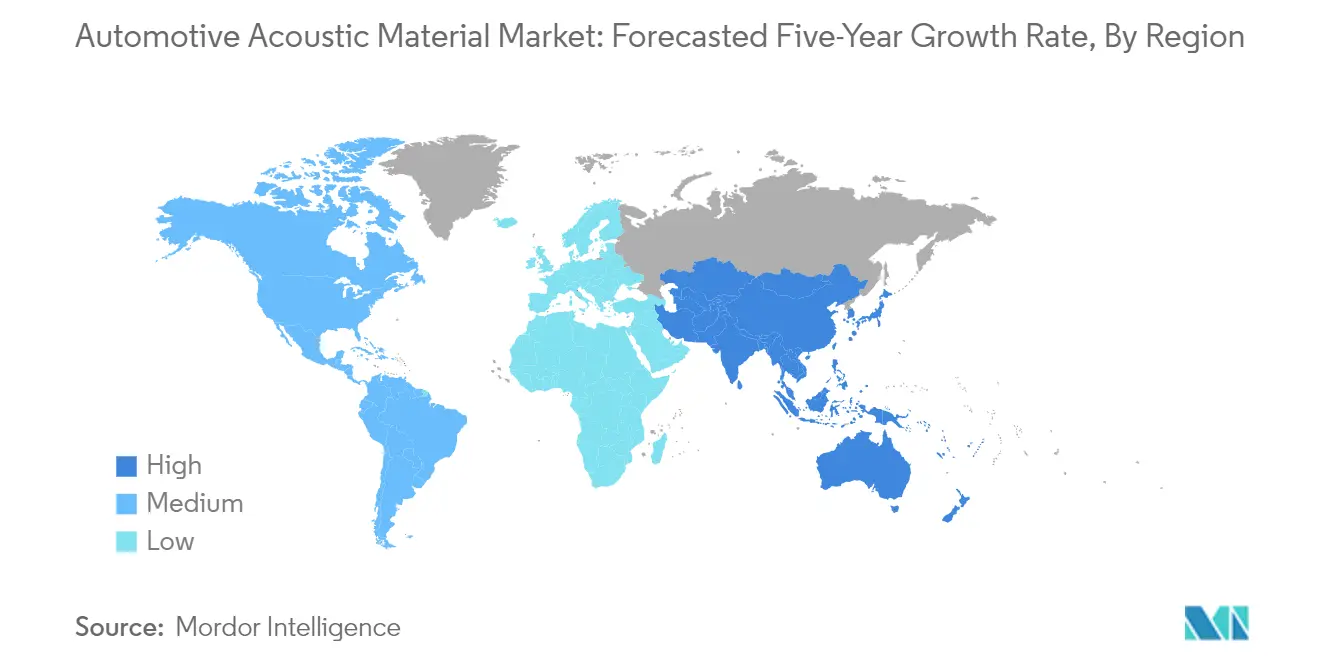

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

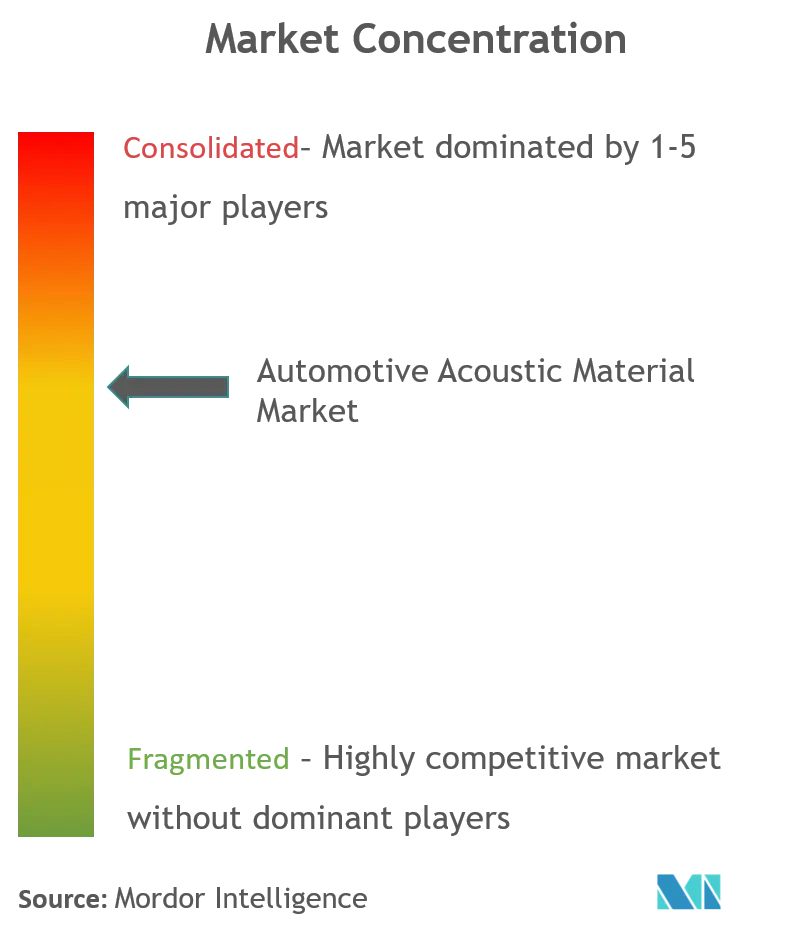

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Automotive Acoustic Material Market Analysis

The Automotive Acoustic Material Market size is estimated at USD 5.34 billion in 2025, and is expected to reach USD 6.52 billion by 2030, at a CAGR of 4.09% during the forecast period (2025-2030).

The automotive acoustic materials market is experiencing significant transformation driven by evolving vehicle interior design trends and changing consumer preferences. Vehicle interiors are undergoing substantial modifications as customization and autonomous driving capabilities become increasingly prevalent, with the traditional driver role gradually transitioning into that of a passenger. This shift has led automotive manufacturers to prioritize acoustic comfort as a crucial quality factor, with industry players actively developing innovative interior designs that incorporate advanced acoustic solutions. The integration of these materials has become particularly critical in premium and luxury vehicles, where cabin comfort and noise reduction are paramount considerations.

The electric vehicle revolution has fundamentally altered the acoustic requirements in modern vehicles, creating new opportunities and challenges for material manufacturers. Unlike traditional combustion engines, electric vehicles generate different types of noise patterns, particularly from rolling and wind sources, which require specialized automotive acoustic insulation solutions. Manufacturers are responding with innovative materials, as exemplified by Nissan's introduction of acoustic meta-material technology in 2023, which provides the same degree of sound isolation while weighing only one-fourth of traditional rubber boards. This technological advancement represents a significant breakthrough in addressing the specific acoustic needs of electric vehicles while supporting their weight reduction requirements.

The industry is witnessing substantial investments in research and development, particularly in lightweight and sustainable acoustic solutions. Major industry players are expanding their production capabilities and developing new technologies to meet evolving market demands. For instance, Covestro, along with its partners, recently developed a premium concept with material solutions, including a sound-absorbing automotive acoustic foam based on the Baynat® polyurethane system. These developments are complemented by strategic facility expansions, such as 3M Thailand's enhancement of its production facility at Latkrabang Industrial Estate, aimed at establishing a regional hub for Thinsulate sound-absorbing material production serving the automotive industry in the Asia-Pacific region.

The market is experiencing a shift towards more sophisticated acoustic solutions, particularly in the luxury and premium vehicle segments. Automotive manufacturers are increasingly incorporating advanced automotive sound insulation materials in various applications, from engine covers and dash insulators to door trims and bonnet liners. This trend is driven by the growing consumer demand for enhanced cabin comfort and reduced noise, vibration, and harshness (NVH) levels. The integration of acoustic materials has evolved beyond basic noise reduction to become a key differentiator in vehicle comfort and quality perception, with manufacturers developing customized solutions for different vehicle segments and applications.

Automotive Acoustic Material Market Trends

Increasing Electric Vehicle Sales

The rapid growth in electric vehicle adoption globally has emerged as a major driver for automotive acoustic materials, as EVs require specialized automotive sound dampening materials solutions. Electric powertrains consist of fewer moving parts but generate different types of noise and vibrations compared to conventional vehicles, creating unique acoustic challenges that need to be addressed. The absence of engine noise in EVs makes other sounds more noticeable, such as road noise, wind noise, and electrical system sounds, driving the demand for advanced acoustic materials that can effectively manage these noise sources while maintaining the vehicle's lightweight characteristics.

The automotive industry's shift toward electrification has prompted OEMs to invest heavily in R&D for innovative acoustic material products specifically designed for electric vehicles. For instance, Nissan introduced groundbreaking noise-reducing technology known as acoustic meta-material, which combines a lattice structure and plastic film to control air vibrations. This material is particularly effective at limiting the transmission of wide frequency band noise (500-1200 hertz) while being one-fourth the weight of traditional rubber board insulation materials. Similarly, companies like Autoneum have launched new fibrous materials for automotive carpet systems, inner dashes, and floor insulators that can function as both automotive sound deadening materials and absorbers depending on their stiffness.

Understand The Key Trends Shaping This Market

Download PDF

Growing Demand for Premium and Luxury Vehicles

The increasing consumer preference for premium and luxury vehicles has significantly boosted the demand for high-performance acoustic materials in the automotive sector. Luxury vehicle manufacturers are placing greater emphasis on interior comfort and noise reduction, making advanced acoustic solutions a crucial component of their vehicle design. This trend is evidenced by recent developments such as the next-generation Rolls-Royce Ghost, which incorporates more than 220 pounds of sound-absorbing materials in various areas including the roof, doors, trunk, and floor to enhance the ownership experience and interior comfort.

The automotive industry's focus on premium vehicle acoustics has led to continuous innovations in material technology and applications. Manufacturers are developing new acoustic solutions that not only provide superior noise reduction but also contribute to the overall luxury experience. For example, companies like FoamPartner have partnered with innovative concept car developers like Rinspeed to create advanced acoustic materials that combine premium aesthetics with exceptional sound-dampening properties. Additionally, Covestro has developed premium concept solutions including sound-absorbing acoustic foam based on the Baynat® polyurethane system, demonstrating the industry's commitment to meeting the sophisticated acoustic requirements of luxury vehicles.

Technological Advancements and R&D Investments

The automotive acoustic materials market is experiencing substantial growth driven by increased investments in research and development, leading to breakthrough innovations in material science and application technologies. Manufacturers are focusing on developing lightweight, high-performance materials that can effectively address the complex acoustic challenges in modern vehicles. This commitment to innovation is exemplified by recent developments such as Autoneum's Flexi-Loft technology, which utilizes a unique blend of recycled cotton and functional fibers to reduce product weight while maintaining superior acoustic properties and adaptability to complex shapes.

The industry's emphasis on sustainable and efficient acoustic solutions has led to the development of new material technologies that combine multiple functionalities. Companies are investing in creating materials that not only provide superior sound absorption but also contribute to vehicle weight reduction and improved fuel efficiency. For instance, major automotive suppliers are developing acoustical materials based on renewable resources as viable alternatives to traditional materials like mineral wool and fiberglass. These innovations are supported by significant investments in research facilities, as demonstrated by Daimler's new R&D Tech Center in China, which includes dedicated noise, vibration, and harshness (NVH) testing facilities to advance acoustic material development.

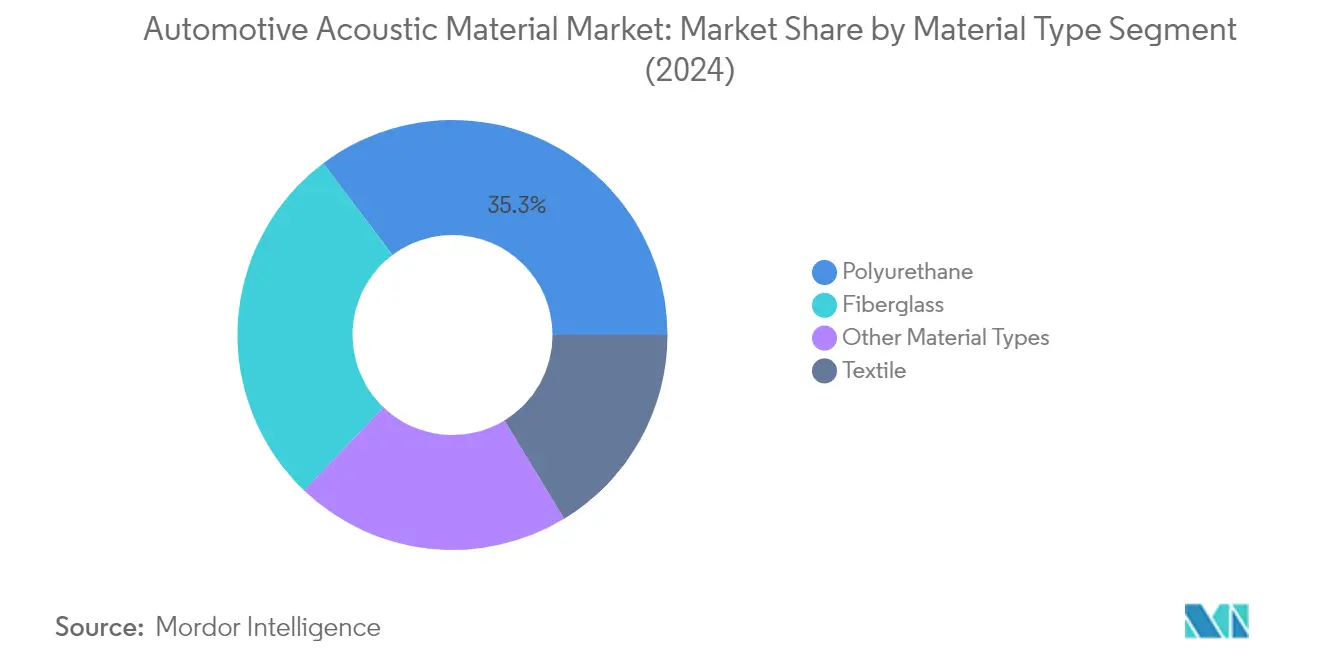

Segment Analysis: By Material Type

Polyurethane Segment in Automotive Acoustic Material Market

The polyurethane segment maintains its dominant position in the automotive acoustic material market, commanding approximately 35% market share in 2024. This significant market presence is attributed to polyurethane's superior soundproofing capabilities and its extensive application in both conventional and electric vehicles. Engine soundproofing remains a predominant application for combustion vehicles, while electric vehicles utilize this material for reducing rolling and wind noises in the passenger compartment. The material's nonwoven structure and its compatibility with other materials like woven structure and polypropylene foam make it ideal for various applications including seating areas, headliners, side panels, carpets, trunks, and bonnet liners for interior noise control. Companies are increasingly developing high-quality, low-emission, and low-odor applications based on polyurethane ester and polyurethane ether foams to meet evolving industry demands. These advancements in automotive sound dampening material are crucial for enhancing vehicle acoustics.

Polyurethane Segment Growth in Automotive Acoustic Material Market

The polyurethane segment is projected to experience robust growth at approximately 4% during the forecast period 2024-2029. This growth trajectory is driven by increasing demand for premium acoustic solutions in vehicles, particularly in the expanding electric vehicle segment. The material's versatility in addressing both traditional and emerging acoustic challenges positions it favorably for sustained growth. Manufacturers are focusing on developing innovative polyurethane-based solutions that offer enhanced sound absorption while maintaining lightweight properties, crucial for improving overall vehicle efficiency. The segment's growth is further supported by ongoing technological advancements in polyurethane formulations that provide superior noise reduction capabilities while meeting stringent automotive industry standards for sustainability and performance. The integration of automotive sound deadening material is pivotal in achieving these advancements.

Remaining Segments in Material Type

The fiberglass and textile segments play crucial complementary roles in the automotive acoustic materials market. Fiberglass materials are particularly valued for their durability and excellent thermal insulation properties alongside acoustic benefits, making them ideal for high-temperature applications in vehicles. The textile segment offers unique advantages in terms of lightweight solutions and flexibility in design, particularly beneficial for electric vehicle applications. Both materials contribute to the overall acoustic performance of vehicles through different mechanisms—fiberglass through its dense structure providing automotive sound barrier, and textiles through their sound absorption capabilities. These segments continue to evolve with new technological developments focusing on improving their acoustic properties while maintaining cost-effectiveness and meeting environmental standards.

Segment Analysis: By Vehicle Type

Passenger Car Segment in Automotive Acoustic Material Market

The passenger car segment dominates the automotive acoustic material market, commanding approximately 78% of the total market share in 2024. This significant market position is driven by increasing consumer demand for quieter and more comfortable vehicle interiors, particularly in premium and luxury vehicles. The segment's growth is further bolstered by stringent noise regulation standards in major automotive markets and the rising adoption of electric vehicles, which require specialized acoustic solutions to address unique noise challenges. Major automakers are investing heavily in acoustic material technologies for their passenger vehicle lines, with a particular focus on developing lightweight solutions that don't compromise on noise reduction capabilities. The integration of advanced automotive sound insulation materials in modern passenger cars has become a key differentiator in the competitive automotive market, especially as consumers increasingly prioritize cabin comfort and noise reduction features.

Commercial Vehicle Segment in Automotive Acoustic Material Market

The commercial vehicle segment plays a crucial role in the automotive acoustic material market, with manufacturers focusing on creating comfortable and noise-optimized driver cabins to enhance operator productivity and safety. This segment has seen significant technological advancements in acoustic solutions, particularly for long-haul trucks and buses where driver comfort is paramount for extended periods of operation. Commercial vehicle manufacturers are increasingly incorporating specialized acoustic materials that offer both sound absorption and thermal shielding properties, addressing the unique challenges posed by larger engines and extended operating hours. The focus on reducing driver fatigue through better noise management has led to innovations in acoustic material applications for commercial vehicles, particularly in areas like engine compartments and cabin insulation. The use of automotive acoustic foam in these applications is becoming increasingly prevalent.

Segment Analysis: By Application Type

Door Trim Segment in Automotive Acoustic Material Market

Door trim represents the largest application segment in the automotive acoustic material market, holding approximately 32% market share in 2024. The segment's dominance is driven by increasing consumer demand for enhanced interior comfort and noise reduction in vehicles. Modern vehicle door upholstery has evolved from being a luxury feature to becoming a standard offering in mid-segment vehicles, with manufacturers incorporating advanced acoustic materials to improve the overall driving experience. The use of materials like ABS, polypropylene, and SMA plastics in door trims has revolutionized automotive interior design while effectively reducing noise, vibration, and harshness levels. The growing trend of electric vehicles has further amplified the importance of door trim acoustic materials, as these vehicles require superior noise insulation due to the absence of engine noise masking other sounds. The application of automotive sound deadening material in door trims is essential for achieving these acoustic enhancements.

Bonnet Liner Segment in Automotive Acoustic Material Market

The bonnet liner segment is emerging as the fastest-growing application segment in the automotive acoustic material market, projected to grow at approximately 4% from 2024 to 2029. This growth is primarily attributed to the increasing focus on engine noise reduction and thermal management requirements in modern vehicles. Sound absorbers for engine covers are gaining prominence as they serve the dual purpose of dampening engine noise while functioning as heat insulators. The segment's growth is further fueled by the automotive industry's shift toward composite materials for under-the-hood applications, offering improved sound barrier properties and lighter weight alternatives compared to traditional materials. The rising adoption of electric vehicles has also created new opportunities for bonnet liner applications, as these vehicles require specialized acoustic solutions to address unique noise patterns and thermal management challenges. The use of automotive acoustic foam in bonnet liners is becoming increasingly significant.

Remaining Segments in Automotive Acoustic Material Market by Application Type

Other application types in the automotive acoustic material market encompass various components such as headliners, floor insulation, trunk liners, and engine compartment insulators. These applications play a crucial role in creating a comprehensive acoustic solution for vehicles, contributing to overall noise reduction and passenger comfort. The diversity of these applications reflects the complex nature of automotive acoustic management, requiring different material properties and installation techniques depending on the specific area of application. Manufacturers are continuously innovating in these segments, developing specialized solutions that address specific noise, vibration, and harshness challenges while meeting stringent automotive industry standards for weight reduction and sustainability.

Automotive Acoustic Material Market Geography Segment Analysis

Automotive Acoustic Material Market in North America

The North American automotive acoustic material market demonstrates a strong presence across the United States, Canada, and other territories. The region's market is characterized by increasing demand for luxury vehicles and growing electric vehicle adoption, which require sophisticated acoustic solutions. Manufacturers in this region are focusing on developing innovative lightweight materials that can provide superior noise reduction while contributing to overall vehicle efficiency. The presence of major automotive manufacturers and stringent noise regulation standards continues to drive market growth across the region.

Automotive Acoustic Material Market in the United States

The United States leads the North American market with approximately 64% market share in 2024. The country's market is driven by strong domestic automotive production and increasing consumer preference for quieter vehicle cabins. Major global players are actively investing in the region to expand their market presence and stay ahead of competitors. The country's push towards electric vehicles has created new opportunities for automotive acoustic insulation manufacturers, as EVs require specialized solutions for road noise and vibration control. The presence of stringent safety and comfort regulations also continues to drive innovation in the automotive acoustic materials market.

Automotive Acoustic Material Market in Canada

Canada represents the fastest-growing market in North America with an expected growth rate of approximately 3% during 2024-2029. The country's automotive sector contributes significantly to its GDP, making it a key market for automotive acoustic material market manufacturers. Canada's position as a major commercial vehicle producer has created sustained demand for acoustic materials. The government's ambitious targets for electric vehicle adoption have spurred investments in acoustic solutions specifically designed for electric powertrains. The country's close integration with the U.S. automotive industry through trade agreements has also facilitated market growth.

Automotive Acoustic Material Market in Europe

The European automotive acoustic materials market maintains a strong position globally, supported by the presence of major automotive manufacturers across Germany, the United Kingdom, and France. The region's stringent noise emission regulations and high consumer expectations for vehicle comfort have created a sophisticated market for acoustic materials. The increasing focus on electric vehicle production has led to new developments in acoustic solutions specifically designed for electric powertrains. The region's emphasis on sustainable manufacturing practices has also influenced innovation in eco-friendly acoustic materials.

Automotive Acoustic Material Market in Germany

Germany dominates the European market with approximately 23% market share in 2024. As Europe's largest automotive manufacturer, Germany's market is characterized by high-end vehicle production and stringent quality standards. The country's strong focus on research and development has led to continuous innovations in automotive sound insulation technology. The presence of major automotive manufacturers and their suppliers has created a robust ecosystem for acoustic material development and implementation. The transition towards electric mobility has further accelerated developments in specialized acoustic solutions.

Automotive Acoustic Material Market in the United Kingdom

The United Kingdom demonstrates strong growth potential with an expected growth rate of approximately 3% during 2024-2029. The country's market is driven by its significant role in luxury vehicle manufacturing and growing electric vehicle adoption. The UK's automotive industry's focus on premium vehicles has created sustained demand for high-quality acoustic materials. The government's push towards electric mobility has spurred investments in specialized acoustic solutions for electric vehicles. The presence of major research and development facilities continues to drive innovation in the automotive acoustic materials market.

Automotive Acoustic Material Market in Asia-Pacific

The Asia-Pacific region represents a dynamic market for the automotive acoustic materials market, encompassing major automotive manufacturing hubs across China, Japan, India, and South Korea. The region's rapid industrialization and increasing vehicle production have created substantial demand for acoustic materials. The growing middle class and increasing consumer preferences for comfortable vehicles have driven manufacturers to incorporate better acoustic solutions in their vehicles. The region's shift towards electric vehicles has also created new opportunities for acoustic material manufacturers.

Automotive Acoustic Material Market in China

China leads the Asia-Pacific market as the largest consumer of automotive acoustic materials. The country's massive automotive production capacity and growing domestic market have created sustained demand for acoustic materials. The government's push towards electric vehicles has spurred investments in specialized acoustic solutions. The presence of major domestic and international automotive manufacturers has created a competitive market for acoustic material suppliers. The country's focus on technological advancement continues to drive innovation in automotive acoustic materials.

Automotive Acoustic Material Market in India

India emerges as the fastest-growing market in the Asia-Pacific region. The country's rapidly expanding automotive sector and increasing consumer preferences for better-equipped vehicles have driven market growth. The government's push towards electric mobility has created new opportunities for automotive acoustic insulation manufacturers. The presence of major global and domestic automotive manufacturers has strengthened the market for acoustic materials. The country's focus on localizing automotive component production has encouraged investments in acoustic material manufacturing capabilities.

Automotive Acoustic Material Market in Rest of the World

The Rest of the World market, encompassing Brazil, the United Arab Emirates, and other countries, shows promising growth potential in the automotive acoustic materials market sector. Brazil leads this region as the largest market, benefiting from its significant automotive manufacturing base and growing domestic demand. The United Arab Emirates emerges as the fastest-growing market, driven by increasing luxury vehicle sales and growing automotive sector investments. The region's diverse automotive industry requirements and increasing focus on vehicle comfort have created varied opportunities for acoustic material manufacturers. The growing emphasis on electric vehicles across these markets has also spurred demand for specialized acoustic solutions.

Get Analysis on Important Geographic Markets

Download PDF

Automotive Acoustic Material Industry Overview

Top Companies in Automotive Acoustic Material Market

The automotive acoustic materials market is led by major chemical and materials companies, including Dow Chemicals, 3M Acoustics, BASF SE, Covestro, Henkel Adhesive Technologies, and LyondellBasell. These industry leaders focus on continuous product innovation through significant R&D investments to develop lighter, more effective acoustic solutions while maintaining high-performance standards. Companies are strengthening their operational capabilities through strategic manufacturing facility expansions, particularly in emerging markets across Asia-Pacific. Market leaders are also pursuing strategic partnerships and acquisitions to enhance their technological capabilities and regional presence, with a notable trend toward developing sustainable and recyclable acoustic materials. The emphasis on developing integrated solutions that combine sound absorption with thermal insulation properties demonstrates the industry's commitment to multi-functional materials that address multiple automotive challenges simultaneously.

Consolidated Market with Strong Regional Players

The automotive acoustic material market exhibits a relatively consolidated structure dominated by large multinational chemical conglomerates with diverse product portfolios. These major players leverage their extensive R&D capabilities, global manufacturing networks, and established relationships with automotive OEMs to maintain their market positions. Regional specialists, particularly in Asia-Pacific, are gaining prominence by offering cost-competitive solutions and maintaining strong local customer relationships, though their influence remains primarily limited to their respective geographical markets.

The market has witnessed significant merger and acquisition activity as companies seek to expand their technological capabilities and geographical reach. Major chemical companies are acquiring specialized acoustic material manufacturers to enhance their product offerings and gain access to proprietary technologies. This consolidation trend is particularly evident in mature markets like North America and Europe, where companies are focusing on vertical integration to strengthen their value chain positions and improve cost competitiveness.

Innovation and Sustainability Drive Future Success

For established players to maintain and expand their market share, developing innovative solutions that address emerging challenges in vehicle acoustics while meeting stringent environmental regulations has become crucial. Companies are investing in developing lightweight materials that contribute to overall vehicle weight reduction without compromising automotive acoustic insulation performance. The ability to offer integrated solutions that combine multiple functionalities, such as acoustic insulation with thermal management and structural support, will be a key differentiator for market success.

New entrants and challenger companies can gain ground by focusing on specific market niches or regional opportunities, particularly in emerging markets where local manufacturing presence and cost competitiveness are valued. The increasing focus on electric vehicles presents opportunities for specialized acoustic solutions, as these vehicles require different noise management approaches compared to traditional internal combustion engines. Success in this market will increasingly depend on the ability to develop sustainable solutions that meet both environmental regulations and customer demands for recyclable materials while maintaining competitive pricing and performance standards. The development of automotive sound insulation technologies is pivotal in addressing these evolving needs.

Automotive Acoustic Material Market Leaders

-

Dow Chemicals

-

3M Acoustics

-

BASF SE

-

Covestro

-

Henkel Adhesive Technologies

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Automotive Acoustic Material Market News

- In October 2021, Sumitomo Riko announced that as part of a joint research project with the National Institute of Advanced Industrial Science and Technology (AIST) in Japan, it had recovered a part of the proving ground for vehicle testing installed at the Tsukuba North Site of AIST and installed a new course with special road surfaces. Six types of special road surfaces were installed: road noise road, ride comfort road, Belgian-block road, undulating road, gravel and sand exposed road, and harshness road, to measure and evaluate the NVH of vehicles.

- In September 2021, BASF presented a new flame-retardant Ultramid grade (PA66) that expands the portfolio of color-stable, tailor-made engineering plastics for use in electric cars for the first time at Fakuma in Friedrichshafen, Germany, where engine and transmission mounts are presented, which lead to savings in production but also contribute to optimized acoustic experiences.

- In May 2020, Freudenberg Group acquired Low & Bonar PLC, London, United Kingdom. The company will be integrated with the Freudenberg Performance Materials Business Group.

Automotive Acoustic Material Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

- 4.1 Market Drivers

- 4.2 Market Restraints

-

4.3 Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION

-

5.1 Material

- 5.1.1 Polyurethane

- 5.1.2 Textile

- 5.1.3 Fiberglass

- 5.1.4 Other Materials

-

5.2 Vehicle Type

- 5.2.1 Passenger Cars

- 5.2.2 Commercial Vehicles

-

5.3 Application

- 5.3.1 Bonnet Liner

- 5.3.2 Door Trim

- 5.3.3 Other Applications

-

5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 India

- 5.4.3.2 China

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 Rest of the World

- 5.4.4.1 Brazil

- 5.4.4.2 United Arab Emirates

- 5.4.4.3 Other Countries

6. COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

-

6.2 Company Profiles

- 6.2.1 Dow Chemicals

- 6.2.2 3M Acoustics

- 6.2.3 BASF SE

- 6.2.4 Covestro

- 6.2.5 Henkel Adhesive Technologies

- 6.2.6 Lyondellbasell

- 6.2.7 Sumitomo Riko

- 6.2.8 Sika

- 6.2.9 Toray Industries

- 6.2.10 Huntsman

- 6.2.11 Freudenberg Group

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Automotive Acoustic Material Industry Segmentation

The automotive acoustic material market is segmented by material, vehicle type, application, and geography. By material, the market is segmented into polyurethane, textile, fiberglass, and other materials. By vehicle type, the market is segmented into passenger cars and commercial vehicles. By application, the market is segmented into bonnet liner, door trim, and other applications. By geography, the market is segmented into North America, Europe, Asia-Pacific, and Rest of the World.

| Material | Polyurethane | ||

| Textile | |||

| Fiberglass | |||

| Other Materials | |||

| Vehicle Type | Passenger Cars | ||

| Commercial Vehicles | |||

| Application | Bonnet Liner | ||

| Door Trim | |||

| Other Applications | |||

| Geography | North America | United States | |

| Canada | |||

| Rest of North America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Rest of Europe | |||

| Asia-Pacific | India | ||

| China | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Rest of the World | Brazil | ||

| United Arab Emirates | |||

| Other Countries | |||

Need A Different Region or Segment?

Customize Now

Automotive Acoustic Material Market Research FAQs

How big is the Automotive Acoustic Material Market?

The Automotive Acoustic Material Market size is expected to reach USD 5.34 billion in 2025 and grow at a CAGR of 4.09% to reach USD 6.52 billion by 2030.

What is the current Automotive Acoustic Material Market size?

In 2025, the Automotive Acoustic Material Market size is expected to reach USD 5.34 billion.

Who are the key players in Automotive Acoustic Material Market?

Dow Chemicals, 3M Acoustics, BASF SE, Covestro and Henkel Adhesive Technologies are the major companies operating in the Automotive Acoustic Material Market.

Which is the fastest growing region in Automotive Acoustic Material Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Automotive Acoustic Material Market?

In 2025, the Asia Pacific accounts for the largest market share in Automotive Acoustic Material Market.

What years does this Automotive Acoustic Material Market cover, and what was the market size in 2024?

In 2024, the Automotive Acoustic Material Market size was estimated at USD 5.12 billion. The report covers the Automotive Acoustic Material Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Automotive Acoustic Material Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Automotive Acoustic Material Market Research

Mordor Intelligence provides a comprehensive analysis of the automotive acoustic material market. We leverage our extensive experience in industrial research and consulting. Our latest report examines the full range of automotive acoustic insulation and automotive sound barrier technologies. This includes a detailed analysis of automotive acoustic foam applications and emerging trends in automotive sound insulation solutions. The research covers various automotive sound dampening material technologies and automotive sound deadening material innovations that are reshaping the industry landscape.

Stakeholders gain valuable insights through our detailed examination of vehicle sound proofing material developments and automotive noise dampening technologies. These insights are available in an easy-to-download report PDF format. The analysis provides strategic information about automotive acoustic materials market dynamics, including demand patterns, technological advancements, and regional growth opportunities. Our research methodology ensures comprehensive coverage of material types, applications, and emerging technologies. This enables businesses to make informed decisions based on reliable market intelligence and industry expertise.