Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

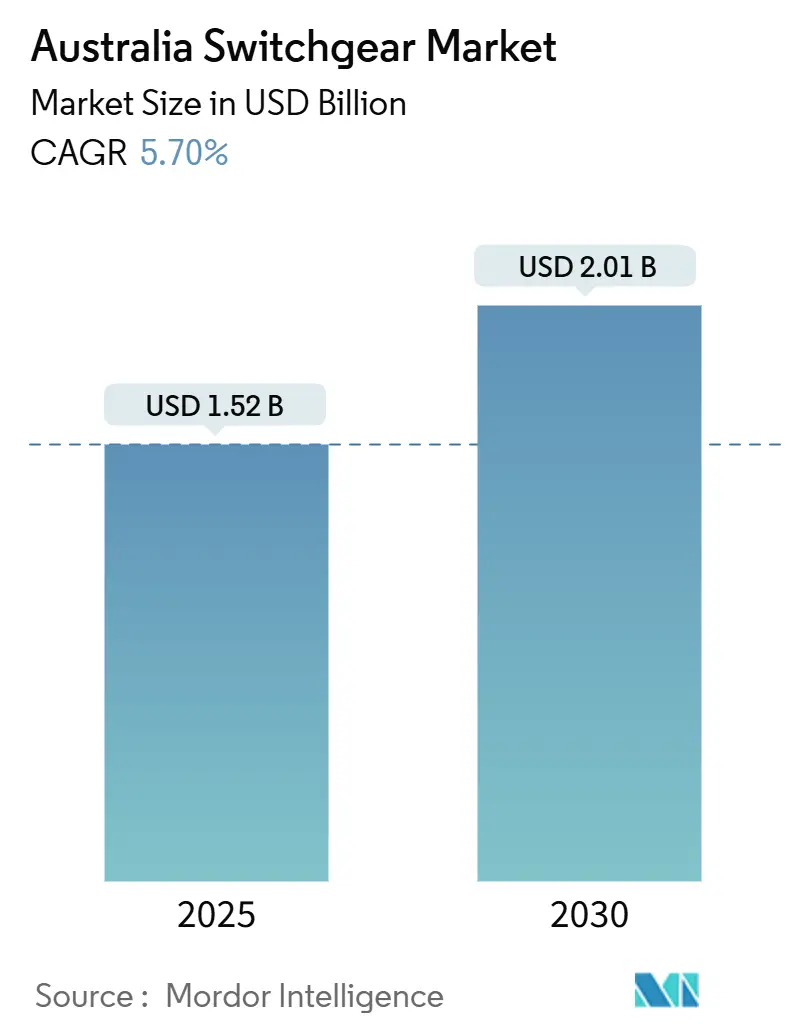

| Market Size (2025) | USD 1.52 Billion |

| Market Size (2030) | USD 2.01 Billion |

| Growth Rate (2025 - 2030) | 5.70% CAGR |

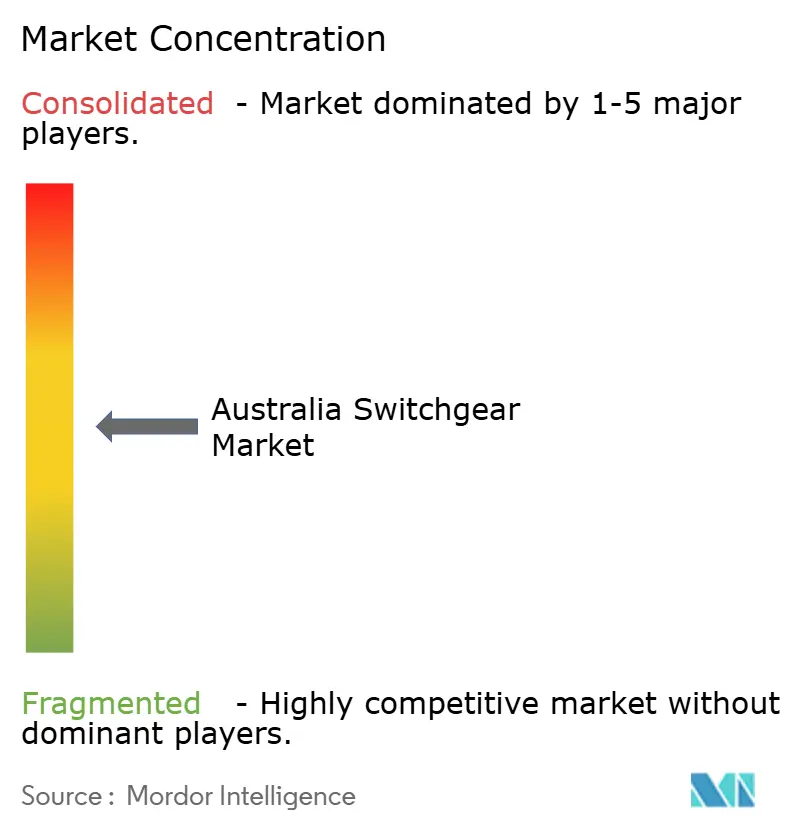

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Australia Switchgear Market Analysis by Mordor Intelligence

The Australia switchgear market size stood at USD 1.52 billion in 2025 and is forecast to expand at a 5.7% CAGR, hitting USD 2.01 billion by 2030. Rising renewable connections, urgent upgrades to forty-year-old networks, and substantial public funding under the Rewiring the Nation and the Future Made in Australia packages are the primary accelerants. Utilities are specifying digital, condition-monitored equipment to contain outage costs, while industrial buyers in mining and manufacturing favor ruggedized models that support on-site renewables and battery systems. Gas-insulated and SF6-free technologies are gaining share where land prices exceed USD 100,000 per hectare or where emissions rules impose penalties of USD 75 per tonne CO2-equivalent. Local assembly and inventory buffers have become crucial differentiators as global lead times for high-voltage gear have stretched to 24-36 months.

Key Report Takeaways

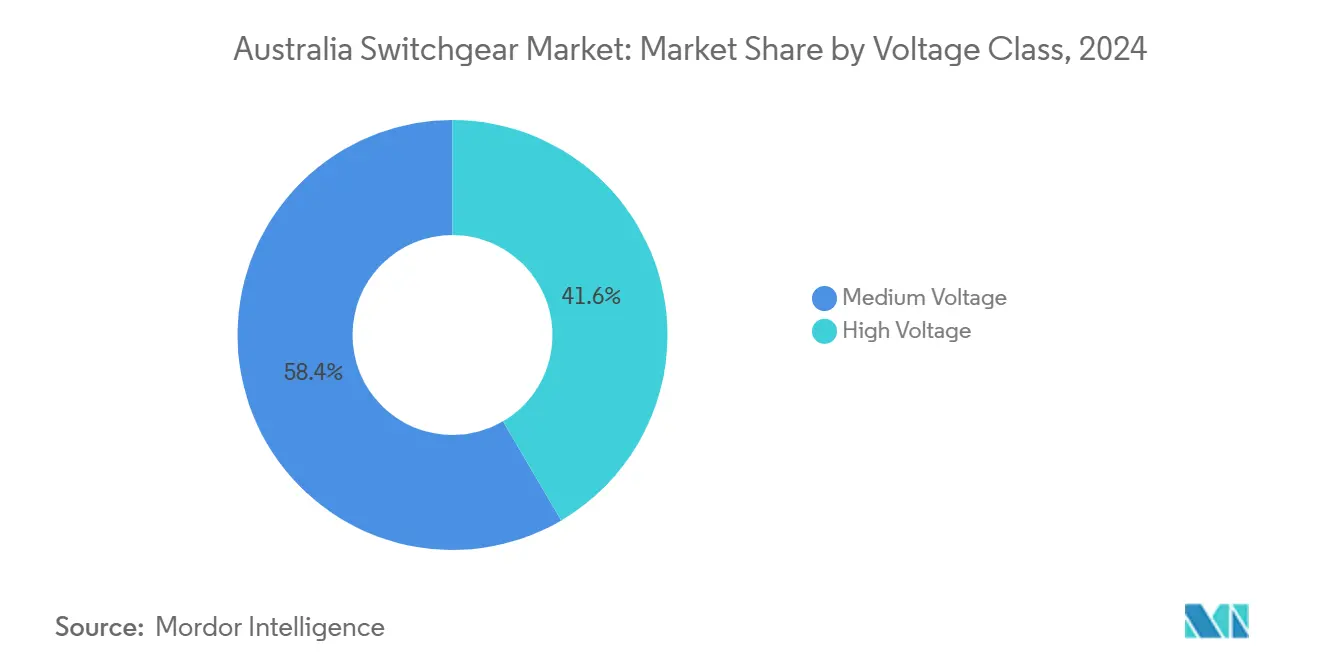

- By voltage class, medium voltage captured 58.43% of the Australia switchgear market share in 2024; high voltage is advancing at a 6.77% CAGR through 2030.

- By insulation type, air-insulated products held 64.68% of the Australia switchgear market size in 2024, while gas-insulated alternatives are expanding at a 7.42% CAGR to 2030.

- By installation, indoor systems accounted for 61.54% of the Australia switchgear market size in 2024; outdoor units post the quickest pace at a 6.98% CAGR.

- By end user, utilities represented 46.88% of revenue in 2024 and are growing at a 6.54% CAGR through 2030.

- By application, transmission and distribution retained a 37.89% share in 2024, whereas renewable integration is projected to rise at an 8.01% CAGR between 2025 and 2030.

Australia Switchgear Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in renewable energy integration | +2.1% | National, concentrated in NSW, QLD, SA renewable energy zones | Medium term (2-4 years) |

| Ongoing upgrades to aging T & D infrastructure | +1.8% | National, priority in metropolitan networks and regional transmission corridors | Long term (≥ 4 years) |

| Growing investments in mining and resources sector | +1.2% | WA Pilbara, QLD Bowen Basin, SA Olympic Dam region | Medium term (2-4 years) |

| Rapid electrification of remote microgrids | +0.9% | NT remote communities, WA mining sites, regional Indigenous communities | Short term (≤ 2 years) |

| Government push for domestic manufacturing | +0.7% | National, hubs in VIC, NSW, SA | Long term (≥ 4 years) |

| Adoption of digital switchgear with condition monitoring | +0.6% | National, led by major utilities and industrial facilities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Renewable Energy Integration

Australia is targeting 82% renewable electricity by 2030, and the associated shift from one-way to bidirectional power flows demands switchgear with faster fault-clearing and inverter-friendly protection schemes. [1]Australian Energy Market Operator, “2024 Integrated System Plan,” aemo.com.au Projects such as HumeLink and Marinus Link require 500 kV and HVDC equipment that tolerates higher fault currents and integrates synchronous condensers for stability. [2]Transgrid, “HumeLink Project,” transgrid.com.auThe 2024 Integrated System Plan identifies 10,000 km of new lines, many of which are routed through land-scarce renewable energy zones, where utilities tend to favor compact gas-insulated solutions. Each GIS yard avoids roughly 23,500 tCO2-e of lifetime SF6 emissions compared with legacy units. Higher capital outlays are balanced by land savings and lower leak-monitoring costs.

Ongoing Upgrades to Aging T & D Infrastructure

Average substation equipment in metropolitan networks exceeds 40 years, prompting state utilities to schedule systematic replacements through 2030. Transgrid, Powerlink, and ElectraNet together plan over USD 8 billion in capital work, with switchgear representing roughly one-quarter of the spend. Victoria’s bushfire-driven rollout of Rapid Earth Fault Current Limiters across 22 zone substations necessitates auxiliary switchgear rated for instant neutral switching. The Australian Energy Regulator rewards condition-based maintenance, so digital units that forecast insulation wear can defer replacements by up to five years. Lifecycle analytics are, therefore, transitioning from an optional to a standard specification.

Growing Investments in Mining and Resources Sector

Mining enterprises have announced USD 15 billion in electrification projects to reduce diesel consumption and meet their Scope 1 targets. Fortescue’s USD 6.2 billion program involves high-voltage switchgear that integrates wind, solar, and 400 MWh of battery capacity at iron ore sites. BHP’s Nickel West spent USD 300 million on adding 181 MW of renewables, which required explosion-proof, arc-resistant gear for underground haulage tunnels. Modular panels that ship on skids reduce mine commissioning time by 40% and support rapid redeployment as the pit progresses. Suppliers able to guarantee seismic resilience and operate within the temperature range of −10 °C to +55 °C win most Pilbara bids.

Rapid Electrification of Remote Microgrids

Federal grants worth USD 175.4 million back microgrids for off-grid towns and Indigenous communities. The 100 kW solar + 136 kWh battery project at Marlinja demonstrates that islanded systems require switchgear that combines recloser and sectionalizer functions to maintain stability during cloud events. Harsh-environment designs with IP66 enclosures and corrosion-resistant aluminum frames are mandatory in tropical and desert climates. Because local technicians are scarce, units are equipped with cellular SCADA and require maintenance only every five years, a feature highlighted in the Powering the Regions Fund guidelines.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent environmental and safety regulations | -1.1% | National, with state-specific implementation | Long term (≥ 4 years) |

| Supply chain disruptions and raw-material inflation | -0.8% | National, affecting all segments | Short term (≤ 2 years) |

| Delays in grid interconnect approvals on Indigenous lands | -0.4% | NT, WA, QLD regions with significant Indigenous holdings | Medium term (2-4 years) |

| Skill shortages in high-voltage technicians | -0.3% | National, acute in regional project locations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Environmental and Safety Regulations

SF6 restrictions tighten annually, and major networks must phase out the gas by 2030, adding certification and disposal costs to legacy fleets. Facilities emitting over 100,000 tCO2-e now face a 4.9% yearly reduction mandate, making emissions-free switchgear the lower-risk choice for long-lived assets. Utilities piloting SF6-free kits report a 10-15% higher upfront cost, but the payback arrives within seven years once leak monitoring, carbon penalties, and reclamation charges are factored in. The framework has accelerated product testing yet slowed approvals, extending procurement by three months in some states.

Supply Chain Disruptions and Raw-Material Inflation

Copper and steel prices increased by 35% and 28%, respectively, between 2023 and 2025, resulting in a 15-20% rise in finished switchgear prices. Lead times for 245 kV breakers lengthened to 24-36 months during 2024, compelling utilities to pre-order and store spares. The Future Made in Australia plan allocates USD 1.7 billion for local fabrication; however, new plants are not expected to contribute meaningfully until 2027. [3]Department of Industry, Science and Resources, “Future Made in Australia,” industry.gov.auDomestic firms like Legrand have offset part shortages through multi-port inventories; however, rising freight prices still squeeze their margins.

Segment Analysis

By Voltage Class: High-Voltage Growth Accelerates Infrastructure Modernization

Medium-voltage gear held 58.43% of the Australia switchgear market share in 2024, anchored by distribution upgrades across urban centers. The high-voltage category is expected to deliver a 6.77% CAGR as large-scale transmission schemes, such as HumeLink and Marinus Link, proceed. This shift lifts the Australia switchgear market size allocated to 245-kV and above ratings faster than at any time since 2010. Gas-insulated platforms dominate these tenders because each compact bay saves up to 60% of land compared to air-insulated yards, a decisive factor when land costs exceed USD 100,000 per hectare.

Historically, high-voltage demand grew 4.2% from 2019-2024, but renewable mandates and interstate connectors lifted the pace to 6.77%. State regulators now permit accelerated depreciation for assets that integrate inverter-based resources, shortening project payback. Medium-voltage products remain critical for downstream feeders, with Victorian Rapid Earth Fault Current Limiter sites driving orders for multi-feeder panels. Digital monitoring adds roughly 4% to the purchase cost yet cuts unplanned outages by up to 30%, a saving that utilities quantify in their regulatory submissions.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Insulation Type: SF6-Free Technologies Gain Regulatory Momentum

Air-insulated designs accounted for 64.68% of 2024 revenue, primarily due to itslower initial prices and ease of servicing. However, the gas-insulated segment will expand at 7.42% CAGR through 2030 as urban substations face tight footprints. The Australia switchgear market size for SF6-free GIS is on track to triple by 2028 once mainstream utilities finalize type tests. Schneider Electric’s pure air replacement and Siemens’ fluoronitrile blends now match legacy performance while removing 23,500 tCO2-e per installation. Early adopters absorb a 10-15% premium, but carbon-price exposure and leak reporting justify the switch within seven years.

Hybrid switchgear, which combines air interrupters with gas-insulated bus sections, is an interim option for mining companies that require compact skids yet prefer field-serviceable breakers. Standards Australia finalized updated AS/NZS 62271 parts in 2024 to reflect vacuum-interrupting requirements, simplifying approvals for SF6-free lines. Utilities have begun issuing bulk tenders stipulating maximum GWP thresholds, an implicit constraint that accelerates the retirement of SF6.

By Installation: Outdoor Applications Drive Renewable Integration

Indoor panels retained 61.54% of 2024 spend as urban utilities favor climate-controlled switchrooms to prolong asset life. Still, outdoor cabinets will grow at a rate of 6.98% annually because large renewable parks and long-distance connectors often sit in remote zones where sheds are impractical. The Australia switchgear market size for outdoor systems aligns with solar farm rollouts that need 33 kV ring-main units resistant to 50 °C daytime heat and cyclonic winds.

Outdoor enclosures cut civil costs by up to 30% compared with masonry buildings. Mining customers choose containerized 11 kV boards that arrive pre-tested, shaving eight weeks off the schedule. Australian Standard dust ingress tests grade IP66 units, and both Fortescue and Rio Tinto stipulate this level for Pilbara deployments. Meanwhile, indoor switchgear remains the preferred choice for distribution substations in Melbourne and Sydney, where security and noise regulations apply.

By End User: Utilities Lead Modernization Investment

Utilities commanded 46.88% of revenue in 2024 and will expand at 6.54% CAGR as regulators approve record capex to support 82% renewables. Their bulk orders stabilize plant utilization for original-equipment manufacturers and anchor local assembly lines. Large transmission operators allocate roughly 25% of total rebuild budgets to switchgear, underscoring its central role.

Industrial users reward suppliers that package rugged mechanics with digital diagnostics. BHP’s Nickel West and OZ Minerals’ West Musgrave mine both embed thermal cameras in 11 kV cubicles to pre-empt cable joint failures. Commercial building retrofits adopt compact, withdrawable units compatible with electric-vehicle charging upgrades, whereas residential growth remains negligible because switchgear remains largely utility-owned behind the meter.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Application: Renewable Integration Emerges as Growth Leader

Transmission and distribution maintained the largest share at 37.89% in 2024, but renewable integration is expected to grow 8.01% annually through 2030, as every gigawatt of wind or solar energy requires advanced breaker and disconnector schemes. High-speed relays that ride through fault-induced voltage dips are mandatory under AEMO’s grid-forming inverter guidelines.

Mining electrification is the second-fastest niche, demanding modular 33 kV boards that tolerate vibration and dust. Transport projects, such as the Sydney Metro, employ 1,500 V DC traction switchgear, a specialist subsegment forecasted to rise with rail expansions. Utilities also retrofit substations to support fast chargers, each 350 kW unit needing new low-voltage switchgear with arc-flash mitigation.

Geography Analysis

New South Wales and Victoria together account for roughly 45% of the Australia switchgear market, driven by dense loads and large renewable energy zones such as Central-West Orana and Gippsland. HumeLink’s USD 4.3 billion outlay boosts demand for 500 kV equipment from 2025 onward, while VNI West adds HVDC converter station packages. Distribution operators in these states are rolling out fault-current limiters and replacing oil breakers with vacuum units, thereby lifting medium-voltage orders.

Queensland follows, underpinned by the Bowen Basin and Galilee Basin mines, transitioning from diesel to hybrid power. CopperString 2032 will connect North Queensland resources to the main grid, opening a fresh high-voltage opportunity set. Western Australia is the fastest-growing region because the Pilbara’s USD 6.2 billion renewable push forces a step-change in high-voltage installations, often sited hundreds of kilometers from service hubs.

South Australia already sourced 70% of its electricity from renewables in 2024, so stability rather than capacity drives switchgear specifications. Fast-acting STATCOM and battery plants, exemplified by Hornsdale, need breakers that operate within two cycles, a new benchmark other regions are now adopting. Tasmania’s Marinus Link introduces HVDC technologies to its grid, while the Northern Territory’s microgrid grants fund rugged IP66 rated equipment for Indigenous communities such as Marlinja.

Competitive Landscape

The Australia switchgear market is moderately concentrated. Schneider Electric and SA Power Networks commenced the nation’s largest SF6-free rollout in 2024, signaling a shift to fluoronitrile and vacuum interrupters. Siemens’ blue GIS installations demonstrated endurance during the 48 °C Port Augusta heatwave, easing adoption barriers.

Local players such as NOJA Power hold niches in reclosers and pole-top switchgear, exporting to 90 countries and supplying Ergon Energy’s feeder automation needs. NHP and Ampcontrol extend reach through service contracts, offsetting the scarcity of high-voltage technicians by offering turnkey lifecycle packages. Supply chain resilience is now a competitive advantage; manufacturers with domestic warehouses can deliver 33 kV panels in 12 weeks, compared to 40 weeks for fully imported sets. Government tender rules favor bids that exceed 50% local content, a policy that encourages firms to establish assembly lines in New South Wales and South Australia.

Australia Switchgear Industry Leaders

-

ABB Ltd.

-

Schneider Electric SE

-

Siemens AG

-

Eaton Corporation PLC

-

TAMCO Switchgear (Malaysia) Sdn Bhd

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- October 2024: Schneider Electric expanded SF6-free switchgear trials with SA Power Networks, aiming for full phase-out by 2030.

- September 2024: GE Vernova won a Powerlink Queensland order for dead-tank breakers on the USD 5 billion CopperString 2032 project.

- August 2024: Siemens deployed blue GIS in multiple substations, validating SF6-free performance in extreme heat.

- July 2024: NOJA Power increased Brisbane's recloser capacity to serve the rising demand for exports and domestic microgrids.

Australia Switchgear Market Report Scope

A switchgear, integral for power system protection, regulates, switches, and controls electrical circuits. Its components include circuit breakers, isolators, relays, switches, fuses, and control panels. Switchgear plays a crucial role in de-energizing equipment for testing, maintenance, and fault clearance.

The Australia Switchgear Market Report is Segmented by Voltage Class (High Voltage (≥72.5 kV), Medium Voltage (1 kV-72.5 kV)), Insulation Type (Air-Insulated Switchgear (AIS), Gas-Insulated Switchgear (GIS), Hybrid and Other Insulation Types), Installation (Indoor, and Outdoor), End User (Utilities, Residential, Commercial, and Industrial), and Application (Transmission and Distribution, Renewable Integration, Infrastructure and Transportation, Mining and Resources, and Other Applications). The Market Forecasts are Provided in Terms of Value (USD).

By Voltage Class

| High Voltage |

| Medium Voltage |

By Insulation Type

| Air-Insulated Switchgear (AIS) |

| Gas-Insulated Switchgear (GIS) |

| Hybrid |

| Other Insulation Types |

By Installation

| Indoor |

| Outdoor |

By End User

| Utilities |

| Residential |

| Commercial |

| Industrial |

By Application

| Transmission and Distribution |

| Renewable Integration |

| Infrastructure and Transportation |

| Mining and Resources |

| Other Applications |

| By Voltage Class | High Voltage |

| Medium Voltage | |

| By Insulation Type | Air-Insulated Switchgear (AIS) |

| Gas-Insulated Switchgear (GIS) | |

| Hybrid | |

| Other Insulation Types | |

| By Installation | Indoor |

| Outdoor | |

| By End User | Utilities |

| Residential | |

| Commercial | |

| Industrial | |

| By Application | Transmission and Distribution |

| Renewable Integration | |

| Infrastructure and Transportation | |

| Mining and Resources | |

| Other Applications |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the forecast value of the Australia switchgear market in 2030?

The market is projected to reach USD 2.01 billion by 2030.

Which voltage class is growing the fastest?

High-voltage switchgear is expanding at a 6.77% CAGR through 2030 as new transmission links proceed.

Why are gas-insulated units gaining popularity?

They save up to 60% land and avoid SF6 emissions, important where land costs and environmental rules are strict.

How large is the utility share of spending?

Utilities accounted for 46.88% of 2024 revenue and remain the biggest buyers.

What role do domestic manufacturers play?

Local firms supply niche products and assembly, helping mitigate import lead-time risks and meet local-content rules.

How do environmental regulations affect purchasing decisions?

Tightening SF6 limits and carbon costs make SF6-free or low-GWP designs more cost-effective over asset life.

Page last updated on: