| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 1.58 Billion |

| Market Size (2030) | USD 2.00 Billion |

| CAGR (2025 - 2030) | 4.83 % |

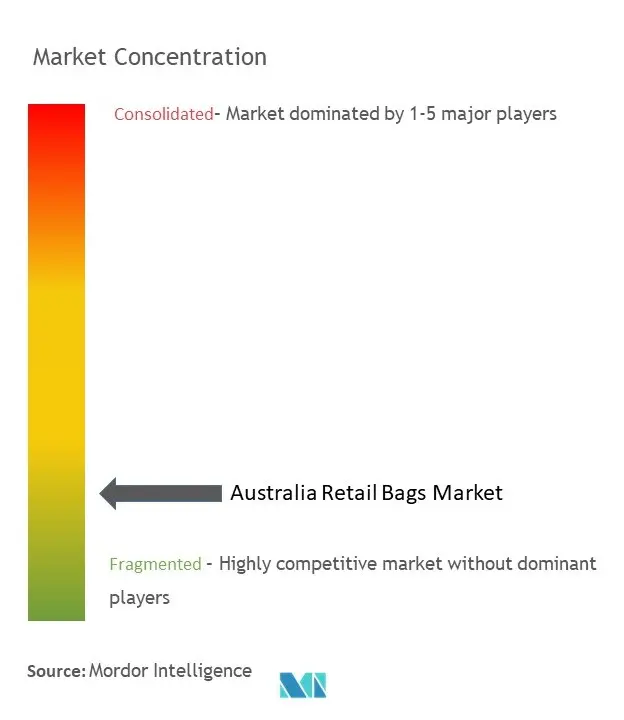

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Australia Retail Bags Market Analysis

The Australia Retail Bags Market size is worth USD 1.58 Billion in 2025, growing at an 4.83% CAGR and is forecast to hit USD 2.00 Billion by 2030.

The Australian retail sector has undergone significant transformation, driven by changing consumer preferences and evolving shopping behaviors. The retail landscape has witnessed substantial growth across various segments, with homeware and appliances leading at 21.3% of total retail expenditure, followed by department stores at 17.1%, and grocery and liquor at 15.6% in 2022. This diversification in retail spending has created unique demands for retail packaging solutions, particularly in the retail bags segment. The shift in consumer behavior has led retailers to adapt their packaging strategies, focusing on convenience, functionality, and brand representation across different retail categories.

The market is experiencing a profound shift towards sustainable and eco-friendly packaging solutions, reflecting growing environmental consciousness among Australian consumers and retailers. Major retail chains are actively transitioning away from traditional plastic shopping bags, with leading supermarkets like Woolworths and Coles Group dominating the online grocery retail space, holding approximately 45% and 29% market share respectively as of Q3 2023. This transition has sparked innovation in sustainable packaging materials, including recyclable paper, natural fabrics, and biodegradable alternatives, fundamentally reshaping the retail bags landscape.

The rapid expansion of e-commerce and omnichannel retail has revolutionized packaging requirements across the Australian retail sector. The foodservice industry has particularly demonstrated remarkable growth, with annual revenue from cafes, restaurants, and takeaway food services reaching AUD 58.15 billion in 2022. This growth has necessitated innovative packaging solutions that can accommodate both in-store and delivery requirements, leading to the development of more versatile and durable shopping bags options. The integration of online and offline retail channels has created new opportunities for packaging manufacturers to develop solutions that cater to multiple distribution channels.

Technological advancement and material innovation have become crucial differentiators in the retail bags market. Companies are investing in research and development to create advanced materials that combine sustainability with enhanced functionality. The annual revenue generated from clothing, footwear, and personal accessories reached AUD 34.73 billion in 2022, driving demand for sophisticated packaging solutions that align with brand values and consumer expectations. This has led to the emergence of new materials and designs that offer improved durability, aesthetics, and environmental performance, while meeting the specific requirements of different retail segments. The increasing use of reusable shopping bags is a testament to this trend, as consumers and retailers alike seek to reduce environmental impact.

Australia Retail Bags Market Trends

The Growing Demand for Unit-Sized Bags is Expected to Drive Growth

The expanding foodservice industry in Australia has created substantial demand for unit-sized retail bags, particularly driven by the proliferation of quick-service restaurants, cafes, and food delivery services. According to recent data, over 51.9 thousand cafés and restaurants were operational across Australia by the end of fiscal year 2022, with major chains like McDonald's expanding their presence to 1,039 stores nationwide as of January 2024. This extensive network of food establishments requires a consistent supply of appropriately sized shopping bags for takeaway and delivery orders, making unit-sized bags an essential component of their operations. The rising urban population and shifting consumer preferences toward dining out and takeaway options have further accelerated the demand for convenient, portion-appropriate packaging solutions.

The retail sector's evolution, particularly in response to changing consumer behaviors and sustainability requirements, has intensified the need for unit-sized shopping bags across various applications. Major retailers are increasingly adopting right-sized packaging solutions to minimize waste and improve efficiency in their operations. This trend is particularly evident in the grocery and food retail segments, where the retail turnover in New South Wales alone witnessed a significant increase from USD 9.201 billion in February 2022 to USD 9.8186 billion in February 2023, indicating robust growth in retail activities that require appropriate packaging solutions. The surge in online shopping and delivery services has further amplified the demand for unit-sized bags that can safely and efficiently transport individual items while maintaining product integrity throughout the delivery process.

Understand The Key Trends Shaping This Market

Download PDF

Legislative Changes Will Propel the Growth of Paper-Based Bags (State-Wise Ban on Plastic Bags <35 Microns)

The implementation of comprehensive plastic bag bans across Australian states and territories has created a significant shift toward paper shopping bags and natural fabric retail bags. Various state governments, including Western Australia (July 2022), New South Wales (June 2022), Victoria (November 2019), and Queensland (July 2018), have introduced bans on lightweight plastic shopping bags with a thickness of 35 microns or less, including degradable, biodegradable shopping bags, and compostable bags. This legislative framework has compelled retailers and consumers to transition to more sustainable alternatives, particularly paper shopping bags solutions. The Australian Packaging Covenant Organization (APCO) reports that paper and paperboard packaging already accounts for more than half of the overall packaging consumed in Australia, demonstrating the market's readiness to embrace paper-based alternatives.

The Australian government's 2025 national packaging targets have further strengthened the momentum toward paper-based retail bags. These ambitious targets mandate 100% reusable, recyclable, or compostable packaging, along with achieving 70% recycling or composting rates for plastic packaging and incorporating 50% average recycled content in packaging materials. Major retailers are actively aligning their operations with these legislative requirements, as exemplified by Woolworths' initiative to phase out 15-cent reusable plastic shopping bags from its stores and online orders in favor of more sustainable packaging options. This transition is particularly significant as it demonstrates the retail industry's commitment to environmental sustainability while creating substantial opportunities for paper-based bag manufacturers to fill the market gap created by plastic bag restrictions.

Segment Analysis: By Material

Paper and Natural Fabric Segment in Australia Retail Bags Market

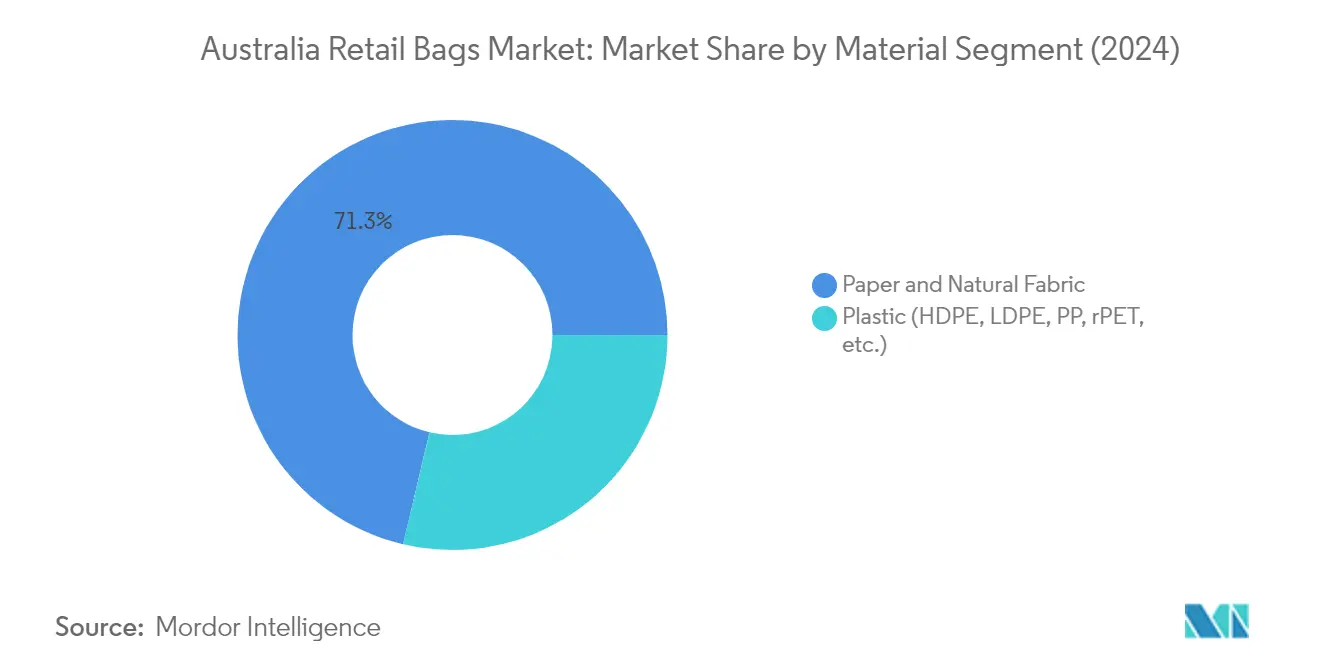

The paper shopping bags and natural fabric segment dominates the Australian retail bags market, commanding approximately 71% market share in 2024. This dominance is driven by increasing environmental consciousness and stringent regulations against plastic shopping bags usage. The segment's prominence is reinforced by major retailers like Woolworths partnering with local manufacturers to increase the supply of paper bags, particularly in response to the nationwide transition away from plastic shopping bags. The segment's growth is further supported by the Australian Packaging Covenant Organization's (APCO) initiatives promoting paper and paperboard packaging, which accounts for more than half of the overall packaging consumed in Australia. Paper shopping bags and natural fabric bags are experiencing the highest growth rate of around 7% during the forecast period 2024-2029, propelled by government regulations banning lightweight plastic shopping bags across various Australian states and territories, increasing adoption of sustainable retail packaging solutions by retailers, and growing consumer preference for eco-friendly alternatives.

Plastic Segment in Australia Retail Bags Market

The plastic shopping bags segment, encompassing HDPE, LDPE, PP, and rPET materials, represents approximately 29% of the market share in 2024. This segment continues to serve specific market needs where durability and moisture resistance are essential, particularly in applications requiring heavy-duty or reusable shopping bags. The segment maintains its presence through the production of bags with thickness greater than 35 microns, which are still permitted under current regulations. Manufacturers in this segment are increasingly focusing on developing recycled content solutions, with the Australian Packaging Covenant Organization (APCO) setting new targets for recycled content in plastic shopping bags. The segment is adapting to market demands by introducing innovations in recyclable and reusable plastic materials, though its growth is constrained by stringent regulations and shifting consumer preferences toward more sustainable alternatives.

Segment Analysis: By End-User Industry

Foodservice Segment in Australia Retail Bags Market

The foodservice segment dominates the Australian retail bags market, commanding approximately 51% market share in 2024. This dominance is driven by the robust growth of quick-service restaurants, cafes, and food delivery services across the country. The segment's prominence is attributed to the increasing consumer preference for takeaway and delivered meals, coupled with the rising number of cafes and restaurants operating across Australia, which exceeded 51,900 establishments. The surge in online food delivery platforms like UberEats, Menulog, and DoorDash has further amplified the demand for shopping bags in this sector. Additionally, the segment is experiencing the highest growth rate of around 6% for the forecast period 2024-2029, primarily due to the expanding food truck market, growing catering services sector, and increasing adoption of sustainable retail packaging solutions by major food service chains. The shift towards eco-friendly packaging materials and the implementation of strict regulations regarding single-use plastics have prompted foodservice operators to transition to more sustainable retail bags options.

Remaining Segments in End-User Industry

The grocery bags segment represents the second-largest end-user category, driven by the increasing adoption of online grocery shopping and the expansion of supermarket chains across Australia. The industrial segment caters to bulk packaging needs for food, chemical, and fertilizer products, while the hospitality segment utilizes merchandise bags primarily for events, tourism-related activities, and accommodation services. Other end-user industries, including cosmetics, personal care, pet food, e-commerce, footwear, apparel, and pharmaceutical sectors, collectively contribute significantly to the market's growth through their diverse packaging requirements and increasing focus on sustainable retail packaging solutions. The growing e-commerce sector and rising consumer awareness about environmental sustainability have prompted these segments to adopt more eco-friendly retail bags options, particularly paper and natural fabric-based solutions.

Australia Retail Bags Industry Overview

Top Companies in Australia Retail Bags Market

The Australian retail bags market features a mix of established domestic manufacturers and international players, with companies like Detmold Group, United Paper, Gispac, and Pacific National Industries leading the market. Product innovation has been primarily focused on developing sustainable and eco-friendly alternatives to plastic shopping bags, with companies investing in paper, cotton, and biodegradable materials. Operational agility has become crucial as manufacturers adapt to changing regulations around single-use plastics and evolving consumer preferences. Companies are strengthening their local manufacturing capabilities and forming strategic partnerships with retailers to ensure consistent supply. Market expansion strategies have centered on developing specialized products for different end-user segments, particularly in food service and grocery retail, while also enhancing distribution networks across major Australian cities.

Local Players Dominate Fragmented Market Structure

The Australian retail bags market exhibits a moderately fragmented structure with a strong presence of local manufacturers who have deep-rooted relationships with regional retailers and an understanding of local regulations. While global players like Berry Global Group maintain a presence, domestic companies hold significant market share due to their established distribution networks and ability to provide customized solutions. The market has seen limited consolidation activity, with companies preferring organic growth through capacity expansion and product development rather than acquisitions.

The competitive dynamics are characterized by a mix of large-scale manufacturers serving national retail chains and smaller specialists focusing on niche segments or specific geographical regions. Market participants range from family-owned businesses like Polypac Converting to larger conglomerates like Detmold Group that offer diverse retail packaging solutions. The industry structure supports both integrated manufacturers producing their own materials and converters who source materials from suppliers, creating varied business models within the market.

Innovation and Sustainability Drive Future Success

Success in the Australian retail bags market increasingly depends on companies' ability to develop sustainable solutions while maintaining cost competitiveness. Manufacturers must invest in research and development to create innovative materials and designs that meet both environmental regulations and consumer preferences. Building strong relationships with key retail chains and foodservice operators is crucial, as these sectors represent significant volume opportunities. Companies also need to develop efficient production processes and robust supply chains to manage raw material costs and ensure reliable delivery.

For new entrants and smaller players, focusing on specialized market segments and developing unique value propositions around sustainability or customization offers the best path forward. The risk of substitution from alternative packaging solutions remains moderate, primarily mitigated by convenience factors and regulatory support for certain materials like paper. Future regulatory changes around packaging materials and waste management will continue to shape market dynamics, making regulatory compliance and adaptability critical success factors. Companies that can balance environmental responsibility with operational efficiency while maintaining strong customer relationships will be best positioned for growth. Additionally, the integration of branded shopping bags and promotional shopping bags into product lines can offer competitive advantages in appealing to environmentally conscious consumers.

Australia Retail Bags Market Leaders

-

Detmold Group

-

United Paper

-

Gispac

-

Pacific National Industries Pty Ltd

-

Bag People Australia

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Australia Retail Bags Market News

- April 2024 - W23 Global unites five major players in the global grocery arena. Ahold Delhaize (operating in the US, Europe, and Indonesia), Tesco (based in the UK, ROI, and Europe), Woolworths Group (hailing from Australia and New Zealand), Empire Company Limited/Sobeys Inc. (representing Canada), and Shoprite Group (focused on Africa). This collaborative effort has birthed a new retail venture capital (VC) fund, aiming to invest USD125 million into the most innovative start-ups and scale-ups worldwide over the next five years. These investments are specifically targeted at revolutionizing the grocery retail landscape and tackling its sustainability challenges head-on.

- March 2024 - Visy, a packaging and resource recovery firm, has enhanced sustainability by introducing recyclable paper bags made in Australia. This move aims to reduce single-use plastics. The bags, made from thick paper with recycled content, are recyclable through local kerbside bins. Manufactured at Visy's Reservoir facility in Melbourne, these heavyweight bags are now available in retail stores nationwide.

Australia Retail Bags Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

- 4.1 Market Overview

-

4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

5. MARKET DYNAMICS

-

5.1 Market Drivers

- 5.1.1 The Growing Demand for Unit-sized Bags is Expected to Drive Growth

- 5.1.2 Legislative Changes will Propel the Growth of Paper-based Bags (State-wise Ban on Plastic Bags <35 microns)

-

5.2 Market Restraints

- 5.2.1 Near and Medium-term Dependence on Material Prices and the Dynamic Nature of the End-user Demand Expected to Pose Challenges

- 5.2.2 Anticipated Barriers to Entry for New Entrants Posed by Incumbents who have Established Partnerships with Retailers in the Country

- 5.3 Assessment of the Impact of COVID-19 and the Recent Changes on the Market in Australia

- 5.4 Analysis of the Retail and Foodservice Sector in Australia

- 5.5 Import-Export Analysis of Major Grades of Paper Bags and Sacks in Australia

- 5.6 Analysis of the Demand for Re-usable and Disposable Retail Bags in Australia

- 5.7 Material Innovations in Retail Bags Category

6. MARKET SEGMENTATION

-

6.1 By Material

- 6.1.1 Paper and Natural Fabric

- 6.1.2 Plastic (HDPE, LDPE, PP, rPET, etc.)

-

6.2 By End-user Industry

- 6.2.1 Foodservice

- 6.2.2 Grocery

- 6.2.3 Industrial

- 6.2.4 Hospitality

- 6.2.5 Other End-user Industries

7. COMPETITIVE LANDSCAPE

-

7.1 Company Profiles*

- 7.1.1 Detmold Group

- 7.1.2 United Paper

- 7.1.3 Gispac

- 7.1.4 Pacific National Industries Pty Ltd

- 7.1.5 Bag People Australia

- 7.1.6 Polypac Converting

- 7.1.7 PrimePac

- 7.1.8 JB Packaging

- 7.1.9 Berry Global Group

- 7.1.10 PakPlast International

8. INVESTMENT ANALYSIS

9. FUTURE OF THE MARKET

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Australia Retail Bags Industry Segmentation

Retail carry bags are utilized in the retail industry to help consumers. The introduction of reusable bags into the retail carry bags industry has proliferated. Retailers favor using plastic carry bags for their useful properties, such as being easy to use, economical, and store packaging format. The study defines the revenues generated by retail bag sales made from different materials, including paper and natural fabric and plastics, by various vendors. The market volume consists of the consumption of retail bags by consumers. The analysis is based on the market insights captured through secondary research and the primaries. It also covers the major factors impacting the growth of the retail bags market in terms of drivers and restraints.

The Australian retail bags market is segmented by material (paper and natural fabric and plastic (HDPE, LDPE, PP, rPET, etc.)) and end-user industry (foodservice, grocery, industrial, hospitality, and other end-user Industries). The report offers market forecasts and size in value (USD) for all the above segments.

| By Material | Paper and Natural Fabric |

| Plastic (HDPE, LDPE, PP, rPET, etc.) | |

| By End-user Industry | Foodservice |

| Grocery | |

| Industrial | |

| Hospitality | |

| Other End-user Industries |

Need A Different Region or Segment?

Customize Now

Australia Retail Bags Market Research Faqs

How big is the Australia Retail Bags Market?

The Australia Retail Bags Market size is worth USD 1.58 billion in 2025, growing at an 4.83% CAGR and is forecast to hit USD 2.00 billion by 2030.

What is the current Australia Retail Bags Market size?

In 2025, the Australia Retail Bags Market size is expected to reach USD 1.58 billion.

What years does this Australia Retail Bags Market cover, and what was the market size in 2024?

In 2024, the Australia Retail Bags Market size was estimated at USD 1.50 billion. The report covers the Australia Retail Bags Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Australia Retail Bags Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Australia Retail Bags Market Research

Mordor Intelligence offers a comprehensive analysis of the retail bags industry in Australia. Our research examines everything from shopping bags to luxury retail bags. We cover all major segments, including paper shopping bags, plastic shopping bags, and cloth shopping bags. Special attention is given to the emerging trends in biodegradable shopping bags. The report, available as an easy-to-download PDF, provides detailed insights into the carrier bags and store bags markets. It also includes an analysis of the branded shopping bags and promotional shopping bags sectors.

Stakeholders will benefit from our thorough examination of the reusable shopping bags and grocery bags segments. We provide a detailed analysis of retail packaging trends. The report explores the growing demand for tote bags and specialized merchandise bags. It also addresses sustainability initiatives in the department store bags and retail gift bags segments. Our analysis covers retail carry bags across various distribution channels, offering valuable insights for businesses involved in retail packaging and sustainable solutions. The comprehensive report PDF can be downloaded for immediate access to market insights and future projections.