Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

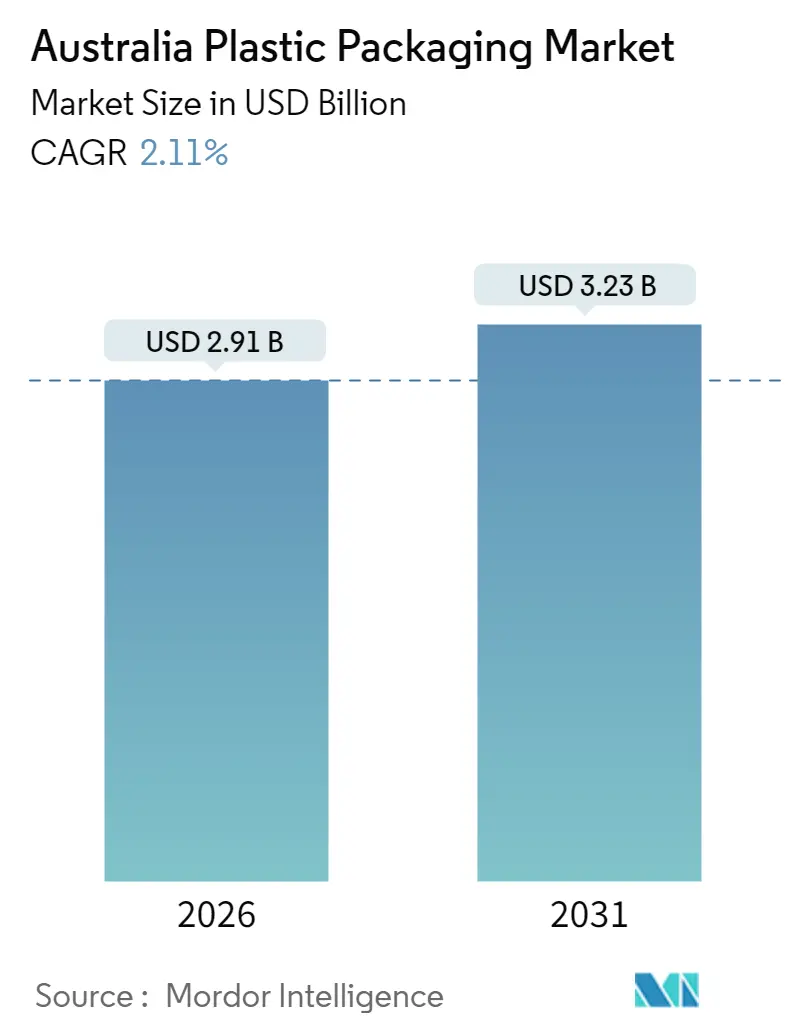

| Market Size (2026) | USD 2.91 Billion |

| Market Size (2031) | USD 3.23 Billion |

| Growth Rate (2026 - 2031) | 2.11% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Australia Plastic Packaging Market Analysis by Mordor Intelligence

Australia plastic packaging market size in 2026 is estimated at USD 2.91 billion, growing from 2025 value of USD 2.85 billion with 2031 projections showing USD 3.23 billion, growing at 2.11% CAGR over 2026-2031. This trajectory illustrates how e-commerce, food-grade recycling investments, and container deposit schemes work together to support volume growth while alleviating regulatory pressure. Investments worth more than USD 100 million through the Recycling Modernization Fund have begun filling gaps in soft-plastic collection and are catalyzing the development of new infrastructure that can supply food-grade rPET. Circular-economy incentives, together with rising consumer preference for refillable and concentrated product formats, are reshaping material choices toward polyethylene terephthalate and advanced mono-material laminates. Meanwhile, digital printing enables converters to profitably serve small and mid-sized brands, intensifying competition while also broadening the customer base for tailored, flexible formats.

Key Report Takeaways

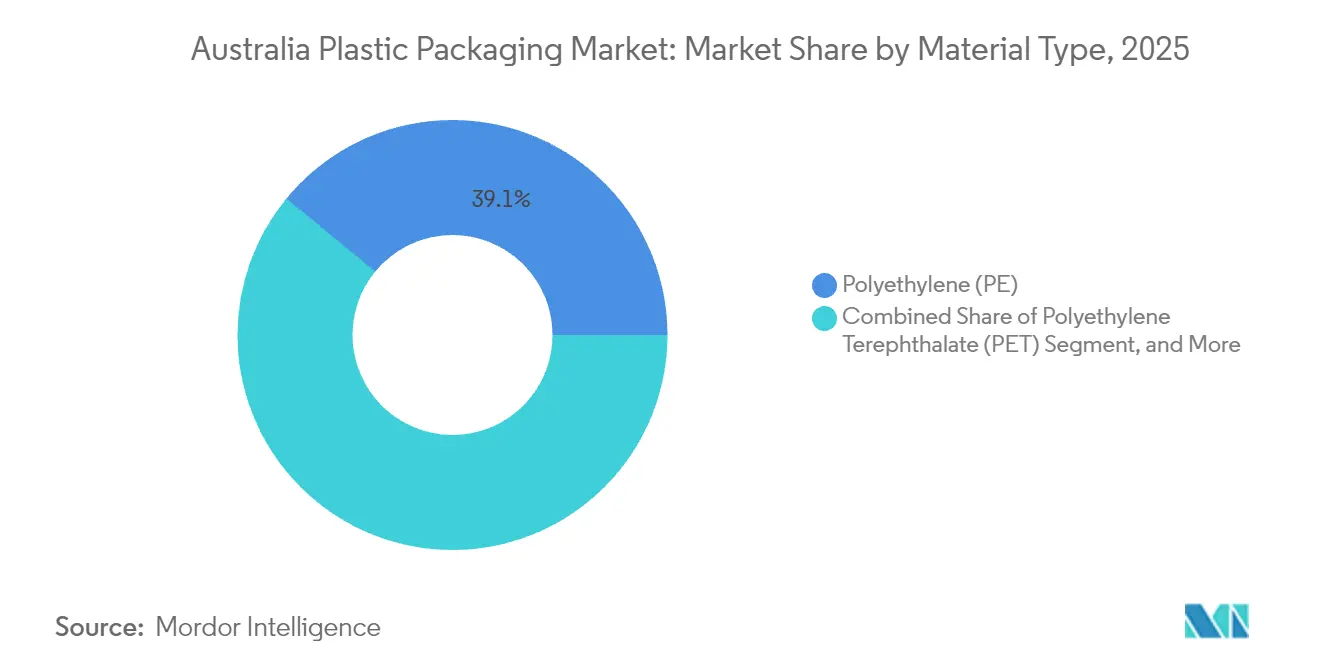

- By material type, polyethylene held 39.05% of Australia plastic packaging market share in 2025, while polyethylene terephthalate recorded the fastest 4.51% CAGR through 2031.

- By packaging type, flexible solutions captured 55.28% of Australia plastic packaging market size in 2025, and rigid alternatives are projected to lag at a 1.56% CAGR to 2031.

- By product form, pouches and sachets commanded 31.18% share of Australia plastic packaging market size in 2025, whereas films and wraps posted the highest 4.14% CAGR through 2031.

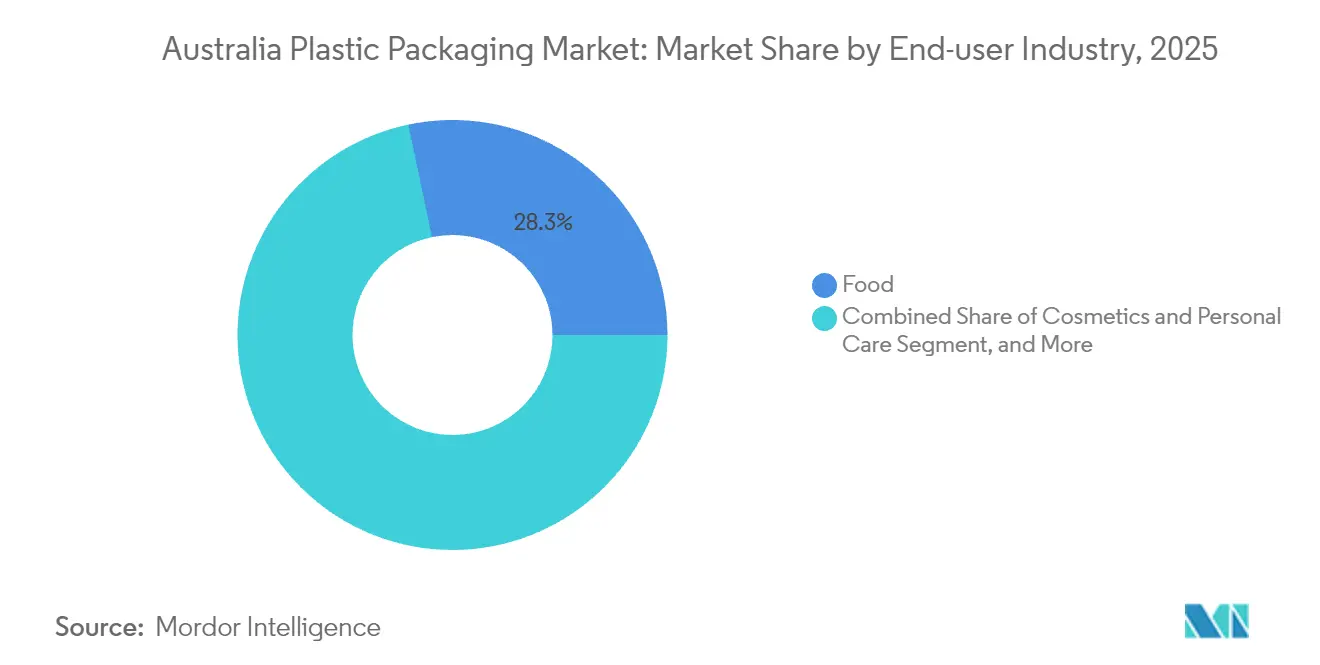

- By end-user industry, food applications led with a 28.29% share of Australia plastic packaging market size in 2025, while cosmetics and personal care achieved the strongest 5.11% CAGR to 2031.

- By manufacturing process, extrusion contributed 28.22% share of Australia plastic packaging market size in 2025, but thermoforming is advancing at a 5.03% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Australia Plastic Packaging Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for packaging from the food and beverage sector | +0.8% | National, concentrated in NSW, VIC, QLD | Medium term (2-4 years) |

| E-commerce and home-delivery boom fuelling lightweight, protective formats | +0.6% | National, early gains in Sydney, Melbourne, Brisbane | Short term (≤ 2 years) |

| Regulatory push for eco-friendly and recyclable plastic packaging solutions | +0.4% | National, led by SA and WA | Long term (≥ 4 years) |

| Expansion of domestic advanced recycling capacity enabling food-grade rPET supply | +0.3% | Victoria, NSW, SA | Medium term (2-4 years) |

| Harmonised state container deposit schemes generating high-quality PET and HDPE feedstock | +0.2% | National rollout, early success in NSW, SA | Long term (≥ 4 years) |

| Federal circular-economy incentives spurring regional investment in plastics reprocessing | +0.2% | Regional manufacturing hubs, Adelaide, Melbourne | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Packaging from the Food and Beverage Sector

Food and beverage producers have intensified their packaging use, growing packaging intensity 15% since 2022 as urban consumers demand extended shelf life and convenience. New investments worth USD 105.5 million by Coca-Cola Europacific Partners mirror sustained local demand for sports drinks and teas that need high-barrier containers. Food safety rules under the Australia New Zealand Food Standards Code favor plastic solutions that minimize contamination risk, offsetting environmental scrutiny. Export-oriented processors increasingly adopt modified-atmosphere packaging to enter Asian markets, pushing adoption of high-barrier pouches and trays. Combined, these trends keep Australia plastic packaging market on a steady growth path.

E-commerce and Home-Delivery Boom Fuelling Lightweight, Protective Formats

E-commerce volumes climbed 35% in 2024, driving demand for right-sized flexible packs that lower dimensional-weight freight charges while protecting contents during longer parcel journeys. [1]ePac Flexible Packaging, “ePac Custom Flexible Packaging Company,” epacflexibles.comAmcor’s USD 45 million stake expansion in ePac delivers digital printing capacity that slashes lead times for small Australian brands, enabling personalized designs at industrial scale. Automated fulfillment centers now specify engineered films with consistent tensile strength, steering converters toward mono-material laminates. These technology and logistics shifts strengthen the Australia plastic packaging market by opening high-margin niches beyond commodity films.

Regulatory Push for Eco-Friendly and Recyclable Plastic Packaging Solutions

South Australia and Western Australia implemented single-use plastics bans in September 2024, prompting national brands to reformulate portfolios and avoid dual supply chains. Detpak responded by launching a polybutylene succinate carton range that complies with the new rules. The Australian Packaging Covenant Organisation is tightening its co-regulatory model so that, from 2025, non-compliant packs risk delisting from major retailers. Visy’s USD 19.4 million (AUD 29 million) Smithfield upgrade secured government backing because it can deliver food-grade recycled content at industrial scale. Early compliance gives a first-mover advantage, reinforcing the competitive appeal of recycled-ready plastics and lifting Australia plastic packaging market value.

Expansion of Domestic Advanced Recycling Capacity Enabling Food-Grade rPET Supply

Chemical recycling plants are moving from concept to commercialization. APR Plastics and partners plan to convert 3,000 tonnes of multi-layer soft plastics into food-safe polypropylene each year, bridging a capability gap that mechanical processes cannot reach. Mondelez has agreed to source 1,000 tonnes of post-consumer recycled resin annually from Amcor, signaling confidence in the brand's domestic supply chains. Government grants of USD 40.2 million (AUD 60 million) under the Recycling Modernization Fund specifically target these processing bottlenecks, as noted by DCCEEW. Enhanced recycling capacity therefore stabilizes feedstock prices and anchors long-term growth in the Australian plastic packaging market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heightened environmental activism and consumer backlash against single-use plastics | -0.5% | National, strongest in urban centers | Short term (≤ 2 years) |

| Escalating bans and levies on problematic packaging formats across states | -0.4% | SA, WA leading, national expansion | Medium term (2-4 years) |

| Volatile imported rPET prices undermining domestic recyclate competitiveness | -0.3% | National supply chains | Short term (≤ 2 years) |

| Post-REDcycle collapse leaving limited soft-plastic collection infrastructure | -0.2% | National, acute in suburban areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Heightened Environmental Activism and Consumer Backlash Against Single-Use Plastics

Public sentiment shifted sharply after the REDcycle scheme collapsed in 2022, spurring skepticism toward recyclability claims. Retailers such as Coles have pivoted to paper-based pouches to pre-empt social media backlash over perceived greenwashing. Large brands face mounting pressure to document full material flows, sometimes sacrificing optimal shelf life to satisfy consumer optics. Zero-waste stores remain niche but wield outsized influence on public discourse, forcing mainstream companies to trial refill stations and concentrated product formats. This cautious environment can slow decision-making and temper volume growth in the Australian plastic packaging market.

Escalating Bans and Levies on Problematic Packaging Formats Across States

State legislation adds compliance complexity. South Australia’s 2024 ban now covers expanded polystyrene foodware, cotton buds, and other items, prompting national product reformulations. [2]New South Wales Environment Protection Authority, “Soft plastics recycling in NSW gets major new investment,” epa.nsw.gov.auWestern Australia’s parallel initiative has accelerated consultations in Queensland and Victoria. While levies under container-deposit schemes generate high-quality PET and HDPE, they also raise supplier costs that smaller firms struggle to absorb. The need to qualify multiple materials for disparate state rules slows innovation, constraining short-term growth of Australia plastic packaging market until a more uniform national standard emerges.

Segment Analysis

By Material Type: Polyethylene Dominance Faces Sustainability Pressure

Polyethylene retained a 39.05% share of the Australian plastic packaging market in 2025, thanks to its broad applicability across films, bottles, and closures. Growth, however, is decelerating as regulators and brand owners pivot toward resins with clearer closed-loop pathways. In contrast, polyethylene terephthalate posted a 4.51% CAGR outlook because container-deposit schemes nurture a clean stream of rPET suitable for food-grade bottles. Polypropylene is experiencing steady uptake in ready-meal trays that require microwave tolerance, although its recycling pathways remain less mature. Recyclability labeling under APCO increasingly favors PET and HDPE, eroding long-term polyethylene dominance in Australia plastic packaging market.

Polyethylene terephthalate’s share rise reflects investment in advanced depolymerization facilities that can turn mixed-colored flakes into resin equivalent to virgin material. Brands that use clear bottles gain higher recycling yields, creating a feedback loop that further boosts PET demand. Meanwhile, bioplastics carve out premium niches where claims of compostability justify cost premiums. The shift underscores how sustainability metrics, more than classical cost-performance trade-offs, now steer material decisions in Australia plastic packaging market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Packaging Type: Flexible Solutions Capture E-Commerce Growth

Flexible formats accounted for 55.28% of Australia plastic packaging market size in 2025, and their 3.81% CAGR exceeds that of rigid containers as online grocery grows. Lightweight pouches cut logistics emissions and enable tamper-evident seals that withstand parcel handling. Digital printing in short runs allows regional brands to refresh graphics for promotional campaigns without holding excess inventory. Rigid PET bottles still dominate carbonated beverages where gas retention is critical, but face margin pressure as deposit-scheme fees rise.

Converters rushing to qualify recyclable mono-material laminates are narrowing the recyclability gap between rigid and flexible formats. Companies that master the transition from multilayer foil barriers to high-barrier EVOH or all-polyethylene structures are well-positioned to capture market share. As a result, flexible packaging’s value proposition extends beyond freight savings to include end-of-life compliance, reinforcing its lead in the Australian plastic packaging market.

By Product Form: Pouches Lead Innovation While Films Expand Fastest

Pouches and sachets secured 31.18% share in 2025 by appealing to convenience-oriented consumers who want resealable and stand-up functionality. Films and wraps, although smaller in value, are projected to grow at a rate of 4.14% annually as automated fulfillment centers adopt engineered wrap formats that preserve the freshness of meal-kit ingredients. Bottles remain entrenched in beverages but lose market share in household cleaners, which are now sold as concentrate refills shipped in lightweight sachets.

The performance gap between conventional cling films and newer, breathable variants is shrinking, enabling fresh-produce exporters to meet Asian shelf-life standards without the need for excess ice or preservatives. Meanwhile, high-clarity lidding films enhance product visibility, a subtle yet influential factor in online grocery shopping, where photography often replaces in-store inspection. This iterative technical progress highlights how incremental innovations sustain Australia's momentum in the plastic packaging market.

By End-User Industry: Food Dominance Challenged by Beauty Growth

Food retained 28.29% of Australia plastic packaging market share in 2025 as busy consumers relied on ready-to-eat meals and extended-shelf-life produce. The segment’s growth aligns with investments by Smithfield and other processors in vacuum-skin packaging lines that lock in freshness. However, cosmetics and personal care outpace the market with a 5.11% CAGR, fueled by influencer-driven premiumization that rewards distinctive packaging. Beauty brands are early adopters of refill pods and concentrated serums shipped in dropper vials, which reduce overall plastic waste.

Pharmaceutical demand grows steadily as aging demographics increase prescription volumes, driving up blister-pack and bottle orders. Industrial users seek chemical-resistant drums made of high-density polyethylene that can withstand harsh solvents, a niche that offers margin insulation from retail price wars. The mix change toward higher-margin personal care keeps revenue growth ahead of tonnage growth in Australia plastic packaging market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Manufacturing Process: Thermoforming Leads Technology Innovation

Extrusion still commands 28.22% of 2025 volume, yet thermoforming is the star performer with a 5.03% CAGR through 2031. Advanced infrared heating and multi-zone ovens cut energy use by 30%, making thermoformed trays both cost-competitive and compliant with corporate emission targets. Injection molding sustains demand for caps and closures where dimensional accuracy is vital. Blow-molded containers are evolving toward tethered-cap designs required by European export markets, prompting Australian lines to upgrade their equipment.

Thermoforming’s ascendancy benefits regional plants that retrofit existing roll-stock equipment rather than investing in new injection presses. Producers pairing thermoforming with in-line trimming eliminate secondary handling, further boosting productivity. This process innovation supports the long-term competitiveness of Australia plastic packaging market.

Geography Analysis

New South Wales and Victoria together generated roughly 64.72% of Australia plastic packaging market value in 2025, reflecting dense populations and proximity to large food processors. Queensland followed with an 18.25% share as horticulture output expanded demand for breathable produce bags. South Australia and Western Australia combined for 12.08% yet punch above their weight in policy innovation, leading container deposit rollouts that raise recycled content demand. Regional centers grew at a rate of 3.14% annually, outpacing capital cities, as processors co-locate near farms to reduce freight miles and carbon footprints.

Recycling infrastructure mirrors this decentralization. Facilities in Kilburn (SA), Maddingley (VIC), and multiple NSW sites build a lattice that shortens transport loops for post-consumer plastics. These hubs collectively divert more than 43,000 tonnes of mixed plastics from landfills each year, supplying feedstock to converters on the eastern seaboard. The Northern Territory and Tasmania remain small but lucrative markets for high-margin mining services and gourmet-food exporters that demand premium barrier films.

Trans-Tasman integration lets companies such as Visy balance capacity between Australian and New Zealand plants, smoothing supply shocks and enhancing service levels. National standards emerging from APCO’s co-regulatory model reduce compliance disparity, yet state differences in single-use bans still require agile supply-chain planning. Geography therefore continues to shape logistics, regulatory strategy and investment priorities in Australia plastic packaging market.

Competitive Landscape

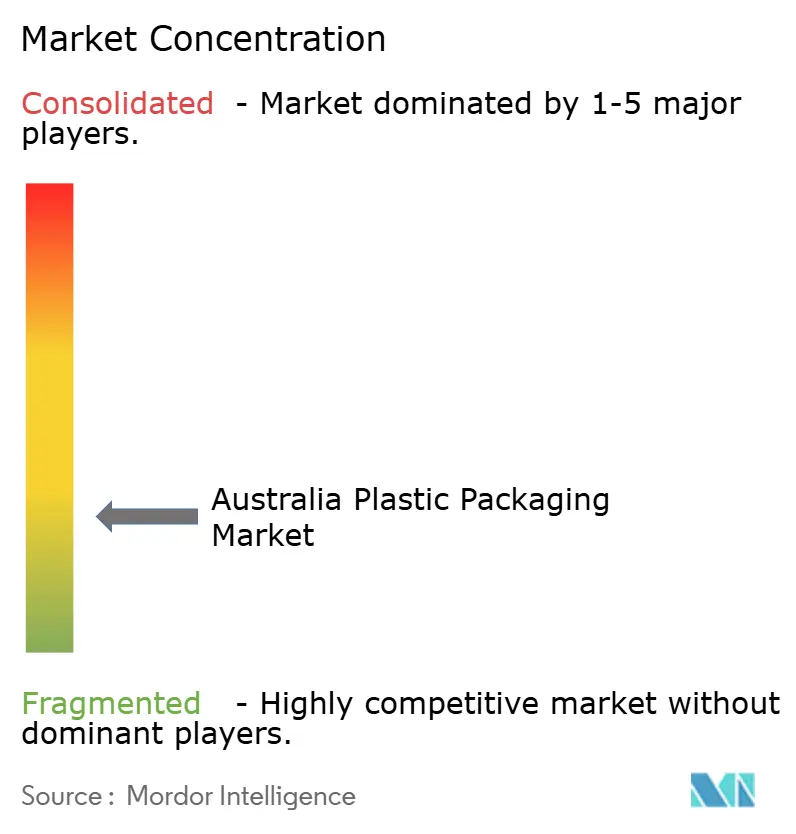

Australia plastic packaging market exhibits a fragmented structure. Amcor, Visy, and Pact Group leverage integrated resin-to-conversion capabilities and long-term contracts with multinational companies. Yet digital-native entrants such as ePac Flexible Packaging nibble share by offering sub-10-day lead times for runs below 25,000 packs, a segment the majors once ignored. Amcor’s planned USD 24 billion revenue after its merger with Berry Global extends scale advantages in material sourcing and R&D investment but invites antitrust scrutiny.

Sustainability drives consolidation of recycling assets. Visy’s purchase of Advanced Circular Polymers bolsters its closed-loop pitch and secures rPET supply amid volatile import prices. Pact Group’s AgriG8 drums demonstrate how circular models open niche revenue streams by capturing agricultural chemical container loops. Meanwhile, BioPak’s acquisition of Huskee adds reusable cup expertise, aligning with its corporate commitments to reducing packaging waste

Technology investments differentiate players. Close the Loop’s brand unification across 16 global businesses enhances cross-selling of collection, recycling and packaging services. Visy’s USD 100.5 million glass furnace in Penrith underscores how energy-efficient assets can double output while halving fuel use. Converters that integrate automation, digital printing and advanced recycling gain resilience in pricing negotiations, sustaining profitability within Australia plastic packaging market.

Australia Plastic Packaging Industry Leaders

Amcor plc

Visy Industries Australia Pty Ltd

Orora Packaging Australia Pty Ltd

Pact Group Holdings Ltd

Pro-Pac Packaging Ltd

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- January 2025: Amcor finalized its USD 13 billion all-scrip merger with Berry Global, creating a USD 24 billion packaging group.

- November 2024: Amcor announced the merger agreement with Berry Global, projecting USD 650 million cost synergies.

- September 2024: Pro-Pac Packaging reported USD 36.0 million losses and began building a 15,000-tonne soft-plastic recycling plant in Albury.

- September 2024: Federal and Victorian governments injected USD 10.5 million into soft-plastic recycling under the Recycling Modernisation Fund.

Australia Plastic Packaging Market Report Scope

Plastics are used in packaging materials for food, beverages, and oil. They are used mainly because of their performance, cost-effectiveness, and durability. Depending on the type of product being packed, plastics can be of different grades and material combinations, such as polyethylene, polypropylene, and polyvinyl chloride.

The Australian plastic packaging market is segmented by rigid packaging (material (polyethylene terephthalate (PET), polypropylene (PP), polystyrene (PS) and expanded polystyrene (EPS), polyvinyl chloride (PVC), and polyethene (PE)) and product (bottles and jars, trays and containers, and other product types)), flexible packaging (material (polyethene (PE), bi-orientated polypropylene (BOPP), cast polypropylene (CPP), polyvinyl chloride (PVC), and other flexible packaging materials) and product (pouches, bags, films and wraps, and other product types)), industrial plastic film market (stretch film and agricultural film), and end-user industry (food, beverage, healthcare, personal care and household, and other end-user industries). The market sizes and forecasts are in terms of value (USD) for all the above segments.

By Material Type

| Polyethylene (PE) |

| Polypropylene (PP) |

| Polyethylene Terephthalate (PET) |

| Polystyrene and EPS |

| Other Material Types |

By Packaging Type

| Flexible Plastic Packaging |

| Rigid Plastic Packaging |

By Product Form

| Bottles and Jars |

| Trays and Containers |

| Pouches and Sachets |

| Bags and Sacks |

| Films and Wraps |

| Other Product Forms |

By End-User Industry

| Food |

| Beverage |

| Pharmaceuticals and Healthcare |

| Cosmetics and Personal Care |

| Industrial |

| Other End-user Industries |

By Manufacturing Process

| Extrusion |

| Injection Molding |

| Blow Molding |

| Thermoforming |

| Other Manufacturing Processes |

| By Material Type | Polyethylene (PE) |

| Polypropylene (PP) | |

| Polyethylene Terephthalate (PET) | |

| Polystyrene and EPS | |

| Other Material Types | |

| By Packaging Type | Flexible Plastic Packaging |

| Rigid Plastic Packaging | |

| By Product Form | Bottles and Jars |

| Trays and Containers | |

| Pouches and Sachets | |

| Bags and Sacks | |

| Films and Wraps | |

| Other Product Forms | |

| By End-User Industry | Food |

| Beverage | |

| Pharmaceuticals and Healthcare | |

| Cosmetics and Personal Care | |

| Industrial | |

| Other End-user Industries | |

| By Manufacturing Process | Extrusion |

| Injection Molding | |

| Blow Molding | |

| Thermoforming | |

| Other Manufacturing Processes |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the projected value of Australia plastic packaging market by 2031?

It is forecast to reach USD 3.23 billion by 2031, growing at a 2.11% CAGR.

Which material is gaining the fastest share in Australian plastic packs?

Polyethylene terephthalate leads segment growth with a 4.51% CAGR on rising food-grade recycling capacity.

How are single-use bans affecting packaging suppliers?

State-level prohibitions accelerate shifts to recyclable or compostable alternatives, creating reformulation costs but also new product opportunities.

Why is thermoforming attracting fresh investment?

Energy-efficient heaters and quick tool changes reduce operating costs while meeting complex geometry needs, driving a 5.03% CAGR for the process.

Where are recycling infrastructure gaps being closed first?

Government grants prioritize new facilities in Kilburn, Maddingley and regional NSW to process soft-plastic streams into food-grade resin.