| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 1.07 Trillion |

| Market Size (2030) | USD 2.29 Trillion |

| CAGR (2025 - 2030) | 16.44 % |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Australia Payments Market Analysis

The Australia Payments Market size is estimated at USD 1.07 trillion in 2025, and is expected to reach USD 2.29 trillion by 2030, at a CAGR of 16.44% during the forecast period (2025-2030).

The Australian payments landscape is undergoing a fundamental transformation driven by rapid digitalization and changing consumer preferences. The shift away from traditional payment methods has accelerated significantly, with cash usage declining by approximately 30% over the past three years based on ATM withdrawal volumes. This transition reflects broader technological adoption across the financial services sector, where digital wallets like Apple Pay and Google Pay are becoming increasingly prevalent for everyday transactions. The integration of these digital payment solutions with existing banking infrastructure has created a more seamless and efficient payment ecosystem, enabling consumers to conduct transactions through multiple channels while maintaining security and convenience.

The New Payments Platform (NPP) has emerged as a cornerstone of Australia's modern payment infrastructure, processing over 2 million payments daily and accounting for approximately 25% of all account-to-account credit transfers. With more than 72 million account holders now having access to NPP's real-time instant payments capabilities, the platform has significantly enhanced the speed and efficiency of financial transactions across the country. This robust payment infrastructure has facilitated the growth of innovative financial services and fostered greater competition among payment service providers, leading to improved services and reduced transaction costs for both businesses and consumers.

The consolidation of payment systems under the Australian Payments Plus (AP+) banner marks a significant development in the industry's structure, bringing together BPAY, eftpos, and NPP Australia under unified governance. This merger, backed by major banks including Westpac, ANZ, CBA, and NAB, represents a strategic move to streamline payment systems and enhance operational efficiency. The integration of these platforms has created a more cohesive payment ecosystem, enabling better coordination of technological innovations and standardization of payment protocols across different channels.

The fintech sector has become increasingly prominent in shaping the future of payments, with numerous innovative companies introducing specialized payment solutions. Australian paytech companies like BeforePay, Pin Payments, and Assembly Payments are revolutionizing various aspects of the payment process, from instant access to earned wages to unified payment approaches for small and medium-sized businesses. These innovations are complemented by the advancement of payment technologies such as EMV chip cards and contactless payments, which have significantly enhanced transaction security and convenience. The industry's focus on technological advancement has led to the development of sophisticated payment gateways and payment processing systems that support multiple payment methods and cross-border transactions.

Australia Payments Market Trends

Rising Digital Payment Adoption and Mobile Wallet Integration

The Australian payments landscape is experiencing a fundamental shift driven by increasing consumer comfort with digital payment methods and digital wallet solutions. According to Marqeta's 2022 State of Consumer Money Movement study, an overwhelming 69% of Australians feel secure enough using digital wallets to leave their physical wallets at home, significantly outpacing adoption rates in other developed markets like the United States. This confidence is reinforced by the fact that 90% of Australian consumers rate mobile wallets as highly convenient for their daily transactions, while 86% report being able to make mobile payments wherever they wish, indicating the widespread acceptance and infrastructure support for digital payments across the country.

The integration of advanced payment technologies and biometric payment authentication methods has further accelerated the adoption of digital payment solutions. Banks have actively promoted mobile payments that utilize device biometrics for authentication, eliminating the need for PIN entry at payment terminals and enhancing both security and convenience. The expansion of payment options through digital wallets has created a more diverse and flexible payment ecosystem, with consumers increasingly storing their card details in digital wallets on mobile devices for contactless payments, reflecting a broader shift toward more sophisticated and user-friendly payment methods.

Understand The Key Trends Shaping This Market

Download PDF

Regulatory Support and Infrastructure Modernization

The Australian payments market is significantly propelled by progressive regulatory frameworks and continuous infrastructure modernization efforts. The Federal Government's financial market infrastructure (FMI) reforms, supported by the Reserve Bank of Australia's Payment Systems Board, have established a robust foundation for payment innovation and security. These regulatory initiatives have positioned Australia as a leading cross-border payment hub in real-time, facilitating more efficient and accessible international transactions while maintaining high payment security standards and consumer protection measures.

The implementation of open banking initiatives has created new opportunities for payment service providers and fostered innovation in the financial technology sector. The regulatory environment has encouraged the development of new payment networks and services, most notably the introduction of the New Payments Platform (NPP), which enables real-time, information-rich, account-to-account bank transfers using PayIDs. This infrastructure modernization has been complemented by the industry's move toward scheme tokenization, least cost routing, and enhanced security measures like Strong Customer Authentication (SCA), creating a more secure and efficient payment ecosystem that benefits both consumers and businesses.

Evolution of Consumer Payment Preferences

The transformation of consumer payment preferences has emerged as a significant driver in the Australian payments market, characterized by the rapid adoption of diverse payment methods and channels. The rise of Buy Now Pay Later (BNPL) services has been particularly noteworthy, with over half of Australians maintaining at least one BNPL account, forcing retailers to adapt their payment offerings to meet this growing demand. This shift in consumer behavior has led to the integration of multiple payment options at checkout points, including traditional credit cards, digital wallets, and installment payment solutions, creating a more inclusive and flexible payment environment.

The growing preference for omnichannel commerce has further reshaped the payment landscape, with consumers expecting seamless payment experiences across multiple channels—from online payments on e-commerce websites to social media platforms and physical stores. The emergence of shoppable posts across social media channels and the integration of payment capabilities into various customer touchpoints has created new opportunities for merchants to engage with customers. This evolution is particularly evident in the rising popularity of Click & Collect services, which has prompted retailers to develop more sophisticated payment software and fulfillment systems that bridge the gap between online and offline commerce while meeting consumer expectations for convenience and flexibility.

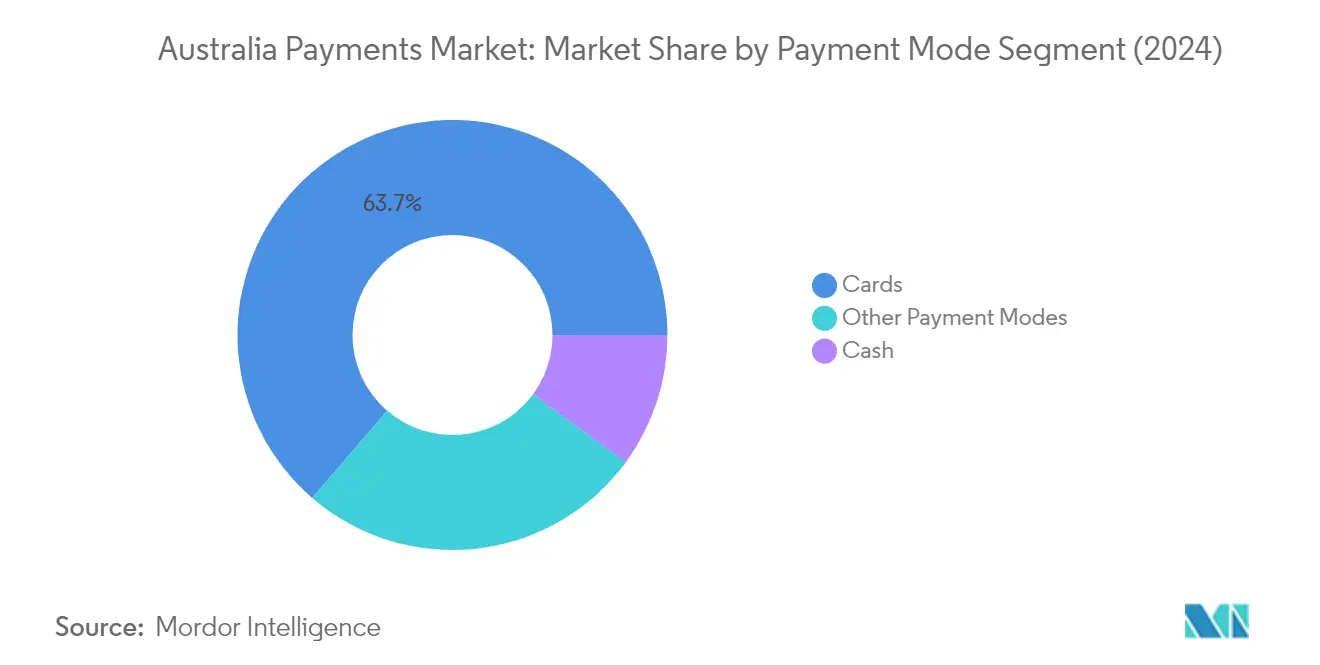

Segment Analysis: By Payment Mode

Cards Segment in Australia Payments Market

The cards segment dominates the Australian payments market, commanding approximately 64% market share in 2024. This segment, comprising debit cards, credit cards, and prepaid cards, has maintained its leadership position due to increasing consumer preference for digital and contactless card payments. The widespread acceptance of card payments across retail locations, coupled with the robust infrastructure of payment terminals and the growing e-commerce sector, has solidified its market position. Debit cards particularly stand out as the preferred payment method among Australian consumers, while credit cards continue to serve as a crucial payment tool for both personal and business transactions.

Cards Segment in Australia Payments Market

The cards segment is also experiencing the fastest growth in the Australian payments market, with an expected growth rate of approximately 7% during 2024-2029. This growth is primarily driven by the increasing adoption of contactless payments, the expansion of e-commerce platforms, and the integration of card payments with mobile wallets. The segment's growth is further supported by technological innovations such as tokenization and enhanced security features, making card payments more secure and convenient for consumers. Financial institutions and payment service providers are continuously introducing new card products and features to meet evolving consumer needs and maintain this growth momentum. The role of merchant services and payment acquisition strategies is pivotal in this expansion.

Remaining Segments in Payment Mode Market

The remaining segments in the Australian payments market include cash-based transactions through ATMs and EFTPOS, as well as other payment modes such as internet banking, BPAY, direct debits, and emerging payment solutions. While cash transactions continue to decline, EFTPOS remains an important part of the payment infrastructure, particularly for point of sale payments. The other payment modes segment has gained significance with the rise of digital banking solutions and innovative payment technologies. These segments collectively provide consumers and businesses with diverse payment options, ensuring flexibility and accessibility in the payment ecosystem. The development of payment hardware is crucial in supporting these diverse POS payments.

Australia Payments Industry Overview

Top Companies in Australia Payments Market

The Australian payments landscape is dominated by established financial institutions and innovative fintech players, including National Australia Bank (NAB), Westpac Bank, Suncorp Bank, Gobbill, Novatti, Fat Zebra, Ezypay, Mastercard, and Visa. The market is characterized by continuous product innovations, particularly in digital payment solutions, contactless technologies, and integrated payment platforms. Companies are focusing on technological advancement through AI integration, enhanced security features, and seamless payment experiences. Strategic partnerships and acquisitions have become increasingly common, as demonstrated by NAB's acquisition of digital bank 86400 and Citigroup's Australian consumer business. Operational agility is evident in the rapid adoption of digital transformation initiatives, with companies expanding their digital wallet offerings, developing new payment platforms, and enhancing their mobile payment capabilities to meet evolving consumer preferences.

Dynamic Market with Strong Growth Potential

The Australian payments market exhibits a fragmented yet competitive structure, with a mix of global payment networks, domestic banks, and emerging fintech players. Traditional banking institutions maintain significant market presence through their established infrastructure and customer base, while international players like Mastercard and Visa leverage their global networks and technological capabilities. The market is witnessing increased consolidation through strategic acquisitions and partnerships, particularly in the digital banking and payment technology segments, as companies seek to enhance their competitive positions and expand their service offerings.

The market dynamics are shaped by the strong presence of domestic financial institutions that compete with global payment solution providers. Merger and acquisition activities are primarily driven by the need to acquire technological capabilities, expand customer reach, and enhance digital service offerings. The competitive landscape is further intensified by the entry of fintech companies that bring innovative solutions and challenge traditional payment models, forcing established players to adapt and modernize their service offerings to maintain market relevance.

Innovation and Adaptation Drive Market Success

Success in the Australian payments market increasingly depends on the ability to innovate and adapt to changing consumer preferences while maintaining robust security measures. Incumbent players must focus on digital transformation, enhanced user experience, and seamless integration across payment channels to maintain their market position. The development of value-added services, strategic partnerships with fintech companies, and investment in emerging technologies are crucial for established players to defend their market share against new entrants and evolving competition.

For contenders seeking to gain ground, differentiation through specialized services, focus on underserved market segments, and technological innovation are key strategies. The market presents significant opportunities for players who can effectively address the growing demand for digital payment solutions while navigating regulatory requirements and security concerns. Success factors include the ability to build trust with consumers, maintain competitive pricing structures, and develop scalable solutions that can adapt to changing market conditions. The regulatory environment, particularly the government's Digital Economy Strategy and payment system reforms, will continue to shape competitive dynamics and market entry opportunities.

Australia Payments Market Leaders

-

Secure Pay

-

WorldPay

-

Pin Payments

-

2Checkout

-

Google Pay

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Australia Payments Market News

April 2022 - ANZ Worldline Payment Solutions, a joint venture between ANZ and global payments services company Worldline, has launched in Australia. Australian merchants will have access to some of the world's most advanced payment solutions, which have been proven in other markets and tailored to fit the specific needs of the Australian market.

March 2022 - Zepto, an account-to-account (A2A) merchant payments firm, has raised ASD 25 million in a Series A fundraising round headed by AirTree Ventures and Decade Partners in preparation for worldwide expansion.

Australia Payments Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definitions

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Stakeholder Analysis

-

4.3 Industry Attractiveness-Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Evolution of the payments landscape in Germany

- 4.5 Key market trends pertaining to the growth of cashless transaction in Germany

- 4.6 Impact of COVID-19 on the payments market in the country

5. MARKET DYNAMICS

-

5.1 Market Drivers

- 5.1.1 High Proliferation of E-commerce, including the rise of m-commerce and cross-border e-commerce supported by the increase in purchasing power

- 5.1.2 Enablement Programs by Key Retailers and Government encouraging digitization of the market

- 5.1.3 Growth of Real-time Payments in Germany

-

5.2 Market Challenges

- 5.2.1 Card Related Frauds to Pose Challenges to the Market Growth

-

5.3 Market Opportunities

- 5.3.1 Move towards Cashless Society

- 5.3.2 New Entrants to Drive Innovation Leading to Higher Adoption

- 5.4 Key Regulations and Standards in the Digital Payments Industry

- 5.5 Analysis of major case studies and use-cases

- 5.6 Analysis of key demographic trends and patterns related to payments industry in Australia (Coverage to include Population, Internet Penetration, Banking Penetration/Unbanking Population, Age & Income etc.)

- 5.7 Analysis of the increasing emphasis on customer satisfaction and convergence of global trends in Australia

- 5.8 Analysis of cash displacement and rise of contactless payment modes in Australia

6. Market Segmentation

-

6.1 By Mode of Payment

- 6.1.1 Point of Sale

- 6.1.1.1 Card Payments (includes Debit Cards, Credit Cards, Bank Financing Prepaid Cards)

- 6.1.1.2 Digital Wallet (includes Mobile Wallets)

- 6.1.1.3 Cash

- 6.1.1.4 Others

- 6.1.2 Online Sale

- 6.1.2.1 Card Payments (includes Debit Cards, Credit Cards, Bank Financing Prepaid Cards)

- 6.1.2.2 Digital Wallet (includes Mobile Wallets)

- 6.1.2.3 Others (includes Cash on Delivery, Bank Transfer, and Buy Now, Pay Later)

-

6.2 By End-user Industry

- 6.2.1 Retail

- 6.2.2 Entertainment

- 6.2.3 Healthcare

- 6.2.4 Hospitality

- 6.2.5 Other End-user Industries

7. Competitive Landscape

-

7.1 Company Profiles

- 7.1.1 Secure Pay

- 7.1.2 WorldPay

- 7.1.3 Pin Payments

- 7.1.4 2Checkout

- 7.1.5 Google Pay

- 7.1.6 Amazon Pay

- 7.1.7 eway

- 7.1.8 Square

- 7.1.9 Mastercard

- 7.1.10 Visa

- *List Not Exhaustive

8. Investment Analysis

9. Future Outlook of the Market

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Australia Payments Industry Segmentation

The Australian Payments Market is segmented by Mode of Payment (Point of Sale (Card Payments, Digital Wallet, Cash), Online Sale (Card Payments, Digital Wallet)), and by End-user Industries (Retail, Entertainment, Healthcare, Hospitality).

E-commerce payments include online purchases of goods and services such as purchases made on e-commerce websites and online booking of travel and accommodation. The market scope excludes online purchases of motor vehicles, real estate, utility bill payments (such as water, heating, and electricity), mortgage payments, loans, credit card bills, or purchases of shares and bonds. As for Point-of-Sale, all transactions that occur at the physical point of sale are included in the scope of the market. It includes traditional in-store transactions and all face-to-face transactions regardless of the location of the transaction. Cash is also considered for both cases (cash-on-delivery for e-commerce sales). The study looks at COVID-19's overall influence on the Australian payment ecosystem.

| By Mode of Payment | Point of Sale | Card Payments (includes Debit Cards, Credit Cards, Bank Financing Prepaid Cards) | |

| Digital Wallet (includes Mobile Wallets) | |||

| Cash | |||

| Others | |||

| Online Sale | Card Payments (includes Debit Cards, Credit Cards, Bank Financing Prepaid Cards) | ||

| Digital Wallet (includes Mobile Wallets) | |||

| Others (includes Cash on Delivery, Bank Transfer, and Buy Now, Pay Later) | |||

| By End-user Industry | Retail | ||

| Entertainment | |||

| Healthcare | |||

| Hospitality | |||

| Other End-user Industries | |||

Need A Different Region or Segment?

Customize Now

Australia Payments Market Research FAQs

How big is the Australia Payments Market?

The Australia Payments Market size is expected to reach USD 1.07 trillion in 2025 and grow at a CAGR of 16.44% to reach USD 2.29 trillion by 2030.

What is the current Australia Payments Market size?

In 2025, the Australia Payments Market size is expected to reach USD 1.07 trillion.

Who are the key players in Australia Payments Market?

Secure Pay, WorldPay, Pin Payments, 2Checkout and Google Pay are the major companies operating in the Australia Payments Market.

What years does this Australia Payments Market cover, and what was the market size in 2024?

In 2024, the Australia Payments Market size was estimated at USD 0.89 trillion. The report covers the Australia Payments Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Australia Payments Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Australia Payments Market Research

Mordor Intelligence delivers a comprehensive analysis of the payments industry, with a focus on electronic payments and emerging digital payments technologies. Our extensive research covers the complete ecosystem, ranging from traditional credit card and debit card solutions to modern digital wallet platforms and payment gateway infrastructure. The report, available as an easy-to-download PDF, provides detailed insights into online payments, bank transfer systems, and evolving mobile payments technologies. It also examines the growing adoption of contactless payments and cryptocurrency payments.

The report offers stakeholders valuable insights into payment solutions and payment services. It includes a detailed analysis of merchant services and payment processing systems. We thoroughly examine developments in payment infrastructure, payment security measures, and payment authentication protocols. The research covers various transaction types, including B2B payments, P2P payments, C2B payments, and international remittance. It also analyzes payment technology innovations in point of sale payments and instant payments. Our comprehensive coverage extends to payment software implementations, payment hardware solutions, and emerging trends in payment acquisition strategies. This provides stakeholders with actionable intelligence for informed decision-making.