Market Trends of Australia LNG Bunkering Industry

This section covers the major market trends shaping the Australia LNG Bunkering Market according to our research experts:

Ferries and OSV to Dominate the Market

- Ferries are vessels used to carry cargo and passengers across the water. A passenger ferry is used as a water bus or taxi to travel from one place to another. Various ferries include double-ended, hydrofoil, hovercraft, catamaran, roll-on/ roll-off, cruise ferry (RoPax), fast RoPax ferry, and others. OSVs also find heavy demand from the offshore oil and gas offshore wind energy sectors, where OSVs are essential during offshore construction and maintenance work.

- These vessels majorly operate on heavy fuel oil and marine gas oil. However, government regulations regarding the emission of sulfur, carbon dioxide, and other pollutants have encouraged using LNG as fuel in vessels. However, with the regulations related to sulfur content in the fuel, The option of using LNG as a fuel is attractive to these types of vessels because of the operating profile and economic, regulatory, and environmental reasons.

- Despite having no offshore wind farms, Australia has one of the highest offshore wind potentials globally due to its long coastline. The country has decided to invest in offshore wind to increase the share of renewable energy in the electricity generation mix. In December 2022, with approvals from relevant stakeholders, the Australian government formally declared the Bass Strait off Gippsland as Australia's first offshore wind zone and awarded Major Project Status to the Start of the South offshore wind farm.

- In July 2022, Shell Australia, a subsidiary of Shell, submitted an environment plan (EP) to the country's offshore regulator for development drilling on the Crux natural gas field off the coast of Western Australia.

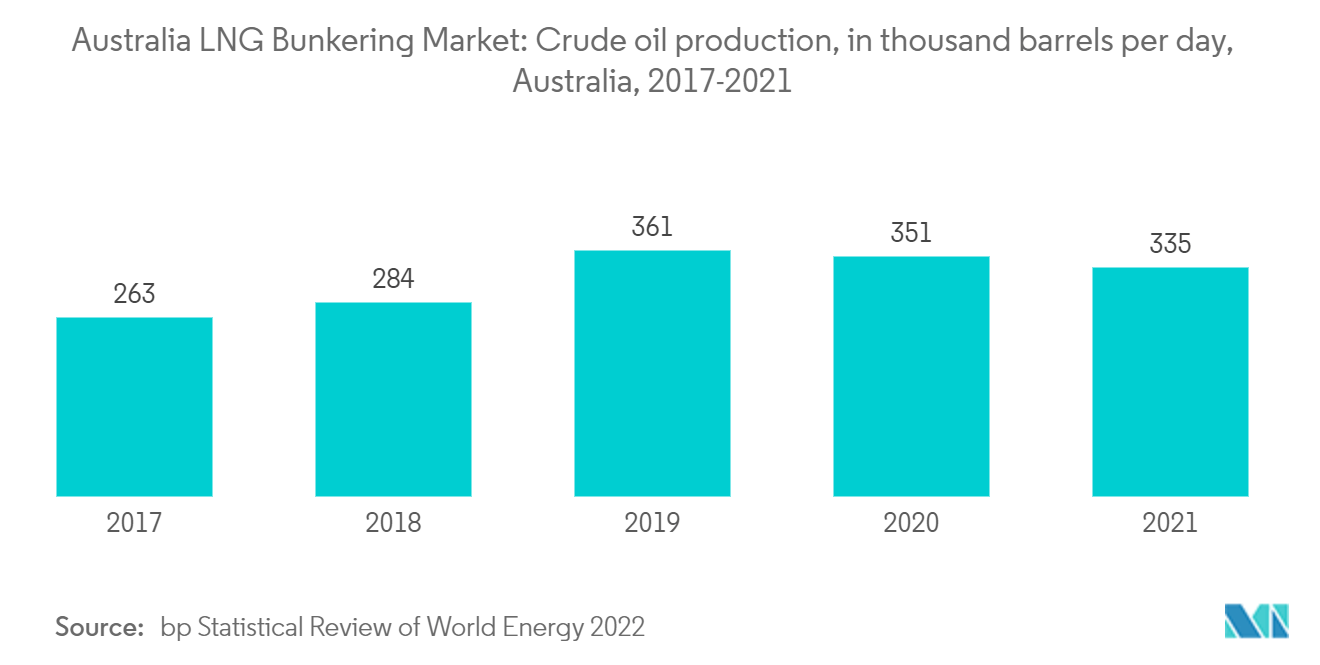

- The country is also making significant investments in offshore oil and gas production. As of 2021, Australia produced 335 thousand barrels/day of crude oil, which is expected to grow during the forecast period, primarily during rising investments in the oil and gas offshore sector.

- Hence, the increasing number of ferries and OSV fleets is expected to drive the demand for LNG-fueled fleets, driving the demand for the LNG bunkering market in Australia during the forecast period.

Understand The Key Trends Shaping This Market

Download PDF

Development in LNG Bunkering Facilities to Drive the Market

- Australia is expected to be one of the leading countries for the supply of LNG, whose demand is expected to witness a significant increase in the coming years. Establishing a strong LNG bunkering industry in Australia holds the potential to resurrect a domestic shipping fleet for coastal trading, utilizing LNG as a primary fuel source.

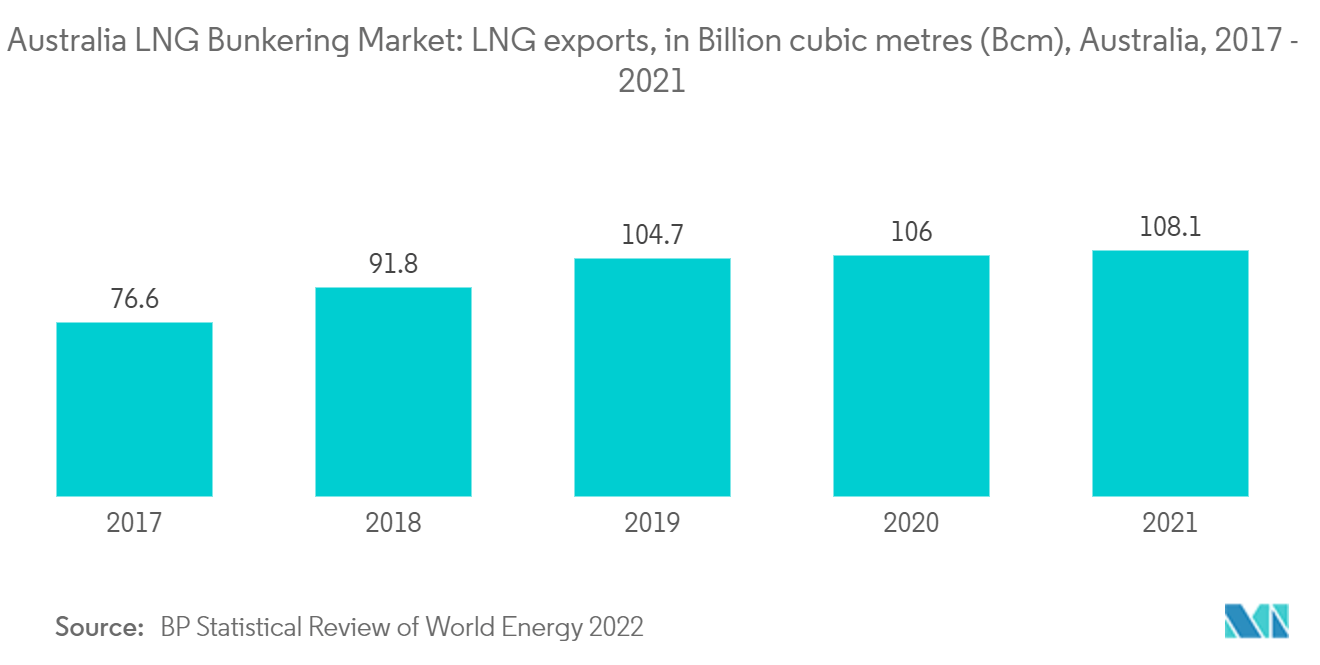

- Australia is one of the largest LNG producers and exporters globally, and in 2021, exports reached 108.1 Bcm, and with a global spike in energy demand, especially for LNG, export volumes are expected to rise. As most of Australia's LNG is exported via large LNG tankers, using LNG for refueling LNG tankers can both reduce emissions and lower costs due to easy availability of LNG. This is expected to drive the demand for LNG bunkering facilities in the country during the forecast period.

- In January 2023, Pilbara Clean Fuels (PCF) and Oceania Marine Energy agreed to work together to develop an 'end-to-end' low-carbon profile eLNG production and ship bunkering capability concept for the port of Port Hedland. The eLNG plant is being developed for the production of marine bunker fuel, with a base case capacity of 0.5 mtpa and a potential expansion to over 1 mtpa, and Oceania is expected to develop an LNG marine fuel bunkering business using a purpose-designed LNG refuelling vessel

- With the significant domestic LNG production available and commercial LNG bunkering now taking place in Fremantle and Pilbara Ports, Australia is well placed to use LNG as a maritime fuel to comply with the regulations. Hence, such developments are expected to drive the LNG bunkering market in Australia during the forecast period.