Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

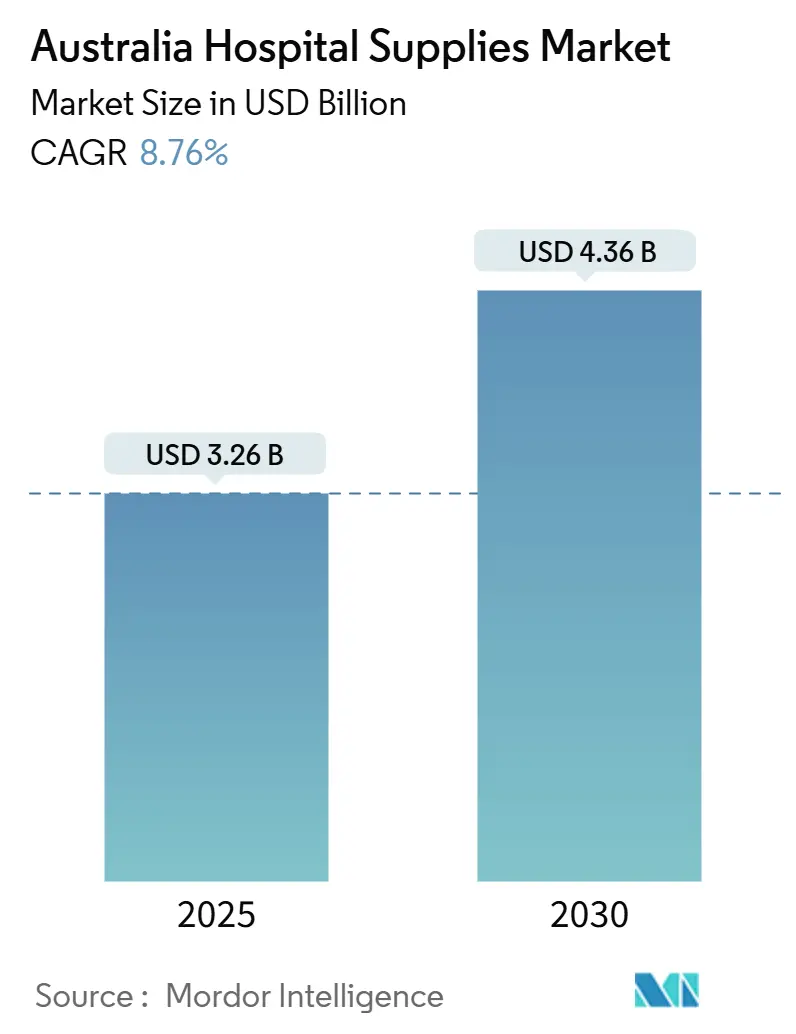

| Market Size (2025) | USD 3.26 Billion |

| Market Size (2030) | USD 4.36 Billion |

| Growth Rate (2025 - 2030) | 8.76% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Australia Hospital Supplies Market Analysis by Mordor Intelligence

The Australia Hospital Supplies Market size is estimated at USD 3.26 billion in 2025, and is expected to reach USD 4.36 billion by 2030, at a CAGR of 8.76% during the forecast period (2025-2030).

Rapid population ageing, surging chronic-disease admissions, and the nationwide pivot toward minimally invasive and day-surgery models are lifting baseline demand across disposables, diagnostic kits, and high-throughput sterilisation devices. Tighter infection-control rules, exemplified by the Therapeutic Goods Administration’s new Unique Device Identification framework, are steering procurement toward traceable, single-use and re-processable products that can demonstrate verifiable quality. Rising state and federal capital outlays for hospital infrastructure are fuelling orders for operating-room equipment and smart monitoring systems, while regional workforce shortages encourage bulk purchases of mobility aids that support faster patient turnover. From a competitive standpoint, global brands with in-house R&D and local servicing capabilities now emphasise value-based contracts that link product performance to measurable reductions in patient complications

Key Report Takeaways

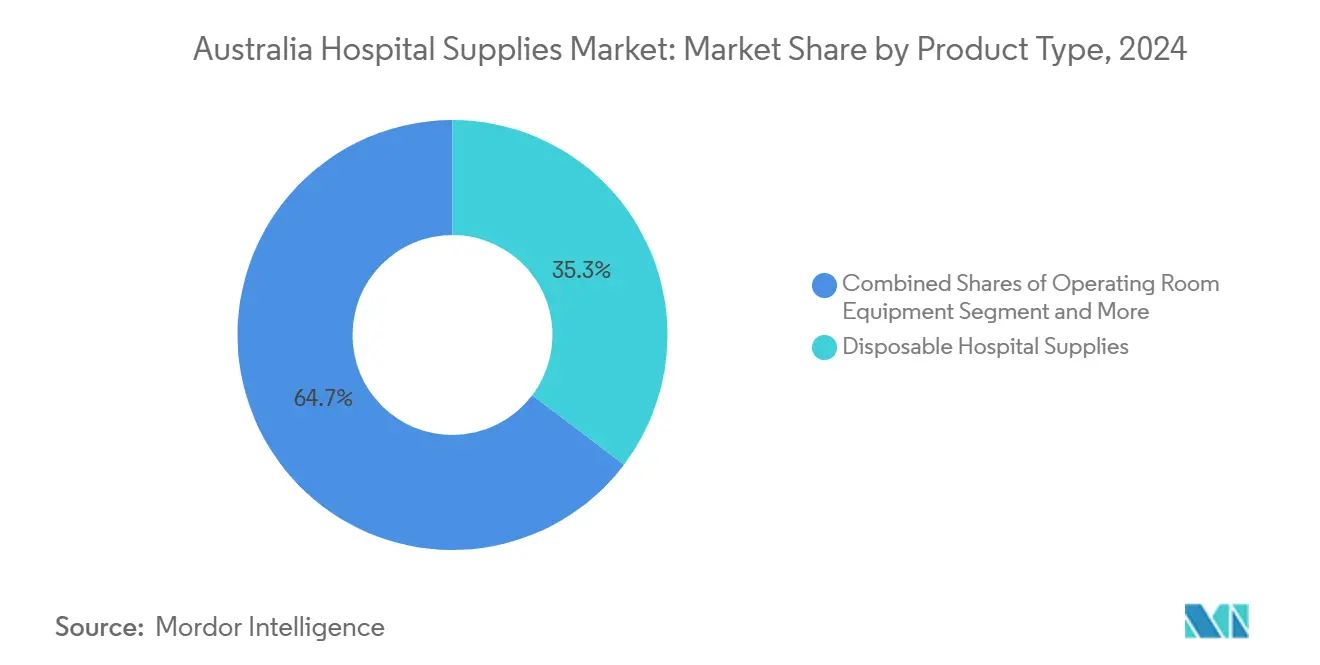

- By product type, disposables led with 35.32% of Australia's hospital supplies market share in 2024; sterilisation & disinfectant equipment is set to rise at a 9.63% CAGR through 2030, outpacing all other categories.

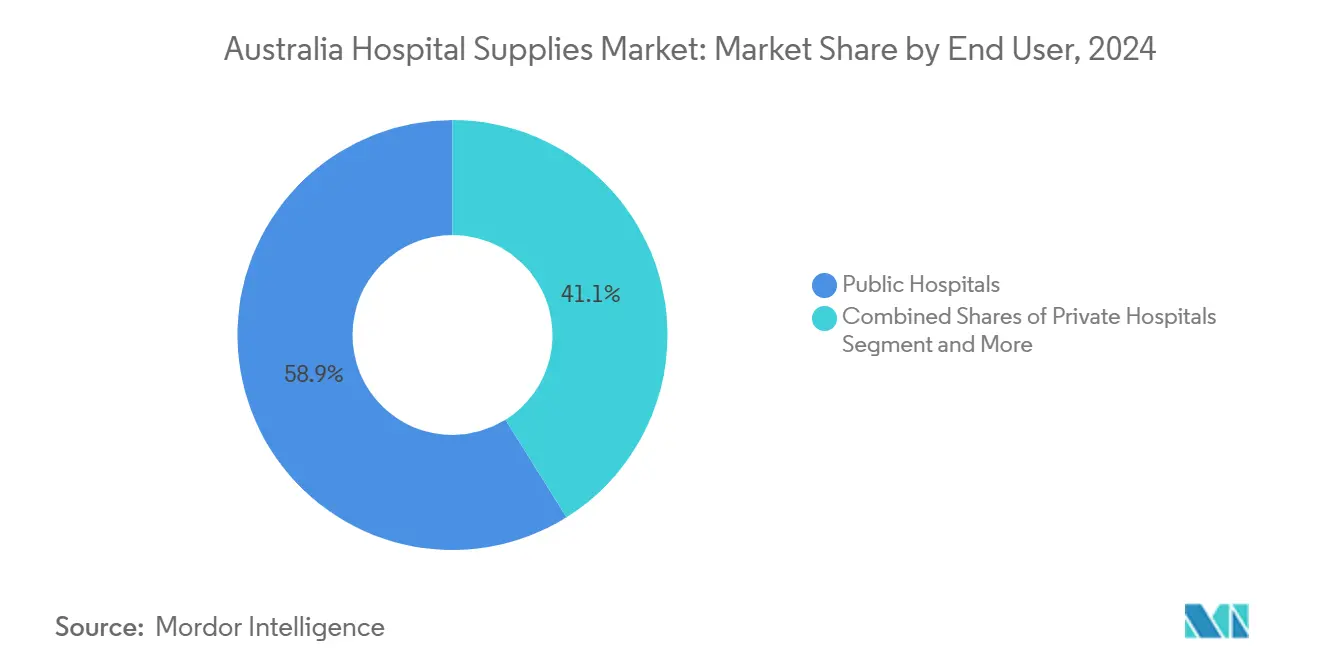

- By end user, public hospitals held 58.91% of Australia's hospital supplies market share in 2024, while private hospitals and day-surgery centres recorded the highest projected CAGR at 10.12% to 2030.

Australia Hospital Supplies Market Trends and Insights

Drivers Impact Analysis

| Drivers Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ageing population & chronic-disease admissions elevating baseline supply demand | +2.10% | National; metro focus | Long term (≥ 4 years) |

| Escalating federal & state healthcare capital expenditure on hospital infrastructure | +1.80% | NSW, Victoria | Medium term (2-4 years) |

| Surge in surgical procedure volumes—particularly minimally-invasive & day-surgeries | +1.50% | Major urban hubs | Medium term (2-4 years) |

| Rising multi-drug-resistant infections driving demand for advanced sterilisation solutions | +1.00% | High-density acute-care centres | Long term (≥ 4 years) |

| Shift to digital patient-monitoring increasing demand for connected examination devices | +1.20% | National | Medium term (2-4 years) |

| Regulatory Compliance Driving Growth | +1.40% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Ageing Population & Rising Chronic-Disease Admissions Elevating Baseline Supply Demand

Emergency-department presentations among Australians aged 65 years and above are forecast to jump 574% by 2050 compared with 2010 levels, sharply increasing utilisation of diagnostic consumables and patient-monitoring kits.[1]Mark Burkett, “Projected Growth in Emergency Presentations Among Older Australians,” Emergency Medicine Australasia, onlinelibrary.wiley.com Dementia patients are already exhibiting higher rates of hospital-acquired complications, driving sales of specialised pressure-injury dressings, fall-prevention mats, and innovative mobility aids. Unplanned hospitalisations for home-care recipients aged 65+ touch 39.8%, underscoring persistent reliance on acute settings even as community programmes scale. The Australia hospital supplies market, therefore, sees sustained orders for infection-control disposables and advanced wound-care portfolios that lower complication risk. Procurement policies now routinely bundle fall sensors, low-air-loss mattresses, and rapid sepsis-screening strips as integrated safety packages that appeal to overstretched clinical teams.

Escalating Federal & State Healthcare Capital Expenditure on Hospital Infrastructure

The 2024-25 Commonwealth Budget earmarked AUD 20.2 billion (USD 13.2 billion) for hospital expansion and equipment modernisation across priority states.[2]“Hospital Resources 2025 Budget Measures,” Australian Government Budget Papers, budget.gov.au Coupled with co-funding from New South Wales and Victoria, the programme channels fresh demand into surgical robotics, 4K endoscopy towers, and modular CSSD (Central Sterile Services Department) suites. Capital grants stipulate demonstrable lifecycle cost savings, motivating suppliers to offer energy-efficient autoclaves and IoT-enabled asset-tracking tags that align with green-hospital mandates. The Australian hospital supplies market thereby benefits from multi-year framework agreements that lock in baseline volumes and pave the way for incremental upgrades.

Surge in Surgical Procedure Volumes—Particularly Minimally-Invasive & Day-Surgeries

Ambulatory surgery now accounts for more than 90% of cataract procedures and 75% of hernia repairs in Australia, mirroring OECD peers.[3]“Day Surgery Trends in OECD Countries,” Organisation for Economic Co-operation and Development, oecd.org Shorter inpatient stays pivot inventory toward pre-packed disposable kits, single-use laparoscopic ports, and compact sterilisation trays that fit day-theatre cycles. Philips reports that its LumiGuide system trims procedure times by 37% and eliminates X-ray exposure, spurring hospitals to invest in light-based navigation consumables and disposable sensor arrays. With robotic platforms averaging USD 4.4 million per installation, group purchasing organisations increasingly negotiate bundled consumable contracts to offset capital costs, deepening supplier lock-in across the Australian hospital supplies market.

Rising Multi-Drug-Resistant Infections Driving Demand for Advanced Sterilisation Solutions

Outbreak-linked reports of carbapenem-resistant organisms in tertiary ICUs lead infection-control committees to mandate low-temperature plasma sterilisers, trace-element disinfectant indicators and antimicrobial instrument trays. Vendors pairing smart autoclaves with cloud analytics offer predictive maintenance and audit-ready cycle logs that assist hospitals in meeting AS/NZS 4187 compliance and lowering re-processing failures.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Emergence of home care services | -1.20% | National; higher impact in metropolitan areas | Medium term (2-4 years) |

| Stringent Australian regulatory framework for small & mid-size enterprises (SMEs) | -0.90% | National | Short term (≤ 2 years) |

| Sustainability regulations phasing down single-use plastics | -0.70% | National; stronger effect in states with active waste-levy schemes | Medium term (2-4 years) |

| Increasing purchasing power of group procurement organisations compressing margins | -0.60% | National; most pronounced in NSW and Victoria public-hospital clusters | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Emergence of Home-Care Services

Admissions to government-funded home-care programmes climbed 32% between FY 2017-18 and FY 2023-24, reaching 102,000 new placements.[4]“National Unique Device Identification System,” Therapeutic Goods Administration, tga.gov.au The shift siphons low-acuity cases from wards, tempering growth in basic linen packs and non-critical disposables. Yet demand for portable infusion pumps, tele-vital-sign monitors, and negative-pressure wound-therapy dressings climbs as clinicians support patients remotely. Suppliers are redesigning packaging to consumer-friendly formats and forging last-mile logistics partnerships, ensuring the Australian hospital supplies market continues to capture value even as care migrates to homes.

Stringent Australian Regulatory Framework for Small & Mid-Size Enterprises (SMEs)

Compliance with the new Medical Device Vigilance Program obliges manufacturers to maintain post-market incident databases and field-safety corrective action plans. For SMEs with limited quality-management infrastructure, costs rise, narrowing product portfolios, and delaying Australian launches. Hospitals respond by consolidating supplier panels in favour of firms with proven audit readiness. While safety gains are evident, the Australia hospital supplies market faces near-term product-variety constraints until smaller players adapt or pursue partnership strategies.

Segment Analysis

By Product Type: Disposables Remain Core While Sterilisation Equipment Accelerates

Disposable items, ranging from surgical gloves to isolation gowns, generated the most significant slice of the Australian hospital supplies market size at 35.32% in 2024. High turnover in emergency rooms and rising multi-resistant organisms alert to bulk orders for sterile drapes, sharps containers, and single-use procedure packs. National guidelines that obligation single-patient-use for numerous invasive accessories continue to elevate unit volumes. Suppliers differentiate through hypoallergenic materials and biodegradable polymers that align with hospital sustainability pledges and waste-levy caps. Private procurement groups now insist on end-to-end carbon disclosure, rewarding firms able to quantify lower incineration emissions.

Sterilisation & disinfectant equipment is the fastest-growing line, advancing at a 9.63% CAGR, well ahead of other categories in the Australian hospital supplies market. CSSDs are replacing legacy steam sterilisers with low-temperature hydrogen-peroxide plasma units that safeguard delicate optics and battery-integrated arthroscopy hand-pieces. Smart autoclaves log cycle parameters to cloud dashboards, enabling predictive maintenance and UDI-linked load traceability. Regional facilities—particularly in Queensland’s coastal belt—invest in compact tabletop sterilisers that support outreach clinics. Multinational vendors bundle consumable indicator strips and RFID load tags to lock in recurring revenue, inflating overall Australia hospital supplies market size for sterilisation inputs.

Patient examination devices, including digital stethoscopes and tablet-integrated otoscopes, capture a growing share as point-of-care documentation rises. Mobility aids & transportation equipment benefit from the National Disability Insurance Scheme’s support for functional-impairment aids, expanding beyond walkers to powered transfer-hoists that reduce manual-handling injuries. The “other types” cluster features smart hospital beds with integrated sensors and antimicrobial privacy curtains, signalling escalating sophistication in infection-control infrastructure throughout the Australia hospital supplies industry.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End User: Public Hospitals Dominate While Private Facilities Gain Momentum

Public hospitals controlled 58.91% of total demand in 2024, due to owning roughly two-thirds of the nation’s bed stock and 90% of emergency presentations. Procurement authorities increasingly pursue collective-tender models, awarding multiyear contracts that cover disposables, diagnostic reagents, and CSSD consumables. State supply agencies embed social-procurement clauses, prompting suppliers to source raw materials domestically where feasible. Cost containment imperatives deepen interest in closed-loop inventory systems that trace SKU consumption at the procedural level, feeding data into activity-based funding calculations.

Private hospitals and day-surgery centres are the fastest-growing customer bloc, set to post a 10.12% CAGR through 2030. Despite pandemic-era profit compression, admissions returned to 4% growth in FY 2024, propelled by elective-surgery wait-list transfers and insurer incentives. Facilities highlight shorter waiting times and hotel-style amenities, spurring investment in premium disposables such as latex-free gown lines and colour-coded trocar kits. Agile procurement privileges suppliers able to guarantee next-day replenishment and loan sets for complex orthopaedics, helping them carve a strategic niche within the Australia hospital supplies market. Specialist clinics & rehabilitation centres widen usage of robotics-assisted physiotherapy aids, drawing on an ageing cohort seeking post-acute functional recovery programmes.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

New South Wales (NSW) and Victoria house the most significant clusters of tertiary and quaternary hospitals, together accounting for a significant share of the overall Australian hospital supplies market demand in 2024. Integrated-care pilots in Western Sydney and Melbourne’s north emphasise cross-setting supply visibility, encouraging suppliers to provide interoperable tracking software alongside disposables. High urban density concentrates outbreaks of multi-drug-resistant organisms, fostering above-average purchase rates for single-use laryngoscopes and bactericidal surface wipes.

Regional and remote jurisdictions face logistical challenges that drive higher per-capita procurement of inventory with long shelf lives. Northern Territory and parts of Western Australia stockpile heat-stable intravenous solutions and solar-powered vaccine refrigerators, mitigating long lead times caused by seasonal road closures. Government freight subsidies under the Remote Area Health Corps programme ensure parity of supply, reinforcing demand predictability in these zones of the Australia hospital supplies market. Telehealth expansion, combining satellite broadband and clinician-guided home-diagnostic kits, further diversifies supply patterns, moving certain SKUs directly to patients rather than regional hospitals.

Queensland records the fastest growth, aided by accelerated population gains along the Sunshine Coast and large capital programmes such as the AUD 1.8 billion (USD 1.2 billion) expansion of Sunshine Coast University Hospital. Surge capacity planning prioritises modular theatre builds equipped with quick-connect gas outlets and portable CSSD pods. Western Australia invests in high-acuity emergency departments to service mining districts, boosting acquisition of rapid blood-gas analysers and rugged patient-transport stretchers. Across all states, the Medical Science Co-Investment Plan and supply-chain diversification policies cultivate domestic manufacturing for sterile packs and complex electrosurgical tips, tempering exposure to freight volatility and enhancing the long-term resilience of the Australia hospital supplies market.

Competitive Landscape

Competitive Landscape

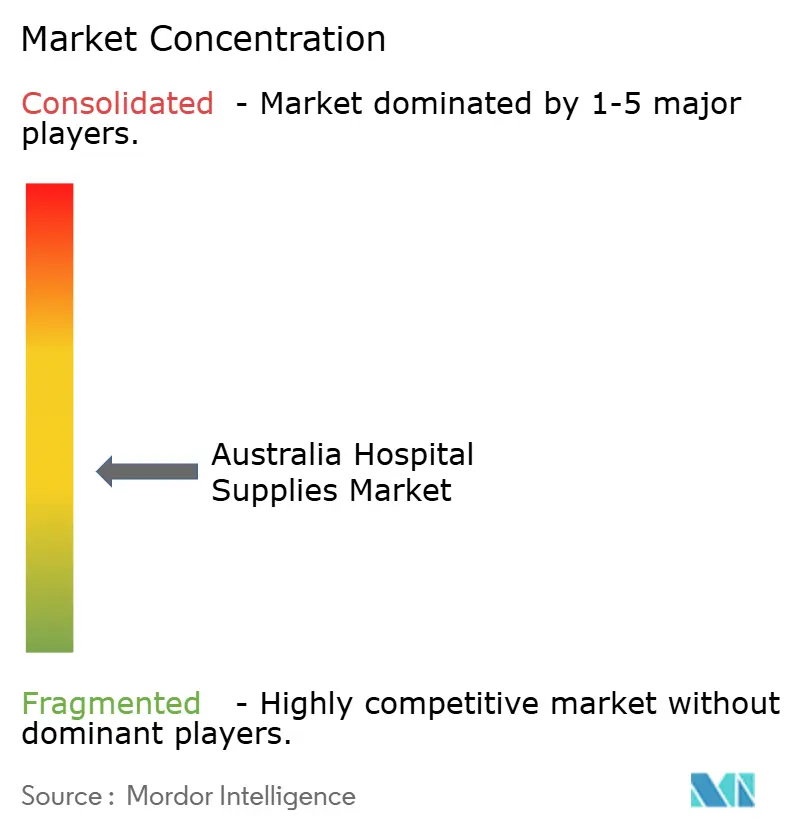

Competition is moderate, with the top five vendors controlling an estimated major share of Australia's hospital supplies market revenue. Global conglomerates such as Johnson & Johnson, Medtronic, and Philips leverage multi-country regulatory dossiers and scale efficiencies, yet maintain local technical support centres to comply with TGA serviceability requirements. Local manufacturers specialise in niche sterilisation accessories and custom procedure packs, often partnering with hospital-based clinicians to co-design new product iterations that meet Australian Standard AS/NZS 4187 compliance cycles.

Strategic alliances between suppliers and health-service networks foster shared-savings models under which vendors provide capital equipment at reduced upfront cost in return for long-term consumables commitments. Johnson & Johnson’s 2025 acquisition of Shockwave Medical brings intravascular lithotripsy devices into its cardiovascular bundle, expanding opportunities for hospital-wide platform contracts that consolidate purchasing lines. Philips uses data from pilot deployments of LumiGuide to negotiate outcome-based agreements that link payment levels to measured reductions in radiation exposure and procedure time, differentiating within the technology-intensive segments of the Australia hospital supplies market.

White-space growth areas include biodegradable instrument packaging, closed-loop sterilisation indicators that integrate with electronic medical records, and smart beds capable of automated micro-turning to prevent pressure injuries. Vendors that invest in locally relevant R&D such as humidity-resistant wraps tailored for tropical northern regions gain preferential access to state procurement panels across all tiers of the Australia hospital supplies industry.

Australia Hospital Supplies Industry Leaders

-

B. Braun Melsungen AG

-

Becton, Dickinson and Company

-

Cardinal Health Inc.

-

ResMed Inc.

-

3M

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- May 2025: The Australian Government has unveiled preliminary plans to expand Mount Druitt Hospital in New South Wales, as part of a broader AUD 120 million (USD 77 million) investment to upgrade Blacktown and Mount Druitt Hospitals. This initiative, which aims to add 60 additional beds across the two facilities, marks a significant development in the Australia hospital supplies market, reflecting ongoing efforts to enhance healthcare infrastructure and capacity.

- May 2025: Johnson & Johnson acquired Shockwave Medical for USD 13.1 billion, expanding its portfolio of intravascular lithotripsy devices for treating calcified plaque in heart diseases, strengthening its position in the cardiovascular segment of the Australian hospital supplies market

- April 2025: The Therapeutic Goods Administration implemented the Unique Device Identification (UDI) regulatory framework, requiring manufacturers to obtain UDI-Device Identifiers and include UDI in labeling and packaging, enhancing device identification and traceability in the Australian market

- August 2024: The Australian Capital Territory (ACT) Government's announcement of CPB Contractors and Multiplex Construction as shortlisted candidates for the Northside Hospital Project in Bruce, ACT, Australia, a venture exceeding a billion dollars.

- July 2024: The South Australian (SA) Government's AUD 117m (USD 78.84m) expansion of Modbury Hospital represents a key development in the Australian hospital supplies market. This initiative aims to enhance healthcare services in Adelaide's northeastern suburbs. It includes the establishment of a new cancer center and an increase in mental health beds.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Australia hospital supplies market as yearly sales to public and private hospitals, including day-surgery centers, of routine patient-examination devices, core operating-room tools, mobility and transport aids, sterilization or disinfectant systems, and single-use consumables. The flow is traced from manufacturer or distributor to the hospital loading dock and aligns with Therapeutic Goods Administration product codes.

Scope Exclusions: Heavy imaging capital equipment, home-care only consumables, pharmaceuticals, and aftermarket service contracts lie outside this frame.

Segmentation Overview

- By Product Type

- Patient Examination Devices

- Operating Room Equipment

- Mobility Aids and Transportation Equipment

- Sterilisation and Disinfectant Equipment

- Disposable Hospital Supplies

- Other Types

- By End User

- Public Hospitals

- Private Hospitals and Day-Surgery Centres

- Specialist Clinics and Rehabilitation Centres

Detailed Research Methodology and Data Validation

Primary Research

We spoke with procurement chiefs, group-purchasing heads, and infection-control nurses across New South Wales, Victoria, and Queensland. Their insights on consumption ratios, discount bands, and tender calendars grounded our secondary findings and filled information gaps.

Desk Research

Mordor analysts collected admission counts, bed numbers, and procedure volumes from Australian Institute of Health and Welfare tables, matched public spend data from the Australian Bureau of Statistics, and linked landed quantities in TGA import logs with state tender prices to derive average selling points. Company filings obtained through D&B Hoovers and news screened in Dow Jones Factiva clarified supplier revenue splits and expansion plans, while briefs from the Medical Technology Association of Australia described usage norms. The sources named are illustrative; numerous additional publications supported data checks and terminology alignment.

Market-Sizing & Forecasting

According to Mordor Intelligence modelling, a top-down construct multiplies inpatient admissions, average length of stay, surgical counts, and per-bed disposable intensity to rebuild demand. It then adjusts totals with selective bottom-up vendor roll-ups and channel checks. Core variables include public-private bed mix, day-surgery throughput, sterilization-cycle frequency, average selling-price drift, and replacement rates. A multivariate regression on population aged 65 and older, real health-spend growth, and infection prevalence shapes the 2025-2030 curve, while expert scenarios stress-test extremes. Gaps are bridged with median tender price curves.

Data Validation & Update Cycle

Outputs clear three analyst reviews; variances prompt call-backs to sources, and anomalies are traced to raw inputs. Models refresh each year, with rapid updates released for material policy or supplier events, ensuring clients receive the latest view.

Why Mordor's Australia Hospital Supplies Baseline Stands Firm

Published estimates often diverge because some fold primary-care spend into totals, apply list prices, or stretch global ratios to Australia, whereas our scope sticks to verified hospital purchasing and is rebuilt every fiscal year with local inputs.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.26 B (2025) | Mordor Intelligence | - |

| USD 5.00 B (2024) | Global Consultancy A | Includes out-of-hospital PPE; no margin adjustment |

| USD 5.50 B (2024) | Industry Tracker B | Adds capital equipment; uses list prices |

A disciplined scope, Australia-specific signals, and timely refresh cycles let Mordor Intelligence give decision-makers a balanced, transparent baseline they can trust.

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size of the Australia hospital supplies market?

The market is valued at USD 3.26 billion in 2025 and is forecast to reach USD 4.36 billion by 2030, growing at an 8.8% CAGR.

Which product category commands the largest market share?

Disposables lead at 35.32% Australia hospital supplies market share, reflecting persistent infection-control priorities.

Why is sterilisation equipment growing so rapidly?

Stricter infection-control guidelines and the need for re-processing delicate minimally invasive instruments are propelling a 9.6% CAGR in this segment.

Which end-user segment is expanding fastest?

Private hospitals and day-surgery centres, supported by shorter waiting times and specialised care, are projected to grow at 10.12% annually through 2030.

Page last updated on: