Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

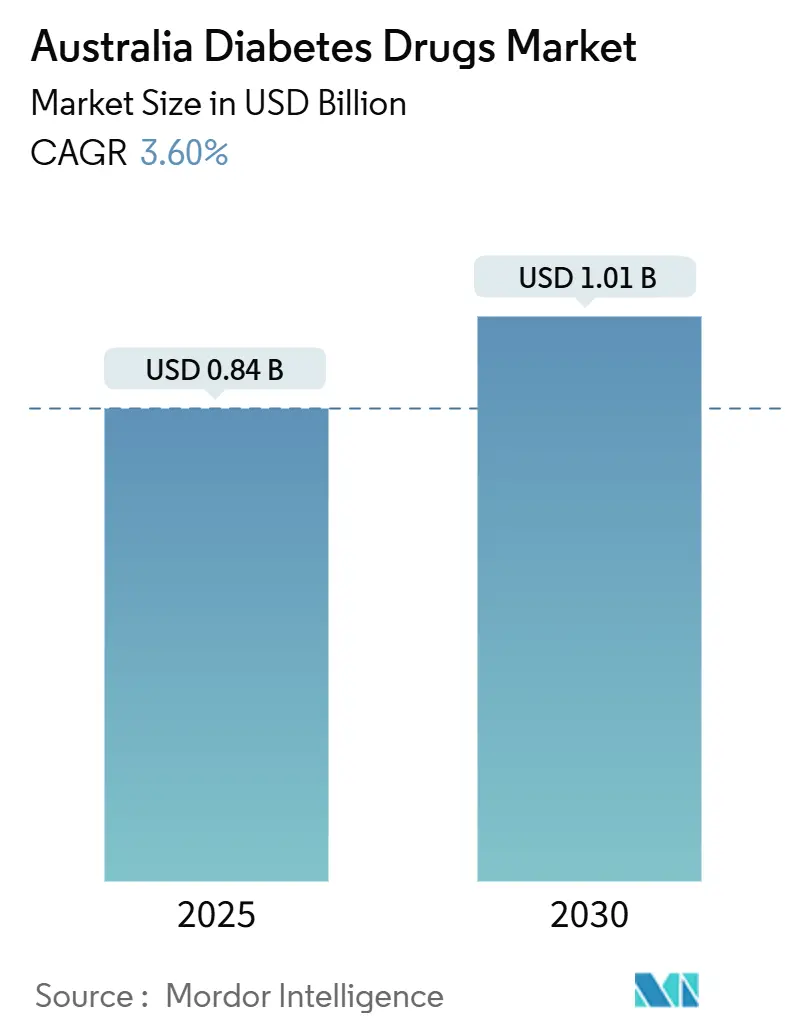

| Market Size (2025) | USD 0.84 Billion |

| Market Size (2030) | USD 1.01 Billion |

| Growth Rate (2025 - 2030) | 3.60% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Australia Diabetes Drugs Market Analysis by Mordor Intelligence

The Australia Diabetes Drugs Market size is estimated at USD 0.84 billion in 2025, and is expected to reach USD 1.01 billion by 2030, at a CAGR of 3.60% during the forecast period (2025-2030).

The COVID-19 epidemic boosted the expansion of the Australia Diabetes Drugs Market. Diabetes patients infected with COVID-19 may have high blood glucose levels, irregular glucose variability, and diabetic complications. According to the Australian Government Department of Health and Aged Care, there have been 92,35,681 confirmed cases of COVID-19 in Australia since the pandemic's commencement in July 2022. Diabetes prevalence in adults with COVID-19 produced a substantial increase in COVID-19 severity and mortality in people with type 1 (T1DM) or type 2 diabetes mellitus (T2DM), particularly in connection with poor glycemic control. While new-onset hyperglycemia and diabetes (both T1DM and T2DM) have become more recognized in the setting of COVID-19 and have been linked to worse outcomes. To minimize aggravation, a patient's blood glucose should be checked and maintained on a regular basis, emphasizing the significance of diabetes care medicines.

Obesity, a poor diet, and physical inactivity are all contributing to a rise in the number of newly diagnosed Type 1 and Type 2 diabetes cases. The fast-rising incidence and prevalence of diabetes patients, as well as healthcare spending in industrialized nations, are indicators of increased use of diabetic care products. Furthermore, rising diabetes incidence and increased usage of insulin delivery devices are boosting market expansion. Leading manufacturers are focused on technical advancements and the creation of improved goods to achieve a significant market share.

Australia Diabetes Drugs Market Trends and Insights

Oral-Anti Diabetes Drugs is Having the Highest Market Share in the Current Year.

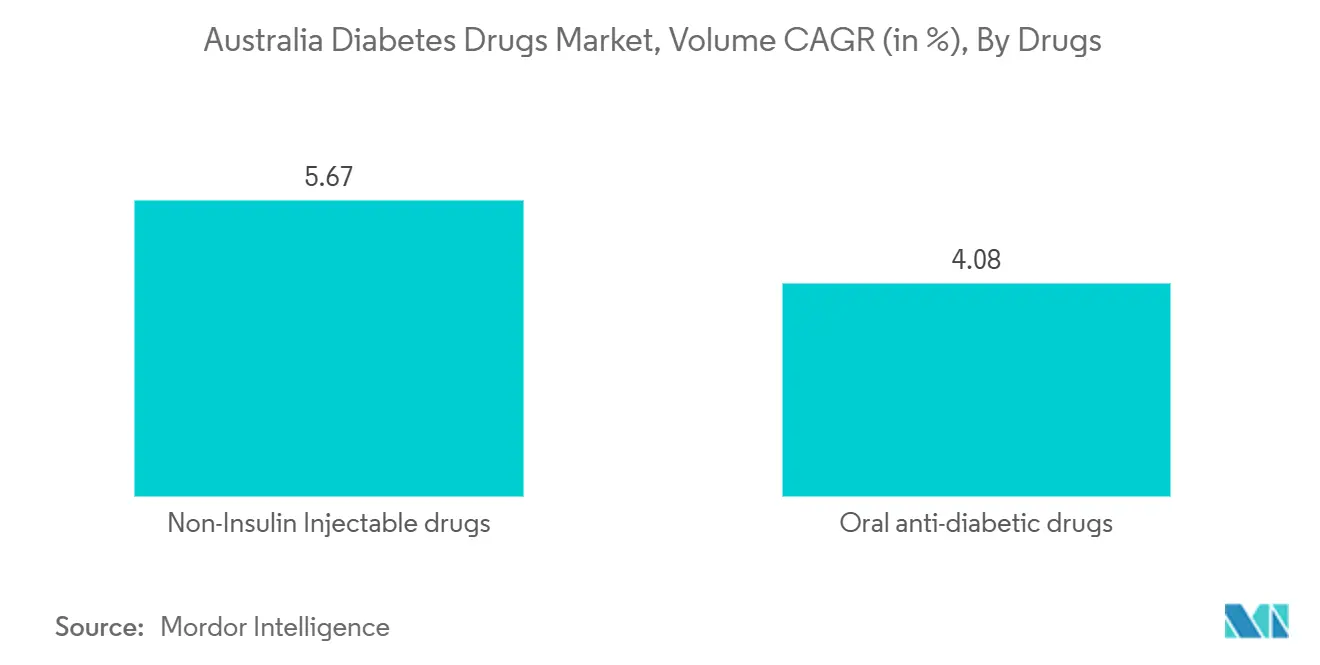

The Oral-Anti Diabetes Drugs segment is expected to increase with a CAGR of over 5% during the forecast period, mainly due to the demand from the diabetes population, which was more than 1.4 million by the end of the current year.

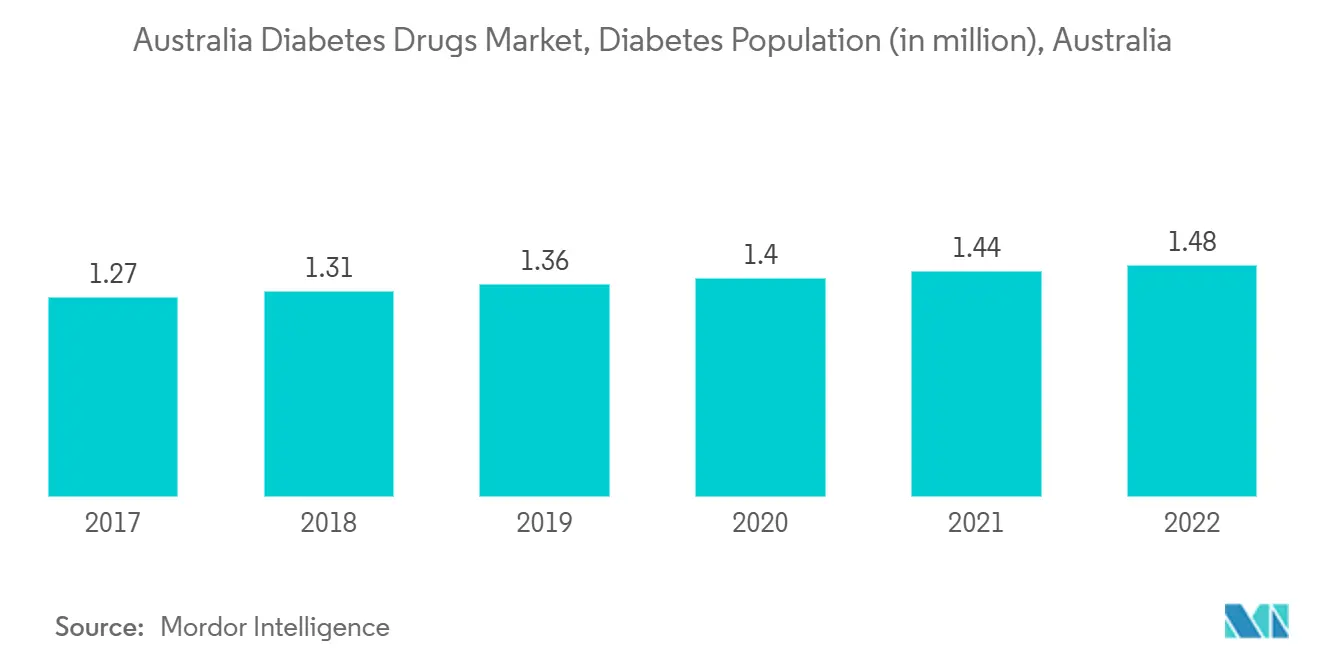

According to the Australian National Health Survey 2020-2021, one out of every 20 persons (5.3%) suffers from diabetes. Type 2 diabetes was the most frequent (85.5%), followed by Type 1 diabetes (11.0%) and diabetes not known by the individual reporting (4.1%). Diabetes patients are diagnosed with blood glucose imbalances that do not follow conventional blood glucose values. The common lab diagnostic tests can only assist physicians in diagnosing the condition. Patients whose glucose levels fluctuate more often should monitor it every day. Patients who use insulin must monitor their blood glucose levels often and alter insulin dosages or change medications as needed. People with type 2 diabetes who do not use insulin need oral drugs frequently. The Australian National Diabetes Strategy was developed in response to diabetes and outlined how existing limited healthcare resources across all levels of government might be effectively integrated and targeted. This strategy identifies the most effective and suitable strategies to decrease the community burden of diabetes and sets the standard for diabetes prevention, care, and research on a global scale.

Diabetes pills are not insulin taken orally. People with type 2 diabetes are frequently prescribed drugs, including insulin, to help them control their blood glucose levels. Most of these drugs are taken as pills; others are administered through injection. Tablets and injections are meant to supplement, not replace, a balanced diet and frequent physical exercise.

Through the Australian government's encouragement, the usage of drugs increased over the forecast period.

The rising prevalence of diabetes in Australia is boosting the country's diabetes drug market.

Diabetes prevalence occurred in Australia more than quadrupled between 1991 and 2021. In current, Australia includes around more than 2 million diabetes patients. According to Mordor Intelligence statistics, Type-2 diabetes patients accounted for most of the overall diabetic population in Australia in the current year. Nevertheless, diabetes is far more prevalent in Australia than in many other nations. One of the primary goals of diabetes therapy is to keep blood glucose levels within a certain target range. It can be accomplished by balancing food, activity, lifestyle, and diabetes medications. Blood glucose monitoring results give the information needed to establish the appropriate diabetes care approach. Maintaining target blood glucose levels can help minimize a person's chance of acquiring various diabetes-related problems such as diabetic retinopathy, heart disease, renal disease, etc. The frequency with which patients with diabetes who take insulin check their blood glucose levels varies depending on various factors.

Because of the early age and longer diabetes duration, youth are more likely to get diabetes at a younger age, lowering their quality of life, shortening their life expectancy, and increasing societal healthcare expenditures. As a result, the demand for diabetes care drugs is growing, and their acceptance rate is increasing, driving the market. In addition, with increased awareness among Type 2 diabetes patients, the need for Diabetes drugs is developing rapidly.

Thus, the above factors are expected to drive the market growth over the forecast period.

Competitive Landscape

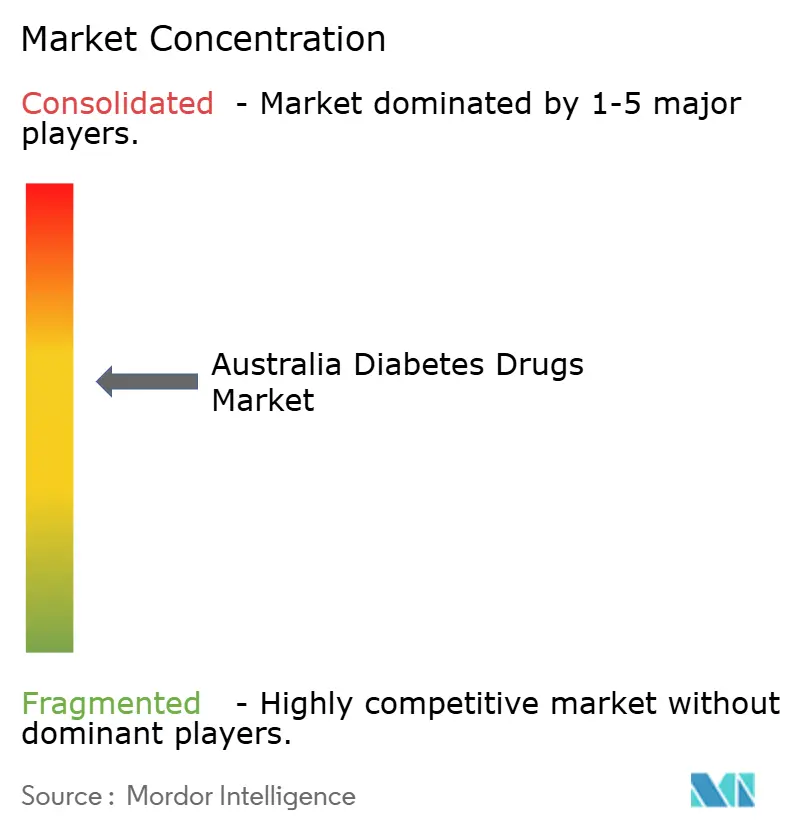

The diabetes drugs market is moderately fragmented, with few significant generic players. A few major players, like Novo-Nordisk, Sanofi, AstraZeneca, and Bristol Myers Squibb, dominate the insulin drugs and Sglt-2 drugs market. The market for oral drugs, like Sulfonylureas and Meglitinides, comprises more generic players. The intensity of competition among the players is high, as each player is striving to develop new drugs and offer them at competitive pricing. Furthermore, players are tapping into new markets to increase their market shares. It is especially applicable in emerging economies where the demand is very high compared to the supply.

Australia Diabetes Drugs Industry Leaders

-

Eli Lilly

-

Boehringer Ingelheim

-

Astrazeneca

-

Sanofi

-

NovoNordisk

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- March 2023: Albanese Government decided to extend access to Fiasp insulin and Fiasp FlexTouch via the Pharmaceutical Benefits Scheme for an additional six months. Under the arrangements, people with a current prescription for Fiasp can access it for the next six months.

- May 2022: The TGA published a joint statement with Novo Nordisk and health professional organizations that asked doctors to prescribe Ozempic for patients with type 2 diabetes as a priority. These organizations included Diabetes Australia, the Australian Medical Association, and the Pharmaceutical Society of Australia.

Australia Diabetes Drugs Market Report Scope

Diabetes or diabetes mellitus describes a group of metabolic disorders characterized by a high blood sugar level in a person. With diabetes, the body either does not produce enough insulin or the body's cells do not respond properly to insulin, or both. Australia Diabetes Drugs Market is segmented by drugs (oral anti-diabetic drugs (Biguanides, Alpha-Glucosidase inhibitors, Dopamine D2 receptor agonists, SGLT-2 inhibitors, DPP-4 inhibitors, Sulfonylureas, and Meglitinides), insulin (Basal or long-acting insulins, bolus or fast-acting insulins, traditional human insulins, biosimilar insulins), non-insulin injectable drugs (GLP-1 receptor agonists and Amylin Analogue), and combination drugs (insulin combinations and oral combinations)). The report offers the value (in USD million) and Volume (in units million) for the above segments.

Oral Anti-diabetic drugs

| Biguanides | Metformin |

| Alpha-Glucosidase Inhibitors | Alpha-Glucosidase Inhibitors |

| Dopamine D2 receptor agonist | Bromocriptin |

| SGLT-2 inhibitors | Invokana (Canagliflozin) |

| Jardiance (Empagliflozin) | |

| Farxiga/Forxiga (Dapagliflozin) | |

| Suglat (Ipragliflozin) | |

| DPP-4 inhibitors | Onglyza (Saxagliptin) |

| Tradjenta (Linagliptin) | |

| Vipidia/Nesina(Alogliptin) | |

| Galvus (Vildagliptin) | |

| Sulfonylureas | Sulfonylureas |

| Meglitinides | Meglitinides |

Insulins

| Basal or Long Acting Insulins | Lantus (Insulin Glargine) |

| Levemir (Insulin Detemir) | |

| Toujeo (Insulin Glargine) | |

| Tresiba (Insulin Degludec) | |

| Basaglar (Insulin Glargine) | |

| Bolus or Fast Acting Insulins | NovoRapid/Novolog (Insulin Aspart) |

| Humalog (Insulin Lispro) | |

| Apidra (Insulin Glulisine) | |

| Traditional Human Insulins | Novolin/Actrapid/Insulatard |

| Humulin | |

| Insuman | |

| Biosimilar Insulins | Insulin Glargine Biosimilars |

| Human Insulin Biosimilars |

Non-Insulin Injectable drugs

| GLP-1 receptor agonists | Victoza (Liraglutide) |

| Byetta (Exenatide) | |

| Bydureon (Exenatide) | |

| Trulicity (Dulaglutide) | |

| Lyxumia (Lixisenatide) | |

| Amylin Analogue | Symlin (Pramlintide) |

Combination drugs

| Insulin combinations | NovoMix (Biphasic Insulin Aspart) |

| Ryzodeg (Insulin Degludec and Insulin Aspart) | |

| Xultophy (Insulin Degludec and Liraglutide) | |

| Oral Combinations | Janumet (Sitagliptin and Metformin) |

| Oral Anti-diabetic drugs | Biguanides | Metformin |

| Alpha-Glucosidase Inhibitors | Alpha-Glucosidase Inhibitors | |

| Dopamine D2 receptor agonist | Bromocriptin | |

| SGLT-2 inhibitors | Invokana (Canagliflozin) | |

| Jardiance (Empagliflozin) | ||

| Farxiga/Forxiga (Dapagliflozin) | ||

| Suglat (Ipragliflozin) | ||

| DPP-4 inhibitors | Onglyza (Saxagliptin) | |

| Tradjenta (Linagliptin) | ||

| Vipidia/Nesina(Alogliptin) | ||

| Galvus (Vildagliptin) | ||

| Sulfonylureas | Sulfonylureas | |

| Meglitinides | Meglitinides | |

| Insulins | Basal or Long Acting Insulins | Lantus (Insulin Glargine) |

| Levemir (Insulin Detemir) | ||

| Toujeo (Insulin Glargine) | ||

| Tresiba (Insulin Degludec) | ||

| Basaglar (Insulin Glargine) | ||

| Bolus or Fast Acting Insulins | NovoRapid/Novolog (Insulin Aspart) | |

| Humalog (Insulin Lispro) | ||

| Apidra (Insulin Glulisine) | ||

| Traditional Human Insulins | Novolin/Actrapid/Insulatard | |

| Humulin | ||

| Insuman | ||

| Biosimilar Insulins | Insulin Glargine Biosimilars | |

| Human Insulin Biosimilars | ||

| Non-Insulin Injectable drugs | GLP-1 receptor agonists | Victoza (Liraglutide) |

| Byetta (Exenatide) | ||

| Bydureon (Exenatide) | ||

| Trulicity (Dulaglutide) | ||

| Lyxumia (Lixisenatide) | ||

| Amylin Analogue | Symlin (Pramlintide) | |

| Combination drugs | Insulin combinations | NovoMix (Biphasic Insulin Aspart) |

| Ryzodeg (Insulin Degludec and Insulin Aspart) | ||

| Xultophy (Insulin Degludec and Liraglutide) | ||

| Oral Combinations | Janumet (Sitagliptin and Metformin) | |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How big is the Australia Diabetes Care Drugs Market?

The Australia Diabetes Drugs Market size is expected to reach USD 0.84 billion in 2025 and grow at a CAGR of 3.60% to reach USD 1.01 billion by 2030.

What is the current Australia Diabetes Drugs Market size?

In 2025, the Australia Diabetes Drugs Market size is expected to reach USD 0.84 billion.

Who are the key players in Australia Diabetes Drugs Market?

Eli Lilly, Boehringer Ingelheim, Astrazeneca, Sanofi and NovoNordisk are the major companies operating in the Australia Diabetes Drugs Market.

What years does this Australia Diabetes Drugs Market cover, and what was the market size in 2024?

In 2024, the Australia Diabetes Drugs Market size was estimated at USD 0.81 billion. The report covers the Australia Diabetes Drugs Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Australia Diabetes Drugs Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: