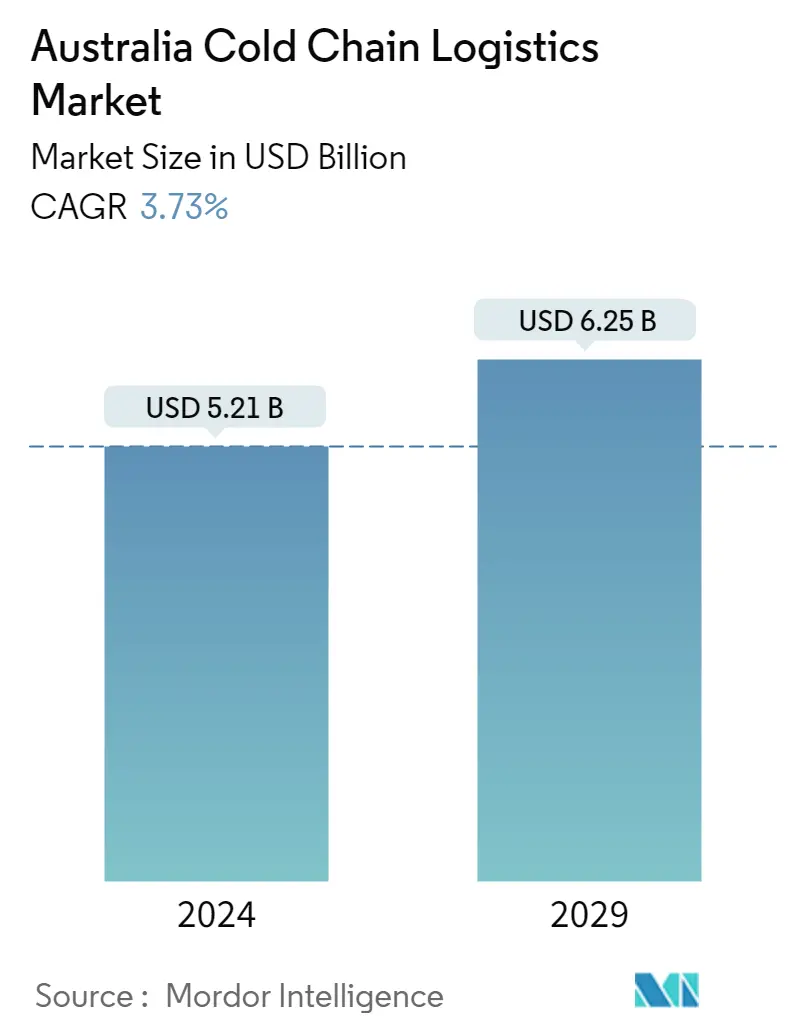

Cold Chain Logistics Australia Market Size

| Study Period | 2020 - 2029 |

| Base Year For Estimation | 2023 |

| Market Size (2024) | USD 5.21 Billion |

| Market Size (2029) | USD 6.25 Billion |

| CAGR (2024 - 2029) | 3.73 % |

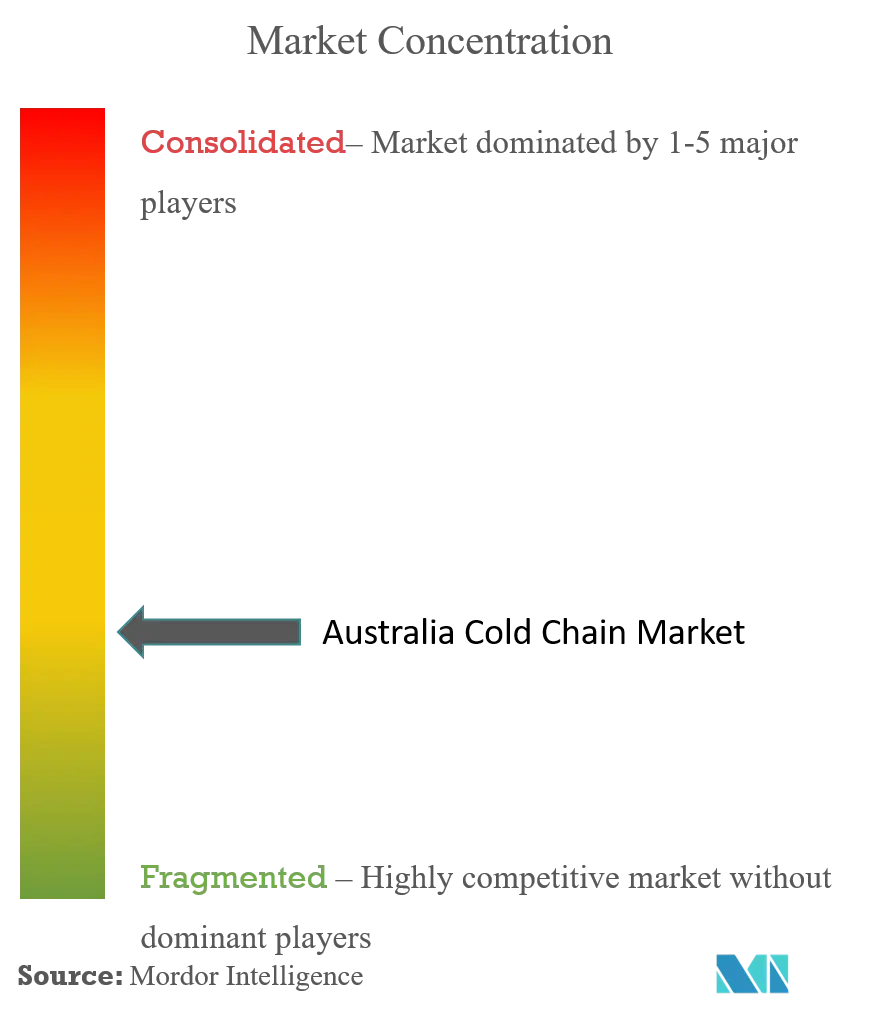

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Cold Chain Logistics Australia Market Analysis

The Australia Cold Chain Logistics Market size is estimated at USD 5.21 billion in 2024, and is expected to reach USD 6.25 billion by 2029, growing at a CAGR of 3.73% during the forecast period (2024-2029).

- The Australian cold chain logistics market was severely impacted by the pandemic. Not only did the abrupt closure of Australia's borders and subsequent closure of passenger routes result in a halt in human movement, but it also impacted transport cargo capacity in and out of Australia. The previous routes were no longer as easily accessible for businesses looking to move goods in and out of the country, and prices for the limited opportunities available were at a premium. Australia is a major player in the production and export of perishable goods, with the largest share of the country's cold chain logistics market.

- According to the data from the Australian Bureau of Statistics, more than a third of all businesses (37%) experienced supply chain disruptions in February 2022. This latest data shows that supply chain issues had decreased since January, when nearly half of all businesses (47%) reported having them, but have remained elevated since the survey was last collected in April 2021. According to the report, the most common supply chain issue facing businesses is domestic and international delivery delays (88%), followed by supply constraints (80%) and price increases (75%).

- Every year, 7.6 million tonnes of food are wasted in Australia, costing USD 37 billion, with flaws in the cold chain playing a significant role. Food demand will increase by 50% over the next ten years, while energy demand will increase by 50%, and water demand will increase by 30%. The National Construction Code (NCC) specifies insulation for everything, and there is no standard or regulation for insulation in the cold chain followed. One area where Australia falls far short is in necessities such as standardized truck widths and pallet sizes. The rest of the world uses 2.6-meter pallets, while Australians use 2.5-meter pallets, which causes overloading, reduced airflow, and other issues.

- Despite the rising challenges in the market, cold chain logistics is experiencing growth in Australia due to the surge in demand for food products, meat, pharmaceuticals, and other goods which require temperature requirement and end-to-end delivery. Furthermore, there is growth in the market because of the supply of vaccines which require temperature controlled environment until it is administered to the citizens.

- One more trend in the market is the growth of e-commerce in the sector; this has created opportunities for wholesalers and retailers to deliver their products directly to customers. Many products which are sold through e-commerce distribution channels require cold chain logistics, and the ease of product availability has propelled the logistics partners to provide facilities for the smooth movement of these products to the consumers without any damage. These trends, along with some others, are expected to drive the market in the forecast period despite the challenges rising in the industry.

Cold Chain Logistics Australia Market Trends

This section covers the major market trends shaping the Australia Cold Chain Logistics Market according to our research experts:

Huge Demand for Meat Propelling Demand for Cold Chain Logistics in Australia

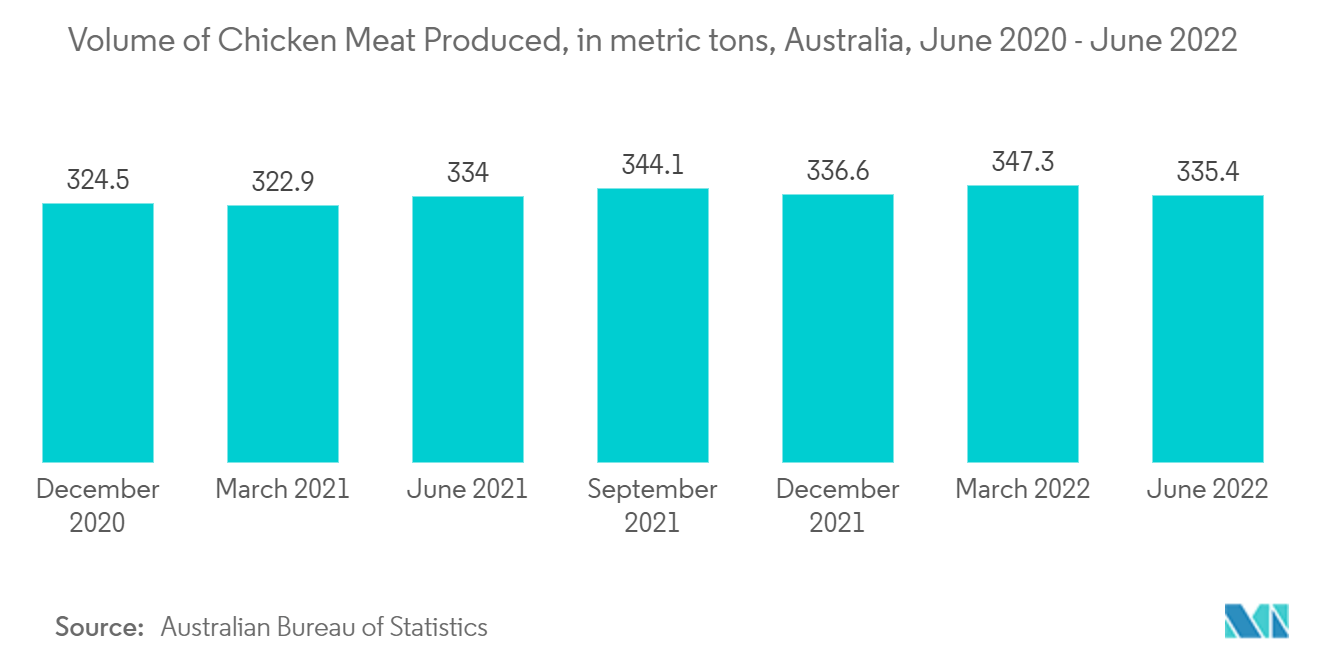

Meat and Livestock Australia (MLA) reduced its 2022 cattle slaughter predictions from 6.70 million to 6.15 million head for the year. This follows a lower-than-expected kill in the first quarter of 2022, which was 6.3% lower than in the same period in the previous year. The key drivers of reduced slaughter capacity are ongoing issues with the pandemic, labor availability, and forced shutdowns due to public holidays and weather. On top of that, producers are withholding more stock from slaughter to rebuild herd sizes. Despite lower slaughter numbers, production in the first quarter of 2022 fell by only 2.5% year on year. Because of record numbers of cattle in feedlot systems and higher prices incentivizing higher weights, average carcass weights were 10.8kg heavier in Q1 2022 compared to 2021. Total beef production for the year is expected to reach 1.97 million tonnes, a 4.5% increase over 2021. Australia exported 437,000 tonnes of fresh and frozen beef in the first six months of 2022, a 5.0% decrease from the same period last year. The first quarter of the year was the most affected, with February and March falling 12.8% and 15.0% behind 2021 volumes, respectively. Volumes increased in June, with exports increasing 16.3% year on year.

Lower supply and logistical challenges have been the primary constraints on export volumes. Long-haul routes became less appealing as freight costs rose, and disruptions to shipping channels caused by lockdowns at Chinese ports and the war in Ukraine left goods stranded or necessitated lengthy detours. Despite lower prices, Australian beef remains more expensive than that of other major producers, including the United Kingdom. Although the UK-Australia free trade agreement is set to take effect before the end of the year, a flood of Australian beef is unlikely due to higher prices, limited supply in Australia, and global shipping issues. Shipping issues are heavily influencing which markets traders prioritize, with nations closer to the home being preferred over those further away. This is likely to keep Southeast Asia as Australia's most important market. According to the Australian Food Cold Chain Council, logistical companies and supermarkets were doing their best within the current cold chain, but the lack of another layer of verification at critical control points had a negative impact. As technology advances, the role of the cold food supply chain becomes more prominent as chilled and frozen products that were previously limited in their marketability can now be transported over longer distances. The absence of a national regulatory system to ensure a uniform approach to the transport of chilled and frozen goods was the most serious issue confronting the Australian cold chain.

Growth of E-commerce to Propel the Forward

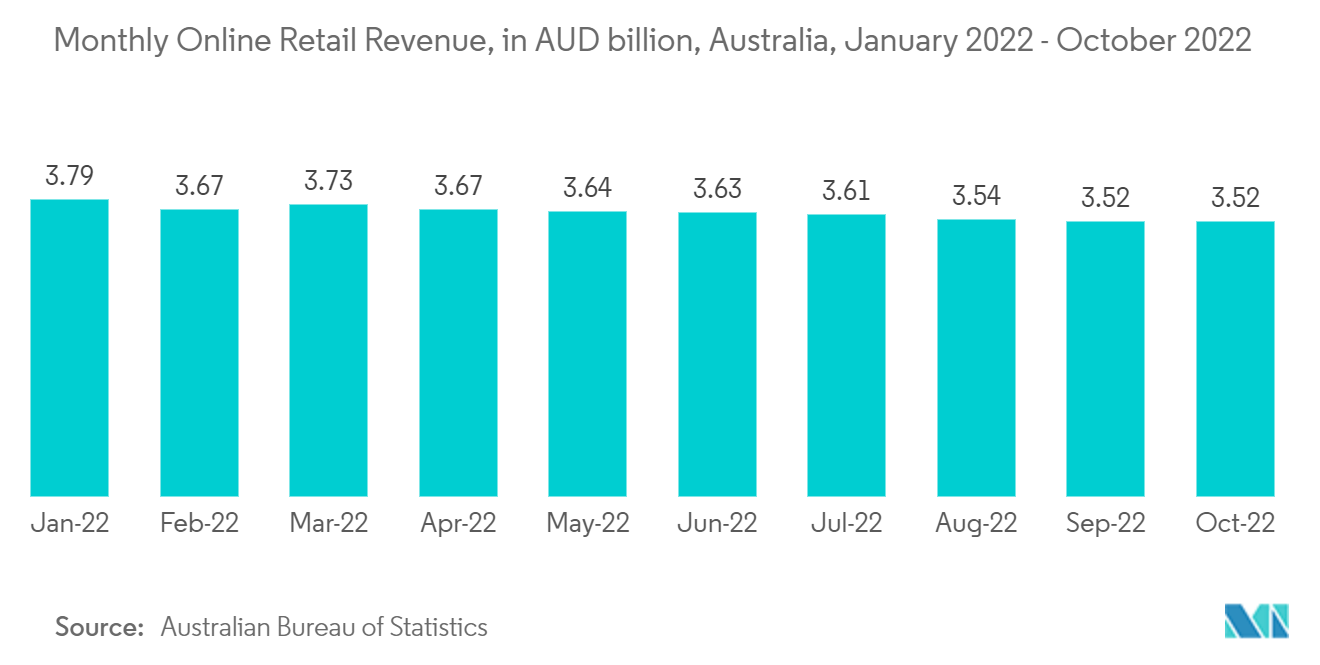

In Australia's business landscape, e-commerce is evolving and becoming even more important. Knowing the latest industry figures is critical to staying on par with your competition, especially with the advent of convenient and contactless shopping. E-commerce spending reached an all-time high in 2022, with fashion products taking the top spot with USD 9.7 billion in sales. Australia recorded a total retail turnover through e-commerce of more than USD 4 million in September 2021, a USD 1 million increase from September 2020, which was just shy of USD 3 million.

According to Australia Post, in 2021, 2.9 million households purchased from Specialty Food & Liquor retailers. The Specialty Food & Liquor segment experienced its highest peak in 2021 during Black Friday, but it also increased during non-essential retail restrictions. Specialty Food items were in high demand in July and August 2021, while Wine & Liquor began to rise in October and November, peaking during the Cyber Sales as people stocked up for the holiday season. While physical stores began to reopen, shoppers continued to buy online. Given the evolution of lifestyles, some retailers discovered that their customers still prefer to have their goods delivered. This implies that digital demand will remain strong, and businesses should keep this in mind.

Growth in e-commerce will propel the market as it will create a huge demand for perishable goods, food products, and pharmaceuticals, which will require the support of cold chain logistics to cater to the consumers. There are loopholes in the system, but it also has immense opportunities for the players in the e-commerce market.

Cold Chain Logistics Australia Industry Overview

The Australian cold chain logistics market is fragmented in nature, which consists of a large number of local players to cater to the growing demand. Some of the major players in the market include Americold, Newcold Advanced Cold Logistics, Karras Cold Logistics, Auscold Logistics PTY Ltd. and many more. Other major players are MFR Cool Logistics, AGRO Merchants Group LLC, PakCan, ChillFreeze Logistics & Storage, Chill WA and others. International players are trying to enter the market in various ways, but the stronghold of local companies and the challenges in the market has become issues for the international players. But, the opportunities are expected to make way for them.

Cold Chain Logistics Australia Market Leaders

-

Americold Logistics

-

Karras Cold Logistics

-

Global Cold Chain Solutions (GCCS)

-

Auscold Logistics PTY Ltd.

-

ChillFreeze Logistics & Storage

*Disclaimer: Major Players sorted in no particular order

Cold Chain Logistics Australia Market News

- July 2022: NewCold, a pioneering Netherlands-based cold chain logistics company, announced a new customer and an additional USD 160 million investment in its Victorian state-of-the-art facility, bringing its total investment in Victoria to USD 460 million. NewCold's Melbourne 2 facility will more than double in size, providing customers with a powerhouse of advanced features and a seamless experience. The site will grow from 115,000 to 225,000 pallet positions at 43 meters in height, an increase of 110,000 pallets.

- March 2022: Global Cold Chain Solutions introduced new Rotational Moulded Shippers. The vacuum-insulated panel (VIP) insulation is extremely effective, resulting in a shipper that can maintain temperatures for up to eight days. RotoMoulded Shippers are currently available in two sizes: 24L and 48L, with internal payload capacities of 8L and 15L, respectively. The shippers can maintain temperatures ranging from 2°C to 8°C for up to 201 hours, which is more than double the time of competitor models.

Cold Chain Logistics Australia Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

2.1 Analysis Method

2.2 Research Phases

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS AND DYNAMICS

4.1 Current Market Scenario

4.2 Market Overview

4.3 Market Dynamics

4.3.1 Drivers

4.3.2 Restraints

4.3.3 Opportunities

4.4 Value Chain / Supply Chain Analysis

4.5 Industry Attaractiveness - Porter's Five Forces Analysis

4.5.1 Threat of New Entrants

4.5.2 Bargaining Power of Buyers/Consumers

4.5.3 Bargaining Power of Suppliers

4.5.4 Threat of Substitute Products

4.5.5 Intensity of Competitive Rivalry

4.6 Technological Trends and Automation

4.7 Government Regulations and Initiatives

4.8 Industry Value Chain/Supply Chain Analysis

4.9 Spotlight on Ambient/Temperature-controlled Storage

4.10 Impact of Emission Standards and Regulations on Cold Chain Industry

4.11 Impact of COVID-19 on the Market

5. MARKET SEGMENTATION

5.1 By Services

5.1.1 Storage

5.1.2 Transportation

5.1.3 Value-added Services (Blast Freezing, Labeling, Inventory Management, etc.)

5.2 By Temperature Type

5.2.1 Chilled

5.2.2 Frozen

5.3 By Application

5.3.1 Fruits & Vegetables

5.3.2 Dairy Products

5.3.3 Meat and Seafood

5.3.4 Processed Food

5.3.5 Pharmaceuticals (Include Biopharma)

5.3.6 Bakery and Confectionery

5.3.7 Other Applications

6. COMPETITIVE LANDSCAPE

6.1 Market Concentration Overview

6.2 Company Profiles

6.2.1 Americold Logistics

6.2.2 Karras Cold Logistics

6.2.3 NewCold Advanced Cold Logistics

6.2.4 Global Cold Chain Solutions

6.2.5 Lineage Logistics (includes Emergent Cold Chain and Swire Cold Storage)

6.2.6 MFR Cool Logistics

6.2.7 AGRO Merchants Group, LLC

6.2.8 PakCan

6.2.9 Kerry Logistics

6.2.10 Auscold Logistics PTY Ltd.

6.2.11 AustraCold*

- *List Not Exhaustive

7. FUTURE OF AUSTRALIA COLD CHAIN LOGISTICS MARKET

8. APPENDIX

Cold Chain Logistics Australia Industry Segmentation

A cold chain is a temperature-controlled supply chain. Cold chain logistics is the technology and process that allows the safe transport of temperature-sensitive goods and products along the supply chain. A complete background analysis of the Australia Cold Chain Logistics Market, including the assessment of the economy and contribution of sectors in the economy, market overview, market size estimation for key segments, and emerging trends in the market segments, market dynamics, and geographical trends, and COVID-19 impact is included in the report.

The Australia cold chain logistics market is segmented by service (storage, transportation, and value-added services), temperature type (chilled and frozen), and application (fruits and vegetables, dairy products, meat and seafood, processed food, pharmaceuticals (include biopharma), bakery and confectionery, and other applications). The report offers market sizes and forecasts in values (USD billion) for all the above segments.

| By Services | |

| Storage | |

| Transportation | |

| Value-added Services (Blast Freezing, Labeling, Inventory Management, etc.) |

| By Temperature Type | |

| Chilled | |

| Frozen |

| By Application | |

| Fruits & Vegetables | |

| Dairy Products | |

| Meat and Seafood | |

| Processed Food | |

| Pharmaceuticals (Include Biopharma) | |

| Bakery and Confectionery | |

| Other Applications |

Cold Chain Logistics Australia Market Research FAQs

How big is the Australia Cold Chain Logistics Market?

The Australia Cold Chain Logistics Market size is expected to reach USD 5.21 billion in 2024 and grow at a CAGR of 3.73% to reach USD 6.25 billion by 2029.

What is the current Australia Cold Chain Logistics Market size?

In 2024, the Australia Cold Chain Logistics Market size is expected to reach USD 5.21 billion.

Who are the key players in Australia Cold Chain Logistics Market?

Americold Logistics, Karras Cold Logistics, Global Cold Chain Solutions (GCCS), Auscold Logistics PTY Ltd. and ChillFreeze Logistics & Storage are the major companies operating in the Australia Cold Chain Logistics Market.

What years does this Australia Cold Chain Logistics Market cover, and what was the market size in 2023?

In 2023, the Australia Cold Chain Logistics Market size was estimated at USD 5.02 billion. The report covers the Australia Cold Chain Logistics Market historical market size for years: 2020, 2021, 2022 and 2023. The report also forecasts the Australia Cold Chain Logistics Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

Cold Chain Logistics in Australia Industry Report

Statistics for the 2024 Cold Chain Logistics in Australia market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. Cold Chain Logistics in Australia analysis includes a market forecast outlook to 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.

Cold Chain Logistics Market in Australia Report Snapshots