| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 6.21 Billion |

| Market Size (2030) | USD 7.23 Billion |

| CAGR (2025 - 2030) | 3.10 % |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Australia Agricultural Machinery Market Analysis

The Australia Agricultural Machinery Market size is estimated at USD 6.21 billion in 2025, and is expected to reach USD 7.23 billion by 2030, at a CAGR of 3.1% during the forecast period (2025-2030).

Australia's agricultural machinery sector plays a vital role in the nation's economy, contributing significantly to the agricultural output that accounts for approximately 4% of the country's GDP. The sector operates within a unique context of vast regional differences and climate variability, which necessitates specialized farm equipment adaptations. Large-scale farming operations, enabled by extensive land availability, have positioned Australia as a major agricultural producer and exporter. The country's farming landscape is characterized by increasing farm sizes, with the Australian Bureau of Agricultural and Resource Economics reporting that the average area operated by large cropping farms reached approximately 4.72 thousand hectares in 2022, showcasing the scale of operations requiring mechanized solutions.

The market has witnessed substantial productivity gains through advanced farm machinery adoption, particularly evident in the grain sector. According to FAOSTAT, barley production in Australia increased significantly from 10.1 million metric tons in 2021 to 14.6 million metric tons in 2022, demonstrating the impact of efficient machinery utilization. This productivity enhancement has been supported by the growing integration of precision agriculture technologies, including GPS-guided agricultural equipment and automated systems. The sector has also seen a shift toward larger, more sophisticated machinery capable of handling extensive farming operations while maintaining operational efficiency.

The industry landscape is experiencing a notable transformation with manufacturers focusing on developing specialized agricultural implements suited to Australian conditions. The Tractor and Machinery Association of Australia (TMA) reported a 10% increase in sales for the under-40 horsepower tractor segment in 2022, indicating strong demand for compact and specialized machinery. This trend reflects the diversification of farming operations and the growing need for versatile farm equipment that can handle various agricultural tasks efficiently. Manufacturers are responding with innovations in machinery design and functionality, particularly in areas such as precision seeding, efficient harvesting, and sustainable farming practices.

The market is witnessing significant technological integration across various equipment categories, with a particular emphasis on smart farming solutions. Recent product launches in 2023 demonstrate this trend, including CNH Industrial's introduction of the Farmall Subcompact 25SC with advanced features for the lifestyle farming segment, and Case IH's launch of the Steiger 645 Quadtrac, representing the highest horsepower tractor in their range for the Australian market. These developments indicate a clear industry direction toward more sophisticated, technologically advanced machinery that can improve operational efficiency while addressing the specific needs of Australian farmers. The sector continues to evolve with an increasing focus on precision agriculture, autonomous capabilities, and integrated digital solutions that enhance farming productivity.

Australia Agricultural Machinery Market Trends

Declining Labor Availability and Rising Cost of Farm Labor

Labor is a critical input to Australian agriculture, and there is significant interest in understanding the extent to which labor markets are currently meeting the needs of the Australian farm sector. According to ABRES (Department of Agriculture, Water, and Environment), Australian farms employed 239,000 workers on average across 2021, including full-time, part-time, casual, and contract employees. Employment in the agriculture sector has shown a consistent decline, decreasing from 2.7% in 2020 to 2.4% in 2021 of total employment, indicating the growing labor shortage in the sector.

The limited availability of farm laborers has resulted in an increase in wages for farm workers, as Australia now has the fourth-highest wage rate globally according to the Australian Farm Institute. This increase in labor costs is compelling farmers to seek alternatives through mechanization. Poor rural reforms have been leading to decreasing rural labor, thereby pushing farmers to further mechanize their various farm operations. The continually rising real wage of farm labor has had a positive impact on the demand for agricultural automation and precision agriculture equipment in the region, as farmers have been increasingly adopting mechanization as a substitute for manual labor, which is further anticipated to drive the studied market in the upcoming future.

Rising Preference for Agricultural Machinery

Australian agriculture faces prominent challenges of climate inconsistency and increased local competition in key export markets. As a result, Australian agriculture has been adopting innovative techniques, such as increased use of data science, automation, and communication technologies, along with modern agricultural machinery, including tractors, harvesters, and irrigation machinery. According to the Tractor and Machinery Association of Australia (TMA), the equipment most in demand includes self-propelled boom sprayers, high-density balers, tracked tractor technology, and automated feeding systems, highlighting the growing preference for smart farming equipment among Australian farmers.

Almost 95% of all agricultural machinery and equipment used in Australia is imported, with most farm tractors and harvesting equipment coming from Europe and the United States. The red-hot demand is being driven by improved seasonal conditions in many areas, making Australia an ideal target market for machinery manufacturers. Australian farmers and distributors actively look to overseas suppliers for new and efficient products and solutions that can improve productivity and farming efficiency. For instance, Wisconsin-based manufacturer Miller successfully introduced their new self-propelled sprayer to the Australian market, demonstrating the country's openness to adopting new agricultural robotics technologies.

Rapid Technological Advancements by Key Players

The rapid technological innovations in agricultural machinery are currently revolutionizing Australian farming. Major agricultural machinery manufacturers are continuously launching products with advanced features to meet the evolving needs of Australian farmers. For instance, in 2023, John Deere launched John Deere 1 Series Round Balers in the Australian market with Bale Doc technology to document bale moisture and weight in near real-time. Similarly, CNH Industrial brand Case IH introduced the very popular AFS Connect Steiger tractor with the latest updates and launched the new Farmall Subcompact 25SC, designed specifically for the growing lifestyle segment of the agricultural machinery market.

The agricultural machines, especially the recent models, are equipped with sophisticated computerized systems and advanced technologies. Companies are incorporating features like GPS software, tractors equipped with telematics, and precision farming capabilities to improve operational efficiency. For example, the CNH brand Case IH launched the Steiger 645 Quadtrac in 2023, which is one of the most powerful tractors available in the local market, featuring an impressive 645hp under the bonnet and the latest upgrades for the MY24 Steiger range. These technological advancements by key players are not only improving the efficiency of farming operations but also contributing to sustainable agriculture practices through features like reduced fuel consumption and precise application of inputs. The integration of autonomous farm equipment and agricultural drones is further enhancing the capabilities of precision agriculture equipment, supporting the transition to more efficient and sustainable farming practices.

Segment Analysis: Tractors

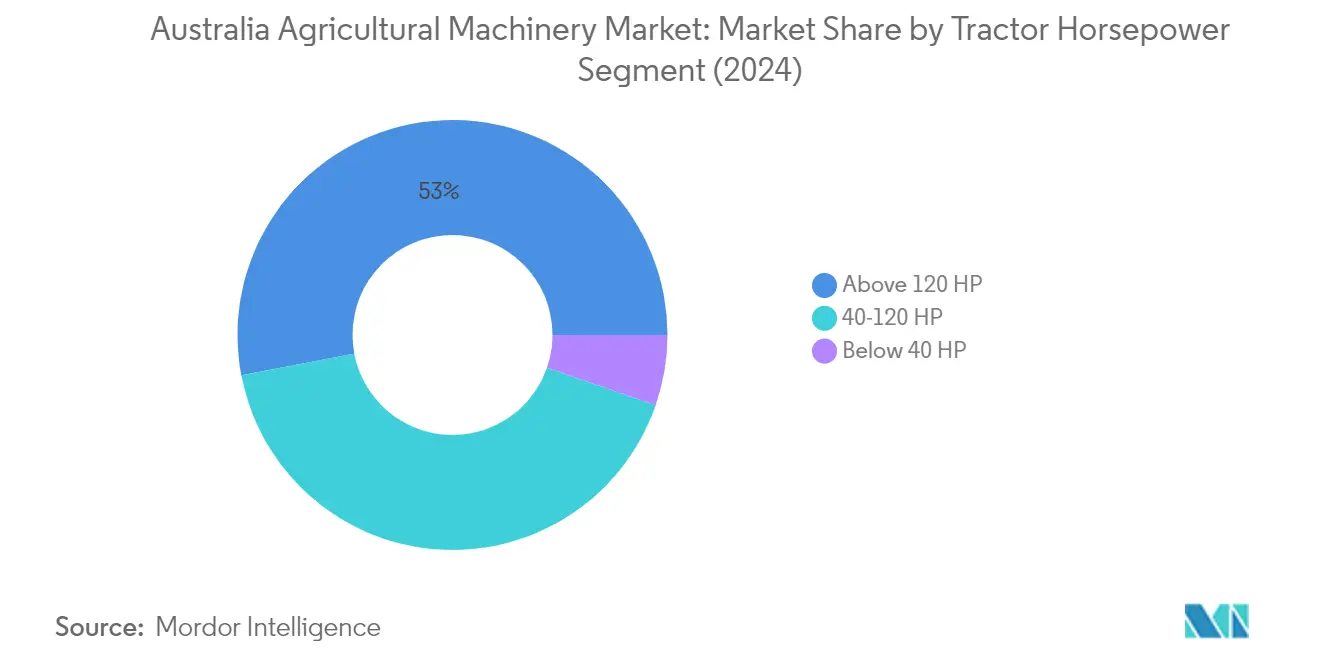

Above 120 HP Segment in Australia Agricultural Machinery Market

The Above 120 HP tractors segment dominates the Australian agricultural machinery market, commanding approximately 53% market share in 2024. This segment's prominence is driven by the extensive harvesting applications and challenging soil conditions across Australia's vast agricultural landscapes. These high-powered tractors are particularly well-suited for carrying out heavy-duty loads with front-end loaders, tillage operations, and larger farm duties, supported by sophisticated fuel-efficient transmissions and well-powered rear connections. The strong agricultural production in Australia, particularly in broadacre farming, continues to drive the demand for these powerful machines. Major manufacturers have responded to this demand by introducing advanced features and technologies in their high-horsepower tractors, ensuring better productivity and operational efficiency for Australian farmers.

40-120 HP Segment in Australia Agricultural Machinery Market

The 40-120 HP tractors segment is experiencing the fastest growth in the Australian agricultural machinery market, with an expected growth rate of approximately 9% during 2024-2029. This robust growth is attributed to the segment's versatility and optimal power range that suits a wide variety of farming operations. These tractors have established themselves as the most popular implements, supported by a well-developed ecosystem of manufacturing and sales through various regional and local manufacturers. The increasing adoption of modern agricultural techniques and the federal government's instant tax write-off incentives have significantly boosted the demand for this segment. Manufacturers are actively expanding their product portfolios in this category, introducing new models with advanced features and improved efficiency to cater to the evolving needs of Australian farmers.

Remaining Segments in Tractors Market

The Below 40 HP tractors segment, while smaller in market share, plays a crucial role in serving specific agricultural needs in Australia. These compact tractors are particularly valuable for small-scale farming operations, gardens, and yards, offering powerful engines for enhanced small-scale field cultivation. Their compact size and versatility make them ideal for tasks such as mowing, plowing, and pulling small trailers. The segment benefits from features like lower fuel consumption and safer operation, making them particularly attractive for smaller agricultural operations and hobby farms. Manufacturers continue to innovate in this segment, introducing new models with improved technology and efficiency to meet the specific requirements of small-scale Australian farmers.

Segment Analysis: Ploughing and Cultivating Machinery

Cultivators and Tillers Segment in Australia Agricultural Machinery Market

Cultivators and tillers represent the largest segment in the Australian agricultural ploughing and cultivating machinery market, holding approximately 34% market share in 2024. The segment's dominance is primarily driven by its versatile applications in preparing proper seedbeds for crop planting, burying crop residue in the soil, controlling weeds, and mixing soil to ensure growing crops have adequate water and nutrients. The used tiller machinery also maintains significant demand due to its lower price point, particularly appealing to small-scale farmers looking to achieve low agricultural expenses during cultivation. Support from the Regional Investment Corporation (RIC) through concessional loans and Rural Research and Development Corporations (RDC) investments has further strengthened the segment's market position in Australia.

Harrows Segment in Australia Agricultural Machinery Market

The harrows segment is projected to experience the fastest growth in the Australian agricultural ploughing and cultivating machinery market from 2024 to 2029, with an expected growth rate of approximately 7%. This robust growth is attributed to farmers' increasing focus on using modern and appropriate agri-equipment to avoid losses in terms of time, money, and crop yield. Disc harrows are particularly preferred as they demonstrate superior capability in breaking large clumps of dirt compared to other harrow types. The large-scale production of broad-acre crops such as sugarcane, grains, and pulses has also enhanced the use of disc harrows in the country. Additionally, farmers are selecting harrows based on sophisticated criteria such as the intensity of implement entering crop residue rather than simply leveling soil structure, driving innovation and adoption in this segment.

Remaining Segments in Ploughing and Cultivating Machinery

The ploughs segment maintains significant importance in the Australian agricultural machinery market, particularly for its effectiveness in weed control practices targeting weed seed banks in conservation wheat production systems. Various types including chisel ploughs, disc ploughs, and moldboard ploughs serve different purposes across Australian farming operations. The other ploughing and cultivating machinery segment, which includes specialized equipment like gyrovators, ridgers, rotary tillers, and cultipackers, plays a complementary role in the market by addressing specific farming needs and supporting various cultivation practices across different agricultural applications.

Segment Analysis: Planting Machinery

Seed Drills Segment in Australia Agricultural Machinery Market

Seed drills continue to dominate the planting equipment segment in Australia, commanding approximately 42% of the market share in 2024. The segment's leadership position is primarily driven by its widespread adoption among Australian farmers, particularly in cereal crop cultivation. The seed drill machinery that plants seeds and adds fertilizers simultaneously has gained significant traction in the market due to its dual functionality. These machines have demonstrated exceptional performance in Australian farming conditions, especially in regions with low moisture content, making the planting process more efficient and less time-consuming. The popularity of seed drills is further enhanced by manufacturing companies launching products with different widths to cater to various farm sizes and tractor compatibility requirements. The segment's strong market position is also supported by the increasing area under cereal crops in Australia, which has created sustained demand for efficient seeding equipment.

Spreaders Segment in Australia Agricultural Machinery Market

The spreaders segment is projected to exhibit the strongest growth trajectory during the forecast period 2024-2029, with an expected CAGR of approximately 10%. This remarkable growth is primarily attributed to the increasing awareness among Australian farmers about the importance of precise fertilizer application and the need to reduce fertilizer wastage. The segment's expansion is further supported by the rising adoption of advanced spreading technologies that enable even distribution of fertilizers and seeds, resulting in improved crop yields. Manufacturers are actively introducing innovative spreader technologies with features like precision control systems and variable rate application capabilities. The growth is also driven by the increasing focus on sustainable farming practices and the need for efficient nutrient management systems in Australian agriculture. The segment is witnessing significant technological advancements, including the integration of GPS and automated control systems, making spreaders more precise and user-friendly.

Remaining Segments in Planting Machinery

The planting equipment market in Australia also encompasses planters and other planting machinery segments, each serving specific agricultural requirements. Planters have established a strong presence in the market, particularly in row crop farming and precision planting applications. These machines are especially valuable for crops requiring precise seed placement and spacing, such as cotton and various pulses. The other planting machinery segment includes specialized equipment like precision seeders and transplanters, which cater to specific farming operations and crop types. These segments complement the overall planting equipment market by providing farmers with specialized solutions for different cropping systems and field conditions. The continuous innovation in these segments, particularly in precision farming technology and automation capabilities, ensures their relevance in the evolving Australian agricultural landscape.

Segment Analysis: Harvesting Machinery

Combine Harvesters Segment in Australia Agricultural Machinery Market

Combine harvesters represent the dominant segment in Australia's harvesting machinery market, commanding approximately 77% of the total harvesting machinery market value in 2024. This significant market presence is driven by the increasing farm sizes in Australia, as larger farms tend to be more profitable and generate higher returns through the use of combines. The segment's strong performance is particularly notable in Western Australia, where sales have shown remarkable growth due to favorable harvesting conditions and rising commodity prices. The segment is also experiencing the highest growth rate in the harvesting machinery market, projected to grow at approximately 9% during 2024-2029. This growth is primarily attributed to farmers' increasing preference for high-horsepower combine harvesters, with machines in the 435-516 HP, 516-598 HP, and 598 HP Plus categories accounting for about 81% of combine harvester sales. The average engine horsepower of combine harvesters in Australia has increased to 484 HP, reflecting the market's shift towards more powerful and efficient harvesting solutions.

Remaining Segments in Harvesting Machinery

The harvesting machinery market in Australia also encompasses forage harvesters and other specialized harvesting equipment, each serving distinct agricultural needs. Forage harvesters play a crucial role in livestock operations and hay production, offering farmers efficient solutions for harvesting and processing forage crops. These machines are particularly valuable in regions with significant dairy and livestock farming activities. The other harvesting machinery segment includes specialized equipment such as sugarcane harvesters and cotton harvesters, which are essential for Australia's diverse agricultural landscape. Sugarcane harvesters are particularly important in Queensland, where approximately 95% of Australia's sugar is produced, while cotton harvesters serve the growing cotton industry, which represents 30% to 60% of total agricultural production in regions where it's grown. These segments continue to evolve with technological advancements, offering improved harvesting efficiency and reduced operational costs for farmers.

Segment Analysis: Haying and Forage Machinery

Balers Segment in Australia Agricultural Machinery Market

Balers represent the dominant segment in Australia's haying and forage machinery market, commanding approximately 57% of the market share in 2024. The segment's leadership position is attributed to the increasing demand for efficient hay and forage handling solutions among Australian farmers. The growing hay-making industry in Australia, coupled with the rising hay exports, has significantly boosted the adoption of balers. Modern balers are equipped with advanced features like automatic density control, moisture sensors, and precision cutting mechanisms, making them indispensable for large-scale farming operations. The segment is also experiencing the fastest growth trajectory, with manufacturers focusing on developing innovative baler technologies that offer improved bale density, enhanced operational efficiency, and reduced maintenance requirements. The introduction of smart balers with IoT capabilities and remote monitoring features has particularly resonated with tech-savvy Australian farmers looking to optimize their harvesting operations.

Mowers and Conditioners Segment in Australia Agricultural Machinery Market

The mowers and conditioners segment has emerged as a vital component of Australia's haying and forage machinery market, demonstrating steady growth potential. This segment's expansion is driven by the increasing adoption of advanced mowing technologies that enable faster cutting speeds while maintaining optimal crop quality. Manufacturers are focusing on developing innovative features such as improved cutting mechanisms, better ground contour following capabilities, and enhanced conditioning systems that help reduce drying time and improve forage quality. The integration of precision farming technologies in modern mowers and conditioners, including GPS guidance systems and automated height control, has significantly improved operational efficiency. The segment is particularly benefiting from the growing emphasis on pasture management practices among Australian livestock farmers who require efficient mowing solutions for maintaining their grazing lands.

Remaining Segments in Haying and Forage Machinery

The other haying and forage machinery segment encompasses essential equipment such as tedders, windrowers, and specialized forage handling equipment. These machines play a crucial role in the complete hay and forage harvesting process, complementing the functions of balers and mowers. Tedders are particularly important for aerating and drying hay efficiently, while windrowers help in forming uniform windrows for better baling efficiency. The segment has seen technological advancements in terms of improved operational efficiency and integration with other farming equipment. Manufacturers are focusing on developing versatile machines that can handle various crop types and operating conditions, making them valuable additions to modern farming operations in Australia.

Segment Analysis: Irrigation Machinery

Drip Irrigation Segment in Australia Agricultural Machinery Market

Drip irrigation dominates the irrigation equipment market in Australia, commanding approximately 46% market share in 2024. This segment's prominence is driven by its exceptional water use efficiency of 90%, making it particularly valuable in Australia's predominantly arid and semi-arid regions. The technology has gained significant traction among farmers due to its ability to reduce energy consumption by around 28% compared to center-pivot and lateral-move systems, while also producing approximately 25% less greenhouse gas emissions. The Australian government's On-Farm Irrigation Efficiency Program, which provides funding for upgrading irrigation systems to surface or sub-surface drip systems, has further accelerated adoption. Additionally, dairy farmers in Southern Murray Darling have increasingly embraced sub-surface drip irrigation for pasture production, particularly in response to decreased water supply, as it ensures uniform moisture and nutrient distribution for optimal pasture growth.

Remaining Segments in Irrigation Machinery

The irrigation equipment market in Australia is further segmented into sprinkler irrigation and other irrigation machinery systems. Sprinkler irrigation systems have established a strong presence in the market, particularly in golf courses and large-scale agricultural operations, offering various options including hand-move sprinkler systems, center-pivot sprinkler systems, solid set and fixed sprinkler systems, and traveling gun sprinkler systems. The other irrigation machinery segment encompasses precision irrigation, pivot irrigation, and boom irrigation systems, which are gaining popularity due to the increasing adoption of precision-based farming operations. These systems are particularly valuable in greenhouse operations and are benefiting from Australia's growing position as a hub for agri-tech and food-tech innovations, with strong connections to rapidly expanding Asian markets.

Segment Analysis: Other Types

Sprayers Segment in Australia Agricultural Machinery Market

The sprayers segment dominates the Other Types category in the Australian agricultural machinery market, driven by the high demand for pesticides and other agrochemicals to increase crop productivity. Australia's significant investment in pesticides, with approximately 8,000 pesticides available in the market where 75% are used for commercial farming, has created a strong foundation for sprayer equipment adoption. The development of tractor-operated sprayers is gradually replacing handheld sprayers, indicating a shift toward modernization of spraying equipment in the country. Companies like AgriFac are introducing advanced technologies such as AiCPlus for self-propelled sprayers, enabling spot-specific treatments that reduce chemical usage by targeting specific weeds. The availability of smart spraying technologies that improve efficiency and reduce chemical waste has been instrumental in driving market growth. Major agricultural manufacturing companies continue to innovate in this space, as evidenced by John Deere's introduction of new spraying equipment with technologies like See & Spray Select, which helps spray solutions effectively to targeted areas while reducing costs associated with excessive chemical usage.

Australia Agricultural Machinery Industry Overview

Top Companies in Australia Agricultural Machinery Market

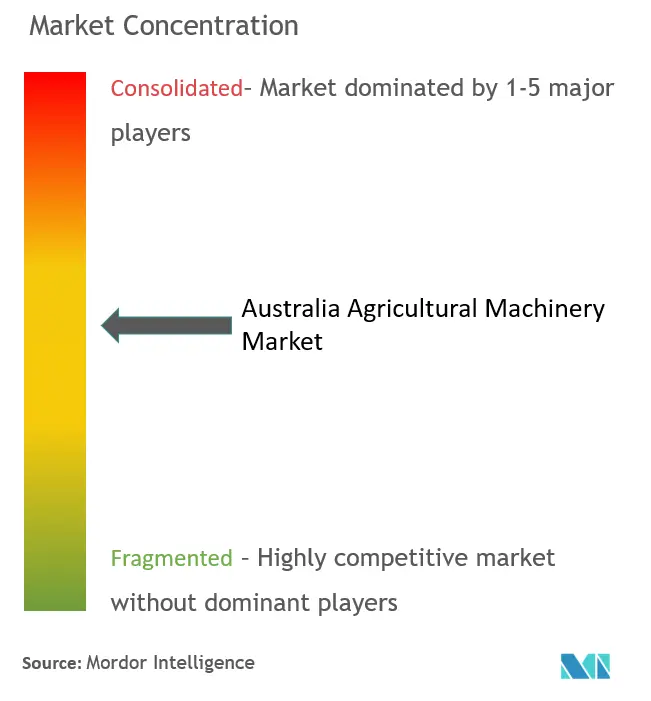

The agricultural machinery market in Australia is characterized by strong product innovation initiatives from leading players like Deere & Company, CNH Industrial, AGCO Corporation, and Kubota Australia. Companies are focusing heavily on launching advanced machinery with smart features, precision farming capabilities, and improved efficiency to meet evolving farmer needs. The competitive landscape shows significant investment in research and development, particularly in areas like autonomous operations, IoT integration, and sustainable solutions. Strategic expansions through dealership networks remain a key trend, as evidenced by companies like KUHN expanding their presence across New South Wales and Queensland. While partnerships and collaborations are emerging, particularly in technology integration and digital solutions, mergers and acquisitions activity has been notably limited during the study period, suggesting organic growth remains the preferred strategy for market development.

Consolidated Market Led By Global Players

The Australian agricultural machinery market demonstrates a high level of consolidation, with major global manufacturers dominating the competitive landscape. These multinational companies leverage their extensive research capabilities, established brand reputation, and comprehensive distribution networks to maintain their market positions. The presence of local players is relatively limited, with most domestic companies focusing on specialized agricultural equipment or custom solutions for specific farming applications. The market structure favors large conglomerates that can offer complete farming solutions across various equipment categories, from tractors to irrigation systems.

The competitive dynamics are shaped by the strong presence of international players who bring global expertise and advanced technology to the Australian market. These companies have established manufacturing facilities, robust after-sales service networks, and strong relationships with local dealers. The market shows limited regional player dominance, with global brands controlling significant market share through their superior technological capabilities and extensive product portfolios. The competitive environment is characterized by high entry barriers due to substantial capital requirements, established distribution networks, and the need for advanced technological expertise.

Innovation and Service Drive Market Success

Success in the Australian agricultural machinery market increasingly depends on companies' ability to offer innovative solutions that address specific regional farming challenges while maintaining strong service support networks. Incumbent players must focus on developing advanced features like precision farming capabilities, autonomous operations, and integrated digital solutions to maintain their market position. The ability to provide comprehensive after-sales support, spare parts availability, and technical assistance across Australia's vast geographic expanse is becoming increasingly crucial for market success. Companies need to balance product innovation with practical considerations like ease of maintenance and durability in harsh Australian conditions.

For contenders looking to gain market share, specialization in specific farm equipment categories or focusing on underserved market segments presents opportunities. Success factors include developing strong relationships with local dealers, offering competitive financing options, and providing specialized solutions for specific crop types or farming conditions. The market shows relatively low substitution risk due to the essential nature of agricultural implements, but regulatory requirements related to emissions, safety standards, and environmental impact are becoming increasingly important considerations. Companies must also address the growing emphasis on sustainable farming practices and water conservation in their product development strategies, while maintaining cost competitiveness in a market where purchase decisions are heavily influenced by return on investment considerations.

Australia Agricultural Machinery Market Leaders

-

John Deere Australia

-

AGCO Corporation

-

Kubota Australia

-

CLAAS KGaA mbH

-

CNH Industrial NV

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Australia Agricultural Machinery Market News

- February 2024: John Deere has announced that autonomous battery-powered electric tractors will be launched in 2026 due to the growing demand for diesel alternatives.

- September 2023: The Western Australian State Government unveiled a USD 10.3 million expansion at Muresk Institute, ushering in a new phase of agricultural education. The expansion's focal point is the Agricultural Machinery Training Centre (AMTC), which features new workshops, classrooms, and information technology laboratories.

- August 2023: John Deere launched John Deere 1 Series Round Balers in the Australian market. It has the Bale Doc technology to document bale moisture and weight in near real-time.

Australia Agricultural Machinery Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

- 4.1 Market Overview

-

4.2 Market Drivers

- 4.2.1 Declining Labour Availability and Rising Cost of Farm Labour

- 4.2.2 Rapid Technological Advancements by Key Players

- 4.2.2.1 Rising Preference for Agricultural Machinery

-

4.3 Market Restraints

- 4.3.1 High Cost of Agricultural Machinery and Repair

- 4.3.1.1 Data Privacy concerns in Modern Farming

-

4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION

-

5.1 Tractors

- 5.1.1 Horsepower

- 5.1.1.1 Below 40 HP

- 5.1.1.2 40-120 HP

- 5.1.1.3 Above 120 HP

- 5.1.2 Utility Type

- 5.1.2.1 Compact Utility Tractors

- 5.1.2.2 Utility Tractors

- 5.1.2.3 Row Crop Tractors

-

5.2 Ploughing and Cultivating Machinery

- 5.2.1 Ploughs

- 5.2.2 Harrows

- 5.2.3 Cultivators and Tillers

- 5.2.4 Other Planting and Cultivating Machinery

-

5.3 Planting Machinery

- 5.3.1 Seed Drills

- 5.3.2 Planters

- 5.3.3 Spreaders

- 5.3.4 Other Planting Machinery

-

5.4 Harvesting Machinery

- 5.4.1 Combine Harvesters

- 5.4.2 Forage Harvesters

- 5.4.3 Other Harvesting Machinery

-

5.5 Haying and Forage Machinery

- 5.5.1 Mowers and Conditioners

- 5.5.2 Balers

- 5.5.3 Other Haying and Forage Machinery

-

5.6 Irrigation Machinery

- 5.6.1 Sprinkler Irrigation

- 5.6.2 Drip Irrigation

- 5.6.3 Other Irrigation Machinery

- 5.7 Other Types

6. COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

-

6.3 Company Profiles

- 6.3.1 Mahindra Automotive Australia

- 6.3.2 Deere & Company

- 6.3.3 Kubota Australia

- 6.3.4 Valmont Industries Inc.

- 6.3.5 Netafim

- 6.3.6 CNH Industrial NV

- 6.3.7 CLASS KGaA mbH

- 6.3.8 AGCO Corporation

- 6.3.9 Kuhn Farm Machinery Pty Ltd

- 6.3.10 Daedong Industrial Co. Ltd

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Australia Agricultural Machinery Industry Segmentation

Agricultural machinery includes mechanical devices used in farming and other agriculture practices. These include different types of equipment, from hand tools and power tools to tractors and various farm implements used to operate farming activities.

The Australian Agricultural Machinery Manufacturers Market is Segmented by Tractors (Horsepower and Utility Type), Ploughing and Cultivating Machinery (Ploughs, Harrows, Cultivators and Tillers, and Other Planting and Cultivating Machinery), Planting Machinery (Seed Drills, Planters, Spreaders, and Other Planting Machinery), Harvesting Machinery (Combine Harvesters-Threshers, Forage Harvesters, and Other Harvesting Machinery), Haying and Forage Machinery (Mowers and Conditioners, Balers, and Other Haying and Forage Machinery) and Irrigation Machinery (Sprinkler Irrigation, Drip Irrigation and Other Irrigation Machinery). The Report Offers the Market Size in Value Terms in USD for all the Abovementioned Segments.

| Tractors | Horsepower | Below 40 HP | |

| 40-120 HP | |||

| Above 120 HP | |||

| Utility Type | Compact Utility Tractors | ||

| Utility Tractors | |||

| Row Crop Tractors | |||

| Ploughing and Cultivating Machinery | Ploughs | ||

| Harrows | |||

| Cultivators and Tillers | |||

| Other Planting and Cultivating Machinery | |||

| Planting Machinery | Seed Drills | ||

| Planters | |||

| Spreaders | |||

| Other Planting Machinery | |||

| Harvesting Machinery | Combine Harvesters | ||

| Forage Harvesters | |||

| Other Harvesting Machinery | |||

| Haying and Forage Machinery | Mowers and Conditioners | ||

| Balers | |||

| Other Haying and Forage Machinery | |||

| Irrigation Machinery | Sprinkler Irrigation | ||

| Drip Irrigation | |||

| Other Irrigation Machinery | |||

Need A Different Region or Segment?

Customize Now

Australia Agricultural Machinery Market Research Faqs

How big is the Australia Agricultural Machinery Market?

The Australia Agricultural Machinery Market size is expected to reach USD 6.21 billion in 2025 and grow at a CAGR of 3.10% to reach USD 7.23 billion by 2030.

What is the current Australia Agricultural Machinery Market size?

In 2025, the Australia Agricultural Machinery Market size is expected to reach USD 6.21 billion.

Who are the key players in Australia Agricultural Machinery Market?

John Deere Australia, AGCO Corporation, Kubota Australia, CLAAS KGaA mbH and CNH Industrial NV are the major companies operating in the Australia Agricultural Machinery Market.

What years does this Australia Agricultural Machinery Market cover, and what was the market size in 2024?

In 2024, the Australia Agricultural Machinery Market size was estimated at USD 6.02 billion. The report covers the Australia Agricultural Machinery Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Australia Agricultural Machinery Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Australia Agricultural Machinery Market Research

Mordor Intelligence provides a comprehensive analysis of the Australian agricultural machinery sector. We leverage our extensive expertise in farm equipment and agri machinery research. Our detailed report covers the full range of agricultural equipment, including tractors, harvesting machinery, agricultural implements, and tillage equipment. The analysis also explores emerging technologies such as agricultural drones, agricultural robotics, and solutions for farm mechanization. This provides stakeholders with crucial insights into market dynamics and technological advancements in the region.

The report, available as an easy-to-download PDF, offers valuable insights for manufacturers, distributors, and investors in agricultural machinery and farm machinery. Our analysis covers various segments, including irrigation equipment, planting equipment, livestock equipment, and seeding equipment. We particularly emphasize technological innovations like autonomous farm equipment, precision agriculture equipment, and smart farming equipment. Traditional aspects such as agricultural attachments and crop protection equipment are also addressed. Stakeholders benefit from our detailed examination of agricultural automation trends and the integration of agricultural tools in modern farming practices. This supports informed decision-making in this evolving sector.