Market Size of Austin Data Center Industry

| Study Period | 2018 - 2030 |

| Base Year For Estimation | 2023 |

| Forecast Data Period | 2024 - 2030 |

| Historical Data Period | 2018 - 2022 |

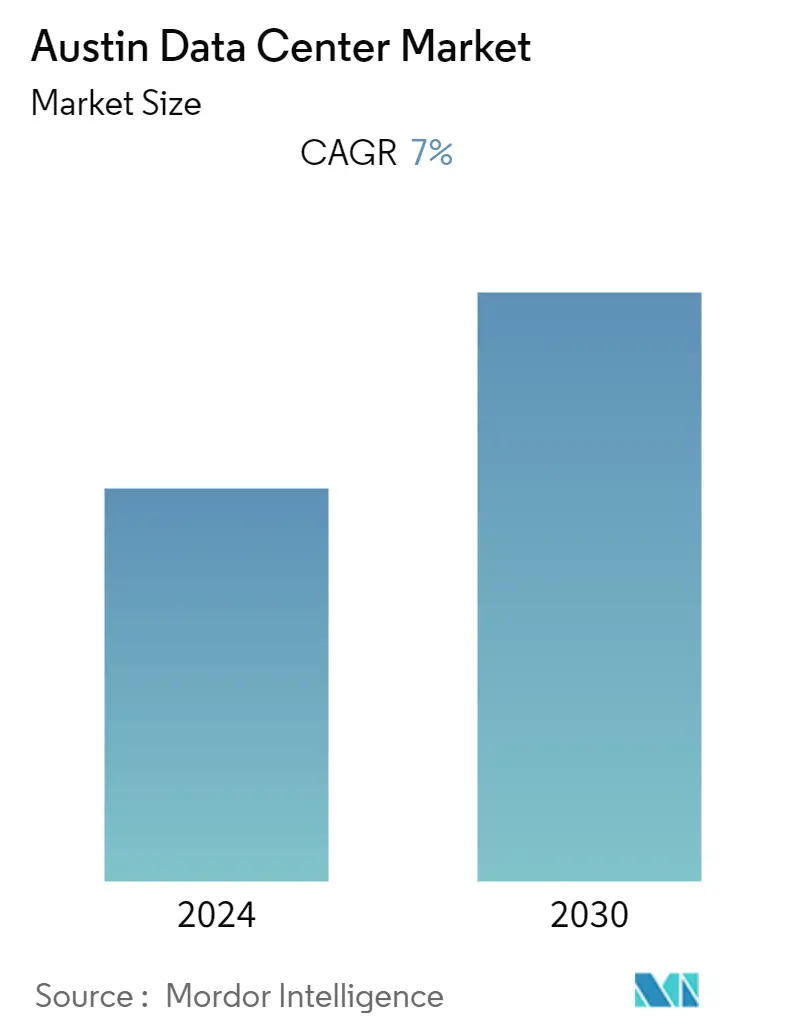

| CAGR | 7.00 % |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Austin Data Center Market Analysis

The Atlanta Data Center market is a volume of 227.16 MW in the previous year and is expected to grow at a CAGR of 7% during the forecast period to become a volume of 488.46 MW by the next six years. The main drivers anticipated to drive the market expansion are the increasing demand for energy-efficient data centers, considerable investment by colocation service and managed service providers, and expanding hyperscale data center building. Additionally, the development of big data, cloud computing, and the Internet of Things (IoT) has made it possible for businesses to invest in new data centers to preserve business continuity. Additionally, industrial development is expected to prosper due to the rising need for security, operational efficiency, improved mobility, and bandwidth. Software-based data centers boost industry growth by providing a higher level of automation.

- Artificial intelligence (AI) with machine learning (ML) necessitates the development of brand-new data center infrastructure more than any other application. Artificial intelligence (AI) and machine learning (ML) may require three times the power density of traditional data processing, necessitating a revolution in data center architecture. This is also dependent on sophisticated cooling systems to support the larger output. The intense nature of AI and ML computations may also result in a significant dispersion of computational, memory, and storage resources among many processors in a computational cluster.

- The developments that are happening toward the data power will drive the studied market. For instance, in April 2022, Austin Commercial, a division of Austin Industries and one of the country's most diverse builders, announced an enterprise collaboration with Versatile. This construction technology pioneer uses artificial intelligence (AI) and the Internet of Things (IoT) to optimize building processes. Versatile's CraneView, which automatically collects and analyses productivity data from construction sites, is the first to be employed by a Texas-based general contractor.

- A data center must adhere to the following specification to be defined as a Tier III facility. The facility should offer N+1 (the amount required for operation plus a backup) fault tolerance. Also, the Tier III facility providers can undergo routine maintenance without a hiccup in the overall operations. However, unplanned maintenance and emergencies may cause problems affecting the system. These problems may potentially affect customer-facing operations.

- These data center facilities provide a 99.982% uptime. The companies using these Tier III facilities are often growing companies or businesses that are considerably larger than the average SMBs (Small to Medium Businesses). These Tier III facilities also offer most of the features of a Tier IV infrastructure facility without some elite protection. For instance, enterprises can leverage the advantage of dual power sources and redundant cooling as the network streams are fully backed up.

- On the flip side, the country's commercial real estate has been constantly evolving and changing due to the continued integration of technology at all levels of the industry and across all property types. As more companies have been transitioning toward cloud computing with major vendors expanding their capacities has been influencing land prices; for instance, Amazon Web Services (AWS) currently has cloud infrastructure in 22 regions and has predicted that new data centers may be needed in hundreds of regions to keep up with demand.

- According to North American Data Centers Report, the strong leasing activity during the second quarter of the pandemic stemmed from hyperscale companies, as many of these tenants pulled forward their requirements due to the distributed workforce and the work-from-home lifestyle. In addition to remote work, online gaming, social media, video streaming, and e-commerce drove leasing activity during the pandemic. Colocation service providers and cloud have been benefactors of rising SaaS and network customer demand from the pandemic response necessitating remote working and educating. In addition, these services are particularly recession-resistant, and demand for services has been increasing, translating to data center construction projects remaining in progress to ensure they could meet demand.

Austin Data Center Industry Segmentation

A data center is a physical room, building, or facility that holds IT infrastructure used to construct, run, and provide applications and services and store and manage the data connected with those applications and services.

The Austin Data Center Market is segmented by DC Size (Small, Medium, Large, Massive, Mega), by Tier Type (Tier 1&2, Tier 3, Tier 4), by Absorption (Utilized (Colocation Type (Retail, Wholescale, Hyperscale), End User ( Cloud & IT, Telecom, Media & Entertainment, Government, BFSI, Manufacturing, E-Commerce)) , Non-Utilized).

The market sizes and forecasts are provided in terms of volume (MW) for all the above segments.

| DC Size | |

| Small | |

| Medium | |

| Large | |

| Massive | |

| Mega |

| Tier Type | |

| Tier 1 & 2 | |

| Tier 3 | |

| Tier 4 |

| Absorption | |||||||||||||||||

| |||||||||||||||||

| Non-Utilized |

Austin Data Center Market Size Summary

The Austin Data Center market is poised for significant growth, driven by the increasing demand for energy-efficient and scalable data center solutions. The expansion of cloud computing, big data, and IoT technologies has prompted businesses to invest in new data centers to ensure business continuity and enhance operational efficiency. The market is further bolstered by substantial investments from colocation and managed service providers, as well as the development of hyperscale data centers. The rise of artificial intelligence and machine learning is also influencing the market, necessitating advanced data center infrastructure capable of handling higher power densities and sophisticated cooling systems. The demand for Tier III and Tier IV data centers, which offer high uptime and fault tolerance, is expected to grow as businesses seek reliable and resilient infrastructure to support their operations.

The market landscape in Austin is characterized by the presence of major players such as Digital Realty Trust, Inc., DataBank, and CyrusOne, who are actively engaging in strategic partnerships and product developments to capture a larger market share. Recent developments include significant construction projects and collaborations aimed at expanding data center capacity and enhancing connectivity options. The retail colocation market is also experiencing growth, driven by the high demand for colocation services, particularly from smaller enterprises and developing regions. These facilities offer economic advantages and ease of maintenance, making them an attractive option for businesses looking to leverage data center capabilities without the overhead of owning a facility. As the market continues to evolve, the integration of new technologies and the expansion of infrastructure are expected to play a crucial role in meeting the increasing demand for data center services in Austin.

Austin Data Center Market Size - Table of Contents

-

1. MARKET SEGMENTATION

-

1.1 DC Size

-

1.1.1 Small

-

1.1.2 Medium

-

1.1.3 Large

-

1.1.4 Massive

-

1.1.5 Mega

-

-

1.2 Tier Type

-

1.2.1 Tier 1 & 2

-

1.2.2 Tier 3

-

1.2.3 Tier 4

-

-

1.3 Absorption

-

1.3.1 Utilized

-

1.3.1.1 Colocation Type

-

1.3.1.1.1 Retail

-

1.3.1.1.2 Wholesale

-

1.3.1.1.3 Hyperscale

-

-

1.3.1.2 End User

-

1.3.1.2.1 Cloud & IT

-

1.3.1.2.2 Telecom

-

1.3.1.2.3 Media & Entertainment

-

1.3.1.2.4 Government

-

1.3.1.2.5 BFSI

-

1.3.1.2.6 Manufacturing

-

1.3.1.2.7 E-Commerce

-

1.3.1.2.8 Other End User

-

-

-

1.3.2 Non-Utilized

-

-

Austin Data Center Market Size FAQs

What is the current Austin Data Center Market size?

The Austin Data Center Market is projected to register a CAGR of 7% during the forecast period (2024-2030)

Who are the key players in Austin Data Center Market?

Digital Realty Trust, Inc., DataBank Ltd, CyrusOne LLC, Switch, Inc. and Sabey Data Center Properties LLC are the major companies operating in the Austin Data Center Market.