| Study Period | 2017 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 6.65 Billion |

| Market Size (2030) | USD 11.29 Billion |

| CAGR (2025 - 2030) | 11.18 % |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order |

Asia-Pacific Pet Treats Market Analysis

The Asia-Pacific Pet Treats Market size is estimated at 6.65 billion USD in 2025, and is expected to reach 11.29 billion USD by 2030, growing at a CAGR of 11.18% during the forecast period (2025-2030).

The Asia-Pacific pet treats market is experiencing significant transformation driven by evolving consumer preferences and changing pet ownership dynamics. The region has witnessed substantial growth in pet ownership, with the total pet population reaching 511.1 million in 2022, reflecting the growing importance of pets in households. This shift has been accompanied by increasing pet humanization, where pets are increasingly considered family members rather than just animals. Pet parents are demonstrating greater willingness to invest in premium and high-quality pet treats, particularly those offering specific functional benefits. This trend is especially evident in developed markets like Japan and Australia, where pet owners are actively seeking customized and premium treat options.

The market is witnessing a notable shift towards natural and functional pet snacks, reflecting broader consumer trends in health and wellness. Pet treat manufacturers are responding by developing products with clean labels, minimal processing, and functional ingredients that address specific health concerns. Dental treats have emerged as a particularly important category, offering both oral health benefits and entertainment value for pets. The industry has seen significant innovation in freeze-dried and jerky pet treats, which are gaining popularity due to their high meat content and minimal processing. These products are particularly appealing to pet owners seeking treats that closely resemble natural food sources.

Distribution channels are evolving rapidly to meet changing consumer preferences, with e-commerce emerging as a dominant force in the pet treats market. Pet treats have become a significant category in the overall pet food market, accounting for 18.2% of the total pet food market value in 2022. Online platforms are offering unprecedented variety and convenience, while specialty stores are differentiating themselves through expert advice and premium product selections. The market is seeing increased integration between online and offline channels, with retailers developing omnichannel strategies to provide seamless shopping experiences.

Product innovation and customization are driving market dynamics, with manufacturers focusing on developing treats that cater to specific pet needs and owner preferences. Chinese pet owners, for instance, demonstrate significant spending power, with an average expenditure of USD 509 per pet, indicating strong potential for premium and specialized products. Manufacturers are investing in research and development to create pet rewards that address specific health concerns while maintaining palatability. There is also a growing emphasis on sustainable packaging and environmentally conscious production methods, reflecting increased consumer awareness of environmental issues. Mars Incorporated, for example, opened its first pet food research and development center in Asia-Pacific in 2023, highlighting the industry's commitment to innovation and regional market development.

Asia-Pacific Pet Treats Market Trends

The evolving ecosystem of pet cafes and pet stores that assist in taking care of the animals and offer a wide variety of cat food products and services is driving the population of cats

- In Asia-Pacific, cats have a lower share compared to dogs, accounting for 26.1% of the pet population in 2022. Countries such as China, India, and Australia witnessed an increase in pet ownership due to health benefits such as feeling relaxed and less stressed and companionship. Therefore, the cat population grew by 0.28% between 2017 and 2022. The shares of cat parents are higher than dog parents in Indonesia and Malaysia, accounting for 47% and 34%, respectively, in 2021. The religious cultures of these countries and the preference for cats as pets over dogs drove the cat population. This trend may help the companies invest more in cat food in these countries.

- In China, there has been an increase in the no. of pets, including cats, in urban areas, and the pet population, including cats, grew by 10.2% between 2018-2020, reaching 100.8 million in 2020. The cat population grew from 74.4 million in 2020 to 82.5 million in 2022 due to a rise in the need for companionship during the pandemic. This trend may have long-term effects as the life span of cats is more than 20 years.

- A new pet adoption and purchase ecosystem is evolving in the region in the form of pet cafes and pet stores that assist in purchasing and taking care of animals through a wide variety of pet food products and services. For instance, in Vietnam, the Meow House by R House is a cat cafe that serves vegetarian and vegan food and serves as a home for cats. Factors such as the rising adoption of cats due to health benefits, the region's culture, and changes in the pet ecosystem are helping boost cat adoption in the region.

Increased demand for premium pet treats such as grain-free and natural products is boosting pet expenditure

- In Asia-Pacific, there has been a rise in pet expenditure because of the availability of different types of pet food and pet parents' preference for good quality pet food as they are willing to pay premium prices. Traditionally, pet parents had a higher number of pet dogs, but there has been an increase in the cat population in recent years. However, pet dogs had a higher share of expenditure in 2022, i.e., 45.4%. This high share was due to higher consumption of high-quality pet food and a high demand for customized treats for dogs. Dogs are most popular in Australia, and about 40% of households had a pet dog in 2022, which increased the demand for pet treats.

- China, India, and South Korea are the major pet markets in the region, further registering growth in pet expenditure. These countries witnessed a high number of pet adoptions and high consumption of good quality, premium pet food, especially after the pandemic, as pet parents became more aware of the nutritional requirements of their pets. For instance, in Hong Kong's cat food market, the premium pet food segment accounted for 75% of the pet food sales in 2022. Online pet food sales are high, especially in China, due to the vast number of products on the websites and the ease of placing orders. For instance, in 2022, China's pet food sales from online channels were 58.9% compared to the offline pet stores' contribution of 27.5%.

- The rising demand for pet food and growing awareness about good quality pet food are expected to increase pet expenditure in the region during the forecast period.

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT

- The higher life span and the evolution of a pet ecosystem are helping increase the dog population in the region

- Fish is one of the most adopted other pets in the region

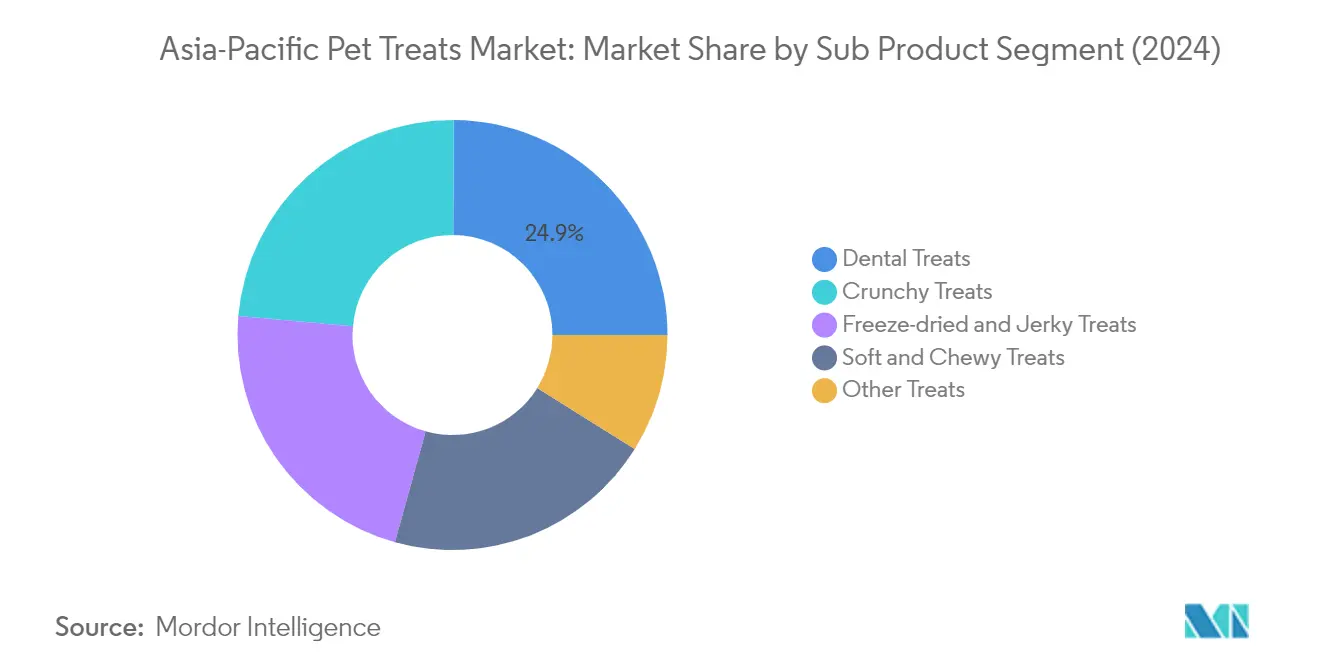

Segment Analysis: SUB PRODUCT

Dental Treats Segment in Asia-Pacific Pet Treats Market

Dental treats have emerged as the dominant segment in the Asia-Pacific pet treats market, commanding approximately 25% of the market share in 2024. The segment's leadership position is primarily attributed to the increasing awareness among pet owners about the importance of maintaining their pets' oral hygiene. These treats are specifically designed to provide mechanical cleaning action for teeth, help control plaque and tartar buildup, and freshen breath in pets. The growing focus on preventive healthcare for pets and the rising incidence of dental issues in companion animals have significantly contributed to the segment's dominance. Additionally, veterinarians' recommendations and the treats' dual benefits of serving as both a reward and a dental care solution have strengthened their market position.

Freeze-dried and Jerky Treats Segment in Asia-Pacific Pet Treats Market

The freeze-dried and jerky treats segment is projected to experience the most robust growth in the Asia-Pacific pet treats market during 2024-2029, with an expected CAGR of approximately 13%. This remarkable growth trajectory is driven by several factors, including the increasing demand for minimally processed treats with high meat content and longer shelf life. Pet owners are increasingly gravitating towards these treats due to their nutritional superiority, as the freeze-drying process preserves the natural nutrients better than traditional processing methods. The segment's growth is further fueled by the rising preference for natural and premium pet treats, particularly among urban pet owners who are willing to pay more for high-quality, protein-rich treats that closely resemble real meat in taste and texture.

Remaining Segments in Sub Product Segmentation

The other significant segments in the Asia-Pacific pet treats market include crunchy treats, soft & chewy treats, and other treats, each serving distinct consumer preferences and pet needs. Crunchy treats maintain a strong market presence due to their effectiveness in satisfying pets' natural urge to chew while providing essential nutrients. Soft & chewy treats have gained popularity, particularly among owners of senior pets or those with dental sensitivities, offering easier consumption while maintaining palatability. The other treats category, which includes specialized products like lickable treats and catnips, caters to specific pet preferences and training needs, contributing to the market's diversity and comprehensive product offerings.

Segment Analysis: PETS

Dogs Segment in Asia-Pacific Pet Treats Market

The dogs segment dominates the Asia-Pacific pet treats market, accounting for approximately 51% of the total market value in 2024. This significant market share can be attributed to the larger population of dogs compared to other pets in the region, with dogs accounting for nearly 34% of the total pet population. The segment's dominance is further strengthened by dogs' higher preference for treats compared to other pets, along with their natural desire to chew and their requirement for training aids. The market is particularly driven by the increasing demand for dental treats, crunchy treats, and freeze-dried treats among dog owners. Additionally, the growing trend of pet humanization and the increasing willingness of pet parents to spend on premium and functional treats for their dogs have contributed significantly to this segment's market leadership.

Cats Segment in Asia-Pacific Pet Treats Market

The cats segment is experiencing remarkable growth in the Asia-Pacific pet treats market, projected to expand at approximately 12% CAGR during 2024-2029. This accelerated growth is primarily driven by the increasing adoption of cats in urban areas, particularly due to their adaptability to smaller living spaces compared to dogs. The segment's growth is further fueled by the rising demand for specialized cat treats, including dental treats and freeze-dried options that cater to cats' specific nutritional needs and preferences. The increasing awareness among cat owners about the importance of treats in maintaining dental health and providing mental stimulation is also contributing to the segment's expansion. Moreover, the growing trend of premium and natural ingredient-based treats, particularly those with high meat content and minimal processing, is expected to sustain this growth trajectory.

Remaining Segments in Asia-Pacific Pet Treats Market

The other pets segment, which includes treats for fish, birds, and small animals, plays a significant role in the Asia-Pacific pet treats market. This segment caters to a diverse range of pets that are increasingly popular in urban households due to their lower maintenance requirements and suitability for smaller living spaces. The segment primarily focuses on specialized treats designed for specific dietary needs and preferences of various pet types, including soft and chewy treats for small mammals and specialized food supplements for birds. The market for these treats is particularly influenced by the growing trend of keeping exotic pets and the increasing awareness about proper nutrition for these animals. Additionally, the segment benefits from the expanding distribution channels and the development of innovative treat formulations specifically designed for these diverse pet categories.

Segment Analysis: DISTRIBUTION CHANNEL

Online Channel Segment in Asia-Pacific Pet Treats Market

The online channel has emerged as the dominant distribution channel in the Asia-Pacific pet treats market, commanding approximately 38% market share in 2024. This channel's prominence is driven by several key factors including the convenience of home delivery, wider product selection, and competitive pricing through various e-commerce platforms. Major online platforms like Taobao and Tmall in China, Lazada in Thailand, and Bow and Wow in the Philippines have significantly contributed to this channel's growth. The segment has particularly benefited from the increasing digitalization of retail in key markets like China, Japan, and Indonesia, which together account for nearly 89% of online pet snacks sales in the region. The channel's success is further bolstered by features such as detailed product information, customer reviews, and the ability to compare prices across different brands, making it particularly attractive to modern pet owners who prioritize convenience and informed decision-making in their purchasing behavior.

Online Channel Growth in Asia-Pacific Pet Treats Market

The online channel is projected to maintain its strong growth trajectory, with an expected growth rate of approximately 12% during the forecast period 2024-2029. This robust growth is being fueled by the increasing penetration of e-commerce platforms in emerging markets, improved logistics networks, and the growing preference for contactless shopping options. The channel's growth is particularly pronounced in dental treats and premium pet snacks segments, where online platforms offer extensive product information and educational content about pet health benefits. The expansion of mobile commerce, integration of artificial intelligence for personalized shopping experiences, and the introduction of subscription-based models for regular pet rewards deliveries are further accelerating this growth. Additionally, online retailers are increasingly partnering with veterinary professionals and pet care experts to provide specialized advice and product recommendations, enhancing customer trust and loyalty in the digital shopping experience.

Remaining Segments in Distribution Channel

The other distribution channels in the Asia-Pacific pet treats market include specialty stores, supermarkets/hypermarkets, convenience stores, and other retail formats. Specialty stores remain significant due to their expert staff, personalized service, and comprehensive product range. Supermarkets and hypermarkets maintain their importance through their widespread presence and the convenience of one-stop shopping for pet owners. Convenience stores, while having a smaller market share, serve an important role in providing easy access to pet treats, especially in urban areas. Other channels, including veterinary clinics and pet shelters, contribute to the market by offering specialized products and professional recommendations. Each of these channels serves distinct consumer needs and preferences, contributing to a robust and diverse distribution network in the region's pet treats market.

Asia-Pacific Pet Treats Market Geography Segment Analysis

Pet Treats Market in China

China continues to dominate the largest pet market in Asia, driven by its massive pet population and increasing pet humanization trends. The country accounts for approximately 53% of the regional market value in 2024, establishing itself as the undisputed leader in the pet treats sector. The market's strength is particularly evident in dental treats, which have emerged as the leading segment due to growing awareness about pet dental health. Chinese pet owners are increasingly focusing on premium and functional treats, with a notable preference for products that offer specific health benefits. The country's urban areas have witnessed a significant surge in pet ownership, accompanied by sophisticated consumer preferences for high-quality, natural ingredients. The market is characterized by strong distribution networks, particularly in online channels, which have become a preferred mode of purchase for pet treats. Local manufacturers are increasingly investing in research and development to create innovative products that cater to specific dietary requirements and health concerns of pets.

Pet Treats Market in the Philippines

The Philippines represents the most dynamic market in the Asia-Pacific region, with projections indicating a remarkable growth rate of approximately 20% annually from 2024 to 2029. This exceptional growth is fueled by rapidly evolving consumer preferences and increasing awareness about pet nutrition. The market is witnessing a significant shift towards premium pet treats, particularly in dental and crunchy varieties, which have emerged as leading segments. Filipino pet owners are increasingly recognizing the importance of treats not just as rewards but as essential components of their pets' overall health and wellness routine. The country's pet treat market is benefiting from expanding distribution networks, particularly in urban areas, where specialty pet stores and online retailers are making premium products more accessible. Manufacturers are responding to this growth by introducing innovative products that cater to local preferences while maintaining international quality standards. The market is also seeing increased competition, leading to product diversification and improved quality standards across all segments.

Pet Treats Market in Japan

Japan's pet treats market exemplifies sophistication and premium quality, reflecting the country's advanced pet care culture. Japanese pet owners are particularly discerning about product quality and safety, driving manufacturers to maintain exceptionally high production standards. The market is characterized by strong innovation in functional treats, particularly those addressing specific health concerns such as aging and dental care. There's a growing trend toward natural and organic ingredients, with Japanese consumers showing a strong preference for treats that align with human-grade food standards. The country's retail landscape for pet treats is highly developed, with specialty pet stores and premium pet boutiques playing a crucial role in product distribution. Japanese manufacturers are at the forefront of developing novel treat formulations, often incorporating local ingredients and traditional wellness concepts into their products. The market also shows strong demand for portion-controlled and calorie-conscious treats, reflecting the overall health-conscious nature of Japanese pet owners.

Pet Treats Market in Australia

Australia's pet treats market is characterized by its strong focus on natural and locally sourced ingredients, reflecting the country's emphasis on sustainable and ethical pet care products. The market demonstrates sophisticated consumer preferences, with pet owners increasingly seeking treats that offer specific functional benefits beyond basic nutrition. Australian pet parents show a strong inclination towards grain-free and novel protein treats, driving innovation in product formulations. The country's regulatory framework ensures high-quality standards in pet treats manufacturing, contributing to consumer confidence in domestic products. Distribution channels are well-developed, with specialty pet retailers and veterinary clinics playing significant roles in product education and recommendations. The market shows particular strength in dental treats and natural chews, reflecting growing awareness about pet dental health. Australian manufacturers are increasingly focusing on environmentally sustainable packaging and production methods, aligning with consumer environmental consciousness.

Pet Treats Market in Other Countries

The pet treats markets in other Asia-Pacific countries, including India, Indonesia, Malaysia, Taiwan, Thailand, and Vietnam, each demonstrate unique characteristics and growth patterns. These markets are experiencing varying degrees of development, influenced by local pet ownership cultures and economic conditions. Countries like India and Indonesia are showing promising growth potential due to their expanding middle-class populations and increasing pet humanization trends. Taiwan and Thailand demonstrate mature market characteristics with sophisticated consumer preferences, particularly in premium treat segments. Malaysia and Vietnam are emerging as significant markets, with growing awareness about pet nutrition and increasing disposable incomes driving market expansion. These markets collectively represent significant opportunities for manufacturers, particularly in developing region-specific products that cater to local preferences while maintaining international quality standards. Notably, the demand for dog treats in Malaysia is rising as consumers seek high-quality options for their pets.

Asia-Pacific Pet Treats Industry Overview

Top Companies in Asia-Pacific Pet Treats Market

The Asia-Pacific pet treats market features several prominent companies actively expanding their presence through various strategic initiatives. Product innovation remains a key focus area, with companies developing new pet treats varieties targeting specific health benefits like dental care and introducing premium natural ingredients. Operational agility is demonstrated through investments in manufacturing facilities and distribution networks, particularly in high-growth markets like China and India. Companies are increasingly adopting expansion strategies through new facility establishments and production capacity enhancements to meet growing demand. Strategic partnerships with research institutes, packaging companies, and local distributors are being leveraged to enhance product development capabilities and market reach. The market also witnesses active engagement in digital transformation, with companies strengthening their e-commerce presence and online distribution channels.

Market Structure Shows Mixed Competition Dynamics

The Asia-Pacific pet treats market exhibits a fragmented competitive landscape with a mix of global conglomerates and regional specialists. Global players leverage their established brand portfolios, research capabilities, and extensive distribution networks to maintain strong market positions, while regional players compete through local market knowledge and specialized product offerings. The market demonstrates moderate consolidation, with the top players collectively holding a significant but not dominant share, indicating healthy competition and opportunities for new entrants.

The market is characterized by increasing merger and acquisition activities as companies seek to expand their geographical presence and product portfolios. Large multinational companies are actively acquiring local manufacturers to strengthen their regional footprint and gain access to established distribution networks. Regional players are forming strategic alliances and partnerships to enhance their competitive position and expand their market reach. The competitive dynamics are further influenced by the growing presence of private label products and the emergence of specialized premium treat manufacturers.

Innovation and Market Adaptation Drive Success

Success in the Asia-Pacific pet treats market increasingly depends on companies' ability to adapt to evolving consumer preferences and market dynamics. Incumbent players need to focus on continuous product innovation, particularly in premium and functional treats segments, while maintaining strong relationships with veterinarians and pet specialty retailers. Developing robust e-commerce capabilities and establishing direct-to-consumer channels are becoming crucial for market success. Companies must also invest in sustainable packaging solutions and transparent sourcing practices to meet growing consumer demands for environmentally responsible products.

For contenders looking to gain market share, focusing on niche segments and underserved markets presents significant opportunities. Success factors include developing specialized products for specific pet health needs, establishing a strong local manufacturing presence, and building effective distribution partnerships. Companies must also consider potential regulatory changes regarding pet food safety and labeling requirements, particularly in emerging markets. Building strong brand recognition through targeted marketing campaigns and educational initiatives about pet health and nutrition is becoming increasingly important for market success. The ability to maintain price competitiveness while ensuring product quality remains crucial in markets with high price sensitivity. Additionally, the emergence of pet snacks as a popular category offers new avenues for growth.

Asia-Pacific Pet Treats Market Leaders

-

Colgate-Palmolive Company (Hill's Pet Nutrition Inc.)

-

EBOS Group Limited

-

General Mills Inc.

-

Mars Incorporated

-

Nestle (Purina)

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Asia-Pacific Pet Treats Market News

- May 2023: Nestle Purina launched new cat treats under the Friskies "Friskies Playfuls - treats" brand. These treats are round in shape and are available in chicken and liver and salmon and shrimp flavors for adult cats.

- May 2023: Vafo Praha, s.r.o. launched its new range of Brit RAW Freeze-dried treats and toppers for dogs. These products are made up of high-quality proteins and minimally processed ingredients for potential health benefits.

- May 2023: Vafo Praha, s.r.o. launched its new line of functional snacks for dogs called Brit Dental Stick. The products are available in four different varieties with seven sticks in a package.

Asia-Pacific Pet Treats Market Report - Table of Contents

1. EXECUTIVE SUMMARY & KEY FINDINGS

2. REPORT OFFERS

3. INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4. KEY INDUSTRY TRENDS

-

4.1 Pet Population

- 4.1.1 Cats

- 4.1.2 Dogs

- 4.1.3 Other Pets

- 4.2 Pet Expenditure

- 4.3 Regulatory Framework

- 4.4 Value Chain & Distribution Channel Analysis

5. MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

-

5.1 Sub Product

- 5.1.1 Crunchy Treats

- 5.1.2 Dental Treats

- 5.1.3 Freeze-dried and Jerky Treats

- 5.1.4 Soft & Chewy Treats

- 5.1.5 Other Treats

-

5.2 Pets

- 5.2.1 Cats

- 5.2.2 Dogs

- 5.2.3 Other Pets

-

5.3 Distribution Channel

- 5.3.1 Convenience Stores

- 5.3.2 Online Channel

- 5.3.3 Specialty Stores

- 5.3.4 Supermarkets/Hypermarkets

- 5.3.5 Other Channels

-

5.4 Country

- 5.4.1 Australia

- 5.4.2 China

- 5.4.3 India

- 5.4.4 Indonesia

- 5.4.5 Japan

- 5.4.6 Malaysia

- 5.4.7 Philippines

- 5.4.8 Taiwan

- 5.4.9 Thailand

- 5.4.10 Vietnam

- 5.4.11 Rest of Asia-Pacific

6. COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

-

6.4 Company Profiles

- 6.4.1 ADM

- 6.4.2 Affinity Petcare SA

- 6.4.3 Clearlake Capital Group, L.P. (Wellness Pet Company Inc.)

- 6.4.4 Colgate-Palmolive Company (Hill's Pet Nutrition Inc.)

- 6.4.5 EBOS Group Limited

- 6.4.6 General Mills Inc.

- 6.4.7 IB Group (Drools Pet Food Pvt. Ltd.)

- 6.4.8 Mars Incorporated

- 6.4.9 Nestle (Purina)

- 6.4.10 Vafo Praha, s.r.o.

- 6.4.11 Virbac

- *List Not Exhaustive

7. KEY STRATEGIC QUESTIONS FOR PET FOOD CEOS

8. APPENDIX

-

8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter’s Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Asia-Pacific Pet Treats Industry Segmentation

Crunchy Treats, Dental Treats, Freeze-dried and Jerky Treats, Soft & Chewy Treats are covered as segments by Sub Product. Cats, Dogs are covered as segments by Pets. Convenience Stores, Online Channel, Specialty Stores, Supermarkets/Hypermarkets are covered as segments by Distribution Channel. Australia, China, India, Indonesia, Japan, Malaysia, Philippines, Taiwan, Thailand, Vietnam are covered as segments by Country.| Sub Product | Crunchy Treats |

| Dental Treats | |

| Freeze-dried and Jerky Treats | |

| Soft & Chewy Treats | |

| Other Treats | |

| Pets | Cats |

| Dogs | |

| Other Pets | |

| Distribution Channel | Convenience Stores |

| Online Channel | |

| Specialty Stores | |

| Supermarkets/Hypermarkets | |

| Other Channels | |

| Country | Australia |

| China | |

| India | |

| Indonesia | |

| Japan | |

| Malaysia | |

| Philippines | |

| Taiwan | |

| Thailand | |

| Vietnam | |

| Rest of Asia-Pacific |

Need A Different Region or Segment?

Customize Now

Asia-Pacific Pet Treats Market Research FAQs

How big is the Asia-Pacific Pet Treats Market?

The Asia-Pacific Pet Treats Market size is expected to reach USD 6.65 billion in 2025 and grow at a CAGR of 11.18% to reach USD 11.29 billion by 2030.

What is the current Asia-Pacific Pet Treats Market size?

In 2025, the Asia-Pacific Pet Treats Market size is expected to reach USD 6.65 billion.

Who are the key players in Asia-Pacific Pet Treats Market?

Colgate-Palmolive Company (Hill's Pet Nutrition Inc.), EBOS Group Limited, General Mills Inc., Mars Incorporated and Nestle (Purina) are the major companies operating in the Asia-Pacific Pet Treats Market.

Which segment has the biggest share in the Asia-Pacific Pet Treats Market?

In the Asia-Pacific Pet Treats Market, the Dogs segment accounts for the largest share by pets.

Which country has the biggest share in the Asia-Pacific Pet Treats Market?

In 2025, China accounts for the largest share by country in the Asia-Pacific Pet Treats Market.

What years does this Asia-Pacific Pet Treats Market cover, and what was the market size in 2025?

In 2025, the Asia-Pacific Pet Treats Market size was estimated at 6.65 billion. The report covers the Asia-Pacific Pet Treats Market historical market size for years: 2017, 2018, 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Asia-Pacific Pet Treats Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Asia-Pacific Pet Treats Market Research

Mordor Intelligence provides a comprehensive analysis of the pet treats market, focusing on the biggest pet market in Asia. Our extensive research covers the rapidly expanding pet snacks and treats industry. This includes a detailed examination of pet rewards systems and various product categories from Asian pet shop networks. The report offers an in-depth analysis of emerging segments, such as freeze dried treats for pets, and regional developments, including the Malaysian dog treats sector.

Stakeholders can access detailed insights through our report PDF, available for download. It examines various segments, including pet snacks and specialty items. The analysis covers emerging trends in pet treats distribution, consumer behavior patterns, and product innovations across the largest pet market in Asia. Our research methodology ensures stakeholders receive actionable intelligence about pet rewards programs and evolving consumer preferences in the Asia-Pacific pet treats landscape. This supports informed decision-making for market participants.