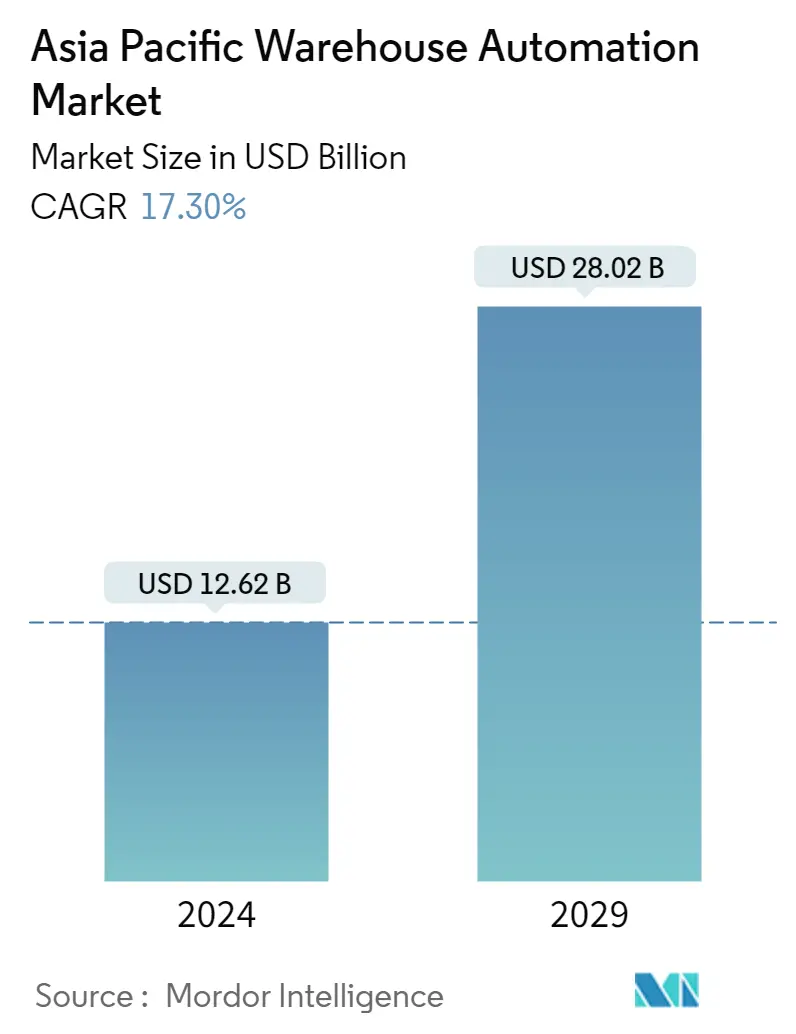

Market Size of Asia Pacific Warehouse Automation Industry

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

| Market Size (2024) | USD 12.62 Billion |

| Market Size (2029) | USD 28.02 Billion |

| CAGR (2024 - 2029) | 17.30 % |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

APAC Warehouse Automation Market Analysis

The Asia Pacific Warehouse Automation Market size is estimated at USD 12.62 billion in 2024, and is expected to reach USD 28.02 billion by 2029, growing at a CAGR of 17.30% during the forecast period (2024-2029).

The COVID-19 pandemic, which wreaked havoc on major economies such as China, Japan, and India, is predicted to impact future market growth. Significant investments are influencing the rise of roller conveyors in the Asia-Pacific in the e-commerce industry and demand from ever-increasing internet-enabled consumers.

Furthermore, with large investments in the industry, the manufacturing sector is predicted to account for a significant market share and become one of the country's major contributors. The requirement to deliver varied products in short durations has grown, necessitating efficient inventory management and reverse logistics systems.

- The expansion of the Asia-Pacific warehouse automation market is examined by looking at India, China, Australia, South Korea, Japan, and the rest of Asia. China, one of the world's major economies, is continually creating and deploying warehouse robots. China is expected to have a significant share in the market. As a result of the high automation rates, the presence of prominent vendors, and the widespread availability of warehouse robots, China's demand for warehouse robotics is significant.

- Due to the rise of the manufacturing, retail, and FMCG industries, there is an ever-increasing demand for industrial automation solutions across the APAC region. Shuttle retrieval systems, as well as automated storage and mobile robot platforms, are seeing a significant increase. Industrial and freight routes are sprouting up throughout the region, increasing the number of organized participants in the storage and industrial parks.

- Moreover, According to a 2022 study on warehouse vision conducted by Zebra Technologies, For the survey, more than 1,500 warehouse decision-makers and colleagues were polled from Australia, China, India, Japan, and Singapore. According to the survey, 27% of warehouse operators worldwide, including those in APAC, have already employed autonomous mobile robots (AMR). This ratio is expected to climb to 92% in APAC and 90% internationally in the next five years.

- While most warehouses will employ AMRs for P2G picking, material movements, and other automated inventory moves, more will invest in software that automates analytics and decision-making. In APAC, 95% of decision-makers expressed willingness to invest in such software to improve worker effectiveness and efficiency while lowering labor costs, slightly exceeding the global average (94%).

- Additionally, companies in the region are hurrying to adopt warehouse automation across the region in the wake of the COVID-19 outbreak. According to Mobile Industrial Robots in Shanghai, China, the company's autonomous robots that can transport pallets and large loads around warehouses and factories have seen growing demand across a wide range of industries. Airbus, Flex, Honeywell, and DHL are the major firms responsible for the rising demand.

APAC Warehouse Automation Industry Segmentation

The Asia Pacific warehouse automation market study involves segmentation by component wherein hardware (AGV/AMR, AS/AR, piece picking, etc.), software (warehouse management systems, warehouse execution systems), and services (value-added services, maintenance, etc.) sub-segments are being analyzed.

Further, the warehouses and fulfillment centers perform activities across end-users, such as food and beverages, post and parcel, apparel, general merchandise, and manufacturing, to name a few. The manufacturing industry majorly includes the automotive, electronics, and pharmaceutical sectors. The study also provides the impact of COVID-19 on the market studied.

| Component | ||||||||

| ||||||||

| Software (Warehouse Management Systems(WMS), Warehouse Execution Systems (WES)) | ||||||||

| Services (Value Added Services, Maintenance, etc.) |

| End-User | |

| Food and Beverage (Including Manufacturing Facilities and Distribution Centers) | |

| Post and Parcel | |

| Groceries | |

| General Merchandise | |

| Apparel | |

| Manufacturing (Durable and Non-Durable) | |

| Other End-user Industries |

| Country | |

| China | |

| India | |

| Japan | |

| Rest Asia-Pacific |

Asia Pacific Warehouse Automation Market Size Summary

The Asia Pacific warehouse automation market is experiencing significant growth, driven by the increasing demand for efficient logistics and inventory management solutions across various industries, including e-commerce, manufacturing, and retail. The region's rapid adoption of automation technologies is largely influenced by the need to streamline operations and reduce costs, particularly in countries like China, India, and Japan. The market is characterized by the deployment of advanced systems such as autonomous mobile robots (AMRs), automated guided vehicles (AGVs), and sophisticated software solutions that enhance decision-making and analytics. These technologies are pivotal in optimizing warehouse operations, improving supply chain efficiency, and meeting the demands of a growing internet-enabled consumer base.

The competitive landscape of the Asia Pacific warehouse automation market is moderately fragmented, with numerous global and regional players actively innovating and forming strategic partnerships to maintain their market positions. Companies like ST Engineering, Toshiba Global, and Daifuku Co., Ltd. are prominent in this space, contributing to the development and implementation of cutting-edge automation solutions. The market is also witnessing significant investments in infrastructure and technology, as seen in initiatives by major firms such as Amazon and DHL, which are expanding their automated warehouse capabilities. As the region continues to embrace automation, the market is poised for substantial growth, with a focus on enhancing operational efficiency and reducing logistical costs.

Asia Pacific Warehouse Automation Market Size - Table of Contents

-

1. MARKET INSIGHTS

-

1.1 Market Overview

-

1.2 Value Chain / Supply Chain Analysis

-

1.3 Industry Attractiveness -Porter's Five Forces Analysis

-

1.3.1 Threat of New Entrants

-

1.3.2 Bargaining Power of Buyers/Consumers

-

1.3.3 Bargaining Power of Suppliers

-

1.3.4 Threat of Substitute Products

-

1.3.5 Intensity of Competitive Rivalry

-

-

1.4 Industry Value Chain Analysis

-

1.5 Warehouse Investment Scenario

-

1.6 Impact of Macro-economic Factors on the Warehouse Automation Market

-

1.7 Impact of COVID-19 on the Market

-

-

2. MARKET SEGMENTATION

-

2.1 Component

-

2.1.1 Hardware

-

2.1.1.1 Mobile Robots (AGV, AMR)

-

2.1.1.2 Automated Storage and Retrieval Systems (AS/RS)

-

2.1.1.3 Automated Conveyor & Sorting Systems

-

2.1.1.4 De-palletizing/Palletizing Systems

-

2.1.1.5 Automatic Identification and Data Collection (AIDC)

-

2.1.1.6 Piece Picking Robots

-

-

2.1.2 Software (Warehouse Management Systems(WMS), Warehouse Execution Systems (WES))

-

2.1.3 Services (Value Added Services, Maintenance, etc.)

-

-

2.2 End-User

-

2.2.1 Food and Beverage (Including Manufacturing Facilities and Distribution Centers)

-

2.2.2 Post and Parcel

-

2.2.3 Groceries

-

2.2.4 General Merchandise

-

2.2.5 Apparel

-

2.2.6 Manufacturing (Durable and Non-Durable)

-

2.2.7 Other End-user Industries

-

-

2.3 Country

-

2.3.1 China

-

2.3.2 India

-

2.3.3 Japan

-

2.3.4 Rest Asia-Pacific

-

-

Asia Pacific Warehouse Automation Market Size FAQs

How big is the Asia Pacific Warehouse Automation Market?

The Asia Pacific Warehouse Automation Market size is expected to reach USD 12.62 billion in 2024 and grow at a CAGR of 17.30% to reach USD 28.02 billion by 2029.

What is the current Asia Pacific Warehouse Automation Market size?

In 2024, the Asia Pacific Warehouse Automation Market size is expected to reach USD 12.62 billion.