Market Overview

| Study Period | 2017 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 414.80 Million |

| Market Size (2030) | USD 549.90 Million |

| Growth Rate (2025 - 2030) | 5.80% CAGR |

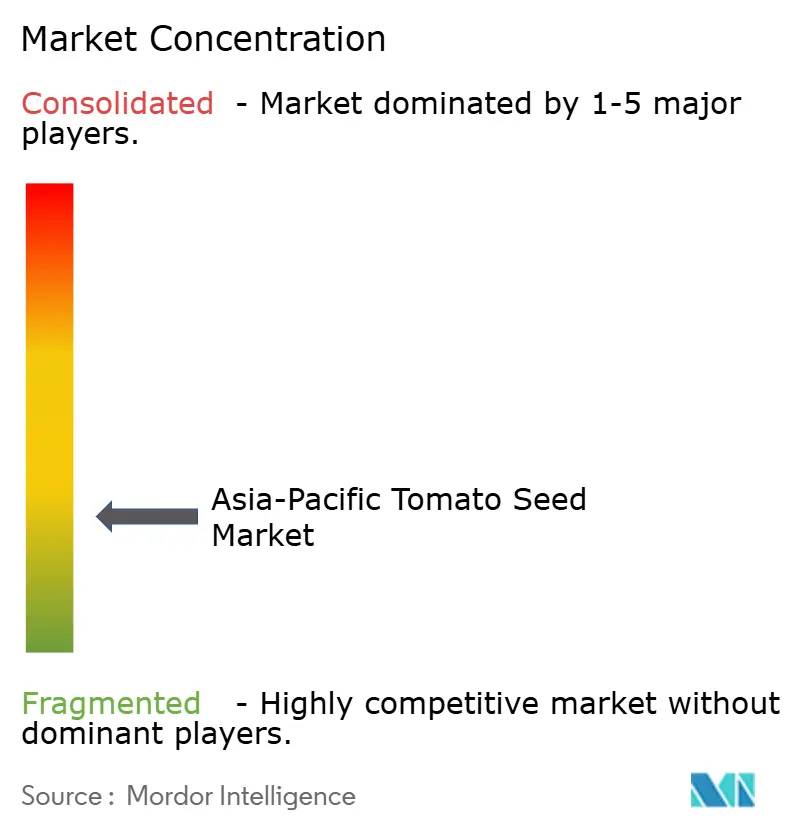

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Asia-Pacific Tomato Seed Market Analysis by Mordor Intelligence

The Asia-Pacific tomato seed market size reached USD 414.8 million in 2025 and is projected to advance at a 5.8% CAGR, lifting the value to USD 549.9 million by 2030. Hybrid breeding, protected cultivation adoption, and government subsidy programs remain the primary engines of growth across the region. China supplies more than half of the regional demand, yet India records the fastest expansion due to subsidy-backed contract farming networks. Processing-grade hybrids with high soluble-solids content draw price premiums and direct corporate sourcing, while salt-tolerant cultivars gain traction in coastal reclamation zones. The competitive landscape stays fragmented because local firms still command strong distribution links to smallholder farmers even as multinational breeders enlarge research pipelines for climate-resilient traits.

Key Report Takeaways

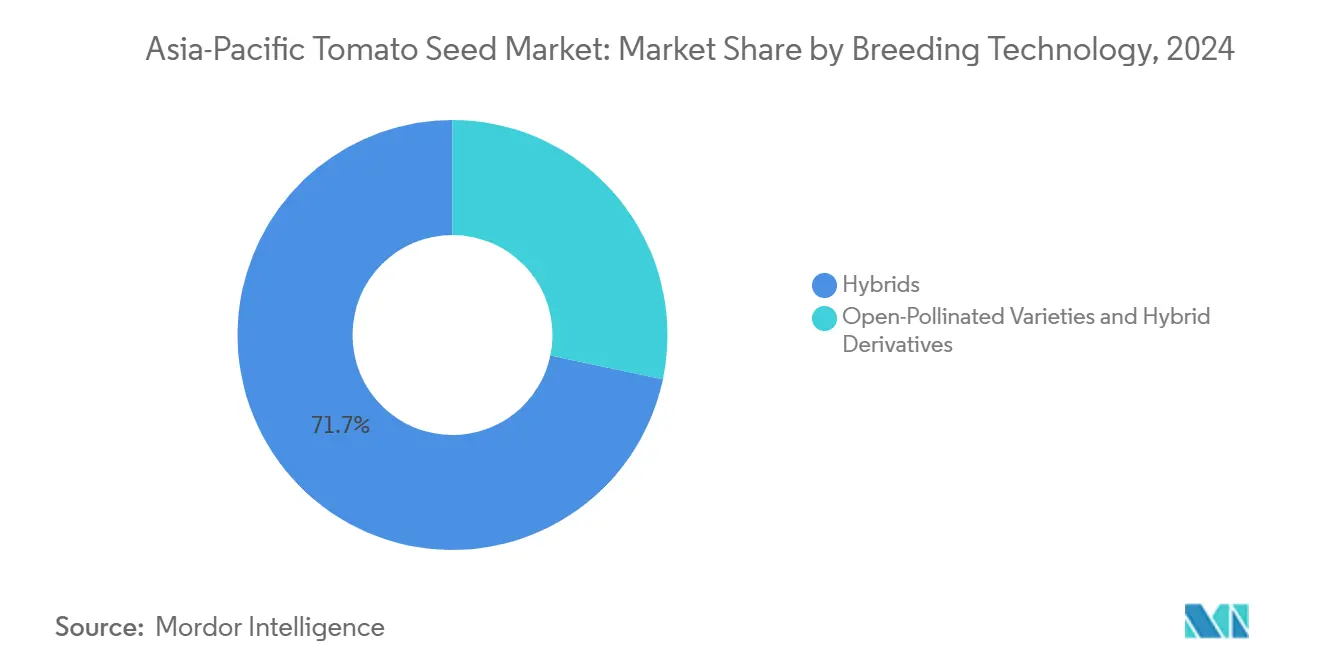

- By breeding technology, hybrids captured 71.7% of the Asia-Pacific tomato seed market share in 2024, and are projected to register a 5.9% CAGR between 2025 and 2030.

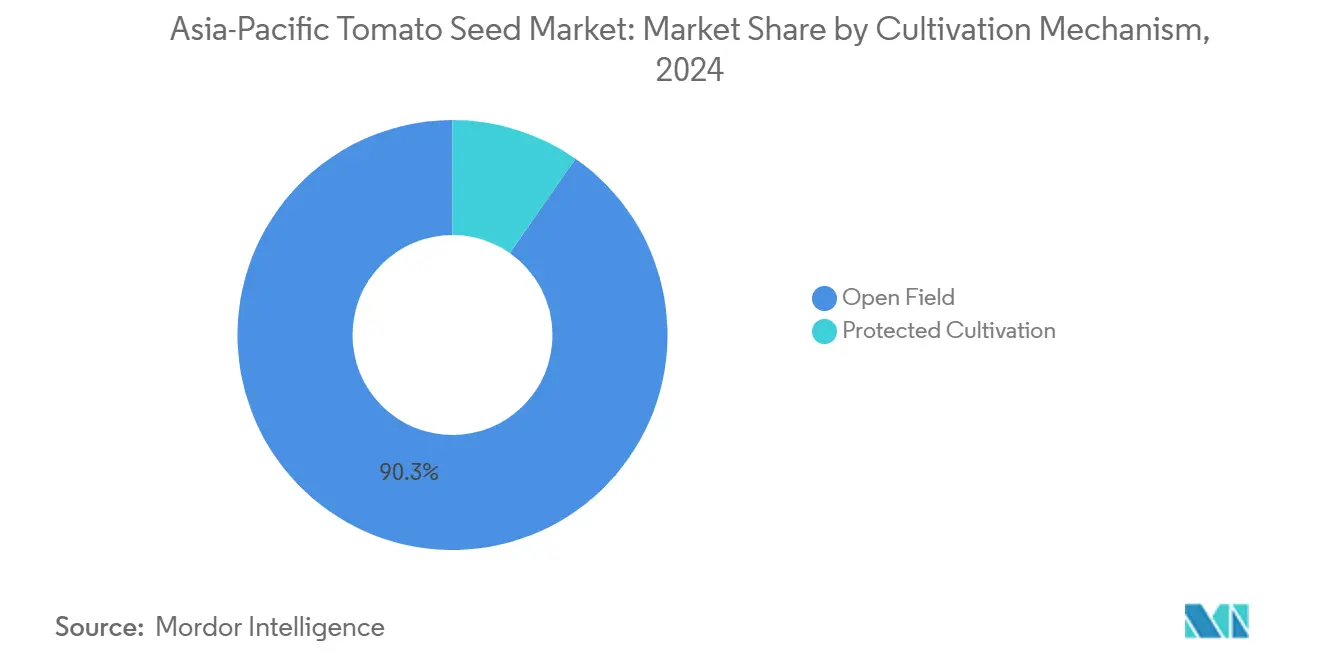

- By cultivation mechanism, open-field systems held 90.3% of the Asia-Pacific tomato seed market size in 2024, whereas protected cultivation acreage is projected to climb at a 7.7% CAGR to 2030.

- By geography, China controlled 50.8% of the Asia-Pacific tomato seed market share in 2024, while India is forecast to grow at a 7.4% CAGR and become the fastest-growing national segment.

- Sakata Seed Corporation, Rijk Zwaan, Bayer AG, Syngenta Group, and Groupe Limagrain together held nearly 31% of total sales in 2024, illustrating a fragmented structure.

Asia-Pacific Tomato Seed Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand from processed tomato industry | +1.2% | China, India, Thailand, and Vietnam | Medium term (2-4 years) |

| Expansion of protected cultivation acreage | +0.9% | Japan, South Korea, and urban zones Asia-Pacific | Long term (≥ 4 years) |

| Government hybrid-seed subsidy programs | +0.8% | India, China, Philippines, and Myanmar | Short term (≤ 2 years) |

| Surge in salt-tolerant seed demand for coastal reclamation | +0.6% | Bangladesh, Vietnam, and eastern India | Medium term (2-4 years) |

| Adoption of seed-priming services by contract nurseries | +0.4% | Thailand, Malaysia, and Indonesia | Short term (≤ 2 years) |

| Climate-resilient variety development | +0.3% | Typhoon-prone Asia-Pacific regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand from Processed Tomato Industry

Sauce, paste, and ketchup manufacturers in China and India now stipulate hybrid seeds that guarantee soluble-solids levels, uniform viscosity, and consistent color. Food processors in China (Shandong and Henan) and India (Maharashtra and Karnataka) lock in volume through contract farming structures that mandate certified hybrid varieties. Indian firms such as ITC and Nestle report that hybrid use boosted processing yields during the 2024 harvests. This direct sourcing model accelerates hybrid penetration, narrows cultivar requirements, and elevates pricing power for breeders offering high-brix lines. The trend reshapes regional seed demand toward processing traits rather than fresh-market attributes, reinforcing the centrality of hybrids within the Asia-Pacific tomato seed market. Ancillary service providers, grading, pulping, and cold storage, also scale up, creating an integrated ecosystem that locks growers into vertically organized supply chains.

Expansion of Protected Cultivation Acreage

Capital expenditure on greenhouses, net-houses, and vertical farms significant amount in 2024 across Asia-Pacific, with Japan and South Korea leading automation adoption. Chinese greenhouses expanded rapidly in peri-urban territories where land costs remain high, forcing growers to intensify production under controlled environments. Southeast Asian municipalities subsidize low-cost tunnel houses that cut input waste while boosting productivity, an initiative driven by Thailand's Royal Project Foundation. Protected systems demand compact, determinant, disease-resistant hybrids priced higher than open-field seeds, steering breeder R&D budgets toward greenhouse niches. Equipment suppliers offer bundled packages that incorporate climate sensors, fertigation, and LED lighting, thus reinforcing protected cultivation momentum within the Asia-Pacific tomato seed market.

Government Hybrid-Seed Subsidy Programs

India’s National Mission for Sustainable Agriculture disbursed INR 420 crores (USD 50.4 million) during 2024 to subsidize hybrid vegetable seeds for 2.3 million smallholders.[1]Source: Ministry of Agriculture and Farmers Welfare, “Hybrid Seed Subsidy Programs,” agricoop.gov.in China’s rural revitalization grants reimburse 60% of certified hybrid purchase costs, driving adoption above 85% within cooperative networks across Shandong and Henan. The Philippines expanded its hybrid vegetable program to cover tomatoes, reimbursing up to 75% of seed costs for growers under contract farming schemes.[2]Source: Department of Agriculture, Philippines, “Hybrid Vegetable Program,” da.gov.ph These incentives diminish financial barriers, intensify hybrid uptake, and lift overall seed replacement rates from biennial to annual cycles. Implementation gaps persist in remote tracts where extension services remain sparse, yet the cumulative effect on the Asia-Pacific tomato seed market remains positive.

Surge in Salt-Tolerant Seed Demand for Coastal Reclamation

Bangladesh targets 1.2 million hectares of reclaimed coastline for horticulture by 2030, stipulating salt-tolerant seed certificates within subsidy frameworks.[3]Source: Bangladesh Agricultural Research Institute, “Coastal Agriculture Research,” bari.gov.bd Vietnamese Mekong Delta producers achieve significant yield improvements when switching to hybrids tolerant of high soil salinity, enabling shrimp farmers to diversify into tomato production under integrated systems. Eastern Indian states impose similar certification norms, supporting premium price realization for breeders achieving defined salinity thresholds. Research and development outlays increase because salinity tolerance involves multigenic traits, yet the resulting market niche commands higher margins and secures long-term demand. This specialist demand channel differentiates competitive offerings inside the Asia-Pacific tomato seed market and encourages public–private breeding collaborations.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Climate-change-driven yield volatility | –0.7% | Monsoon-dependent Asia-Pacific zones | Medium term (2-4 years) |

| Price sensitivity among smallholders | –0.5% | India, Bangladesh, Myanmar, and rural China | Short term (≤ 2 years) |

| Counterfeit seed infiltration in tier-2 markets | –0.4% | Pakistan, rural China, and northern India | Medium term (2-4 years) |

| Limited cold-chain for high-value hybrid seeds | –0.3% | Remote islands and upland Asia-Pacific areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Climate-Change-Driven Yield Volatility

El Niño-Southern Oscillation cycles significantly reduced tomato yields across critical Asia-Pacific regions during recent seasons, with the Philippines and Bangladesh experiencing acute heat stress and irregular rainfall. Chinese meteorological stations logged frequent temperature spikes during flowering, causing pollen sterility and fruit-set loss. These stresses inflict revenue volatility on growers, spur breeder emphasis on heat-tolerant alleles, and elevate risk management costs. Although climate-resilient hybrids are in the pipeline, commercial release requires multiple growing seasons, leaving near-term exposure high. Insurance uptake rises along with interest in protected cultivation, illustrating systemic adaptation within the Asia-Pacific tomato seed market.

Price Sensitivity Among Smallholders

Smallholders with minimal landholdings in India reduce hybrid uptake when seed expenditures exceed a small portion of projected revenue. Pakistani growers revert to saved seed whenever hybrid prices exceed certain thresholds, constraining commercial seed circulation. Rural Chinese cooperatives report resistance to premium lines if price gaps widen significantly relative to local standards. Breeders answer through mid-tier hybrids that trade some performance for affordability, yet the price sensitivity still curbs penetration in subsistence belts. Persistent price tension underscores the fragmented demand landscape inside the Asia-Pacific tomato seed market.

Segment Analysis

By Breeding Technology: Hybrid Dominance Accelerates Processing Adoption

Hybrids secured 71.7% of the Asia-Pacific tomato seed market size in 2024, a testament to processor specifications that require uniformity, firmness, and shelf life. Processing companies in China stipulate hybrids exceeding 5.5% soluble solids, raising demand for high-brix genetics. The Asia-Pacific tomato seed market share for hybrids is projected to climb as the segment posts a 5.9% CAGR through 2030, while open-pollinated varieties inch forward mainly in Myanmar and rural Bangladesh, where seed saving habits persist. Historical growth signaled rapid conversion. The slowing yet robust forecast illustrates maturation in advanced economies alongside continuing room for expansion in emerging geographies. Japanese breeders promote compact greenhouse hybrids carrying multiple virus-resistance genes that command premium prices. Regulatory frameworks in Australia and New Zealand mandate stringent variety registration, tilting commercial advantage toward global firms with extensive trial data. Consequently, product pipelines now concentrate on differentiated niche traits, sustaining hybrid preeminence inside the Asia-Pacific tomato seed market.

Open-pollinated varieties nevertheless retain cultural value in community seed systems and low-input farms. Vietnamese cooperatives, after evaluating demonstration plots, reported increased hybrid usage in recent years, confirming substantial yield gains under identical management. Myanmar's delta region still favors open-pollinated seeds because labor-intensive saved-seed practices reduce cash outlay, yet rising off-season prices for tomatoes motivate younger farmers to experiment with hybrids. Regional NGOs collaborate with public institutes to introduce hybrid derivatives, aiming to merge affordability with partial performance advances. The Asia-Pacific tomato seed market thus stages a gradual yet irreversible pivot toward hybrid dominance, powered by both industrial demand and grower economics.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Cultivation Mechanism: Protected Systems Drive Technology Adoption

Open-field production occupied 90.3% of the Asia-Pacific tomato seed market size in 2024, still reflecting vast rural acreage. Yet protected systems are expanding at a 7.7% CAGR through 2030, propelled by urban land scarcity and consumer preference for blemish-free produce. South Korean vertical farms utilize stacked hydroponic modules to supply premium supermarkets, increasing annual output per square meter by up to 15-fold. Greenhouse operators near Shanghai and Beijing allocate space for cherry tomatoes that command prices 2-3 times higher than field-grown varieties, offsetting increased seed costs. Seed companies develop indeterminate, cluster-fruit varieties specifically for high wire systems, establishing a protected-cultivation segment within the Asia-Pacific tomato seed market.

Greenhouse construction investments reached USD 1.8 billion in 2024, ranging from Thai highland bamboo-frame tunnels at USD 8-12 per square meter for rain protection to advanced facilities. Indonesian greenhouse operators report 40-60% higher yields in climate-controlled environments, enabling off-season production and premium pricing. Philippine growers combine organic certification with protected cultivation to access Japanese and Singaporean export markets. While Singapore implements strict structural requirements, Laos maintains minimal regulatory oversight. This varied landscape has prompted the Asia-Pacific tomato seed market to focus research and development on protected-environment hybrids, supporting the expansion of controlled cultivation systems.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

China dominated the Asia-Pacific tomato seed market with a 50.8% share in 2024, sustained by sprawling processing clusters in Xinjiang and Inner Mongolia and hybrid adoption rates now topping 78% in core provinces. Processing acreage expanded significantly yearly, demanding substantial volumes of high-brix seed, while greenhouse installations in peri-urban belts accelerate due to land conversion pressures. The historical strong growth from the early to mid-2020s is poised to moderate in the coming years through the end of the decade, reflecting saturation in well-served districts yet continued uptake in western frontiers.

India registers the fastest trajectory at a 7.4% CAGR as hybrid subsidies widen and food processors in Maharashtra, Karnataka, and Andhra Pradesh lock in contract acreage. Processing acreage continues to expand significantly each year, demanding substantial volumes of high-brix seed, while greenhouse installations in peri-urban belts accelerate due to land conversion pressures. The market growth rate experienced in recent years is projected to moderate in the coming period, reflecting saturation in well-served districts yet continued uptake in western frontiers.

Southeast Asia, comprising Thailand, Vietnam, and Indonesia, represents a significant portion of regional demand, showing steady growth potential in the forecast period. Thailand's highland projects merge greenhouse production with tourism, while Vietnam's Mekong Delta integrates salt-tolerant lines into diversified aquaculture farms. Indonesian peri-urban horticulture benefits from rising disposable income and online grocery growth, stimulating the adoption of disease-resistant hybrids to ensure consistent quality. Japan and Australia, despite their mature status, supply premium segments: greenhouse tomatoes for sushi outlets in Tokyo and organic-certified lines for boutique grocers in Sydney. These markets show modest expansion, yet their higher price points elevate overall revenue in the Asia-Pacific tomato seed market.

Competitive Landscape

Fragmentation defines the Asia-Pacific tomato seed market: the leading five firms control only 31% of total sales, underscoring room for consolidation. Sakata Seed Corporation maintains market leadership through heat-tolerant cherry varieties suited for subtropical greenhouses. Rijk Zwaan holds a significant market share by supplying high-brix hybrids popular among Chinese sauce manufacturers. Yuan Longping High-Tech Agriculture invests substantially in new marker-assisted breeding facilities to compress product cycle times. Syngenta Group acquired Asia Seed in Thailand to deepen ASEAN distribution, while East-West Seed unveiled processing hybrids tuned to Indian contracts.

Technology investment forms the strategic fulcrum. Bayer expanded its Beijing vegetable R&D hub, focusing on CRISPR-enabled greenhouse varieties. Start-ups affiliated with regional universities exploit indigenous germplasm to breed cultivars tailored to narrow microclimates, gaining footholds in niche segments. Market access hinges on national certification regimes that impose multilocation trials. Established multinationals wield superior compliance resources, reinforcing barriers against smaller firms. Despite such hurdles, white-space opportunities in salt tolerance, heat resilience, and seed priming invite new entrants and joint ventures, ensuring the Asia-Pacific tomato seed market remains dynamic.

Government efforts to stamp out counterfeit seed accelerate formalization, aiding reputable brands. Digital platforms for seed traceability are progress in China and India, allowing farmers to verify authenticity via QR codes. Partnerships between seed companies and logistics providers aim to extend cold-chain coverage, safeguarding the viability of high-value hybrids during transit to remote districts. As market players expand service portfolios, technical advisories, micro-loans, and buy-back guarantees, they seek differentiation beyond genetics alone, a trend likely to reshape competition in the coming years.

Asia-Pacific Tomato Seed Industry Leaders

-

Bayer AG

-

Syngenta Group

-

Rijk Zwaan Zaadteelt en Zaadhandel B.V.

-

Groupe Limagrain

-

Sakata Seed Corporation

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- June 2025: East-West Seed Thailand introduced tomato varieties designed for local farmers, featuring enhanced yield potential, disease resistance, and adaptation to regional growing conditions. The new varieties aim to increase productivity and profitability for Thailand's vegetable farmers.

- April 2025: Bangladesh Agricultural University researchers developed 'BAU Beefsteak Tomato-1', a tomato variety characterized by large size, sweet taste, and high nutrient content. The variety is suitable for burger production and commercial farming due to its high yield potential. The tomato demonstrates natural pest resistance, eliminating the need for pesticides, and maintains freshness for 15-20 days at room temperature.

- March 2025: Bihar Agriculture University scientists have developed a seedless tomato variety using gamma radiation-induced mutagenesis. The new variety features increased pulp content and extended shelf life. While this development has potential applications in vegetable farming and food processing industries, the lack of seeds presents propagation challenges.

Asia-Pacific Tomato Seed Market Report Scope

Hybrids, Open Pollinated Varieties & Hybrid Derivatives are covered as segments by Breeding Technology. Open Field, Protected Cultivation are covered as segments by Cultivation Mechanism. Australia, Bangladesh, China, India, Indonesia, Japan, Myanmar, Pakistan, Philippines, Thailand, Vietnam are covered as segments by Country.

Breeding Technology

| Hybrids |

| Open Pollinated Varieties & Hybrid Derivatives |

Cultivation Mechanism

| Open Field |

| Protected Cultivation |

Country

| Australia |

| Bangladesh |

| China |

| India |

| Indonesia |

| Japan |

| Myanmar |

| Pakistan |

| Philippines |

| Thailand |

| Vietnam |

| Rest of Asia-Pacific |

| Breeding Technology | Hybrids |

| Open Pollinated Varieties & Hybrid Derivatives | |

| Cultivation Mechanism | Open Field |

| Protected Cultivation | |

| Country | Australia |

| Bangladesh | |

| China | |

| India | |

| Indonesia | |

| Japan | |

| Myanmar | |

| Pakistan | |

| Philippines | |

| Thailand | |

| Vietnam | |

| Rest of Asia-Pacific |

Need A Different Region or Segment?

Customize Now

Market Definition

- Commercial Seed - For the purpose of this study, only commercial seeds have been included as part of the scope. Farm-saved Seeds, which are not commercially labeled are excluded from scope, even though a minor percentage of farm-saved seeds are exchanged commercially among farmers. The scope also excludes vegetatively reproduced crops and plant parts, which may be commercially sold in the market.

- Crop Acreage - While calculating the acreage under different crops, the Gross Cropped Area has been considered. Also known as Area Harvested, according to the Food & Agricultural Organization (FAO), this includes the total area cultivated under a particular crop across seasons.

- Seed Replacement Rate - Seed Replacement Rate is the percentage of area sown out of the total area of crop planted in the season by using certified/quality seeds other than the farm-saved seed.

- Protected Cultivation - The report defines protected cultivation as the process of growing crops in a controlled environment. This includes greenhouses, glasshouses, hydroponics, aeroponics, or any other cultivation system that protects the crop against any abiotic stress. However, cultivation in an open field using plastic mulch is excluded from this definition and is included under open field.

| Keyword | Definition |

|---|---|

| Row Crops | These are usually the field crops which include the different crop categories like grains & cereals, oilseeds, fiber crops like cotton, pulses, and forage crops. |

| Solanaceae | These are the family of flowering plants which includes tomato, chili, eggplants, and other crops. |

| Cucurbits | It represents a gourd family consisting of about 965 species in around 95 genera. The major crops considered for this study include Cucumber & Gherkin, Pumpkin and squash, and other crops. |

| Brassicas | It is a genus of plants in the cabbage and mustard family. It includes crops such as carrots, cabbage, cauliflower & broccoli. |

| Roots & Bulbs | The roots and bulbs segment includes onion, garlic, potato, and other crops. |

| Unclassified Vegetables | This segment in the report includes the crops which don’t belong to any of the above-mentioned categories. These include crops such as okra, asparagus, lettuce, peas, spinach, and others. |

| Hybrid Seed | It is the first generation of the seed produced by controlling cross-pollination and by combining two or more varieties, or species. |

| Transgenic Seed | It is a seed that is genetically modified to contain certain desirable input and/or output traits. |

| Non-Transgenic Seed | The seed produced through cross-pollination without any genetic modification. |

| Open-Pollinated Varieties & Hybrid Derivatives | Open-pollinated varieties produce seeds true to type as they cross-pollinate only with other plants of the same variety. |

| Other Solanaceae | The crops considered under other Solanaceae include bell peppers and other different peppers based on the locality of the respective countries. |

| Other Brassicaceae | The crops considered under other brassicas include radishes, turnips, Brussels sprouts, and kale. |

| Other Roots & Bulbs | The crops considered under other roots & bulbs include Sweet Potatoes and cassava. |

| Other Cucurbits | The crops considered under other cucurbits include gourds (bottle gourd, bitter gourd, ridge gourd, Snake gourd, and others). |

| Other Grains & Cereals | The crops considered under other grains & cereals include Barley, Buck Wheat, Canary Seed, Triticale, Oats, Millets, and Rye. |

| Other Fibre Crops | The crops considered under other fibers include Hemp, Jute, Agave fibers, Flax, Kenaf, Ramie, Abaca, Sisal, and Kapok. |

| Other Oilseeds | The crops considered under other oilseeds include Ground nut, Hempseed, Mustard seed, Castor seeds, safflower seeds, Sesame seeds, and Linseeds. |

| Other Forage Crops | The crops considered under other forages include Napier grass, Oat grass, White clover, Ryegrass, and Timothy. Other forage crops were considered based on the locality of the respective countries. |

| Pulses | Pigeon peas, Lentils, Broad and horse beans, Vetches, Chickpeas, Cowpeas, Lupins, and Bambara beans are the crops considered under pulses. |

| Other Unclassified Vegetables | The crops considered under other unclassified vegetables include Artichokes, Cassava Leaves, Leeks, Chicory, and String beans. |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases, and Subscription Platforms

Get More Details On Research Methodology

Download PDF