Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 0.96 Billion |

| Market Size (2030) | USD 1.43 Billion |

| Growth Rate (2025 - 2030) | 8.25% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Asia-Pacific Sodium Reduction Agents Market Analysis by Mordor Intelligence

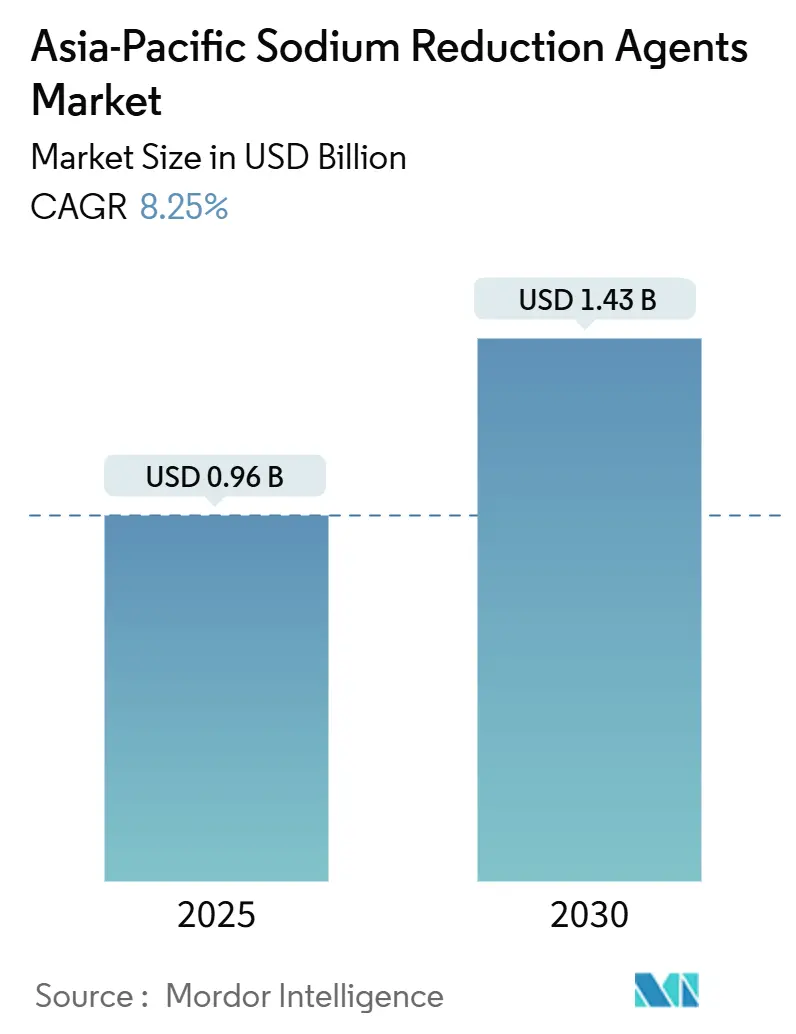

In 2025, the Asia-Pacific sodium reduction agents market is set to be valued at USD 0.96 billion, with projections indicating a rise to USD 1.43 billion by 2030, marking an 8.25% CAGR. This growth is bolstered by stringent enforcement of reformulation deadlines, a significant hypertension challenge in the region, and a swift adoption of potassium-based mineral salts alongside yeast-derived umami platforms. While China spearheads revenue generation, South Korea is witnessing the most rapid growth, driven by tightening sodium regulations on packaging. Innovations such as taste-masking peptides, economical nucleotide blends, and combined texture-plus-salt-replacement solutions are breaking sensory barriers, expanding their application in bakery, dairy, and ready-to-eat products. However, challenges persist with securing potassium chloride supplies and the intricate task of reformulating instant noodles and fermented condiments.

Key Report Takeaways

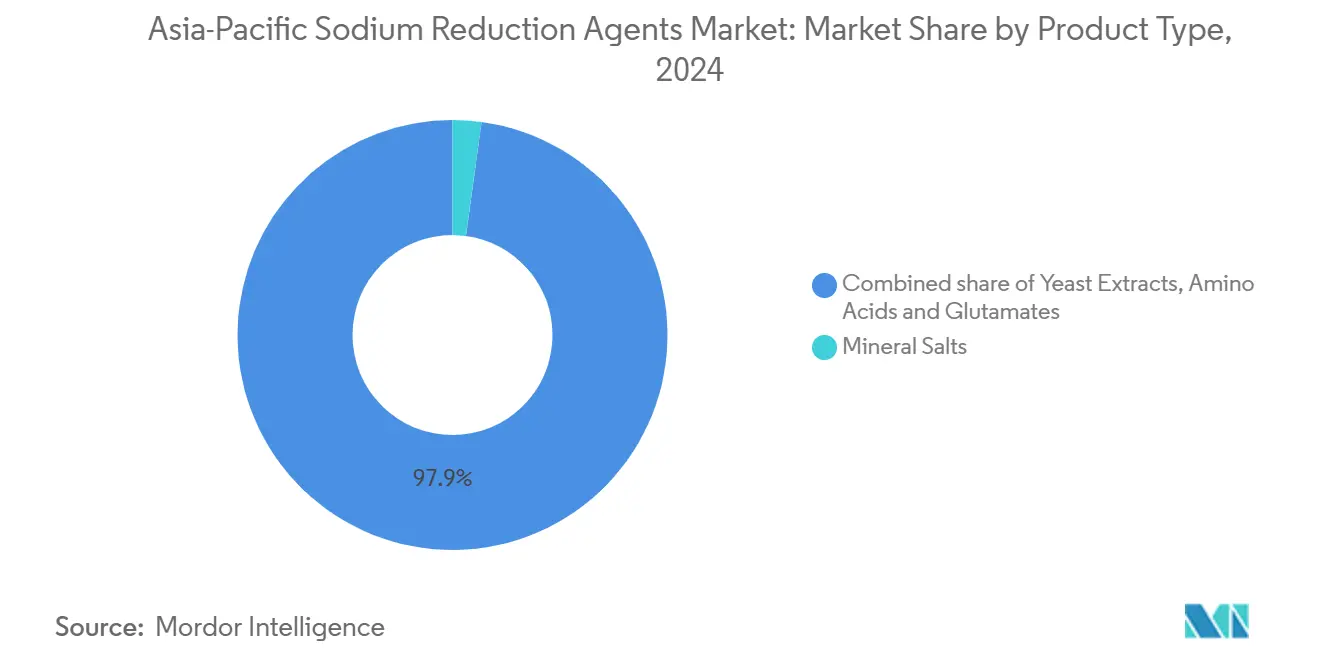

- By product type, mineral salts commanded 68.71% of revenue in 2024; yeast extracts are tracking an 8.74% CAGR to 2030.

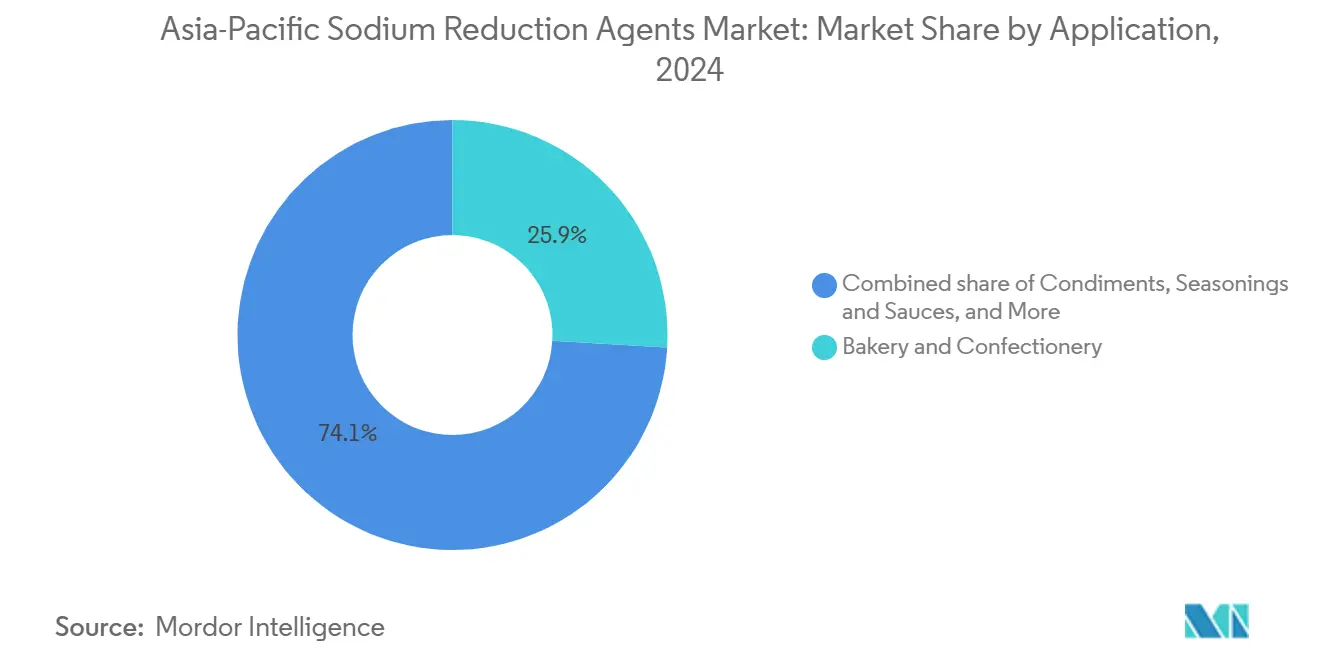

- By application, bakery and confectionery contributed 25.92% of sales in 2024; dairy and frozen foods are advancing at a 10.53% CAGR through 2030.

- By geography, China held 36.41% of 2024 value while South Korea is forecast to post a 9.31% CAGR to 2030.

Asia-Pacific Sodium Reduction Agents Market Trends and Insights

Driver Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising health consciousness among consumers drives demand for low-sodium food products | +1.8% | Global, with strongest uptake in Japan, South Korea, Singapore | Medium term (2-4 years) |

| Stringent government regulations and national salt reduction frameworks | +2.1% | China, Japan, South Korea, Thailand, Australia | Short term (≤ 2 years) |

| Increasing prevalence of diet-related diseases such as hypertension and cardiovascular issues | +1.5% | India, Indonesia, China | Long term (≥ 4 years) |

| Technological advancements enable development of innovative, palatable sodium replacers | +1.3% | Japan, South Korea, Singapore, Australia | Medium term (2-4 years) |

| Rising demand for processed and convenience foods requires sodium reduction in high-sodium staples | +1.0% | China, India, Indonesia, Thailand | Medium term (2-4 years) |

| Intensified R&D investments lead to novel, cost-effective, naturally derived sodium reduction agents | +0.9% | Global, with R&D hubs in Japan, South Korea, Singapore | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Health Consciousness Among Consumers Drives Demand for Low-Sodium Food Products

Awareness of sodium's health risks is rising across Asia-Pacific, especially in urbanized and aging regions. In Japan, men consume 10.8 grams of salt daily on average, while women consume 9.2 grams, according to the National Health and Nutrition Survey[1]National Health and Nutrition Survey (NHNS), "The National Health and Nutrition Survey (NHNS) Japan", nibn.go.jp. To address this, the Ministry of Health set a 6.0-gram daily target for individuals with hypertension or kidney disease under the 2020 Dietary Reference Intakes framework. In 2022, Japan launched an initiative urging food manufacturers to reformulate staples like soy sauce, miso soup, and pickled vegetables, which contribute 40% of household sodium intake. Similarly, in 2024, Singapore tightened sodium limits for ready-to-eat meals and condiments under its Healthier Choice Symbol program, complementing the Nutri-Grade beverage labeling system introduced in late 2023. These measures reflect a growing trend of consumers favoring low-sodium products with government endorsements, giving early reformulators a competitive edge.

Stringent Government Regulations and National Salt Reduction Frameworks

Salt reduction frameworks in the Asia-Pacific region have shifted from voluntary guidelines to enforceable standards. China's GB 2760-2024 food additive standard, effective February 2025, sets limits for potassium chloride, potassium lactate, and glutamate-based flavor enhancers. Additionally, 2024 guidelines promote low-sodium salt with clinical benchmarks for processed food substitution. Thailand's National Salt Reduction Strategy (2016–2025) requires sodium labeling on packaged foods and introduced the "Healthier Choice" logo to encourage reformulation, aiming to cut daily sodium intake from 10.8 grams to 5 grams. Australia's Healthy Food Partnership targets a 10% sodium reduction by 2020 and 25% by 2025 across 30+ food categories. Food Standards Australia New Zealand will review nutrition content and health claims in December 2024 under proposal P1050 to align labeling with reformulation progress[2]Food Standards Australia New Zealand, "FSANZ Board communique: 11 December 2024 meeting", foodstandards.gov.au. In South Korea, the Ministry of Food and Drug Safety plans October 2025 amendments to expand reduced-sodium labeling eligibility, tightening the Food Labeling Act. These regulations shorten product development timelines and highlight the need for sodium reduction agents that match the taste of traditional formulations.

Increasing Prevalence of Diet-Related Diseases Such as Hypertension and Cardiovascular Issues

Hypertension has reached epidemic levels in the Asia-Pacific region. Indonesia leads with the highest prevalence, while India reports a staggering 220 million cases. This surge coincides with daily sodium intakes in these countries that are roughly double the World Health Organization's (WHO) recommended limit of 5 grams. The WHO's HEARTS initiative, aimed at managing cardiovascular diseases, highlights sodium reduction as a top-tier intervention. They project that if the population's salt intake is reduced by 30%, millions of premature deaths could be prevented in the region. Genetic factors make Asian populations more sensitive to salt, intensifying their blood pressure response to dietary sodium. This sensitivity underscores the cost-effectiveness of reformulation efforts in public health. In July 2024, India's Food Safety and Standards Authority took a significant step by requiring bolder, larger font sizes for sodium content on packaged foods. Healthcare associations believe this move will boost consumer demand for low-sodium products. Given the economic toll of hypertension-related issues like strokes and renal failures, governments are now prioritizing sodium reduction in their health agendas. This focus has led to a consistent demand for agents that facilitate reformulation without diminishing product appeal.

Technological Advancements Enable Development of Innovative, Palatable Sodium Replacers

Taste-masking technologies have advanced to eliminate the bitter and metallic notes of potassium chloride, enabling broader use in dairy, bakery, and savory snacks. Kerry Group's TasteSense Salt platform uses mineral salts and umami peptides from enzymatic hydrolysis to cut sodium by up to 50% in bakery and snack products while maintaining saltiness. Givaudan's TasteSolutions, with its fermentation facility in Singapore, produces yeast extracts and nucleotide blends tailored to regional flavors, helping reformulate soy and fish sauces where sodium chloride is key for flavor and preservation. Ajinomoto's Smart Salt Project in Japan uses monosodium glutamate and disodium inosinate to boost umami, allowing a 20%-30% sodium reduction without affecting taste. The European Food Safety Authority's 2024 review confirmed potassium chloride (E508) is safe at current use levels, encouraging its adoption in markets influenced by EFSA regulations. These innovations reduce reformulation risks for manufacturers, especially in high-demand categories where consumer acceptance is critical.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory compliance hurdles | -0.7% | China, India, Indonesia, Thailand | Short term (≤ 2 years) |

| Supply chain limitations | -0.5% | Global, with acute pressure in Indonesia, Thailand | Medium term (2-4 years) |

| Technical formulation challenges | -0.6% | Global, particularly in fermented and high-moisture products | Medium term (2-4 years) |

| Substitutes can negatively impact food texture, reducing product appeal | -0.4% | Japan, South Korea, Australia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Regulatory Compliance Hurdles

Ingredient suppliers and food manufacturers face significant time and cost burdens due to divergent food additive regulations across Asia-Pacific jurisdictions. In China, the GB 26687-2011 standard mandates separate approvals for multi-component sodium reduction blends. This requirement delays the market entry of formulations that integrate potassium chloride, yeast extracts, and amino acids into a single ingredient system. Meanwhile, Indonesia's BPOM Regulation No. 11 of 2019 sets maximum use levels for individual food additives. However, it lacks clear guidance on synergistic blends. As a result, manufacturers are compelled to submit case-by-case applications, extending product development timelines by 6 to 12 months. In India, the Food Safety and Standards Act of 2006 requires licensing and registration for food additive manufacturers[3]Food Safety and Standards Authority of India. "Sodium Labeling Requirements." fssai.gov.in. However, inconsistent enforcement across states creates uncertainty for regional producers aiming to expand distribution. Thailand's FDA imposes additional challenges by mandating Thai-language labeling and pre-market notification for imported sodium reduction agents. This requirement complicates logistics for multinational suppliers. Such regulatory fragmentation not only slows the adoption of novel agents but also advantages incumbents. These established players possess regulatory affairs teams adept at navigating multi-country submissions.

Technical Formulation Challenges

Sodium chloride serves critical functions in food systems, including flavor enhancement, microbial control, protein solubilization, and water activity regulation, making substitution complex. Potassium chloride can replace up to 30% of sodium chloride in cheese and processed meats, but higher levels cause bitter and metallic flavors that consumers reject. Yeast extracts add umami but lack sodium chloride's antimicrobial properties, requiring changes to preservation systems in ready-to-eat meals and fermented condiments to maintain shelf life. In bakery products, sodium chloride strengthens gluten and controls fermentation, while substitutes weaken dough, reducing loaf volume and creating a coarser texture. In dairy and frozen desserts, potassium-based agents affect freezing points and ice crystal formation, compromising the smooth texture of premium ice cream. These challenges demand extensive testing, increasing reformulation time and the risk of consumer rejection.

Segment Analysis

By Product Type: Mineral Salts Dominate Through Regulatory Acceptance

In 2024, mineral salts accounted for 68.71% of product-type revenue, buoyed by potassium chloride's regulatory nods from Food Standards Australia New Zealand, China's GB 2760-2024, and South Korea's Food Additive Code. Potassium chloride, adept at substituting up to 30% of sodium chloride in cheese, processed meats, and baked goods—without the bitter off-notes when paired with umami enhancers—has emerged as the go-to for manufacturers racing to meet national sodium reduction targets. Jungbunzlauer's potassium citrate and potassium lactate formulations tackle taste-masking in dairy and frozen desserts, countering the metallic notes potassium chloride can introduce. In May 2024, Corbion teamed up with IMCD Thailand, amplifying the reach of potassium lactate blends among Southeast Asian processed meat producers, aligning with the region's surging appetite for shelf-stable, reduced-sodium protein products. Despite some technical constraints, the segment's lead endures, as regulatory knowledge and cost advantages eclipse the sensory benefits offered by yeast extracts and amino acids in budget-conscious markets.

Yeast extracts, poised to grow at a brisk 8.74% CAGR through 2030, are favored for their umami punch without the bitter aftertaste linked to heavy potassium chloride use. Angel Yeast's LA00 formulation, with under 2% sodium chloride, caters to the clean-label sodium reduction trend, supplying 10,000 metric tons monthly to food makers in China, Japan, and Southeast Asia for products like soy sauce and instant noodles. Biospringer, a Lesaffre subsidiary, bolstered its yeast extract production in Asia-Pacific, aiding the reformulation of high-sodium condiments where sodium chloride plays a dual role of flavor and preservation. Givaudan's PrimeLake fermentation facility in Singapore, launched in 2020, crafts nucleotide-rich yeast extracts attuned to local tastes, allowing a 20% to 30% sodium cut in fish and oyster sauces without sacrificing flavor. This segment's ascent underscores a shift towards naturally sourced, label-friendly ingredients, as urban Asia-Pacific consumers grow wary of synthetic additives.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Application: Dairy and Frozen Foods Accelerate Amid Texture Preservation Breakthroughs

Dairy and frozen foods are the fastest-growing application segment, with a 10.53% CAGR through 2030. Manufacturers have addressed texture preservation issues that previously hindered sodium reduction in cheese, ice cream, and frozen desserts. Potassium chloride can replace up to 30% of sodium chloride in cheese without causing bitter flavors. For higher substitution, blends of potassium lactate and citrate are used to mask metallic tastes and maintain protein solubility. Corbion's Verdad Opti Powder N70, launched in 2017 and gaining traction in 2024, combines potassium lactate with buffering agents to preserve the smooth texture and freezing properties essential for premium ice cream. Yeast extracts enhance umami flavors in processed cheese and cheese-flavored snacks, enabling a 20%-30% sodium reduction while maintaining savory notes. Japan's Ministry of Health, Labour and Welfare has prioritized dairy reformulation under the Health Japan 21 initiative, aiming to reduce daily salt intake to 7 grams by 2032. This segment's growth is driven by regulatory demands, consumer interest in healthier indulgent products, and advancements in sodium reduction technologies.

Bakery and confectionery accounted for 25.92% of application revenue in 2024, supported by high production volumes and the feasibility of mineral salt substitution in leavened systems. Kerry Group's TasteSense Salt platform enables up to 50% sodium reduction in bakery and snack products by combining potassium chloride with umami peptides, enhancing saltiness perception without affecting dough strength or fermentation. Japan's Japanese Society of Hypertension reported a sodium reduction of 9,678 metric tons across 292 products by 2023, with bakery goods contributing significantly. Australia's Healthy Food Partnership set a 25% sodium reduction target for bread and bakery products by 2025, prompting reformulation by suppliers. Sodium chloride strengthens gluten and controls fermentation in yeast-leavened doughs, but substitutes can weaken dough, reducing loaf volume and texture quality. While bakery has led sodium reduction efforts, confectionery still faces challenges in reducing both sodium and sugar, leaving room for growth in this subcategory.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

In 2024, China accounted for 36.41% of regional revenue, driven by the upcoming GB 2760-2024 food additive standards (effective February 2025) and guidelines promoting low-sodium salt substitutes in processed foods. The China National Center for Food Safety Risk Assessment set potassium chloride benchmarks for soy sauce, instant noodles, and pickled vegetables, key sodium sources in Chinese diets. Angel Yeast, with a monthly capacity of 10,000 metric tons for LA00 yeast extract, is well-positioned to meet domestic and export demand for clean-label sodium reduction in snacks and condiments. The November 2025 update to food safety standards expanded potassium lactate and citrate use in dairy and meat, accelerating reformulations to meet voluntary sodium reduction targets. China's leadership stems from regulatory progress, strong production capacity, and a premiumizing processed food sector.

South Korea is the fastest-growing market, with a 9.31% CAGR forecast through 2030. Growth is driven by the Ministry of Food and Drug Safety's October 2025 amendments, which expanded reduced-sodium labeling and enforced stricter compliance under the Food Labeling Act. These changes shorten product development timelines and increase the importance of sodium reduction agents that maintain flavor. Urban consumers, aware of cardiovascular risks, favor brands reformulating ahead of regulations to secure low-sodium claims. South Korea's advanced food processing and R&D capabilities, supported by collaborations between suppliers and universities, enable rapid adoption of innovative sodium alternatives.

Japan's Ministry of Health set a 6-gram daily salt limit for individuals with hypertension or chronic kidney disease under its 2020 Dietary Reference Intakes, while the Health Japan 21 initiative targets 7 grams by 2032 for the general population. Between 2013 and 2023, the Japanese Society of Hypertension reported a 9,678-metric-ton sodium reduction across 292 products, with soy sauce and pickled vegetables contributing 20% and 10%, respectively. Ajinomoto's Smart Salt Project uses monosodium glutamate and disodium inosinate to enhance umami, enabling a 20%-30% sodium reduction without flavor loss. In July 2024, India's Food Safety and Standards Authority mandated larger sodium labels, addressing 220 million hypertension cases and salt consumption double the WHO's 5-gram recommendation. Australia's Healthy Food Partnership set a 25% sodium reduction target by 2025 for over 30 food categories, while Food Standards Australia New Zealand reviewed nutrition claims in December 2024.

Competitive Landscape

The Asia-Pacific sodium reduction agents market is expanding steadily as governments, health agencies, and consumers intensify their focus on lowering sodium intake to address rising hypertension and cardiovascular risks across the region. Countries such as Japan, China, Australia, South Korea, and India have introduced national salt-reduction strategies that are pressuring food manufacturers to reformulate packaged foods, snacks, seasonings, sauces, and instant meals. This policy push, combined with growing consumer awareness of clean-label, low-sodium, and better-for-you foods, is creating strong demand for innovative sodium reduction solutions across retail and foodservice segments.

Market growth is further supported by the rapid modernization of the food industry, with leading regional and multinational players adopting potassium chloride, yeast extracts, mineral salts, amino acids, and flavor-enhancing technologies to maintain taste while reducing sodium levels. The region’s diverse culinary traditions—ranging from soy-sauce-rich East Asian diets to spice-intensive South Asian dishes—create a complex formulation landscape, prompting food manufacturers to seek tailored sodium-reduction systems that work across different categories. As a result, suppliers offering customized ingredient blends or application-specific technologies are gaining a competitive edge.

The competitive landscape includes global leaders such as Givaudan SA, Tate & Lyle Plc, Kerry Group Plc, DSM-Firmenich AG, and Lesaffre, along with strong regional solution providers that understand local flavor expectations. Companies are investing in R&D centers across Asia-Pacific to co-develop formulations with manufacturers and ensure taste parity in reduced-sodium versions of traditional foods. Looking ahead, continued regulatory tightening, combined with the growth of processed and convenience foods, is expected to sustain long-term demand as brands balance health priorities with taste, affordability, and clean-label expectations.

Asia-Pacific Sodium Reduction Agents Industry Leaders

-

Givaudan SA

-

Tate & Lyle Plc

-

Kerry Group Plc

-

DSM-Firmenich AG

-

Lesaffre

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- November 2025: Angel Yeast has begun trial production at its new specialty yeast facility in Yichang’s Baiyang Biotechnology Park, which will reach an annual capacity of 8,500 tons once fully operational. The launch completes the company’s full specialty yeast value chain, from R&D to large-scale manufacturing, and boosts supply of high-value yeast ingredients for brewing, wine, and bioenergy, further strengthening its biomanufacturing capabilities.

- September 2025: Angel Yeast attended Fi India 2025 by presenting its latest yeast-based innovations designed to enhance flavor, nutrition, and functionality across a wide range of food applications. By highlighting advancements in yeast extracts, fermented ingredients, and specialty yeast products, Angel Yeast is positioning itself as a key partner for food companies seeking next-generation formulation tools.

Asia-Pacific Sodium Reduction Agents Market Report Scope

Asia-Pacific sodium reduction ingredients market is segmented by product type, application, and geography. On the basis of product type, the market is segmented into amino acids & glutamates, mineral salts, yeast extracts, and others. On the basis of application, the market is segmented into bakery & confectionery, condiments, seasonings & sauces, dairy & frozen foods, meat & meat products, snacks, others. Based on geography, the report provide a regional analysis, which includes China, Japan, India, Australia, and rest of Asia-Pacific.

Product Type

| Amino Acids and Glutamates |

| Mineral Salts |

| Yeast Extracts |

| Others |

Application

| Bakery and Confectionery |

| Condiments, Seasonings and Sauces |

| Dairy and Frozen Foods |

| Meat and Seafood Products |

| Snacks and Savoury Products |

| Others |

Country

| China |

| India |

| Japan |

| Australia |

| Indonesia |

| South Korea |

| Thailand |

| Singapore |

| Rest of Asia-Pacific |

| Product Type | Amino Acids and Glutamates |

| Mineral Salts | |

| Yeast Extracts | |

| Others | |

| Application | Bakery and Confectionery |

| Condiments, Seasonings and Sauces | |

| Dairy and Frozen Foods | |

| Meat and Seafood Products | |

| Snacks and Savoury Products | |

| Others | |

| Country | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the forecast value of the Asia-Pacific sodium reduction agents market by 2030?

The market is projected to reach USD 1.43 billion by 2030, up from USD 0.96 billion in 2025.

Which product category currently dominates sales?

Mineral salts, led by potassium chloride, accounted for 68.71% of 2024 revenue.

Which application is expanding the fastest?

Dairy and frozen foods are advancing at a 10.53% CAGR through 2030 as texture-safe lactate blends mature.

Which country is growing quickest in adoption?

South Korea is expected to log a 9.31% CAGR to 2030 due to stricter labeling amendments.

Page last updated on: