| Study Period | 2017 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 17.8 Billion |

| Market Size (2030) | USD 34.11 Billion |

| CAGR (2025 - 2030) | 13.89 % |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order |

Asia-Pacific Small Satellite Market Analysis

The Asia-Pacific Small Satellite Market size is estimated at 17.8 billion USD in 2025, and is expected to reach 34.11 billion USD by 2030, growing at a CAGR of 13.89% during the forecast period (2025-2030).

The Asia-Pacific small satellite industry is experiencing a fundamental transformation through miniaturization and enhanced capabilities, revolutionizing space technology accessibility and applications. Small satellites are increasingly replacing conventional satellites, offering comparable functionality at significantly reduced costs while enabling shorter development cycles and smaller development teams. The trend toward miniaturization has been facilitated by revolutionary technological advancements in electronics and smart materials, reducing satellite bus size and mass over time. This shift is evidenced by the successful deployment of approximately 240 LEO satellites into Low Earth Orbit (LEO) between 2017 and 2022, with Earth observation missions accounting for more than half of these launches.

Commercial applications of small satellites have expanded dramatically, particularly in the Earth observation and communications sectors. A notable example is the ambitious deployment of 89 Jilin-1 satellites between January 2022 and 2023, each weighing 30-45 kg, demonstrating the growing capability of commercial space ventures. These satellites serve various applications, including high-definition video imaging, optical imaging, and hyperspectral imagery for mapping applications. The maritime sector has particularly benefited from these developments, with Asia-Pacific owners controlling approximately 50% of the global commercial merchant shipping fleet as of 2021, driving demand for navigation and communication services.

Technological innovation continues to reshape the industry landscape, with significant breakthroughs in propulsion systems and satellite manufacturing capabilities. A milestone achievement occurred in April 2023 when Space Pioneer successfully launched the Tianlong-2 liquid-propellant rocket from China's Jiuquan satellite launch center, marking the first global launch of a liquid-based propellant rocket by a private company. The China Academy of Space Technology (CAST) has announced plans for an ambitious mega-constellation of 13,000 satellites weighing 190 kg each, showcasing the industry's shift toward large-scale satellite networks for enhanced global connectivity.

Regional cooperation and international partnerships are strengthening the Asia-Pacific small satellite ecosystem, fostering innovation and expanding capabilities. In June 2022, JAXA announced a groundbreaking partnership with ESA to launch a unique comet-chasing mission in 2029, comprising three probes including two smaller satellites. This collaboration exemplifies the growing trend of international cooperation in space exploration and research. The industry is witnessing increased participation from private companies, research institutions, and government agencies, leading to more diverse applications and technological advancements in areas such as Earth observation, communications, and space exploration.

Asia-Pacific Small Satellite Market Trends

The trends for better fuel and operational efficiency are expected to be major drivers of growth

- Satellites are getting smaller nowadays. The fact that the small-sized satellite does almost everything that a conventional satellite does at a fraction of the cost of the conventional satellite made the building, launching, and operation of the small satellite constellations increasingly viable. Correspondingly, our reliance on them has been growing exponentially.

- Small satellites typically have shorter development cycles, smaller development teams, and cost much less for launch. Revolutionary technological advancements facilitated the miniaturization of electronics, which pushed the invention of smart materials, reducing the satellite bus size and mass over time for manufacturers.

- The mass of a satellite has a significant impact on the launch of the satellite, and this is because the heavier the satellite, the more fuel and energy are required to launch it into space. Launching a satellite involves accelerating it to a very high speed, typically around 28,000 km per hour, to place it in orbit around the Earth.

- A heavier satellite requires a larger rocket and more fuel to launch it into space, which increases the cost of the launch and limits the types of launch vehicles that can be used. Similarly, satellites with less than 500 kg are considered small satellites, and around 200+ small satellites were launched in this region. Overall, the mass of a satellite significantly impacts its launch, requiring more energy and fuel to launch a heavier satellite, which increases the cost and can limit the launch options available. The number of operating satellites in the Asia-Pacific region is projected to surge during 2023-2029 due to growing demand in the commercial and military space sector.

-by-country,-Number-of-Satellites-Launched,-Asia-Pacific,-2017---2022.svg)

Understand The Key Trends Shaping This Market

Download PDF

Increasing space expenditures of different space agencies are expected to impact the Asia-Pacific small satellite market positively

- The Asia-Pacific small satellite market has grown rapidly in recent years, owing to technological advancements, increased investment, and growing demand for small satellite services. Nano and microsatellites are smaller and more cost-effective than traditional satellites, making them more accessible to a broader range of organizations

- China, India, and Japan have complete end-to-end space capacity and complete space infrastructure, space technology satellite manufacturing, rockets, and spaceports. Other regions' countries must rely on international cooperation to carry out their respective space programs, which is expected to change to some extent in the coming years. However, many countries in the region are developing indigenous space capabilities as part of their latest agile strategies. In June 2022, South Korea launched the Nuri rocket, putting six satellites into orbit, making it the seventh country in the world to successfully launch a wholly indigenous payload.

- In 2022, according to the draft budget of Japan, the space budget of the country was over USD 1.4 billion. It included investment in space activities of 11 government ministries, such as the development of the H3 rocket, Engineering Test Satellite-9, and the country’s Information Gathering Satellite program.

- Considering the increase in space-related activities in the Asia-Pacific region, satellite manufacturers are enhancing their satellite production capabilities to tap into the rapidly emerging market potentials. The prominent Asia-Pacific countries that possess robust space infrastructure are China, India, Japan, and South Korea. China National Space Administration (CNSA) announced space exploration priorities during 2021–2025, including enhancing national civil space infrastructure.

Segment Analysis: Application

Communication Segment in Asia-Pacific Small Satellite Market

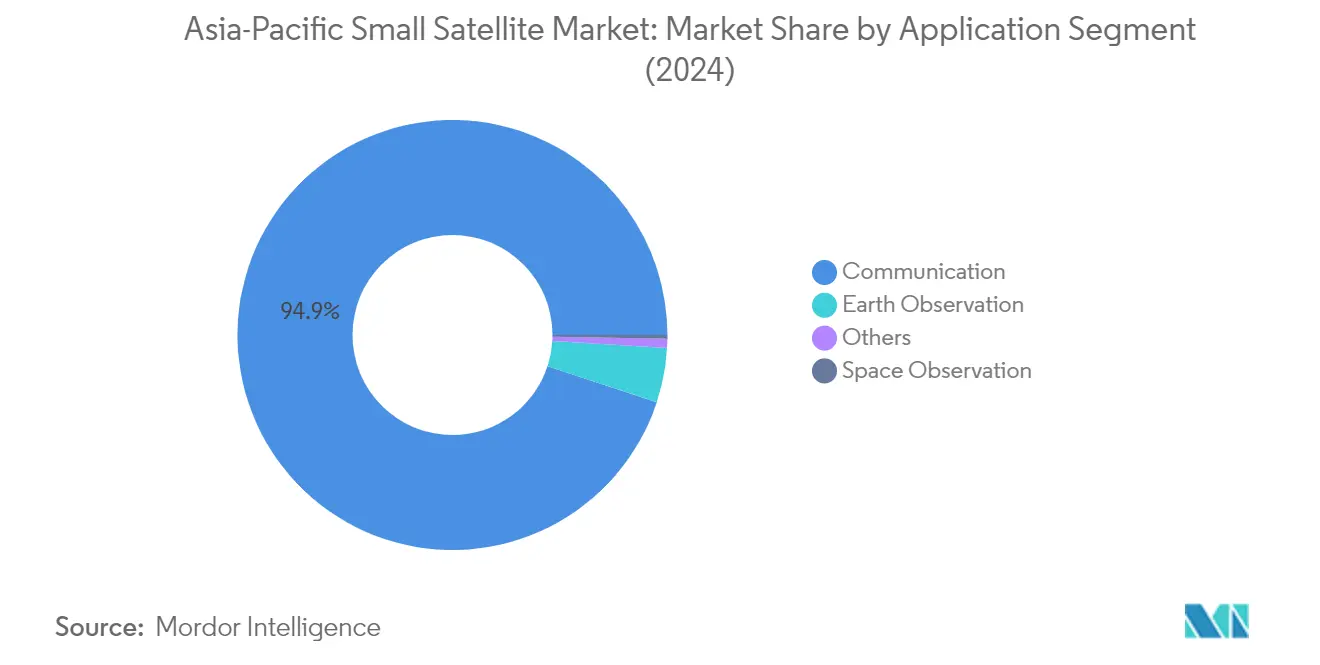

The communication segment dominates the Asia-Pacific small satellite market, commanding approximately 95% market share in 2024. This substantial market position is driven by the increasing demand for high-speed data transmission and rising investments in satellite communication technology, particularly in China and India. The segment's growth is further supported by commercial satellite communication providers like Sky Perfect JSAT and APT Satellite, which operate large fleets of satellites for communication, broadcasting, and related services. The need for uninterrupted connectivity across various applications, including weather forecasting, media and entertainment, aviation, television, internet, and telecommunications, continues to drive demand. Additionally, the growing requirement for motion communication solutions in military vehicles, commercial vehicles, ships, and trains has significantly contributed to the segment's dominant position.

Space Observation Segment in Asia-Pacific Small Satellite Market

The space observation segment is projected to experience the highest growth rate in the Asia-Pacific small satellite market during 2024-2029. This growth is primarily driven by increasing investments in space robotics and the emphasis on developing new space exploration capabilities. The segment's expansion is supported by various space agencies' initiatives in planetary exploration and astronomical research. The development of advanced observation technologies and increasing focus on studying celestial bodies, monitoring climate change, and mapping planetary surfaces are key factors driving this growth. Furthermore, the integration of artificial intelligence and advanced sensing technologies in earth observation satellite systems is expected to enhance their capabilities and drive innovation in this segment over the forecast period.

Remaining Segments in Application

The other segments in the Asia-Pacific small satellite market include earth observation satellite and navigation applications. Earth observation satellites play a crucial role in environmental monitoring, disaster management, urban planning, and natural resource management. These satellites provide valuable data for agriculture, forestry, and climate monitoring applications. The navigation segment focuses on providing precise positioning and timing services for various applications, including transportation, logistics, and defense. Additionally, there are other specialized applications, such as technology demonstration and development, that contribute to the overall market dynamics by testing new technologies and advancing space capabilities.

Segment Analysis: Orbit Class

LEO Segment in Asia-Pacific Small Satellite Market

The Low Earth Orbit (LEO) segment dominates the Asia-Pacific small satellite market, accounting for approximately 99% of the total market share in 2024. This overwhelming dominance is primarily driven by the increasing demand for LEO satellite systems across various applications, including Earth observation, communications, and technology demonstration. The segment's growth is further bolstered by the rising investments from both commercial and government sectors in LEO satellite constellations. The lower launch costs, reduced latency in communications, and improved coverage capabilities associated with LEO satellites have made them particularly attractive for regional operators. Additionally, the surge in demand for launching large constellations of remote sensing satellites for Earth observation has significantly contributed to the segment's market leadership.

MEO Segment in Asia-Pacific Small Satellite Market

The Medium Earth Orbit (MEO) segment is emerging as the fastest-growing segment in the Asia-Pacific small satellite market, projected to grow at approximately 42% during 2024-2029. This remarkable growth is driven by increasing investments in MEO satellite technology for applications such as telecommunications, Earth observation, and scientific research. The segment's expansion is further supported by advancements in miniaturization, propulsion systems, and power generation technologies, which have significantly improved the capabilities of small satellites in MEO. The growing emphasis on enhancing connectivity in rural and remote areas, coupled with the rising demand for high-resolution satellite imaging capabilities, is expected to fuel the segment's growth trajectory in the coming years.

Remaining Segments in Orbit Class

The Geostationary Earth Orbit (GEO) segment, while smaller in market share, plays a crucial role in the Asia-Pacific small satellite market. GEO satellites are particularly valuable for applications requiring continuous coverage over specific geographical areas, such as communication, broadcasting, and weather monitoring. The segment's development is supported by ongoing technological advancements that enable the deployment of smaller, more cost-effective satellites in geostationary orbit. These satellites serve various critical functions, including surveillance, technology demonstration, and automatic identification system applications across the Asia-Pacific region.

Segment Analysis: End User

Commercial Segment in Asia-Pacific Small Satellite Market

The commercial segment dominates the Asia-Pacific small satellite market, commanding approximately 97% market share in 2024, driven by increasing demand for high-speed internet and data connections across the region. This substantial market position is attributed to the growing adoption of satellite communication services for a wide range of applications, including voice and data communications, maritime and air connectivity, and television and radio services. The segment's growth is further bolstered by strong economic development in the region, increased urbanization, and the expansion of e-commerce activities that require robust satellite communication infrastructure. Commercial satellite operators are actively investing in new technologies and solutions to meet the evolving needs of customers across different industries, particularly in remote and rural areas with limited ground infrastructure. The emergence of new players in the satellite manufacturing industry, especially in China and India, has also contributed to the segment's dominance by leveraging their space technology and manufacturing expertise to provide competitive solutions and services to global customers.

Military & Government Segment in Asia-Pacific Small Satellite Market

The military and government segment is projected to experience significant growth at approximately 20% during the forecast period 2024-2029, driven by increasing investments in defense capabilities and national security initiatives. This growth is primarily attributed to the rising demand for small military satellites that provide crucial capabilities such as communication, surveillance, reconnaissance, navigation, and early warning systems. Several countries in the Asia-Pacific region are actively expanding their small satellite capabilities, with China's People's Liberation Army (PLA) leading the way in launching various small satellites for communication, navigation, and reconnaissance applications. The segment's growth is further supported by increasing government investments in space technology for applications such as territorial surveillance, urban planning, disaster prevention, and mitigation. The emphasis on developing indigenous space capabilities and the growing need for secure communication networks for military operations continue to drive innovation and advancement in military satellite technology across the region.

Remaining Segments in End User Segmentation

The other end-users segment, comprising NGOs, academic institutes, and various research institutions, plays a vital role in advancing satellite technology and research despite its smaller market share. These organizations focus primarily on scientific research and educational purposes, contributing to technological innovation and knowledge advancement in the space sector. Academic institutions particularly generate demand for remote sensing satellites in areas where commercial or government-operated satellites may not provide the necessary specialized data. While these organizations typically operate with limited funding and resources compared to commercial and government entities, their contributions to research and development are crucial for the overall advancement of the small satellite industry. The segment's activities primarily focus on scientific research, Earth observation, and various experimental missions that help push the boundaries of satellite technology and applications.

Segment Analysis: Propulsion Tech

Liquid Fuel Segment in Asia-Pacific Small Satellite Market

The liquid fuel propulsion segment dominates the Asia-Pacific small satellite market, accounting for approximately 73% of the total market value in 2024. This significant market share is attributed to the widespread adoption of liquid propulsion technology across various rocket types, from small launch vehicles to heavy-lift vehicles. The segment's prominence is driven by increasing investments from major economies for satellite launches, growing efforts to reduce carbon footprints through alternate fuels, and continuous technological advancements aimed at reducing manufacturing costs while improving fuel efficiency. Private startups in the region, particularly in China, are focusing on developing reusable liquid propulsion engines, with companies equally divided between choosing liquid oxygen and methane (LOX/CH4) and liquid oxygen and kerosene (LOX/KP1) combinations to achieve competitive launch costs.

Electric Segment in Asia-Pacific Small Satellite Market

The electric propulsion segment is experiencing remarkable growth in the Asia-Pacific small satellite market, projected to expand significantly during 2024-2029. This growth is primarily driven by the increasing adoption of miniaturized electronics and smart manufacturing materials, leading to the development of small satellites with shorter development cycles and lower deployment costs. The physical limitations of such satellites have encouraged the development and integration of robust yet compatible electric propulsion systems for efficient orbit correction operations. The emergence of green emission initiatives has further accelerated the adoption of environment-friendly propulsion technologies, particularly electric propulsion, in the region. This technology's appeal lies in its ability to achieve thrust at high exhaust velocities, significantly reducing the propellant required for space missions compared to conventional propulsion methods.

Remaining Segments in Propulsion Tech

The gas-based propulsion segment represents another important technology in the Asia-Pacific small satellite market. This technology has revolutionized satellite propulsion due to its high efficiency, controllability, reliability, and long lifespan characteristics. Gas-based propulsion systems can be effectively utilized across various orbit classes, including geostationary orbit, low Earth orbit, polar orbit, and Sun-synchronous orbit. The technology has gained attention for its potential in various applications, though its adoption has been relatively measured compared to liquid and electric propulsion systems. Recent innovations in gas-based propulsion, including the development of new propellant combinations and improved thrust systems, continue to enhance its viability as an alternative propulsion solution for small satellites.

Asia-Pacific Small Satellite Market Geography Segment Analysis

Asia-Pacific Small Satellite Market in China

China dominates the Asia-Pacific small satellite market, holding approximately 26% of the total market share in 2024. The country's leadership position is driven by its robust space infrastructure and comprehensive end-to-end capabilities in satellite manufacturing, rockets, and spaceports. The State Administration for Science, Technology, and Industry for National Defence (SASTIND) plays a crucial role in administrating China's civil space program, including licensing, registration, and launch services. Chinese manufacturers have demonstrated particular strength in earth observation satellites, with companies like Chang Guang Satellite Technology Co. Ltd launching multiple satellites in the Jilin-1 constellation. The country's emphasis on developing indigenous capabilities in satellite manufacturing has resulted in a thriving ecosystem of both state-owned enterprises and private companies. The government's supportive policies and substantial investments in space technology have created an environment conducive to innovation and growth in the small satellite sector.

Asia-Pacific Small Satellite Market in India

India's small satellite market is projected to grow at approximately 18% annually from 2024 to 2029, making it the fastest-growing market in the region. The Indian Space Research Organization (ISRO) serves as the cornerstone of the country's space industry, operating under the Department of Space and regulating all aspects of the Indian space sector. The country has made significant strides in developing indigenous capabilities for satellite manufacturing, particularly in the areas of earth observation and satellite communication. The implementation of the Space Activities Bill has created a structured framework for commercial space activities, encouraging private sector participation and foreign investment in the industry. India's focus on cost-effective satellite solutions and its emphasis on applications in agriculture, disaster management, and telecommunications has created unique market opportunities. The country's strategic push towards self-reliance in space technology, coupled with increasing private sector participation, has established a strong foundation for sustained growth in the small satellite sector.

Asia-Pacific Small Satellite Market in Japan

Japan has established itself as a key player in the Asia-Pacific small satellite market through its advanced technological capabilities and innovative approach to satellite development. The Japan Aerospace Exploration Agency (JAXA) works in conjunction with private entities like Rocket Systems Corporation (RSC) to promote commercial satellite launch services and satellite development. The country's Space Activities Act provides a comprehensive regulatory framework that has facilitated the growth of commercial space activities while ensuring safety and environmental protection. Japanese manufacturers have particularly excelled in developing miniaturized satellite technologies and advanced propulsion systems. The country's emphasis on research and development, particularly in areas such as space debris mitigation and satellite constellation management, has positioned it as a technology leader in the region. The collaboration between academic institutions and private companies has created a robust ecosystem for satellite innovation and development.

Asia-Pacific Small Satellite Market in South Korea

South Korea has emerged as a significant player in the small satellite market, marked by its successful development of indigenous launch capabilities and satellite manufacturing expertise. The country's achievement in becoming the seventh nation globally to successfully launch a wholly indigenous payload demonstrates its growing technological capabilities. South Korean manufacturers have focused on developing specialized capabilities in communication and remote sensing satellites, particularly for environmental monitoring and telecommunications applications. The country's strategic focus on developing its space industry has led to increased collaboration between government agencies, research institutions, and private companies. The establishment of dedicated space technology clusters and research centers has created an environment conducive to innovation in satellite technology. South Korea's commitment to developing its space capabilities is reflected in its comprehensive approach to satellite manufacturing, testing, and deployment.

Asia-Pacific Small Satellite Market in Other Countries

Other countries in the Asia-Pacific region, including Singapore, Australia, and New Zealand, are actively developing their capabilities in the small satellite market. These nations have established specialized regulatory frameworks and agencies to oversee space activities and promote industry growth. Singapore, despite not having a national space agency, has created a conducive environment for commercial space activities through its telecommunications regulatory framework. Australia's Space Agency has focused on developing the country's commercial space industry and facilitating international space engagement. New Zealand has positioned itself as an attractive location for satellite launches through its comprehensive regulatory framework and emphasis on safety and security. These countries are increasingly focusing on niche applications and specialized capabilities, contributing to the overall diversity and dynamism of the Asia-Pacific small satellite market.

Get Analysis on Important Geographic Markets

Download PDF

Asia-Pacific Small Satellite Industry Overview

Top Companies in Asia-Pacific Small Satellite Market

The small satellite market in Asia-Pacific is characterized by continuous product innovation and strategic expansion initiatives by key players. Companies are focusing on developing advanced satellite manufacturing technologies, particularly in areas like remote sensing, communication, and Earth observation capabilities. Operational agility has become paramount, with manufacturers streamlining their production processes to meet the growing demand for satellite constellations. Strategic partnerships and collaborations, especially between commercial entities and government space agencies, have emerged as a crucial trend driving market growth. Companies are also expanding their manufacturing facilities and research centers across the region to strengthen their market presence and enhance technological capabilities. The emphasis on developing cost-effective solutions while maintaining high-performance standards has become a key focus area for market players, leading to increased investment in research and development activities.

Market Dominated by State-Backed Space Enterprises

The Asia-Pacific small satellite market exhibits a consolidated structure dominated by state-owned enterprises and established aerospace companies. Chinese and Indian state-backed organizations hold significant market share, leveraging their extensive government support and integrated space technology capabilities. The market shows a strong presence of local players who have developed comprehensive end-to-end space capabilities, from satellite manufacturing to launch services. The competitive landscape is characterized by high entry barriers due to the capital-intensive nature of the industry and the need for advanced technological expertise.

The market has witnessed limited merger and acquisition activity, with companies focusing more on organic growth and strategic partnerships. Major players are primarily large conglomerates with diverse aerospace portfolios, though specialized small satellite manufacturers are gradually gaining prominence. The competitive dynamics are heavily influenced by government space programs and policies, with state-owned enterprises maintaining their dominant position through continued government support and funding. Regional players are increasingly focusing on developing indigenous capabilities to reduce dependence on international cooperation.

Innovation and Partnerships Drive Future Success

Success in the Asia-Pacific small satellite market increasingly depends on developing innovative technologies and establishing strategic partnerships. Incumbent players must focus on expanding their product portfolios to address diverse application requirements while maintaining cost competitiveness. Companies need to invest in advanced manufacturing capabilities and develop expertise in emerging technologies like artificial intelligence and machine learning for satellite operations. Building strong relationships with government agencies and research institutions has become crucial for securing contracts and accessing new market opportunities.

For contenders looking to gain market share, specialization in specific applications or technologies offers a viable entry strategy. Companies must focus on developing unique value propositions that address unmet market needs while building robust supply chain networks. The regulatory environment plays a crucial role, with companies needing to navigate complex space regulations and licensing requirements across different countries. End-user concentration in government and commercial sectors necessitates a balanced approach to market development, while the risk of substitution from alternative technologies requires continuous innovation and adaptation of business strategies. Additionally, the development of satellite components and satellite payload systems, alongside advancements in satellite propulsion, are critical areas for innovation.

Asia-Pacific Small Satellite Market Leaders

-

Axelspace Corporation

-

Chang Guang Satellite Technology Co. Ltd

-

China Aerospace Science and Technology Corporation (CASC)

-

Guodian Gaoke

-

Spacety Aerospace Co.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Asia-Pacific Small Satellite Market News

- March 2022: The China Aerospace Science and Technology Corporation successfully launched the Tiankun-2 satellites into a low-Earth polar orbit on the debut launch of the Long March 6A.

- March 2022: Guodian Gaoke's Tianqi 19 commercial data relay satellite was launched from the Long March 8 rocket.

- February 2022: A total of 89 Jilin-1 optical imaging satellites manufactured by CASC each weighing 30-45 kg were launched into orbit.

Free With This Report

We offer a comprehensive set of global and local metrics that illustrate the fundamentals of the satellites industry. Clients can access in-depth market analysis of various satellites and launch vehicles through granular level segmental information supported by a repository of market data, trends, and expert analysis. Data and analysis on satellite launches, satellite mass, application of satellites, spending on space programs, propulsion systems, end users, etc., are available in the form of comprehensive reports as well as excel based data worksheets.

Asia-Pacific Small Satellite Market Report - Table of Contents

1. EXECUTIVE SUMMARY & KEY FINDINGS

2. REPORT OFFERS

3. INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4. KEY INDUSTRY TRENDS

- 4.1 Satellite Mass

- 4.2 Spending On Space Programs

-

4.3 Regulatory Framework

- 4.3.1 Australia

- 4.3.2 China

- 4.3.3 India

- 4.3.4 Japan

- 4.3.5 New Zealand

- 4.3.6 Singapore

- 4.3.7 South Korea

- 4.4 Value Chain & Distribution Channel Analysis

5. MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

-

5.1 Application

- 5.1.1 Communication

- 5.1.2 Earth Observation

- 5.1.3 Navigation

- 5.1.4 Space Observation

- 5.1.5 Others

-

5.2 Orbit Class

- 5.2.1 GEO

- 5.2.2 LEO

- 5.2.3 MEO

-

5.3 End User

- 5.3.1 Commercial

- 5.3.2 Military & Government

- 5.3.3 Other

-

5.4 Propulsion Tech

- 5.4.1 Electric

- 5.4.2 Gas based

- 5.4.3 Liquid Fuel

6. COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

-

6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Axelspace Corporation

- 6.4.2 Chang Guang Satellite Technology Co. Ltd

- 6.4.3 China Aerospace Science and Technology Corporation (CASC)

- 6.4.4 Guodian Gaoke

- 6.4.5 MinoSpace Technology

- 6.4.6 Spacety Aerospace Co.

- 6.4.7 Zhuhai Orbita Control Engineering

7. KEY STRATEGIC QUESTIONS FOR SATELLITE CEOS

8. APPENDIX

-

8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter’s Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

List of Tables & Figures

- Figure 1:

- SATELLITE MASS (ABOVE 10KG) BY COUNTRY, NUMBER OF SATELLITES LAUNCHED, ASIA-PACIFIC, 2017 - 2022

- Figure 2:

- SPENDING ON SPACE PROGRAMS BY COUNTRY, USD, ASIA-PACIFIC, 2017 - 2022

- Figure 3:

- ASIA-PACIFIC SMALL SATELLITE MARKET, VALUE, USD, 2017 - 2029

- Figure 4:

- VALUE OF SMALL SATELLITE MARKET BY APPLICATION, USD, ASIA-PACIFIC, 2017 - 2029

- Figure 5:

- VALUE SHARE OF SMALL SATELLITE MARKET BY APPLICATION, %, ASIA-PACIFIC, 2017 VS 2023 VS 2029

- Figure 6:

- VALUE OF COMMUNICATION MARKET, USD, ASIA-PACIFIC, 2017 - 2029

- Figure 7:

- VALUE OF EARTH OBSERVATION MARKET, USD, ASIA-PACIFIC, 2017 - 2029

- Figure 8:

- VALUE OF NAVIGATION MARKET, USD, ASIA-PACIFIC, 2017 - 2029

- Figure 9:

- VALUE OF SPACE OBSERVATION MARKET, USD, ASIA-PACIFIC, 2017 - 2029

- Figure 10:

- VALUE OF OTHERS MARKET, USD, ASIA-PACIFIC, 2017 - 2029

- Figure 11:

- VALUE OF SMALL SATELLITE MARKET BY ORBIT CLASS, USD, ASIA-PACIFIC, 2017 - 2029

- Figure 12:

- VALUE SHARE OF SMALL SATELLITE MARKET BY ORBIT CLASS, %, ASIA-PACIFIC, 2017 VS 2023 VS 2029

- Figure 13:

- VALUE OF GEO MARKET, USD, ASIA-PACIFIC, 2017 - 2029

- Figure 14:

- VALUE OF LEO MARKET, USD, ASIA-PACIFIC, 2017 - 2029

- Figure 15:

- VALUE OF MEO MARKET, USD, ASIA-PACIFIC, 2017 - 2029

- Figure 16:

- VALUE OF SMALL SATELLITE MARKET BY END USER, USD, ASIA-PACIFIC, 2017 - 2029

- Figure 17:

- VALUE SHARE OF SMALL SATELLITE MARKET BY END USER, %, ASIA-PACIFIC, 2017 VS 2023 VS 2029

- Figure 18:

- VALUE OF COMMERCIAL MARKET, USD, ASIA-PACIFIC, 2017 - 2029

- Figure 19:

- VALUE OF MILITARY & GOVERNMENT MARKET, USD, ASIA-PACIFIC, 2017 - 2029

- Figure 20:

- VALUE OF OTHER MARKET, USD, ASIA-PACIFIC, 2017 - 2029

- Figure 21:

- VALUE OF SMALL SATELLITE MARKET BY PROPULSION TECH, USD, ASIA-PACIFIC, 2017 - 2029

- Figure 22:

- VALUE SHARE OF SMALL SATELLITE MARKET BY PROPULSION TECH, %, ASIA-PACIFIC, 2017 VS 2023 VS 2029

- Figure 23:

- VALUE OF ELECTRIC MARKET, USD, ASIA-PACIFIC, 2017 - 2029

- Figure 24:

- VALUE OF GAS BASED MARKET, USD, ASIA-PACIFIC, 2017 - 2029

- Figure 25:

- VALUE OF LIQUID FUEL MARKET, USD, ASIA-PACIFIC, 2017 - 2029

- Figure 26:

- NUMBER OF STRATEGIC MOVES OF MOST ACTIVE COMPANIES, ASIA-PACIFIC SMALL SATELLITE MARKET, ASIA-PACIFIC, 2017 - 2029

- Figure 27:

- TOTAL NUMBER OF STRATEGIC MOVES OF COMPANIES, ASIA-PACIFIC SMALL SATELLITE MARKET, ASIA-PACIFIC, 2017 - 2029

- Figure 28:

- MARKET SHARE OF ASIA-PACIFIC SMALL SATELLITE MARKET, %, ASIA-PACIFIC, 2023

Asia-Pacific Small Satellite Industry Segmentation

Communication, Earth Observation, Navigation, Space Observation, Others are covered as segments by Application. GEO, LEO, MEO are covered as segments by Orbit Class. Commercial, Military & Government are covered as segments by End User. Electric, Gas based, Liquid Fuel are covered as segments by Propulsion Tech.| Application | Communication |

| Earth Observation | |

| Navigation | |

| Space Observation | |

| Others | |

| Orbit Class | GEO |

| LEO | |

| MEO | |

| End User | Commercial |

| Military & Government | |

| Other | |

| Propulsion Tech | Electric |

| Gas based | |

| Liquid Fuel |

Need A Different Region or Segment?

Customize Now

Market Definition

- Application - Various applications or purposes of the satellites are classified into communication, earth observation, space observation, navigation, and others. The purposes listed are those self-reported by the satellite’s operator.

- End User - The primary users or end users of the satellite is described as civil (academic, amateur), commercial, government (meteorological, scientific, etc.), military. Satellites can be multi-use, for both commercial and military applications.

- Launch Vehicle MTOW - The launch vehicle MTOW (maximum take-off weight) means the maximum weight of the launch vehicle during take-off, including the weight of payload, equipment and fuel.

- Orbit Class - The satellite orbits are divided into three broad classes namely GEO, LEO, and MEO. Satellites in elliptical orbits have apogees and perigees that differ significantly from each other and categorized satellite orbits with eccentricity 0.14 and higher as elliptical.

- Propulsion tech - Under this segment, different types of satellite propulsion systems have been classified as electric, liquid-fuel and gas-based propulsion systems.

- Satellite Mass - Under this segment, different types of satellite propulsion systems have been classified as electric, liquid-fuel and gas-based propulsion systems.

- Satellite Subsystem - All the components and subsystems which includes propellants, buses, solar panels, other hardware of satellites are included under this segment.

| Keyword | Definition |

|---|---|

| Attitude Control | The orientation of the satellite relative to the Earth and the sun. |

| INTELSAT | The International Telecommunications Satellite Organization operates a network of satellites for international transmission. |

| Geostationary Earth Orbit (GEO) | Geostationary satellites in Earth orbit 35,786 km (22,282 mi) above the equator in the same direction and at the same speed as the earth rotates on its axis, making them appear fixed in the sky. |

| Low Earth Orbit (LEO) | Low Earth Orbit satellites orbit from 160-2000km above the earth, take approximately 1.5 hours for a full orbit and only cover a portion of the earth’s surface. |

| Medium Earth Orbit (MEO) | MEO satellites are located above LEO and below GEO satellites and typically travel in an elliptical orbit over the North and South Pole or in an equatorial orbit. |

| Very Small Aperture Terminal (VSAT) | Very Small Aperture Terminal is an antenna that is typically less than 3 meters in diameter |

| CubeSat | CubeSat is a class of miniature satellites based on a form factor consisting of 10 cm cubes. CubeSats weigh no more than 2 kg per unit and typically use commercially available components for their construction and electronics. |

| Small Satellite Launch Vehicles (SSLVs) | Small Satellite Launch Vehicle (SSLV) is a three-stage Launch Vehicle configured with three Solid Propulsion Stages and a liquid propulsion-based Velocity Trimming Module (VTM) as a terminal stage |

| Space Mining | Asteroid mining is the hypothesis of extracting material from asteroids and other asteroids, including near-Earth objects. |

| Nano Satellites | Nanosatellites are loosely defined as any satellite weighing less than 10 kilograms. |

| Automatic Identification System (AIS) | Automatic identification system (AIS) is an automatic tracking system used to identify and locate ships by exchanging electronic data with other nearby ships, AIS base stations, and satellites. Satellite AIS (S-AIS) is the term used to describe when a satellite is used to detect AIS signatures. |

| Reusable launch vehicles (RLVs) | Reusable launch vehicle (RLV) means a launch vehicle that is designed to return to Earth substantially intact and therefore may be launched more than one time or that contains vehicle stages that may be recovered by a launch operator for future use in the operation of a substantially similar launch vehicle. |

| Apogee | The point in an elliptical satellite orbit which is farthest from the surface of the earth. Geosynchronous satellites which maintain circular orbits around the earth are first launched into highly elliptical orbits with apogees of 22,237 miles. |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue and volume terms. For sales conversion to volume, the average selling price (ASP) is kept constant throughout the forecast period for each country, and inflation is not a part of the pricing.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms.

Get More Details On Research Methodology

Download PDF