Market Trends of Asia-Pacific Silica Sand Industry

Glass Industry to Dominate the Market

- Although silica sand is the primary raw material for glass manufacturing, only high-purity silica sand is used in the process. The reason for such demanding requirements is that the purity of the sand directly impacts the transparency, strength, and durability of the glass. For example, only glass products that are manufactured with high-quality silica sand can meet the optimal vision requirements for vehicle windshields.

- In glass manufacturing, high-quality silica sand makes up around three-quarters of the batch of raw materials used in the glassmaking process. The other quarter is made up of soda, limestone, and clarifying agents, along with a percentage of recycled glass.

- Silica sand finds application in the production of various types of glass, including flat glass, container glass, specialty glass, fiberglass, and others.

- In the Asia Pacific region, China, India, and Japan are among the major contributors to regional glass production. For instance, according to the data published by the UN Comtrade, China's exports of glass and glassware were valued at USD 26.66 billion in 2022. Moreover, glass and glassware products were the 25th most exported products from China in 2022.

- In India, among all sub-segments of glass, float glass experienced strong growth due to increasing demand from the construction and automotive sectors in the country. Additionally, the presence of five float glass producers and 11 float glass lines with an installed capacity of 7.5 kilotons per day contributed to this growth.

- Several glass manufacturers have a presence in Japan. In Japan, glass products are commonly used for packaging. Liquor bottles and food containers were the glass products with the highest production volumes. Glass is infinitely recyclable, reusable, and a more sustainable alternative to plastic packaging. AGC is one of the largest manufacturers of glass. In 2022, AGC represented the most significant glass manufacturing company in Japan, selling glass for approximately JPY 1.7 trillion (USD 11.87 billion). According to the METI, the production volume of tempered glass in Japan amounted close to 22.23 million square meters in 2022.

- The glass industry across the major economies in Asia-Pacific is growing strongly, and the demand for silica sand for glass production is likely to reflect the same trend over the forecast period.

Understand The Key Trends Shaping This Market

Download PDF

China to Dominate the Regional Market

- China dominates the Asia-Pacific silica sand market owing to the vivid presence of the glass manufacturing industry and the growing adoption of glass in several industries, including construction and automotive.

- The glass manufacturing industry is exhibiting strong growth in the country, which is likely to continue to support the growth of the silica sand market in the coming years.

- According to the National Bureau of Statistics of China, China produced approximately 43.07 million square meters of reinforced glass in April 2023. Additionally, in 2022, the total production of reinforced glass amounted to nearly 580 million square meters.

- In 2022, the annual output of photovoltaic rolled glass was 16.062 million tons, an increase of 53.6% year-on-year.

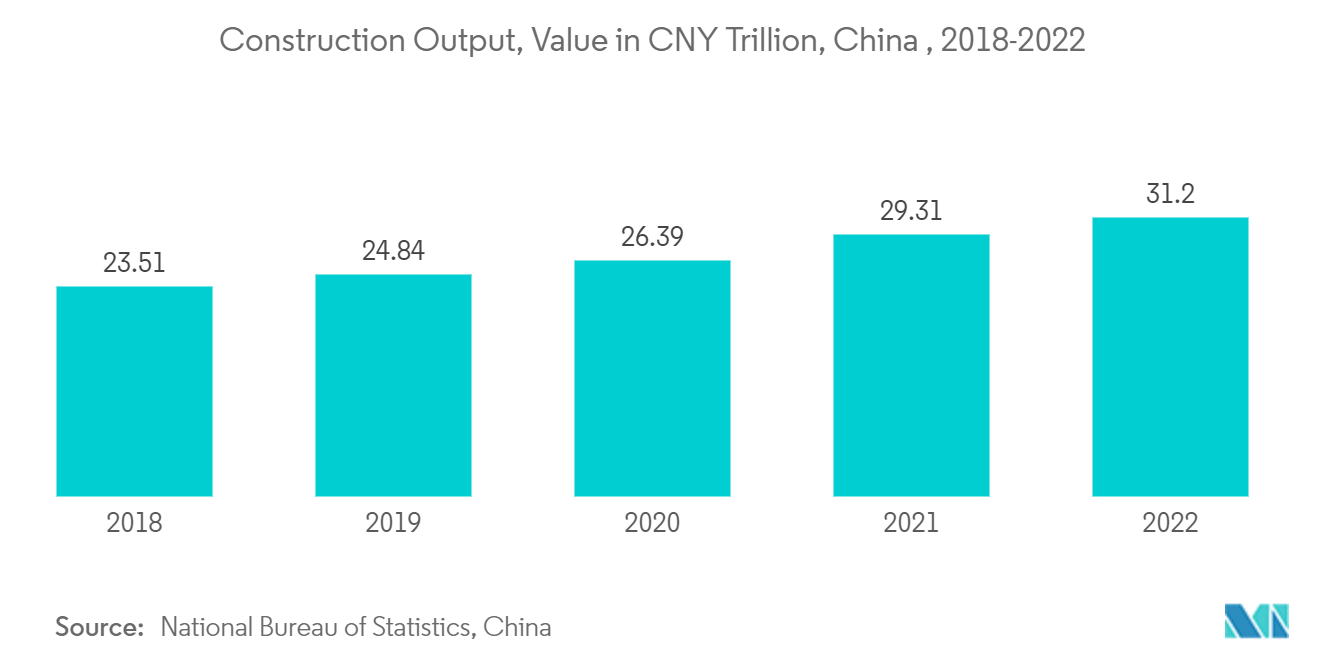

- The construction sector is a key player in China's continued economic development. China is amid a construction mega-boom. According to the National Bureau of Statistics of China, the value of construction output accounted for CNY 31.2 trillion (USD 4.5 trillion) in 2022, up from CNY 29.3 trillion (USD 4.2 trillion) in 2021. China is expected to spend nearly USD 13 trillion on buildings by 2030, creating a positive outlook for the industry.

- The overall Chinese construction industry is expected to increase by 4.6% in real terms over the period 2023-2026. As per the report published by the National Bureau of Statistics of China, transportation investment increased by 6.7% year-on-year in the first half of 2022.

- In the case of long-term plans announced by the Chinese government for infrastructure development, the development of 162,000 km of expressways is planned by 2035.

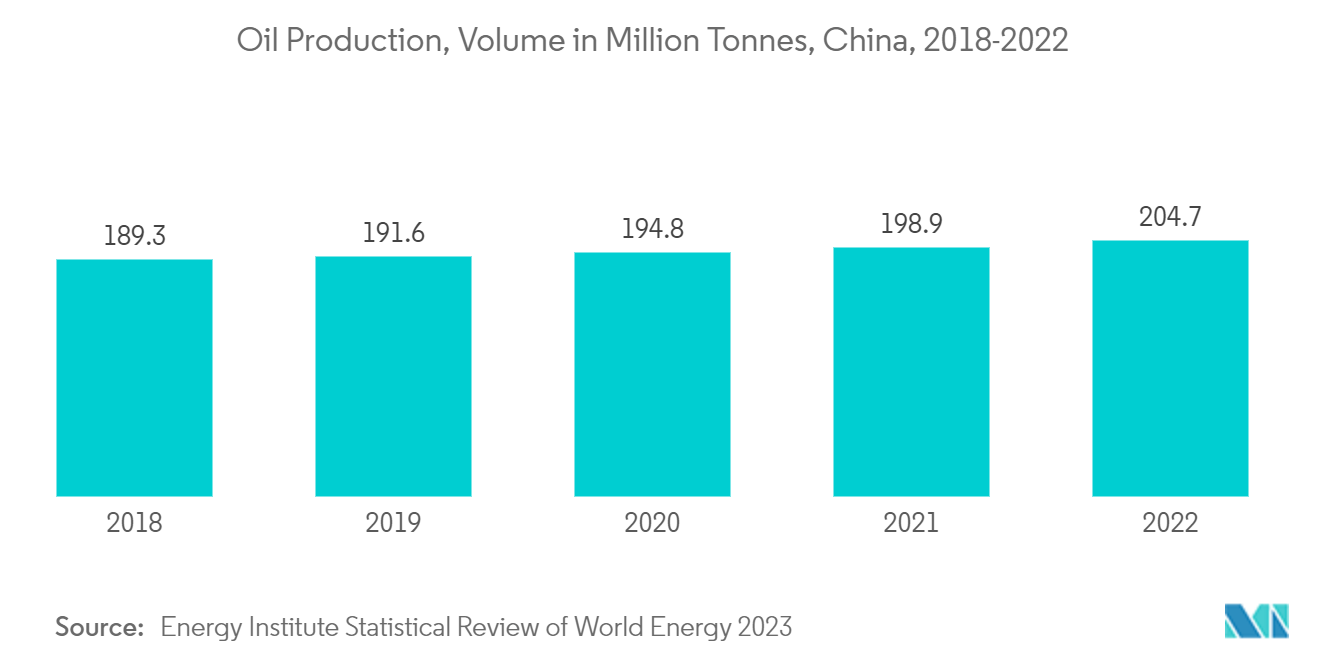

- The oil and gas sector is one of the largest application industries for silica sand in China. China has been investing to scale up its refining capacity over the past two decades for its growing economy. Moreover, for a long-term period, China has continuously expanded its refining capacity for all types of crudes.

- According to Institute for Energy Research, China is likely to register 20 million barrels of refining capacity at the end of 2025, which will trigger the demand for silica sand in the upcoming years.

- Moreover, oil production in China has also increased in 2022. China produced 4.11 million barrels of oil per day, an increase of 2.9% over 2021 figures.

- Such trends and developments across the major end-user industries are expected to drive the demand for silica sand in China over the forecast period.

Get Analysis on Important Geographic Markets

Download PDF