Market Size of Asia-Pacific Silica Sand Industry

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

| Forecast Data Period | 2024 - 2029 |

| Historical Data Period | 2019 - 2022 |

| CAGR | 6.39 % |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Asia-Pacific Silica Sand Market Analysis

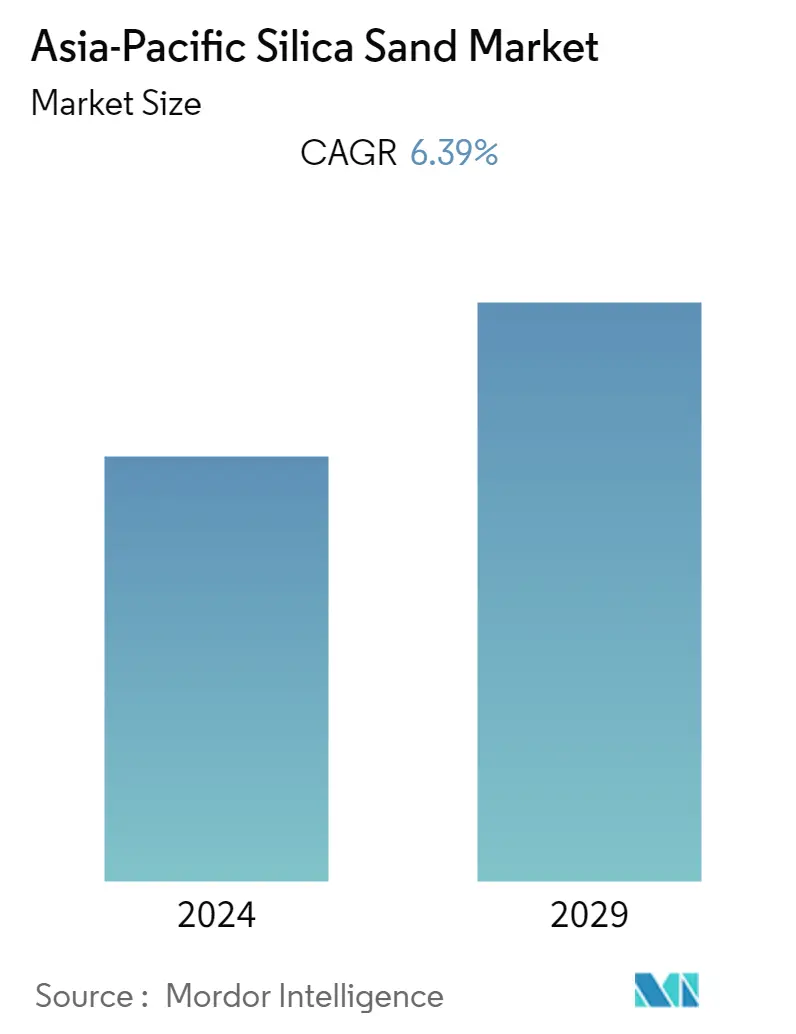

The Asia-Pacific silica sand market is estimated to reach 136.85 million tons by the end of this year and is projected to reach 186.5 million tons in the next five years, registering a CAGR of 6.39% during the forecast period.

- The COVID-19 pandemic affected several industries negatively. The lockdown in most countries in the region caused disruptions in infrastructure and construction activities, mining operations, and freight transportation that disturbed the supply chain in nearly every end-user industry. However, the conditions started recovering in 2021, restoring the market's growth trajectory.

- Over the short term, growing demand from the glass production industry in Asia-Pacific and consumption in the foundry industry are major factors driving the growth of the market studied.

- However, the illegal mining of sand and the availability of substitutes for silica sand are likely to restrain the growth of the studied market.

- Nevertheless, the development of sand-based treatments in dentistry and biotechnology will likely create lucrative growth opportunities for the market in the coming years.

- China represents the largest market for silica sand in the region and is likely to witness strong growth in demand on the back of increasing consumption of silica sand in glass production, oil and gas, and construction industries.

Asia-Pacific Silica Sand Industry Segmentation

Silica sand is a type of sand with high silicon dioxide (SiO2) content. It is a naturally occurring material that is found in many parts of the world. Silica sand is used in a variety of applications, including glassmaking, foundries, and fracking, among others.

The Asia-Pacific is segmented by end-user industry and geography. The end-user industry segment includes glass manufacturing, foundry, chemical production, construction, paints and coatings, ceramics and refractories, filtration, oil and gas, and other end-user industries like food processing, industrial abrasives, and sports fields. These segments highlight the varied applications of silica sand across sectors, enabling tailored product and service offerings. These industry segments help delineate the diverse applications of silica sand across various sectors, aiding in customized product and service offerings.

Geographically, the market spans different regions, each with its distinct demand, supply, and market dynamics. This geographical segmentation allows businesses to adapt their strategies to specific regional conditions, thus enhancing their market presence and competitive advantage.

For each segment, the market sizing and forecasts are provided on the basis of volume (tons).

| End-User Industry | |

| Glass Manufacturing | |

| Foundry | |

| Chemical Production | |

| Construction | |

| Paints and Coatings | |

| Ceramics and Refractories | |

| Filtration | |

| Oil and Gas Recovery | |

| Other End User Industries (Food Processing, Industrial Abrasives and Sports Fields) |

| Geography | |

| China | |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific |

Asia-Pacific Silica Sand Market Size Summary

The Asia-Pacific silica sand market is experiencing a robust growth trajectory, driven primarily by the increasing demand from the glass production and foundry industries. The market, which faced disruptions due to the COVID-19 pandemic, has shown resilience and is on a path of recovery. The region's demand for silica sand is significantly bolstered by the glass manufacturing sector, where high-purity silica sand is essential for producing transparent, strong, and durable glass products. This demand is particularly pronounced in China, India, and Japan, where the glass industry is expanding due to rising consumption in construction and automotive sectors. Despite challenges such as illegal mining and the availability of substitutes, the market is poised for growth, with emerging applications in dentistry and biotechnology offering new opportunities.

China stands out as the dominant player in the Asia-Pacific silica sand market, supported by its thriving glass manufacturing industry and substantial investments in construction and infrastructure. The country's economic development is closely tied to its construction sector, which is experiencing a mega-boom, further driving the demand for silica sand. Additionally, China's oil and gas industry, with its expanding refining capacity, contributes to the market's growth. The market is characterized by a consolidated landscape, with key players like Sibelco, Chongqing Changjiang River Moulding Material Group Co. Ltd, JFE Mineral & Alloy Company Ltd, PUM Group, and Mitsubishi Corporation playing significant roles. These trends indicate a positive outlook for the silica sand market in the region over the forecast period.

Asia-Pacific Silica Sand Market Size - Table of Contents

-

1. MARKET DYNAMICS

-

1.1 Drivers

-

1.1.1 Growing Demand from the Glass Industry

-

1.1.2 Increasing Consumption in the Foundry Industry

-

1.1.3 Other Drivers

-

-

1.2 Restraints

-

1.2.1 Availability of Substitutes

-

1.2.2 Illegal Mining of Sand

-

-

1.3 Industry Value Chain Analysis

-

1.4 Porter's Five Forces Analysis

-

1.4.1 Bargaining Power of Suppliers

-

1.4.2 Bargaining power of Buyers

-

1.4.3 Threat of New Entrants

-

1.4.4 Threat of Substitute Products and Services

-

1.4.5 Degree of Competition

-

-

-

2. MARKET SEGMENTATION (Market Size in Volume)

-

2.1 End-User Industry

-

2.1.1 Glass Manufacturing

-

2.1.2 Foundry

-

2.1.3 Chemical Production

-

2.1.4 Construction

-

2.1.5 Paints and Coatings

-

2.1.6 Ceramics and Refractories

-

2.1.7 Filtration

-

2.1.8 Oil and Gas Recovery

-

2.1.9 Other End User Industries (Food Processing, Industrial Abrasives and Sports Fields)

-

-

2.2 Geography

-

2.2.1 China

-

2.2.2 India

-

2.2.3 Japan

-

2.2.4 South Korea

-

2.2.5 ASEAN Countries

-

2.2.6 Rest of Asia-Pacific

-

-

Asia-Pacific Silica Sand Market Size FAQs

What is the current Asia-Pacific Silica Sand Market size?

The Asia-Pacific Silica Sand Market is projected to register a CAGR of 6.39% during the forecast period (2024-2029)

Who are the key players in Asia-Pacific Silica Sand Market?

Sibelco, Chongqing Changjiang River Moulding Material Group Co. Ltd (CCRMM) , JFE Mineral & Alloy Company Ltd, PUM Group and Mitsubishi Corporation are the major companies operating in the Asia-Pacific Silica Sand Market.