Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

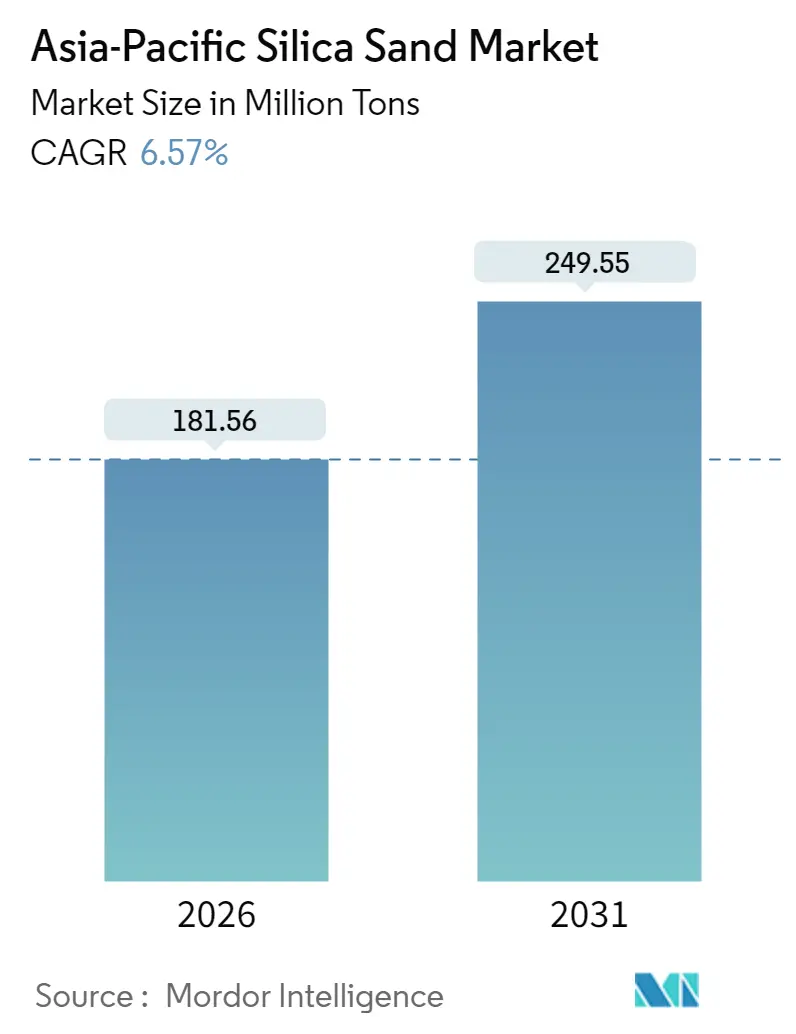

| Market Volume (2026) | 181.56 Million tons |

| Market Volume (2031) | 249.55 Million tons |

| Growth Rate (2026 - 2031) | 6.57% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Silica Sand Market Analysis by Mordor Intelligence

Asia-Pacific Silica Sand Market size in 2026 is estimated at 181.56 million tons, growing from 2025 value of 170.37 million tons with 2031 projections showing 249.55 million tons, growing at 6.57% CAGR over 2026-2031. Multiple demand centers, including glass manufacturing, electronics, foundry applications, and construction materials, are converging to sustain this expansion. Glass grade sand remains the workhorse because flat and container glass output tracks the region’s rapid urbanization and vehicle production. At the same time, hyper-purity quartz (HPQ) grades are transitioning from a niche toward mainstream status as semiconductor manufacturers push below the 3-nanometer design rule. Competitive intensity is rising as large, integrated miners accelerate automation and environmental compliance to lock in premium contracts while smaller operators struggle to meet tightening regulations. Mid-term opportunities cluster around solar glass, advanced electronics, and cross-border infrastructure projects that lock in long-haul supply contracts across Southeast Asia.

Key Report Takeaways

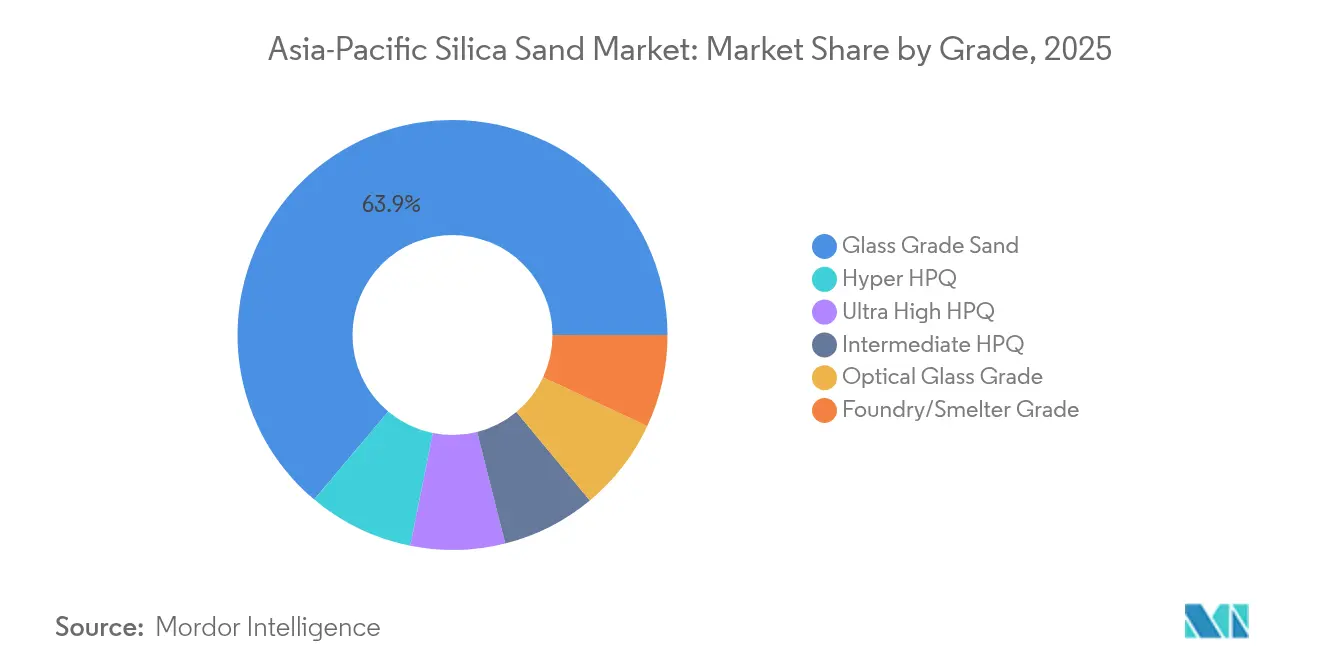

- By grade, glass grade sand held 63.88% of the Asia-Pacific silica sand market share in 2025, whereas hyper HPQ is forecast to expand at an 11.12% CAGR through 2031.

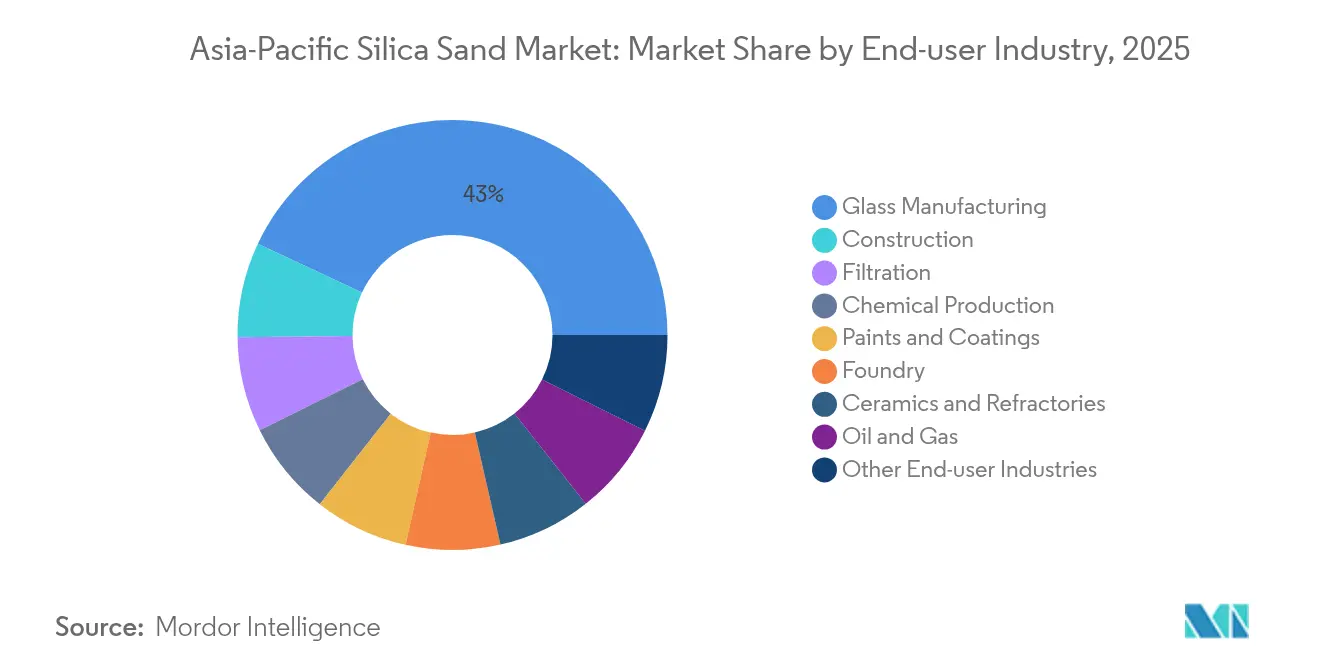

- By end-use, glass manufacturing accounted for 43.02% of the Asia-Pacific silica sand market size in 2025 and is advancing at a 7.29% CAGR through 2031.

- By geography, China commanded 72.98% of the Asia-Pacific silica sand market share in 2025, while India is projected to grow at an 8.43% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific Silica Sand Market Trends and Insights

Driver Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Construction-led flat and container glass demand surge | +2.1% | ASEAN core, spill-over to China and India | Medium term (2-4 years) |

| Foundry revival for EV and wind-power castings | +1.8% | China, Japan, South Korea, with early gains in Thailand, Malaysia | Medium term (2-4 years) |

| Rapid infrastructure spending across ASEAN | +1.5% | Thailand, Malaysia, Philippines, Vietnam, Indonesia | Short term (≤ 2 years) |

| Shift to energy-efficient low-iron solar glass | +1.2% | Global, with concentration in China, India, Japan | Long term (≥ 4 years) |

| Indonesia's silica downstreaming for semiconductors | +0.8% | Indonesia, with technology transfer to regional partners | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Construction-Led Flat and Container Glass Demand Surge

Thailand’s Eastern Economic Corridor is driving 3-4% annual construction growth through 2026, lifting demand for flat and container glass across public works, commercial complexes, and residential towers. Glass manufactures treat silica sand as an essential cost component, often exceeding 60% of raw-material expenses, so rising project backlogs translate directly into higher sand uplift. Inventory corrections that hurt 2024 margins have already reversed, with most ASEAN producers reporting fuller order books for 2025 delivery. Cross-border infrastructure corridors under the ASEAN Connectivity vision are boosting long-distance shipments from Malaysia and Australia to inland Chinese float-glass lines, tightening freight capacity on favored routes. Given that glass output trails economic activity with a 6- to 12-month lag, the rebound indicates a clear volume runway through at least 2027. Energy-efficient low-iron variants secure additional premiums because they enable thinner glazing standards in green-building codes.

Foundry Revival for EV and Wind-Power Castings

Electric-vehicle casting technology increasingly specifies narrow thermal-expansion bands, pushing foundries toward calibrated silica sand blends with tighter grain-size distributions. China’s clean-energy leadership, 70% of global output in 2024, created a lift in aluminum and ductile-iron casting that consumed roughly 9.1 million tons of foundry sand region-wide last year[1]International Energy Agency, “Energy Technology Perspectives 2024,” iea.org. Japan and South Korea, home to advanced molding machinery, are exporting turnkey foundry lines into Thailand and Vietnam, prompting localized demand for premium sand grades. The effect cascades through wind-turbine hubs clustered in Fujian, Jeju, and Cebu, where final-machined castings absorb high silica volumes for nacelle housings and hub assemblies. Investment pipelines worth USD 235 billion in 2024 targeted clean-energy manufacturing, signalling durable sand flows into 2030. Producers that certify thermal-shock performance and dimensional accuracy are capturing multiyear supply contracts from battery and turbine OEMs.

Rapid Infrastructure Spending Across ASEAN

Aggregate mineral imports above USD 94 billion in 2018 set the baseline for a renewed infrastructure push as Southeast Asian governments reopen fiscal spigots after pandemic-era austerity[2]Minerals Council of Australia, “New Frontiers: South and East Asia,” minerals.org.au. Indonesia’s updated medium-term national plan allocates roughly 7% of GDP to transport corridors, ports, and water projects, each consuming silica in concrete and specialty mortars. Malaysia’s third-largest exporter status (USD 132 million in 2024) shows how intra-ASEAN logistics complement domestic mining in meeting contract timelines. Rail-oriented megaprojects stretching from Bangkok to Vientiane channel fresh flows of sand into high-performance precast segments. The Asia-Pacific silica sand market benefits because imported grades make up for local deficits in purity or supply reliability, widening the trade web. Short-term procurement cycles have shifted to multi-year framework agreements, locking in tonnages and pricing formulas for major contractors.

Indonesia’s Silica Downstreaming for Semiconductors

Policy incentives cover tax holidays, power-tariff rebates, and expedited licensing for integrated sand-to-wafer complexes. Java’s proximity to port infrastructure and power grids makes it the logical pilot zone, but Kalimantan’s reserve clusters may later underpin large-scale expansion. Hyper HPQ, requiring impurities below 300 ppm, matches the country’s documented deposit quality of 99.7% SiO₂. Regional partners from Taiwan and South Korea have already tabled feasibility studies for co-investment, signaling that Indonesia could erode China’s current dominance in premium HPQ imports. Long-term, the strategy diversifies supply routes for chip foundries across Asia and raises the floor for HPQ pricing by locking away volumes under strategic off-take agreements.

Restraint Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Illegal and unregulated sand mining curbs | -1.4% | India, Indonesia, Philippines, Vietnam | Short term (≤ 2 years) |

| Substitution by engineered, sand-free building materials | -0.9% | Japan, South Korea, urban China | Medium term (2-4 years) |

| Government drive to consolidate small mines (license cancellations) | -0.7% | China, India, with policy spillover to ASEAN | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Illegal and Unregulated Sand Mining Curbs

Rising enforcement is shrinking unregistered output across riverine deposits, especially in India, where the estimated 52 million-worker cohort exposed to silica dust has spurred sweeping health-and-safety reforms. New exposure limits - 50 µg/m³ for respirable crystalline silica mandate capital upgrades like wet-scrubbing and enclosed conveyors, adding 4-6% to mining opex for compliant operators. In China, authorities canceled thousands of small-scale licenses, reducing projected 2025 supply gaps from 63% to 4% through centrally managed quotas. Such crackdowns eliminate low-cost competition but tighten local availability, reinforcing the Asia-Pacific silica sand market’s reliance on compliant, higher-cost output. Price volatility has already widened between informal spot cargoes and contract-grade supplies.

Substitution by Engineered, Sand-Free Building Materials

Japanese and South Korean construction groups are scaling engineered lumber, geopolymer concrete, and recycled glass aggregates to cut carbon footprints. In premium office builds, these substitutions are displacing modest silica tonnages, particularly where performance or green-building credits offset cost. Nonetheless, bulk infrastructure and commodity concrete maintain their preference for natural silica given its thermal stability, chemical inertness, and cost advantage. Engineered alternatives thus represent a localized threat that trims growth trajectories rather than reversing them. Suppliers mitigate risk by entering specialty fillers and additive markets to diversify revenue away from pure volume metrics.

Segment Analysis

By Grade: Hyper-Purity Ascends Amid Glass Dominance

The glass grade segment captured 63.88% of 2025 shipments, underscoring its role as the backbone of the Asia-Pacific silica sand market. Hyper HPQ, though only a sliver of volume today, is projected to post an 11.12% CAGR, raising its stake in the Asia-Pacific silica sand market size from 2026 onward.

Supply security hinges on automated beneficiation lines, optical sorting, and clean-energy kiln conversions that meet environmental benchmarks. Producers able to certify nuclear-level purity enter the semiconductor chain, while mid-tier suppliers target solar and optics. Blending strategies are emerging, where moderate-purity Indonesian feedstock is upgraded via Japanese chemical leaching, showing how collaboration can capture margin without greenfield development.

Note: Segment shares of all individual segments available upon report purchase

By End-User Industry: Glass Manufacturing Anchors, Semiconductors Accelerate

Glass manufacturing accounted for 43.02% of 2025 regional shipments, expanding at a 7.29% CAGR and cementing leadership in the Asia-Pacific silica sand market. Foundry applications follow as decarbonization mandates spur lightweight EV castings and large-format turbine hubs.

Downstream resilience stems from multiple sub-sectors: architectural glazing, beverage containers, automotive OEM glass, and burgeoning solar-glass lines in China’s Hebei and Anhui provinces. Each additional gigawatt of solar-glass capacity can absorb 180,000 tons of ultra-low-iron sand annually, ensuring structural demand. Semiconductor fabrication, though still a small offtake by tonnage, commands outsize revenues due to HPQ’s 100-fold price premium, placing upward pressure on high-purity supply chains. Paints, ceramics, filtration, and oil and gas collectively smooth demand cycles by spanning multiple economic drivers. As EV adoption accelerates and photovoltaic targets tighten, glass and semiconductor pairings lock in a dual-engine growth pattern resilient to cyclical shocks elsewhere.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

China held a dominant 72.98% slice of the Asia-Pacific silica sand market share in 2025, underpinned by massive float-glass capacity, solar-glass expansions, and an integrated logistics ecosystem. Despite this weight, inventory overhangs in 2024 pushed warehouses to 68.66 million weight cases, prompting margin pressure and faster technology upgrades. The government has shuttered 76% of small mining licenses, steering supply toward larger operators that can meet stricter emissions and occupational-health limits.

India is the fastest-growing geography at 8.43% CAGR, fueled by infrastructure corridors and manufacturing reforms. Diverse deposits across Rajasthan, Andhra Pradesh, and Karnataka ensure regional sourcing flexibility, while foreign direct investment in mining lifted capacity modernization programs through 2025.

Japan and South Korea pivot on value-over-volume, channeling imports into advanced optics and sub-3-nm semiconductor fabs where impurity tolerance sits below 30 ppb. High-purity feedstock is routinely sourced from Australia and the United States under multi-year contracts. The Asia-Pacific silica sand market thus intertwines self-sufficiency aspirations with cross-border interdependencies that equilibrate purity differentials and freight economics.

Competitive Landscape

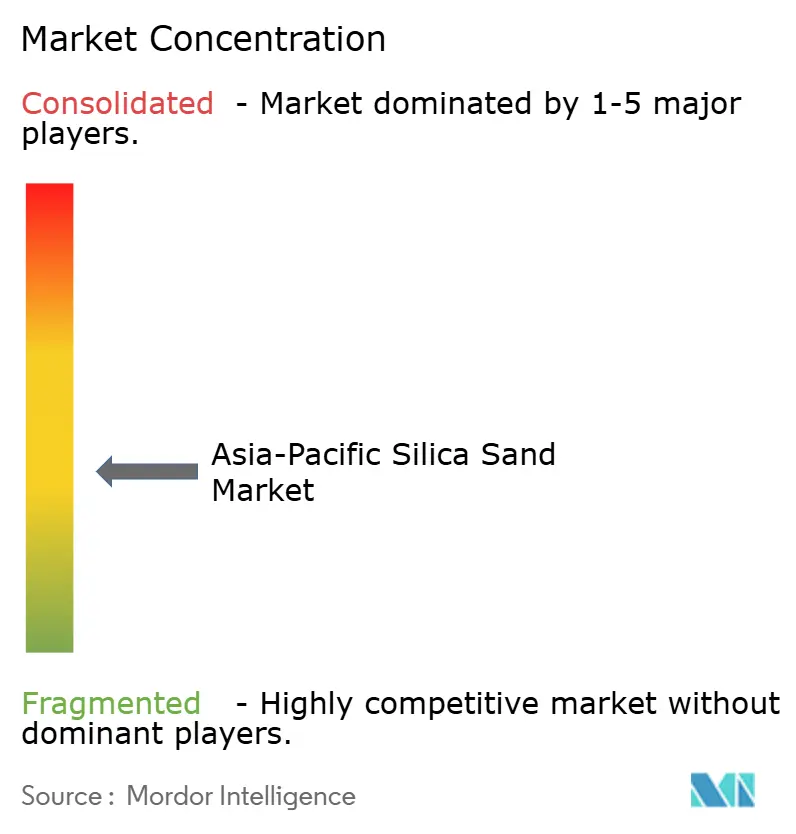

The market is moderately fragmented. Australian developers such as Diatreme secured Major Project Status for the Northern Silica Project in June 2025, streamlining federal approvals and underscoring government backing for export-oriented supply. Indonesian entrants leverage tax holidays and infrastructure grants to climb the value ladder toward wafer-grade HPQ, potentially redrawing procurement patterns for Asian chipmakers by 2030. The Asia-Pacific silica sand market continues to favor scale, integrated logistics, and demonstrated purity, leaving fragmented artisanal diggers at a competitive disadvantage.

Asia-Pacific Silica Sand Industry Leaders

Mitsubishi Corporation

Sibelco

Chongqing Changjiang River Moulding Material Group Co., Ltd.

VRX Silica

Xinyi Golden Ruite Quartz Materials Co., Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Diatreme’s Northern Silica Project was awarded Major Project Status by the Australian Government, unlocking federal facilitation support for permitting.

- December 2024: Xinyi Solar and Xinyi Glass renewed their silica sand agreement for 2025, ensuring continuity of feedstock for float-glass production.

Asia-Pacific Silica Sand Market Report Scope

Silica sand is a chemical compound of silicon and oxygen. It is found in nature and is mined for different end-user industries. Asia-Pacific Silica Sand Market is segmented by end-user industry and geography. By end-user industry, the market is segmented into glass manufacturing, foundry, chemical production, construction, paints and coatings, ceramics and refractories, filtration, oil and gas recovery, and other applications. The report also covers the market sizes and forecasts for the silica sand market in 10 countries across the Asia-Pacific region. The market sizing and forecasts have been done for each segment based on volume (Tons).

By Grade

| Foundry/Smelter Grade |

| Glass Grade Sand |

| Optical Glass Grade |

| Intermediate HPQ |

| Ultra High HPQ |

| Hyper HPQ |

By End-user Industry

| Glass Manufacturing |

| Foundry |

| Chemical Production |

| Construction |

| Paints and Coatings |

| Ceramics and Refractories |

| Filtration |

| Oil and Gas |

| Other End-user Industries |

By Geography

| China |

| India |

| Japan |

| South Korea |

| Indonesia |

| Thailand |

| Malaysia |

| Singapore |

| Philippines |

| Vietnam |

| Rest of Asia-Pacific |

| By Grade | Foundry/Smelter Grade |

| Glass Grade Sand | |

| Optical Glass Grade | |

| Intermediate HPQ | |

| Ultra High HPQ | |

| Hyper HPQ | |

| By End-user Industry | Glass Manufacturing |

| Foundry | |

| Chemical Production | |

| Construction | |

| Paints and Coatings | |

| Ceramics and Refractories | |

| Filtration | |

| Oil and Gas | |

| Other End-user Industries | |

| By Geography | China |

| India | |

| Japan | |

| South Korea | |

| Indonesia | |

| Thailand | |

| Malaysia | |

| Singapore | |

| Philippines | |

| Vietnam | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

What volume do Asia-Pacific glass makers consume yearly?

Glass manufacturers used roughly 78.11 million tons of sand in 2026, accounting for 43.02% of total regional shipments.

Which country supplies most high-purity quartz to Asian chip fabs?

Australia leads, shipping 3 million tons annually from Cape Flattery at 99.93% purity.

How fast is the semiconductor segment growing?

Hyper-purity grades linked to semiconductor demand are forecast to expand at 11.12% CAGR through 2031.

What is the biggest regulatory risk facing miners?

Stricter occupational-health and environmental standards, including 50 µg/m³ dust limits, raise compliance costs.

How did China’s mine-license consolidation affect supply?

Canceling thousands of small licenses cut informal output and shifted market share to large, integrated operations.

Page last updated on: