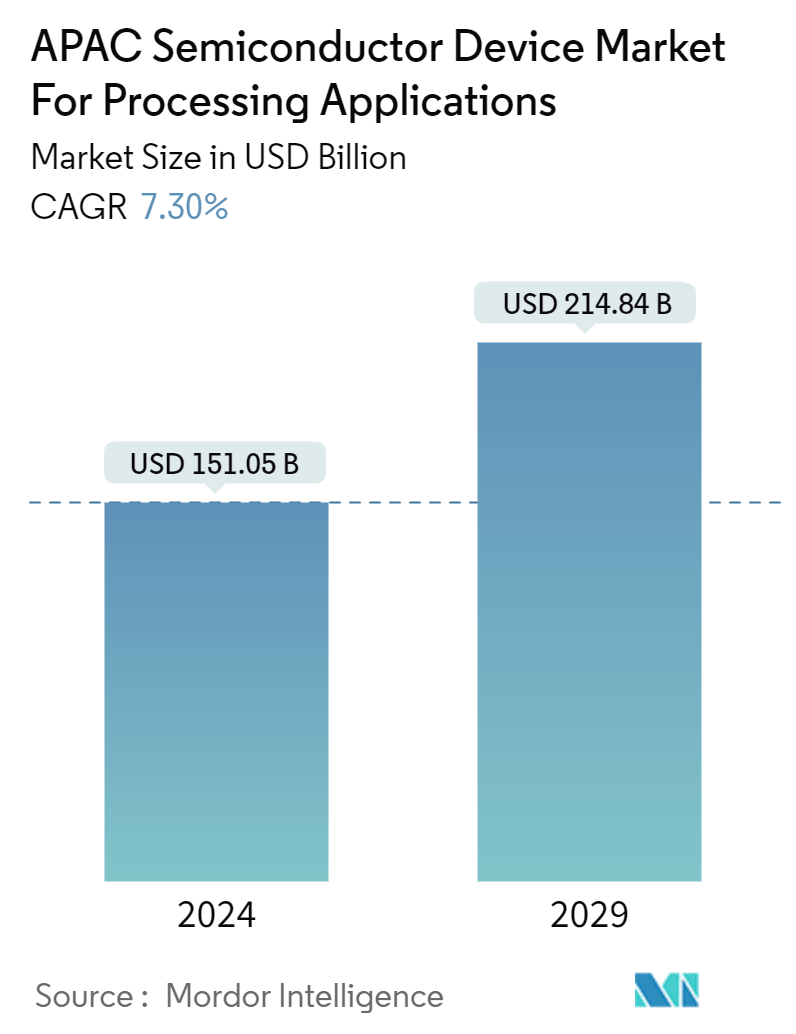

Market Size of APAC Semiconductor Device Industry For Processing Applications

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

| Market Size (2024) | USD 151.05 Billion |

| Market Size (2029) | USD 230.53 Billion |

| CAGR (2024 - 2029) | 7.30 % |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

APAC Semiconductor Device Market Analysis

The APAC Semiconductor Device Market For Processing Applications Industry is expected to grow from USD 151.05 billion in 2024 to USD 214.84 billion by 2029, at a CAGR of 7.30% during the forecast period (2024-2029).

Regional governments launched initiatives to develop the manufacturing and processing industry and recover the growth of semiconductors and manufacturing sectors nationwide. For example, the Japanese government is taking stringent measures to revive its industries, such as manufacturing processes.

- The automation and electrification of manufacturing processes have driven increased demand for semiconductor wafers. Semiconductor ICs with varied functionalities are used in various products, such as infotainment systems, navigation control, HMI, machine vision system, and collision detection systems.

- Moreover, there is enhanced activity from the semiconductor fabrication facilities in Asia-Pacific countries such as China, Singapore, and Korea. Numerous multinational manufacturers of memory direct a large amount of investment into the Chinese semiconductor fabrication market. The country's government initiatives, such as Made in China 2025, significantly support these initiatives. Such initiatives are expected to draw more investments into the country, thus driving the market over the forecast period.

- Moreover, Japan aims to attract overseas companies through financial incentives to secure its chip supplies and address the global shortage. Japan imports significant semiconductors from overseas and wants to build a home supply chain for this technology. During the second pandemic wave, Japan signed off on a JPY 37 billion (USD 0.23 billion) semiconductor research project to develop chip technology in the country with TSMC. About 20 Japanese companies, including Hitachi High-Tech Corp., will work with TSMC on the project, with the Japanese government paying just over half of the cost.

- TSMC formed strategies of opening its first chip plant in Japan as the country pushes to attract more foreign investment into its manufacturing sector. TSMC is considering plans to open a plant in the Kumamoto Prefecture in western Japan, which would help meet the growing demand for image sensors, microcontrollers, and other chips.

- In March 2023, South Korea's parliament approved a bill to boost the country's powerhouse semiconductor industry by giving firms tax breaks to spur investments. The 'K-Chips Act' legislation would increase the tax credit to 15% from the current 8% for major companies investing in manufacturing facilities. At the same time, smaller and medium-sized firms would see the tax break go to 25%, up from 16%. The measure is expected to boost domestic investment for South Korean tech companies such as Samsung Electronics Co. and SK Hynix Inc.

- Further, semiconductors are already Korea's largest export. However, most of that is memory products, NAND Flash, and DRAM memory. The new plan aims to boost the advanced logic chip foundry capacity. Samsung already operates a foundry service with technological capabilities on par with world leader TSMC, but it needs TSMC's volume. SK Hynix has some foundries, but those facilities are far less advanced.

APAC Semiconductor Device Industry Segmentation

The study analyzes the market of semiconductor devices for processing applications in terms of the revenue accrued. For the scope of the study, the report includes devices such as Discrete Semiconductors, Sensors, and Integrated Circuits for the market sizing calculation, and all the other devices, such as passive components, are excluded from the study. The study also covers the activities of major players in the market along with their current strategies, recent developments, and product offerings.

The Asia-Pacific semiconductor device market for processing applications by device type (discrete semiconductors, optoelectronics, sensors, and integrated circuits (analog, logic, memory, and micro (microprocessors, microcontrollers, digital signal processors))) and by country (China, India, Japan, South Korea and Rest of the Asia Pacific). The report offers market forecasts and size in value (USD) for all the above segments.

| By Device Type | ||||||||||

| Discrete Semiconductors | ||||||||||

| Optoelectronics | ||||||||||

| Sensors | ||||||||||

|

| By Country | |

| China | |

| India | |

| Japan | |

| South Korea |

APAC Semiconductor Device Market For Processing Applications Size Summary

The Asia-Pacific semiconductor device market for processing applications is poised for significant growth, driven by government initiatives and increased demand for advanced manufacturing technologies. Regional governments, particularly in Japan, China, and South Korea, are implementing strategies to bolster their semiconductor industries. These include financial incentives, such as tax breaks and investment in research projects, to attract foreign companies and enhance domestic production capabilities. The automation and electrification of manufacturing processes are further propelling the demand for semiconductor wafers and integrated circuits, which are integral to various applications like infotainment systems and machine vision. The market is characterized by active semiconductor fabrication facilities in countries like China, Singapore, and Korea, with substantial investments from multinational manufacturers aiming to capitalize on government support and initiatives like China's Made in China 2025.

The market landscape is competitive and fragmented, with major players such as Intel, Nvidia, Qualcomm, and TSMC focusing on developing customized solutions to meet local demands. Innovations in semiconductor technology, such as Toshiba's silicon carbide MOSFETs and Micron's advanced NAND storage solutions, are setting new industry standards. Additionally, collaborations and expansions, like those by Silvaco and Sony Semiconductor Solutions, are enhancing production capacities and technological advancements. The region's commitment to expanding its semiconductor capabilities is further evidenced by strategic partnerships and investments in new facilities, positioning the Asia-Pacific market as a key player in the global semiconductor industry.

APAC Semiconductor Device Market For Processing Applications Market Size - Table of Contents

-

1. MARKET INSIGHTS

-

1.1 Market Overview

-

1.2 Industry Value Chain Analysis

-

1.3 Technological Trends

-

1.4 Industry Attractiveness - Porter's Five Forces Analysis

-

1.4.1 Threat of New Entrants

-

1.4.2 Bargaining Power of Buyers

-

1.4.3 Bargaining Power of Suppliers

-

1.4.4 Threat of Substitute Products

-

1.4.5 Intensity of Competitive Rivalry

-

-

1.5 Assessment of Impact of COVID-19 on the Market

-

-

2. MARKET SEGMENTATION

-

2.1 By Device Type

-

2.1.1 Discrete Semiconductors

-

2.1.2 Optoelectronics

-

2.1.3 Sensors

-

2.1.4 Integrated Circuits

-

2.1.4.1 Analog

-

2.1.4.2 Logic

-

2.1.4.3 Memory

-

2.1.4.4 Micro

-

2.1.4.4.1 Microprocessors (MPU)

-

2.1.4.4.2 Microcontrollers (MCU)

-

2.1.4.4.3 Digital Signal Processors

-

-

-

-

2.2 By Country

-

2.2.1 China

-

2.2.2 India

-

2.2.3 Japan

-

2.2.4 South Korea

-

-

APAC Semiconductor Device Market For Processing Applications Market Size FAQs

How big is the APAC Semiconductor Device Market For Processing Applications Industry?

The APAC Semiconductor Device Market For Processing Applications Industry size is expected to reach USD 151.05 billion in 2024 and grow at a CAGR of 7.30% to reach USD 230.53 billion by 2029.

What is the current APAC Semiconductor Device Market For Processing Applications Industry size?

In 2024, the APAC Semiconductor Device Market For Processing Applications Industry size is expected to reach USD 151.05 billion.