Market Size of asia-pacific satellite manufacturing Industry

| Icons | Lable | Value |

|---|---|---|

|

|

Study Period | 2017 - 2029 |

|

|

Market Size (2024) | USD 64.71 Billion |

|

|

Market Size (2029) | USD 114.00 Billion |

|

|

Largest Share by Orbit Class | MEO |

|

|

CAGR (2024 - 2029) | 11.99 % |

|

|

Largest Share by Country | China |

|

|

Market Concentration | High |

Major Players |

||

|

|

||

|

*Disclaimer: Major Players sorted in no particular order |

Asia-Pacific Satellite Manufacturing Market Analysis

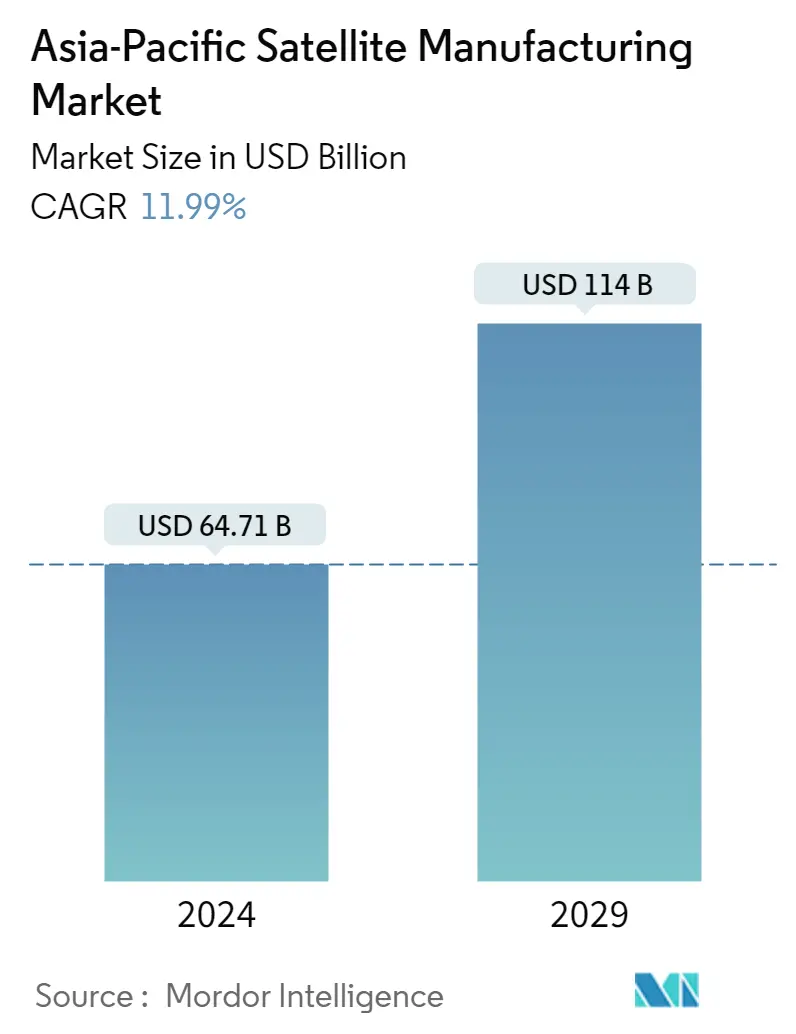

The Asia-Pacific Satellite Manufacturing Market size is estimated at USD 64.71 billion in 2024, and is expected to reach USD 114 billion by 2029, growing at a CAGR of 11.99% during the forecast period (2024-2029).

64.71 Billion

Market Size in 2024 (USD)

114.00 Billion

Market Size in 2029 (USD)

12.07 %

CAGR (2017-2023)

11.99 %

CAGR (2024-2029)

Largest Market by Satellite Mass

75.04 %

value share, above 1000kg, 2022

Large satellites have a higher demand owing to their applications, such as satellite radio, communications, remote sensing, planetary security, and weather forecasting.

Largest Market by Application

60.14 %

value share, Communication, 2022

Governments, space agencies, defense agencies, private defense contractors, and private space industry players are emphasizing the enhancement of the communication network capabilities for various public and military reconnaissance applications.

Largest Market by Orbit Class

72.37 %

value share, MEO, 2022

MEO satellites are increasingly being adopted in modern communication technologies as they play an important role in communication and earth observation applications in the region.

Largest Market by Propulsion Tech

73.93 %

value share, Liquid Fuel, 2022

Because of its high efficiency, controllability, reliability, and long lifespan, liquid fuel-based propulsion technology is becoming an ideal choice for space missions. It can be used in various orbit classes for satellites.

Leading Market Player

92.27 %

market share, China Aerospace Science and Technology Corporation (CASC), 2022

China Aerospace Science and Technology Corporation (CASC) is the largest player in the market. It offers a diverse range of launch vehicles and adopts a competitive pricing strategy to attract customers globally.

MEO satellites are driving the segment's demand

- Asia-Pacific has seen a significant increase in the demand for satellite buses to accommodate a wide range of satellite orbits, including low Earth orbit (LEO), medium Earth orbit (MEO), and geostationary Earth orbit (GEO). This demand has been driven by the growing need for satellite-based communication, navigation, and remote sensing services.

- LEO satellites have become increasingly popular for a wide range of applications, including Earth observation, weather forecasting, and communication. The demand for LEO satellites has been particularly strong in China, where companies such as Spacety and Chang Guang Satellite Technology Co. Ltd offer satellite buses for LEO missions. China has been active in this region with the launch of a series of Gaofen satellites.

- MEO satellites have become increasingly important for global navigation and positioning services such as GPS and Galileo. In the region, Japan has been a leader in this area, with the launch of the Michibiki series of MEO navigation satellites. China has also been investing in MEO satellites with the launch of the Beidou navigation system.

- GEO satellites are particularly important for communication and broadcasting services, such as television and the Internet. The demand for GEO satellites has been particularly strong in India, where companies such as ISRO and Antrix Corporation Ltd have been developing advanced satellite buses for communication missions. China has also been investing heavily in GEO satellites, with the launch of the Zhongxing series of communication satellites.

China is expected to witness significant growth

- Asia-Pacific has emerged as a leading satellite market in recent years. The satellite market is projected to grow rapidly, driven by increasing demand for Earth observation, communication, and scientific research. During 2017-2022, more than 450 satellites were manufactured and launched by various regional commercial and military operators.

- China has established itself as a major player in the global satellite market, launching numerous microsatellites for various applications, including Earth observation, remote sensing, and communication. The country's ambitious space program and growing demand for satellite services are expected to drive further growth of the microsatellite market. During the historic period, the country launched around 370 satellites.

- India has also been making significant strides in the satellite market, with the country's space agency, ISRO, launching a series of microsatellites for various applications. One of the key drivers of the demand for launching remote sensing satellites in India is the country's focus on national development and economic growth. During the historic period, the country manufactured and launched 26 satellites.

- Japan has been actively involved in the development of microsatellites for various applications. Japan's advanced technology expertise and its commitment to space exploration are expected to drive growth in the microsatellite market. Japan's space program is led by the Japan Aerospace Exploration Agency (JAXA), which develops and launches various satellites. During the historic period, the country manufactured and launched around 45 satellites.

Asia-Pacific Satellite Manufacturing Industry Segmentation

Communication, Earth Observation, Navigation, Space Observation, Others are covered as segments by Application. 10-100kg, 100-500kg, 500-1000kg, Below 10 Kg, above 1000kg are covered as segments by Satellite Mass. GEO, LEO, MEO are covered as segments by Orbit Class. Commercial, Military & Government are covered as segments by End User. Propulsion Hardware and Propellant, Satellite Bus & Subsystems, Solar Array & Power Hardware, Structures, Harness & Mechanisms are covered as segments by Satellite Subsystem. Electric, Gas based, Liquid Fuel are covered as segments by Propulsion Tech. Australia, China, India, Japan, New Zealand, Singapore, South Korea are covered as segments by Country.

- Asia-Pacific has seen a significant increase in the demand for satellite buses to accommodate a wide range of satellite orbits, including low Earth orbit (LEO), medium Earth orbit (MEO), and geostationary Earth orbit (GEO). This demand has been driven by the growing need for satellite-based communication, navigation, and remote sensing services.

- LEO satellites have become increasingly popular for a wide range of applications, including Earth observation, weather forecasting, and communication. The demand for LEO satellites has been particularly strong in China, where companies such as Spacety and Chang Guang Satellite Technology Co. Ltd offer satellite buses for LEO missions. China has been active in this region with the launch of a series of Gaofen satellites.

- MEO satellites have become increasingly important for global navigation and positioning services such as GPS and Galileo. In the region, Japan has been a leader in this area, with the launch of the Michibiki series of MEO navigation satellites. China has also been investing in MEO satellites with the launch of the Beidou navigation system.

- GEO satellites are particularly important for communication and broadcasting services, such as television and the Internet. The demand for GEO satellites has been particularly strong in India, where companies such as ISRO and Antrix Corporation Ltd have been developing advanced satellite buses for communication missions. China has also been investing heavily in GEO satellites, with the launch of the Zhongxing series of communication satellites.

| Application | |

| Communication | |

| Earth Observation | |

| Navigation | |

| Space Observation | |

| Others |

| Satellite Mass | |

| 10-100kg | |

| 100-500kg | |

| 500-1000kg | |

| Below 10 Kg | |

| above 1000kg |

| Orbit Class | |

| GEO | |

| LEO | |

| MEO |

| End User | |

| Commercial | |

| Military & Government | |

| Other |

| Satellite Subsystem | |

| Propulsion Hardware and Propellant | |

| Satellite Bus & Subsystems | |

| Solar Array & Power Hardware | |

| Structures, Harness & Mechanisms |

| Propulsion Tech | |

| Electric | |

| Gas based | |

| Liquid Fuel |

| Country | |

| Australia | |

| China | |

| India | |

| Japan | |

| New Zealand | |

| Singapore | |

| South Korea |

Asia-Pacific Satellite Manufacturing Market Size Summary

The Asia-Pacific satellite manufacturing market is experiencing robust growth, driven by increasing demand for satellite-based services such as communication, navigation, and remote sensing. The region has seen a surge in the production of satellite buses to support various orbits, including low Earth orbit (LEO), medium Earth orbit (MEO), and geostationary Earth orbit (GEO). China, Japan, and India are at the forefront of this expansion, with significant investments and developments in satellite technology. China's active space program, including the launch of Gaofen and Beidou satellites, highlights its commitment to enhancing its satellite capabilities. Similarly, Japan's Michibiki series and India's ISRO initiatives underscore the region's focus on advancing satellite manufacturing and deployment.

The market is characterized by a high level of consolidation, with a few key players dominating the landscape. Companies such as Axelspace Corporation, Chang Guang Satellite Technology Co. Ltd, and the Japan Aerospace Exploration Agency (JAXA) are leading the charge in satellite production. The region's potential is further bolstered by the growing interest in nano and microsatellites, with countries like China, India, and Japan investing in these technologies to reduce launch costs and enhance mission capabilities. As the demand for satellite services continues to rise, the Asia-Pacific region is poised to become a significant player in the global satellite manufacturing industry, with ongoing investments in infrastructure and technology development.

Asia-Pacific Satellite Manufacturing Market Size - Table of Contents

-

1. MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2029 and analysis of growth prospects)

-

1.1 Application

-

1.1.1 Communication

-

1.1.2 Earth Observation

-

1.1.3 Navigation

-

1.1.4 Space Observation

-

1.1.5 Others

-

-

1.2 Satellite Mass

-

1.2.1 10-100kg

-

1.2.2 100-500kg

-

1.2.3 500-1000kg

-

1.2.4 Below 10 Kg

-

1.2.5 above 1000kg

-

-

1.3 Orbit Class

-

1.3.1 GEO

-

1.3.2 LEO

-

1.3.3 MEO

-

-

1.4 End User

-

1.4.1 Commercial

-

1.4.2 Military & Government

-

1.4.3 Other

-

-

1.5 Satellite Subsystem

-

1.5.1 Propulsion Hardware and Propellant

-

1.5.2 Satellite Bus & Subsystems

-

1.5.3 Solar Array & Power Hardware

-

1.5.4 Structures, Harness & Mechanisms

-

-

1.6 Propulsion Tech

-

1.6.1 Electric

-

1.6.2 Gas based

-

1.6.3 Liquid Fuel

-

-

1.7 Country

-

1.7.1 Australia

-

1.7.2 China

-

1.7.3 India

-

1.7.4 Japan

-

1.7.5 New Zealand

-

1.7.6 Singapore

-

1.7.7 South Korea

-

-

Asia-Pacific Satellite Manufacturing Market Size FAQs

How big is the Asia-Pacific Satellite Manufacturing Market?

The Asia-Pacific Satellite Manufacturing Market size is expected to reach USD 64.71 billion in 2024 and grow at a CAGR of 11.99% to reach USD 114.00 billion by 2029.

What is the current Asia-Pacific Satellite Manufacturing Market size?

In 2024, the Asia-Pacific Satellite Manufacturing Market size is expected to reach USD 64.71 billion.