Market Size of asia-pacific satellite launch vehicle Industry

| Icons | Lable | Value |

|---|---|---|

|

|

Study Period | 2017 - 2029 |

|

|

Market Size (2024) | USD 1.94 Billion |

|

|

Market Size (2029) | USD 5.13 Billion |

|

|

Largest Share by Orbit Class | GEO |

|

|

CAGR (2024 - 2029) | 21.47 % |

|

|

Largest Share by Country | China |

|

|

Market Concentration | High |

Major Players |

||

|

|

||

|

*Disclaimer: Major Players sorted in no particular order |

Asia-Pacific Satellite Launch Vehicle Market Analysis

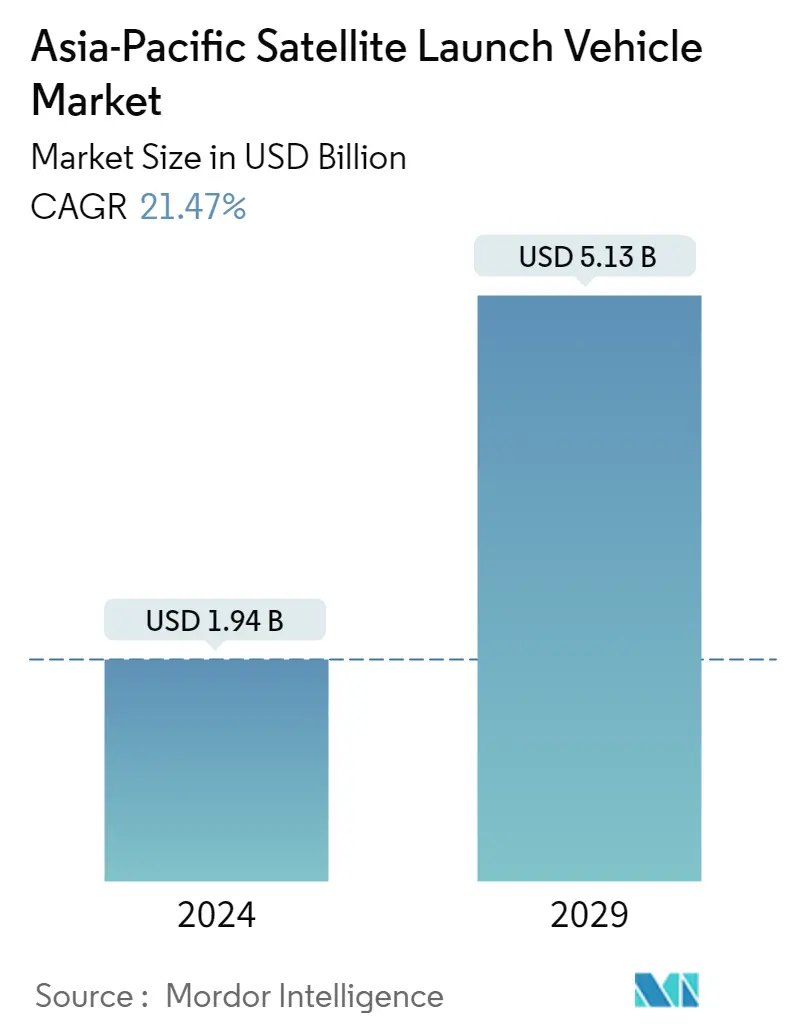

The Asia-Pacific Satellite Launch Vehicle Market size is estimated at USD 1.94 billion in 2024, and is expected to reach USD 5.13 billion by 2029, growing at a CAGR of 21.47% during the forecast period (2024-2029).

1.94 Billion

Market Size in 2024 (USD)

5.13 Billion

Market Size in 2029 (USD)

-0.03 %

CAGR (2017-2023)

21.47 %

CAGR (2024-2029)

Largest Market by Launch Vehicle MTOW

51.11 %

value share, Medium, 2022

The demand for medium launch vehicles is fueled by the granting of multi-year contracts by government and commercial end users to launch vehicle manufacturers and launch service providers.

Fastest-Growing Market by Orbit class

25.96 %

Projected CAGR, LEO, 2023-2029

Government initiatives pertaining to LEO satellites and their numerous uses, such as communications, Earth observation, navigation, and military surveillance, will aid in the growth of LEO satellites.

Largest Market by Orbit Class

53.59 %

value share, GEO, 2022

The increasing demand from governments for military applications is one of the major factors driving the demand for GEO satellites.

Leading Market Player

87.98 %

market share, China Aerospace Science and Technology Corporation (CASC), 2022

China Aerospace Science and Technology Corporation (CASC) is the largest player in the market. It offers a diverse range of launch vehicles and adopts a competitive pricing strategy to attract customers globally.

Second Leading Market Player

10.88 %

market share, Indian Space Research Organisation (ISRO), 2022

ISRO is a major constituent of the Department of Space (DOS), Government of India. It's satellite products and services are being used by Central Government, State Governments, Quasi Governmental Organisations, NGOs and the private sector, therefore enabling to occupy a second largest share in the market.

The demand for orbital launch systems in Asia-Pacific is driven by LEO satellites

- In Asia-Pacific, the demand for LEO-based orbital launch systems has been on the rise. Countries such as China, India, Japan, South Korea, Australia, and Taiwan have been actively developing and utilizing orbital launch systems to deploy satellites into LEO for various applications. For instance, China's Long March series of rockets, India's PSLV and GSLV, Japan's H-IIA and H3 rockets, and South Korea's Korea Space Launch Vehicle-II (KSLV-II) have been used to launch satellites for Earth observation, remote sensing, weather monitoring, and communication purposes in LEO.

- MEO is well-suited for applications such as GNSS and satellite-based communications. In the region, China's Long March 3B and Long March 3B/G2 are some of the launch systems being developed or utilized by countries in the region to deploy satellites into MEO. These satellites provide services such as satellite-based navigation systems like the BeiDou Navigation Satellite System (BDS) developed by China, communication services for remote and rural areas, maritime and aviation industries, and disaster management.

- GEO is ideal for applications such as telecommunications, broadcasting, and meteorological observations, as satellites in GEO appear to be stationary relative to Earth. China's Long March 3B/G2, India's GSLV Mk III, Japan's H3, and South Korea's KSLV-II are some launch systems utilized for launching satellites into GEO for telecommunications, broadcasting, and meteorological observation purposes. Overall, the market is expected to grow in the coming years by 219% in 2029 compared to 2023.

China's satellite industry is expected to witness significant growth

- Asia-Pacific has emerged as a leading market for satellites in recent years. This market is projected to grow rapidly, driven by increasing demand for Earth observation, communication, and scientific research.

- China is stepping up to become a dominant space power. Hence, in October 2020, the country unveiled its ambitious moon mission slated for 2024 and beyond. On this note, China planned to launch a mission to collect samples from the far side of the moon by the end of 2020.

- The Indian Space Research Organisation (ISRO) is working on its Small Satellite Launch Vehicle (SSLV). The SSLV is a three-stage launch platform powered entirely by solid fuel, with a lift-off mass of 120 metric tons and capable of lifting 500 kg to LEO and 300 kg to the sun-synchronous orbit. The first static fire test of SS1 conducted in March 2021 was unsuccessful. The first demonstration flight was expected to take place in October 2021.

- NewSpace India Limited, a newly formed commercial arm of the Indian space agency, is tasked with enabling the Indian industry to scale up high-technology manufacturing and production base for Indian space efforts. It will be involved in the manufacture of SSLV in collaboration with the private sector.

- South Korea's space program has seen slow progress as other countries are reluctant to transfer core technologies. In February 2021, the Ministry of Science and ICT announced a space budget of USD 553.1 million for manufacturing satellites, rockets, and other key space equipment. Such initiatives will drive the demand for launch vehicles in Asia-Pacific during the forecast period.

Asia-Pacific Satellite Launch Vehicle Industry Segmentation

GEO, LEO, MEO are covered as segments by Orbit Class. Heavy, Light, Medium are covered as segments by Launch Vehicle Mtow. China, India, New Zealand are covered as segments by Country.

- In Asia-Pacific, the demand for LEO-based orbital launch systems has been on the rise. Countries such as China, India, Japan, South Korea, Australia, and Taiwan have been actively developing and utilizing orbital launch systems to deploy satellites into LEO for various applications. For instance, China's Long March series of rockets, India's PSLV and GSLV, Japan's H-IIA and H3 rockets, and South Korea's Korea Space Launch Vehicle-II (KSLV-II) have been used to launch satellites for Earth observation, remote sensing, weather monitoring, and communication purposes in LEO.

- MEO is well-suited for applications such as GNSS and satellite-based communications. In the region, China's Long March 3B and Long March 3B/G2 are some of the launch systems being developed or utilized by countries in the region to deploy satellites into MEO. These satellites provide services such as satellite-based navigation systems like the BeiDou Navigation Satellite System (BDS) developed by China, communication services for remote and rural areas, maritime and aviation industries, and disaster management.

- GEO is ideal for applications such as telecommunications, broadcasting, and meteorological observations, as satellites in GEO appear to be stationary relative to Earth. China's Long March 3B/G2, India's GSLV Mk III, Japan's H3, and South Korea's KSLV-II are some launch systems utilized for launching satellites into GEO for telecommunications, broadcasting, and meteorological observation purposes. Overall, the market is expected to grow in the coming years by 219% in 2029 compared to 2023.

| Orbit Class | |

| GEO | |

| LEO | |

| MEO |

| Launch Vehicle Mtow | |

| Heavy | |

| Light | |

| Medium |

| Country | |

| China | |

| India | |

| New Zealand |

Asia-Pacific Satellite Launch Vehicle Market Size Summary

The Asia-Pacific Satellite Launch Vehicle Market is experiencing significant growth, driven by increasing demand for satellite deployment in low Earth orbit (LEO), medium Earth orbit (MEO), and geostationary orbit (GEO). Countries such as China, India, Japan, South Korea, Australia, and Taiwan are actively developing and utilizing advanced orbital launch systems to support various applications, including Earth observation, communication, and scientific research. The region has seen the emergence of major players like China Aerospace Science and Technology Corporation (CASC), Indian Space Research Organisation (ISRO), and Japan Aerospace Exploration Agency (JAXA), which have developed reliable launch vehicles such as the Long March series, PSLV, and H-IIA rockets. These developments are further supported by government investments and initiatives aimed at enhancing domestic space capabilities and fostering collaboration with commercial entities.

The market is characterized by a consolidated landscape, with a few key players dominating the industry. The demand for satellite launch vehicles is fueled by ambitious projects, such as national satellite internet constellations and lunar missions, particularly by China and India. South Korea and Japan are also making strides in expanding their space programs, with significant budgets allocated for developing next-generation launch vehicles and advancing space technology. The market's growth trajectory is supported by ongoing research and development efforts, as well as strategic partnerships aimed at scaling up high-technology manufacturing and production capabilities. As a result, the Asia-Pacific region is poised to become a leading hub for satellite launch activities, with a robust pipeline of projects and a strong focus on innovation and technological advancement.

Asia-Pacific Satellite Launch Vehicle Market Size - Table of Contents

-

1. MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2029 and analysis of growth prospects)

-

1.1 Orbit Class

-

1.1.1 GEO

-

1.1.2 LEO

-

1.1.3 MEO

-

-

1.2 Launch Vehicle Mtow

-

1.2.1 Heavy

-

1.2.2 Light

-

1.2.3 Medium

-

-

1.3 Country

-

1.3.1 China

-

1.3.2 India

-

1.3.3 New Zealand

-

-

Asia-Pacific Satellite Launch Vehicle Market Size FAQs

How big is the Asia-Pacific Satellite Launch Vehicle Market?

The Asia-Pacific Satellite Launch Vehicle Market size is expected to reach USD 1.94 billion in 2024 and grow at a CAGR of 21.47% to reach USD 5.13 billion by 2029.

What is the current Asia-Pacific Satellite Launch Vehicle Market size?

In 2024, the Asia-Pacific Satellite Launch Vehicle Market size is expected to reach USD 1.94 billion.