Market Overview

| Study Period | 2018 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 46.95 Billion |

| Market Size (2030) | USD 67.35 Billion |

| Growth Rate (2025 - 2030) | 7.49% CAGR |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Asia-Pacific Ready to Drink Tea Market Analysis by Mordor Intelligence

The Asia-Pacific Ready to Drink Tea Market size is estimated at 46.95 billion USD in 2025, and is expected to reach 67.35 billion USD by 2030, growing at a CAGR of 7.49% during the forecast period (2025-2030).

The Asia-Pacific ready-to-drink tea market is experiencing a significant transformation driven by changing consumer preferences and lifestyle patterns. The region's deep-rooted cultural affinity for traditional tea variants has evolved to embrace convenient, ready-to-drink formats that align with modern, fast-paced lifestyles. This shift is particularly evident in the digital retail space, where by June 2023, China alone reported approximately 884 million active online shoppers, highlighting the growing importance of e-commerce channels in beverage distribution. The convergence of traditional tea culture with modern consumption patterns has led manufacturers to innovate in both product formulation and distribution strategies.

Health consciousness has emerged as a pivotal factor shaping the RTD tea landscape, with manufacturers responding to growing consumer awareness about wellness and nutrition. Recent market data indicates that approximately 40.2% of the Asia-Pacific population was classified as overweight or obese in 2022, driving demand for healthier beverage alternatives. This health-conscious trend has catalyzed innovation in the sugar-free segment, with a notable 65.69% of Chinese consumers having tried sugar-free tea variants by 2023. Manufacturers are increasingly focusing on developing products with reduced sugar content, natural ingredients, and functional beverage benefits to meet these evolving consumer preferences.

Product innovation and diversification have become key strategies in the market, with companies continuously introducing new flavors and variants to maintain consumer interest. Japan exemplifies this trend, with the market featuring approximately 700 tea drink variants in 2022 and introducing over 100 new products annually. This proliferation of options spans traditional green tea to innovative fusion beverages, incorporating local ingredients and addressing specific functional benefits. The industry has witnessed a particular surge in premium tea and specialized offerings, catering to increasingly sophisticated consumer palates.

The market is experiencing a notable shift toward sustainable and clean-label products, reflecting growing environmental consciousness among consumers. In China alone, over 55,000 food products carried organic labels in 2022, indicating a strong preference for natural and sustainably produced soft drink beverages. This trend has prompted manufacturers to invest in eco-friendly packaging solutions and transparent supply chains. Companies are increasingly highlighting their use of natural ingredients, sustainable sourcing practices, and environmentally responsible packaging, responding to consumer demands for both product quality and environmental stewardship.

Asia-Pacific Ready to Drink Tea Market Trends and Insights

The convenience associated with RTD tea beverages boosts the segment sales

- People tend to consume RTD tea as a healthier alternative to sugary drinks or between meals. Emerging countries like India, China, and Singapore among others are a few of the major markets for RTD tea.

- Rising health concerns related to high sugar intake have boosted the demand for healthier RTD drinks including RTD tea. In response to this evolving consumer preference for sugar reduction, manufacturers have been introducing sugar-free and reduced-sugar alternatives.

- In the Asian market, price competitiveness is the key. In the case of smaller or newer RTD tea brands, consumers are not willing to spend extra to try the new brand. Thereby, manufacturers are citing a price at par with available brands.

- Green tea, commonly consumed in the region is known for potential anti-inflammatory and heart health benefits. Likewise, other variants like chamomile tea, hibiscus tea, jasmine tea, and others are often associated with calming effects and may support digestion.

Understand The Key Trends Shaping This Market

Download PDF

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT

- Companies are introducing a range of unique flavors, as well as exploring innovative brewing techniques and herbal infusions to cater to diverse consumer preferences

- Master Kong's commitment to product innovation, including the launching of healthier options and premium offerings, allowed the brand to sustain in a health-conscious market

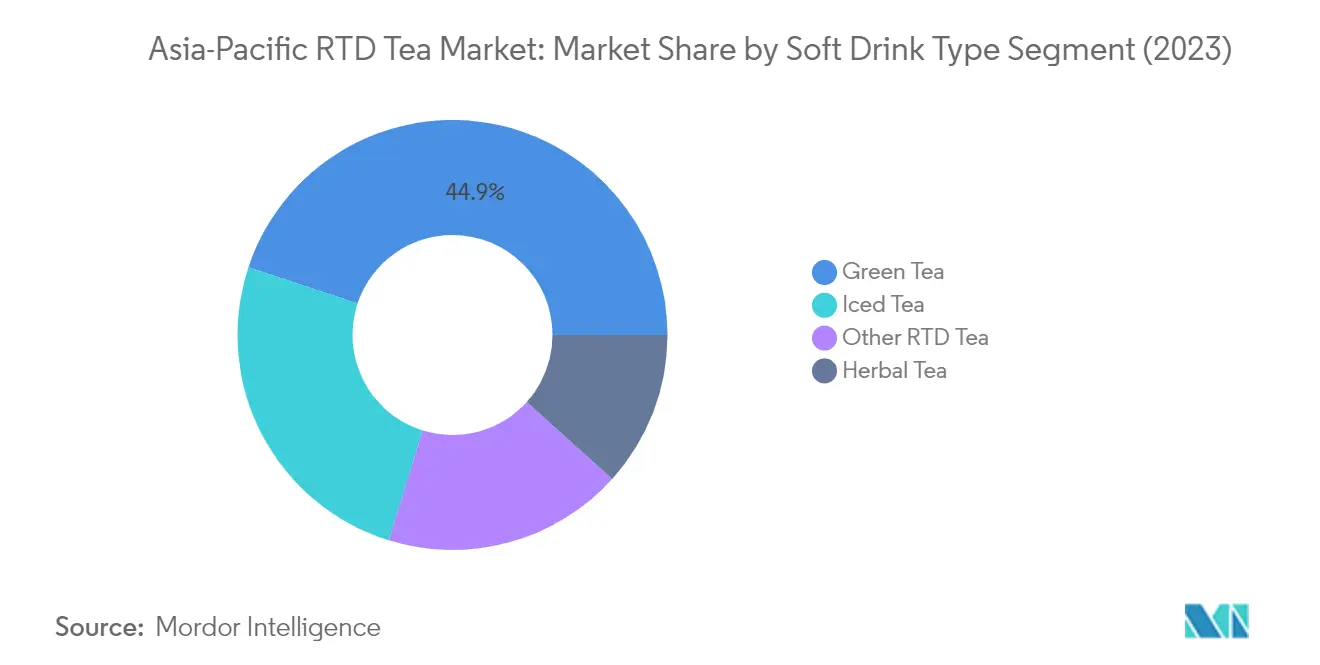

Segment Analysis: Soft Drink Type

Green Tea Segment in Asia-Pacific RTD Tea Market

Green tea dominates the Asia-Pacific ready-to-drink (RTD) tea market, commanding approximately 45% of the market share in 2024. This significant market position is attributed to the deep-rooted cultural significance of green tea in Asian countries, particularly in China, Japan, and India. The segment's growth is primarily driven by increasing health consciousness among consumers, as green tea is perceived to aid in preventing various chronic diseases, including cancer, liver cirrhosis, obesity, and high blood pressure. Japanese consumers, in particular, show a strong preference for RTD green tea, with the country consuming around 80,000 tons annually. Manufacturers are responding to this demand by introducing innovative flavors and formulations, including sugar-free variants and unique blends incorporating ingredients like tulsi, jasmine, lemon, mint, peach, and honey.

Herbal Tea Segment in Asia-Pacific RTD Tea Market

The herbal tea segment is experiencing remarkable growth in the Asia-Pacific RTD tea market, projected to achieve approximately 8% growth during 2024-2029. This surge is driven by increasing consumer awareness of the health benefits associated with herbal tea consumption, including anti-inflammatory and antioxidant properties. Manufacturers are capitalizing on this trend by introducing innovative herbal tea blends that incorporate traditional medicinal ingredients and natural flavors. The segment's growth is further supported by the rising demand for caffeine-free alternatives and functional beverages that offer specific health benefits. Companies are also focusing on developing premium herbal tea variants with unique ingredient combinations and enhanced functional properties to cater to health-conscious consumers.

Remaining Segments in Soft Drink Type

The iced tea and other RTD tea segments continue to play vital roles in the Asia-Pacific market. Iced tea maintains its position as a popular choice, particularly during warmer months, with manufacturers introducing various fruit-infused variants and low-sugar options to meet evolving consumer preferences. The other RTD tea segment, which includes black tea, functional tea, and innovative flavored tea blends, contributes to market diversity by offering unique flavor profiles and functional benefits. These segments are characterized by continuous product innovation, with manufacturers focusing on developing new flavors, functional ingredients, and convenient packaging formats to attract different consumer demographics.

Segment Analysis: Packaging Type

PET Bottles Segment in Asia-Pacific RTD Tea Market

PET bottles dominate the Asia-Pacific ready-to-drink (RTD) tea packaging landscape, commanding approximately 72% market share in 2024. This dominance can be attributed to several key advantages that PET bottles offer over other packaging types. Their lightweight nature, durability, and cost-effectiveness make them particularly appealing to both manufacturers and consumers. PET bottles are especially valued for their ability to effectively block UVA radiation below 315 nm, which helps preserve the beverage's quality and functional ingredients. The segment's strong position is further reinforced by the material's recyclability and its ability to maintain product integrity during transportation and storage. Manufacturers are increasingly incorporating innovative designs and sustainable practices, with companies like Suntory Group committing to adopt 100% sustainable PET bottles made from plant-based materials by 2030.

Glass Bottles Segment in Asia-Pacific RTD Tea Market

The glass bottle segment is experiencing remarkable growth in the Asia-Pacific RTD tea market, projected to expand at approximately 9% CAGR from 2024 to 2029. This growth is primarily driven by increasing environmental consciousness among consumers and the material's superior preservation qualities. Glass bottles are gaining popularity due to their infinite recyclability and ability to maintain the beverage's original taste and quality without any chemical interaction. The segment's growth is particularly strong in Japan, where the country's robust glass bottle production infrastructure and impressive recycling rate of around 70% are supporting expansion. Manufacturers are responding to this trend by introducing premium RTD tea variants in glass packaging, emphasizing both sustainability and product quality. The segment is also benefiting from technological advancements in glass manufacturing that have resulted in lighter and more durable bottles while maintaining their premium appeal.

Remaining Segments in Packaging Type

Metal cans and aseptic packages represent significant segments in the Asia-Pacific RTD tea packaging market, each offering unique advantages to manufacturers and consumers. Canned tea is valued for its excellent barrier properties, durability, and ability to maintain beverage freshness, while also providing effective protection against light and oxygen. The aseptic packaging segment has gained traction due to its ability to preserve beverage quality without refrigeration, making it particularly suitable for regions with limited cold chain infrastructure. Both segments are witnessing continuous innovations in terms of design, functionality, and sustainability features, with manufacturers focusing on reducing material usage while maintaining package integrity. These packaging types are particularly popular in specific distribution channels, with canned tea finding favor in vending machines and convenience stores, while aseptic packages are preferred in supermarkets and hypermarkets.

Segment Analysis: Distribution Channel

Off-trade Segment in Asia-Pacific RTD Tea Market

The off-trade channel maintains its dominant position in the Asia-Pacific ready-to-drink tea market, with supermarkets leading the distribution landscape by commanding approximately 46% market share in 2024. This dominance can be attributed to several factors, including the extensive product variety and competitive pricing offered by supermarket chains. The segment's strength is further reinforced by the strategic positioning of RTD tea products near checkout counters and high-traffic areas, maximizing visibility and impulse purchases. Convenience stores contribute significantly to the off-trade channel's success, accounting for nearly 27% of sales, while the emergence of online retail platforms has created additional growth opportunities. The off-trade channel's success is also driven by various promotional strategies, including bulk purchase discounts, loyalty programs, and seasonal offers that attract price-conscious consumers.

On-trade Segment in Asia-Pacific RTD Tea Market

The on-trade channel is experiencing remarkable growth in the Asia-Pacific RTD tea market, projected to expand at approximately 10% CAGR from 2024 to 2029. This growth is primarily driven by the increasing integration of RTD tea beverages into restaurant and café menus, particularly targeting health-conscious consumers seeking alternatives to sugary carbonated tea drinks. The segment's expansion is further supported by the rising number of cafes and restaurants across the region, with Japan alone hosting over 174,000 cafes operated by around 5,000 companies. The growth is also fueled by significant investments in the HoReCa (Hotel/Restaurant/Café) segment by RTD tea companies, who are introducing innovative flavors and functional variants to capture a larger market share. The segment's appeal is enhanced by the growing popularity of specialty tea experiences and the increasing consumer preference for premium RTD tea offerings in dining establishments.

Asia-Pacific Ready to Drink Tea Market Geography Segment Analysis

Ready to Drink Tea Market in China

China dominates the Asia-Pacific Chinese tea market, commanding approximately 41% of the market value in 2024. The country's fast-paced urban lifestyle has been instrumental in fueling the demand for on-the-go beverages like ready-to-drink tea. Chinese consumers exhibit a distinctive preference for diverse RTD tea flavors, ranging from traditional green and black teas to jasmine, herbal blends, and innovative fusions. The increasing health consciousness among consumers has led to a notable shift towards sugar-free and reduced-sugar RTD tea options. Major brands are responding to this trend by leveraging natural sweeteners like Momordica fruit and highlighting the absence of additives, while some are turning to artificial sweeteners like erythritol as sugar substitutes. The market is further characterized by the rising popularity of RTD teas infused with traditional Chinese ingredients and tea-based alcoholic beverages, reflecting the fusion of traditional tea culture with modern consumption patterns.

Ready to Drink Tea Market in India

India's RTD tea market is poised for remarkable expansion, with projections indicating a growth rate of approximately 11% from 2024 to 2029. Despite tea being a staple beverage with around 80% of the population consuming it traditionally, the RTD segment is witnessing unprecedented growth, particularly among the younger demographic influenced by global trends. The market's evolution is being shaped by the increasing workforce participation, busier lifestyles, and a growing preference for convenient food and beverage options. Manufacturers are actively collaborating with cloud kitchens and food delivery apps to enhance their market presence, while simultaneously expanding their footprint across major city airports throughout India. The rising health and wellness consciousness among consumers has led to increased demand for RTD teas perceived to offer health benefits, such as herbal infusions, antioxidants, and natural ingredients with low sugar content.

Ready to Drink Tea Market in Japan

Japan's Japanese tea market exemplifies the perfect blend of tradition and innovation, with Japanese households demonstrating strong consumption patterns for these convenient beverages. The market is characterized by a diverse range of bottled varieties, including bottled tea, green tea, black tea, barley (mugi) tea, and innovative blended teas. Notable brands like Ito En's Oi Ocha and Coca-Cola Japan's Ayataka have established strong market positions through continuous product innovation and quality focus. The country's thriving café culture has been instrumental in driving demand, particularly among younger consumers. The market's sophistication is evident in its product development, with manufacturers introducing low-sugar or sugar-free RTD tea options to cater to health-conscious consumers. The introduction of unique variants, such as Asahi's unsweetened bottled green tea crafted from slightly withered tea leaves, demonstrates the market's commitment to innovation while maintaining traditional taste preferences.

Ready to Drink Tea Market in Australia

Australia's RTD tea market has emerged as a dynamic segment within the beverage industry, particularly resonating with the country's fast-paced lifestyle and health-conscious consumers. The market is witnessing significant transformation, driven by the younger demographic's increasing preference for the perceived health benefits of tea over coffee. Manufacturers have responded by introducing a wide array of flavors and blends, including unique and exotic profiles and innovative combinations. The presence of RTD teas across various retail channels, spanning supermarkets, convenience stores, and cafes, underscores the rising interest in specialty and premium tea experiences. Marketing strategies have evolved to embrace digital platforms, influencer collaborations, and interactive campaigns, reflecting the market's adaptation to modern consumer engagement preferences. The growing health consciousness among Australian consumers has fueled the demand for products with clean labels, highlighting natural ingredients and avoiding artificial additives.

Ready to Drink Tea Market in Other Countries

The RTD tea market across other Asia-Pacific countries, including South Korea, Indonesia, Malaysia, Vietnam, and Thailand, exhibits diverse consumption patterns and preferences. These markets are characterized by unique cultural influences on tea consumption and varying levels of market maturity. South Korea's market is driven by innovative product developments and health-conscious consumers, while Indonesia's market benefits from its rich tea cultivation heritage and growing urban population. Malaysia's market shows strong potential with increasing health awareness and product innovations, while Vietnam's market is characterized by its young, dynamic consumer base and growing retail infrastructure. Thailand's market demonstrates strong growth potential, particularly in the premium segment, with consumers increasingly seeking healthier beverage alternatives. Each of these markets presents unique opportunities and challenges, shaped by local preferences, distribution networks, and evolving consumer behaviors.

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

Top Companies in Asia-Pacific Ready to Drink Tea Market

Leading companies in the market are driving growth through continuous product innovation and strategic expansion initiatives. Manufacturers are increasingly focusing on developing healthier variants with reduced sugar content and natural ingredients to meet evolving consumer preferences. Companies are strengthening their distribution networks through partnerships with retailers and expanding their presence across both traditional and modern trade channels. There is a notable trend towards sustainable packaging solutions, with many players transitioning to recyclable materials and eco-friendly alternatives. Operational agility is being enhanced through investments in advanced manufacturing facilities and supply chain optimization. Companies are also leveraging digital platforms and e-commerce channels to improve market reach and consumer engagement. The integration of functional ingredients and introduction of unique flavor combinations demonstrates the industry's commitment to product differentiation and value addition, particularly in the RTD tea segment.

Market Structure Shows Regional Leaders' Dominance

The Asia-Pacific RTD tea market exhibits a moderately fragmented structure with a mix of global beverage conglomerates and regional specialists. Local players maintain strong positions in their respective markets through a deep understanding of consumer preferences and established distribution networks. Major multinational companies are competing through extensive product portfolios and significant marketing investments, while regional players leverage their agility and market-specific expertise. The market is characterized by intense competition, with companies vying for market share through product differentiation and pricing strategies.

The industry has witnessed strategic consolidations as larger companies seek to expand their geographical presence and product offerings. Joint ventures and partnerships between international and local players are becoming increasingly common, combining global expertise with local market knowledge. Companies are also pursuing vertical integration strategies to maintain better control over their supply chains and ensure product quality. The market structure is evolving with the entry of new players, particularly those focusing on premium tea and specialized RTD tea segments, leading to increased competition and innovation in the sector.

Innovation and Sustainability Drive Future Success

For established players to maintain and expand their market share, a focus on product innovation and sustainability initiatives is crucial. Companies need to invest in research and development to create unique product offerings that align with changing consumer preferences and health trends. Building strong distribution networks while maintaining product quality and consistency across markets is essential. Established players should also focus on developing strong brand identities and maintaining consumer trust through transparent practices and quality assurance.

New entrants and challenger brands can gain ground by identifying and serving niche market segments with specialized products. Success factors include developing innovative flavors and functional benefits that differentiate their offerings from established brands. Companies must also consider potential regulatory changes regarding sugar content and packaging materials, adapting their strategies accordingly. Building relationships with key distribution partners and investing in digital marketing capabilities will be crucial for market penetration. The ability to quickly respond to changing consumer preferences while maintaining operational efficiency will be key to long-term success in this dynamic packaged beverage market.

Asia-Pacific Ready to Drink Tea Industry Leaders

-

Ito En, Ltd.

-

JDB Group

-

Suntory Holdings Limited

-

Tingyi (Cayman Islands) Holding Corporation

-

Uni-President Enterprises Corp.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- November 2023: The Coca-Cola Company's brand ChaiChun brought exquisite teas to Delhi with its new store, The ChaiChun Store, expanding its business.

- September 2022: Ayataka, a brand of iced green tea produced by Coca-Cola, has announced the release of its new Ayataka Cafe Matcha Latte which will hit stores across Japan

- June 2021: Sermsuk launched “est Play plus vitamins B6 and B12”, a vitamin-infused carbonated soft drink (CSD) certified by “Healthier Choice” nutritional logo.

Asia-Pacific Ready to Drink Tea Market Report Scope

Green Tea, Herbal Tea, Iced Tea are covered as segments by Soft Drink Type. Aseptic packages, Glass Bottles, Metal Can, PET Bottles are covered as segments by Packaging Type. Off-trade, On-trade are covered as segments by Distribution Channel. Australia, China, India, Indonesia, Japan, Malaysia, South Korea, Thailand, Vietnam are covered as segments by Country.

Soft Drink Type

| Green Tea |

| Herbal Tea |

| Iced Tea |

| Other RTD Tea |

Packaging Type

| Aseptic packages |

| Glass Bottles |

| Metal Can |

| PET Bottles |

Distribution Channel

| Off-trade | Convenience Stores |

| Online Retail | |

| Supermarket/Hypermarket | |

| Others | |

| On-trade |

Country

| Australia |

| China |

| India |

| Indonesia |

| Japan |

| Malaysia |

| South Korea |

| Thailand |

| Vietnam |

| Rest of Asia-Pacific |

| Soft Drink Type | Green Tea | |

| Herbal Tea | ||

| Iced Tea | ||

| Other RTD Tea | ||

| Packaging Type | Aseptic packages | |

| Glass Bottles | ||

| Metal Can | ||

| PET Bottles | ||

| Distribution Channel | Off-trade | Convenience Stores |

| Online Retail | ||

| Supermarket/Hypermarket | ||

| Others | ||

| On-trade | ||

| Country | Australia | |

| China | ||

| India | ||

| Indonesia | ||

| Japan | ||

| Malaysia | ||

| South Korea | ||

| Thailand | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

Need A Different Region or Segment?

Customize Now

Market Definition

- Carbonated Soft Drinks (CSDs) - Carbonated soft drinks (CSDs) refer to non-alcoholic beverages that are carbonated and typically flavored, containing dissolved carbon dioxide to create effervescence. These beverages commonly include cola, lemon-lime, orange, and various fruit-flavored sodas. Marketed in cans, bottles, or fountain dispense.

- Juices - We have considered packaged juices which encompass non-alcoholic beverages derived from fruits, vegetables, or a combination thereof, processed and sealed in various packaging formats such as bottles, cartons, or pouches. Excluding fresh juices, this market segment involves commercially prepared and preserved juices, often with added preservatives and flavors.

- Ready-to-Drink (RTD) Tea and RTD Coffee - Ready-to-Drink (RTD) tea and RTD coffee are pre-packaged, non-alcoholic beverages that are brewed and prepared for consumption without further dilution. RTD tea typically includes various tea varieties, infused with flavors and sweeteners, and comes in bottles, cans, or cartons. Similarly, RTD coffee involves pre-brewed coffee formulations, often mixed with milk, sugar, or flavorings, and is conveniently packaged for on-the-go consumption.

- Energy Drinks - Energy drinks are non-alcoholic beverages formulated to provide a quick boost of energy and alertness. Whereas, sports drinks are beverages designed to hydrate and replenish electrolytes, particularly after physical exertion, exercise, or intense activity

| Keyword | Definition |

|---|---|

| Carbonated Soft Drinks | Carbonated soft drinks (CSDs) are a combination of carbonated water and flavouring, sweetened by sugar or a non-sugar sweeteners. |

| Standard Cola | Standard Cola is defined as the original flavor of cola soda. |

| Diet Cola | A cola-based soft drink containing no or low amounts of sugar |

| Fruit Flavored Carbonates | A carbonated beverage prepared from fruit juice/fruit flavor with carbonated water and containing sugar, dextrose, invert sugar or liquid glucose either singly or in combination. It may contain peel oil and fruit essences. |

| Juice | Juice is a drink made from the extraction or pressing of the natural liquid contained in fruit and vegetables. |

| 100% Juice | Fruit/vegetable juice made from fruit in the form of its juice with no water added to make up the volume. It is not permitted to add sugars, sweeteners, preservatives, flavourings or colourings to fruit juice. |

| Juice Drinks (up to 24% Juice) | Fruit/vegetable juice drinks with up to 24% fruits/vegetable extract. |

| Nectars (25-99% Juice) | Juices that can have between 25 and 99% of fruit, with the minimum legal limits defined depending on the type of fruit |

| Juice concentrates | Juice Concentrates are those form of juices when most of this liquid is removed resulting in a thick, syrupy product known as juice concentrate. |

| RTD Coffee | Packaged coffee beverages that are sold in a prepared form and are ready for consumption at the time of purchase. |

| Iced Coffee | An iced coffee is a cold version of coffee, usually a combination of hot espresso and milk with ice added to it. |

| Cold Brew Coffee | Cold brew also called cold water extraction or cold pressing is made by steeping ground coffee in room-temperature water for several hours. |

| RTD Tea | Ready-to-drink (RTD) tea is a packaged tea product ready for immediate consumption without brewing or preparation |

| Iced Tea | Ice tea or iced tea is a drink made from tea without milk but with sugar and sometimes fruit flavourings, drunk cold. |

| Green Tea | Green tea is a tea beverage which promotes mental alertness, relieving digestive symptoms and promoting weight loss. |

| Herbal Tea | Herbal tea beverages are made from the infusion or decoction of herbs, spices, or other plant material in hot water. |

| Energy Drink | A type of drink containing stimulant compounds, usually caffeine, which is marketed as providing mental and physical stimulation. They may or may not be carbonated and may also contain sugar, other sweeteners, or herbal extracts, among numerous possible ingredients. |

| Sugar-free or Low-calories Energy Drinks | Sugar-free or Low-calories Energy Drinks are sugar-free, artificially sweetened energy drinks with few or no calories. |

| Traditional Energy Drink | Traditional Energy Drinks are functional soft drinks containing ingredients designed to boost the consumer's energy. |

| Natural/Oraganic Energy Drinks | Natural/Organic energy drinks are energy drinks free of artificial sweeteners and synthetic colorings. Instead, they contain naturally derived ingredients such as green tea, yerba mate, and botanical extracts. |

| Energy Shots | A small but highly concentrated energy drink that contains large amounts of caffeine and/or other stimulants. The quantity is comparatively smaller compared to energy drinks. |

| Sports Drink | Sports drinks are beverages designed specifically for the rapid supply of fluid, carbohydrates, and electrolytes before, during or after exercise. |

| Isotonic | Isotonic drinks contain similar concentrations of salt and sugar as in the human body, and are designed to quickly replace fluids lost during exercise but with an increase of carbohydrate. |

| Hypertonic | Hypertonic drinks have a higher concentration of salt and sugar than the human body. They are best drunk after exercise as it is important to replace glycogen levels quickly after exercise. |

| Hypotonic | Hypotonic drinks are designed to quickly replace fluids lost during exercise. They have very low carbohydrate content and a lower concentration of salt and sugar than the human body. |

| Electrolyte-Enhanced Water | Electrolyte water is water infused with electrically-charged minerals, such as sodium, potassium, calcium, and magnesium. |

| Protein-based Sport Drinks | Protein-based sports drinks are those sports drinks which has added protein in it that will improve performance and reduce muscle protein breakdown. |

| On-Trade | The on-trade refers to places that sell beverages for immediate consumption on the premises like bars, restaurants, and pubs |

| Off-Trade | Off-trade usually means places like liquor stores, supermarkets and other places where you don't consume the beverage right away. |

| Convenience Store | A retail business that provides the public with a convenient location to quickly purchase a wide variety of consumable products and services, generally food and gasoline. |

| Specialty store | A specialty store is a shop/store that carries a deep assortment of brands, styles, or models within a relatively narrow category of goods |

| Online Retail | Online retail is a type of eCommerce whereby a business sells goods or services directly to consumers from a website. |

| Aseptic Packaging | Aseptic packaging refers to the filling of a cold, commercially sterile product under sterile conditions into a presterilized container and closure under sterile conditions to form a seal that effectively excludes microorganisms. These includes tetra packs, cartons, pouches etc. |

| PET Bottle | PET bottle means a bottle made of polyethylene terephthalate. |

| Metal Cans | Metal containers made of aluminum or tin- plated or zinc-plated steel, which are commonly used for packaging food, beverages or other products. |

| Disposable Cups | Disposable Cup means a cup or other container designed for single use to serve beverages, such as water, cold drinks, hot drinks and alcoholic beverages. |

| Gen Z | A way of referring to the group of people who were born in the late 1990s and early 2000s. |

| Millenial | Anyone born between 1981 and 1996 (ages 23 to 38 in 2019) is considered a Millennial |

| Taurine | Taurine is an amino acid that supports immune health and nervous system function. |

| Bars & Pubs | It is a drinking establishment licensed to serve alcoholic drinks for consumption on the premises. |

| Café | It is a foodservice establishment serving refreshments (mainly coffee) and light meals. |

| On the go | It means doing / dealing with while busily engaged with something and not diverting plans in order to accommodate. |

| Internet Penetration | The Internet Penetration Rate corresponds to the percentage of the total population of a given country or region that uses the Internet. |

| Vending Machine | A machine that dispenses small articles such as food, drinks, or cigarettes when a coin or token is inserted |

| Discount store | A discount store or discounter offers a retail format in which products are sold at prices that are in principle lower than an actual or supposed "full retail price". Discounters rely on bulk purchasing and efficient distribution to keep down costs. |

| Clean Label | Clean label on the beverage market are drinks that are made from few ingredients of natural origin and are not or only slightly processed. |

| Caffeine | An alkaloid compound which is a stimulant of the central nervous system. It is mainly used recreationally, as a mild cognitive enhancer to increase alertness and attentional performance. |

| Extreme sport | Action sports, adventure sports or extreme sports are activities perceived as involving a high degree of risk. |

| High-intensity interval training | It incorporates several rounds that alternate between several minutes of high intensity movements to significantly increase the heart rate to at least 80% of one's maximum heart rate, followed by short periods of lower intensity movements. |

| Shelf life | The length of time for which an item remains usable, fit for consumption, or saleable. |

| Cream Soda | Cream soda is a sweet soft drink. Generally flavored with vanilla and based on the taste of an ice cream float |

| Root Beer | Root beer is a sweet North American soft drink traditionally made using the root bark of the sassafras tree Sassafras albidum or the vine of Smilax ornata as the primary flavor. Root beer is typically, but not exclusively, non-alcoholic, caffeine-free, sweet, and carbonated. |

| Vanilla Soda | A carbonated soft drink flavoured with vanilla. |

| Dairy-Free | A product that does not contain any milk or milk products from cows, sheep or goats. |

| Caffeine-Free Energy Drinks | Caffeine-free energy drinks rely on other ingredients to boost the energy. Popular choices include amino acids, B vitamins, and electrolytes. |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated reports, custom consulting assignments, databases & subscription platforms

Get More Details On Research Methodology

Download PDF